.webp)

Late payments are a persistent challenge for U.S. businesses, with 39% of B2B invoices paid late, slowing down revenue collection and straining cash flow. For businesses struggling with these delays, notes receivable offer a formal, legally binding solution.

Unlike regular invoices, notes receivable provide a structured repayment plan that ensures timely payment, helping businesses stay on top of cash flow. Additionally, 91% of mid-sized businesses using automated systems for managing receivables report improved cash flow by speeding up payment cycles and reducing manual errors.

This blog will explore what notes receivable are, how they work, and why they matter to your business's financial health. We’ll also explore practical examples and key strategies for managing accounts receivable notes effectively, helping you stay on top of payments and optimize cash flow. Let’s begin.

Notes receivable are formal agreements where a company lends money or extends credit to a customer through a promissory note. This document legally binds the customer to repay the debt within a set period, often with interest.

Key aspects of notes receivable include:

Businesses often use notes receivable for larger purchases or employee cash advances. Notes receivable can be sold to third parties or used to secure financing, helping businesses manage cash flow more effectively.

Now that we've covered the basics, let's explore how notes receivable differ from regular accounts receivable.

While both notes receivable and accounts receivable represent amounts owed to a business, they differ significantly in terms of structure, payment terms, and legal enforceability. Here’s a comprehensive table of the key differences:

Understanding which type of receivable applies to your business helps you manage credit and forecast cash flow with greater accuracy.

With that distinction in mind, let’s take a closer look at the key components that make up a notes receivable.

.webp)

Notes receivable are formal agreements to ensure timely payments, often including both a repayment plan and interest. Here’s a breakdown of the key elements:

These components make notes receivable a more secure and structured financial resource than standard accounts receivable.

VJM Global simplifies the management of notes receivable by providing accurate, outsourced accounting services. We ensure proper classification, timely interest tracking, and full compliance, so you can focus on growing your business. Get in touch today.

Understanding these components sets the stage for creating a proper note. Here’s a simple template you can use.

For businesses that accept promissory notes as a form of payment, having a clear, standardized template is essential. Below is a template that can help you create a legally binding note for your transactions:

[Principal value]

[City, Province or Territory, Agreement date]

For value received, the undersigned, [Name of maker], agrees to pay to [Name of Payee], the principal sum of [Principal value], with interest at the rate of [Interest rate]% per annum on the outstanding balance. The interest will accrue from the date of this agreement until the principal is paid in full.

The principal amount and interest are payable in lawful currency of the United States at [City and Province or Territory], as specified by written notice from the holder of the note to the maker, on the specified date. The payment terms are as follows:

Upon demand, not later than [term length]

[Address of maker]

[Signature of maker]

[Seal of the maker]

[Signature of payee]

[Seal of payee or company]

This template provides a foundation for creating a formal note receivable that both the business and customer can rely on.

Also Read: Comprehensive Guide to Accounts Receivable Journal Entries

Now that you have the template, let's walk through some real-world examples to see how notes receivable are used.

Notes receivable are commonly used when businesses formalize an agreement for repayment with specific terms. Here are three examples highlighting different scenarios:

If a restaurant purchases $25,000 of new equipment on credit from a supply store, the supplier normally expects payment within 60 days.

Since the restaurant is newly opened and struggling with cash flow, it requests an extension. The supplier agrees and issues a one-year promissory note at an interest rate of 8%.

Journal Entry at Issuance:

Journal Entry at Payment (Maturity):

*Interest = $25,000 × 8% = $2,000 over one year.

Hence, a standard invoice can be replaced with a promissory note, giving the restaurant more time to pay while securing the supplier’s right to collect interest.

A customer buys $10,000 worth of goods on credit and issues a 90-day promissory note with 5% annual interest. This shifts the transaction from accounts receivable to notes receivable.

Journal Entry at Issuance:

Journal Entry at Payment (Maturity):

The above example is one of the most common uses of notes receivable: converting a credit sale into a legally binding repayment with interest.

A company lends $5,000 to an employee, formalized by a 1-year note at 6% interest.

Journal Entry at Issuance:

Journal Entry at Payment (Maturity):

Hence, notes receivable can also arise from internal loans, not just customer transactions.

A business makes an advance payment of $3,000 to a vendor, secured with a promissory note to guarantee repayment.

Journal Entry at Issuance:

Journal Entry at Repayment:

Businesses can thus use notes receivable to protect advance payments made to vendors.

A customer purchases equipment worth $12,000 but prefers to pay in monthly installments with interest. The arrangement is recorded as notes receivable.

Journal Entry at Issuance:

Journal Entry at First Installment:

The above example is a case of structured repayment, where the business receives both principal and interest over time instead of a single lump sum.

These examples show how notes receivable formalize transactions and provide structured repayment plans for various situations, from trade credit to employee loans.

Struggling to manage complex notes receivable and maintain cash flow? VJM Global’s expert accounting services help streamline the process, ensuring accurate record-keeping and efficient repayment tracking, so your business can focus on growth and success.

Next, let’s explore how to record and manage these notes in your accounting system.

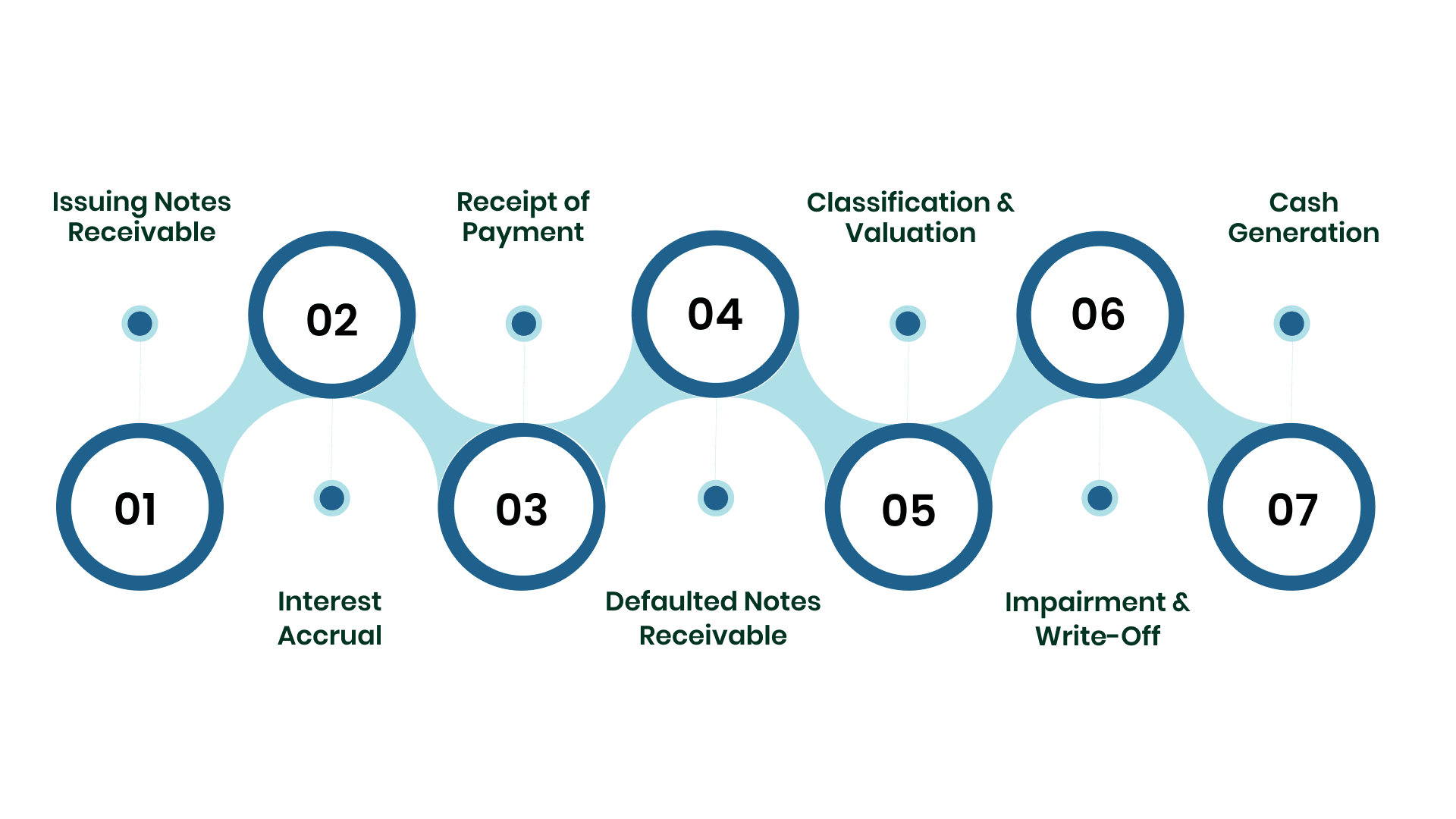

Recording notes receivable ensures businesses track amounts owed and classify them as assets on financial statements. These formal agreements define structured repayment schedules.

Accurate accounting for notes receivable ensures that your financial statements reflect your true assets, supports effective cash flow management, and safeguards against potential credit losses.

Also Read: Accounts Receivable Management Best Practices Guide

Finally, let’s explore how VJM Global can help simplify the entire process, ensuring your notes receivable are well-managed.

Tracking and accounting for notes receivable can be time-consuming. VJM Global helps businesses simplify this process, ensuring accuracy, compliance, and better cash flow management. Key benefits include:

Ensure your notes receivable are recorded accurately and your cash flow remains predictable with VJM Global.

Notes receivable serve as formal agreements that secure repayment and provide businesses with predictable cash flow. Proper recording, interest tracking, and classification ensure accurate financial statements and reduce the risk of uncollectible debts.

Handling defaults, impairments, and write-offs systematically protects both revenue and asset integrity. Using notes receivable strategically can also generate immediate cash through pledging, factoring, or assignment, supporting operational needs and growth.

Take control of your receivables and streamline your accounting process with VJM Global’s solutions, designed to simplify notes management and strengthen cash flow reliability. Contact us today.

Notes receivable are formal promises from a customer to pay you a specific amount, usually with interest, by a certain date. They’re a step up from regular invoices.

When you receive a note, you debit the Notes Receivable account and credit either Sales, Cash, or Accounts Receivable, depending on the transaction. This tracks what’s owed.

You record earned interest by debiting Interest Receivable and crediting Interest Income. This shows the interest you’ve earned but haven’t collected yet.

Interest is usually calculated as Principal × Rate × Time. Make sure the time period matches the note’s term, like months or years.

The maturity date is the day the full principal and any interest must be paid. It marks the end of the note’s term.