%20(2).webp)

Lease accounting is a significant area of financial reporting, particularly for businesses that lease property or equipment. Over the years, both the International Financial Reporting Standards (IFRS) and US Generally Accepted Accounting Principles (US GAAP) have evolved to offer clearer guidance on how to account for leases. For businesses operating under US GAAP lease accounting, understanding the intricacies of lease accounting, particularly how it differs from IFRS, is essential for accurate financial reporting.

This blog provides an overview of US GAAP lease accounting standards, focusing on ASC 842 principles, key distinctions from IFRS 16, and actionable implementation steps for companies.

Key Takeaways:

Lease Accounting Standards are the set of guidelines that companies must follow when accounting for leases in their financial records. These standards ensure that lease transactions are accurately represented in the financial statements, promoting transparency and comparability across organizations. They outline how leases should be classified, measured, and disclosed.

The two main types of leases are:

The classification of leases impacts the reporting of expenses, cash flows, and depreciation during the lease term. Under updated standards, such as ASC 842 and IFRS 16, most leases are now recognized on the balance sheet. Both a right-of-use asset and a lease liability are recorded based on the present value of future lease payments.

These standards aim to improve the accuracy of financial statements, addressing issues with previous guidelines, such as ASC 840, which permitted certain leases to remain off-balance sheet. The Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) introduced these updates to make financial reporting more consistent across different industries and countries.

Other factors, such as the incremental borrowing rate, lease modifications, and initial direct costs, also influence how lease transactions are measured. Whether a company is public, private, or a government entity, adhering to lease accounting standards is vital for accurate reporting and compliance with regulatory requirements.

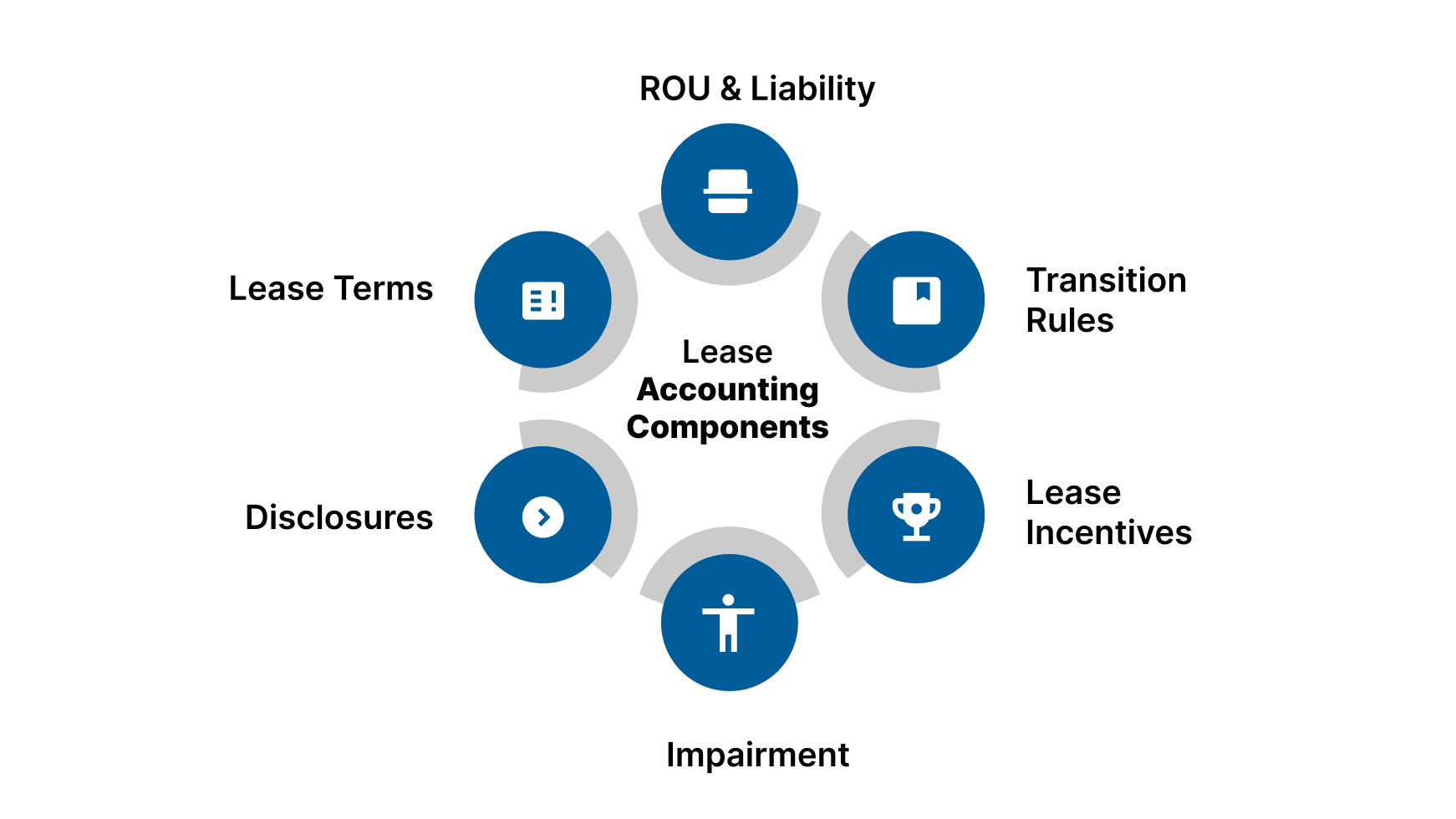

To understand how these standards work in practice, let’s break down their key components.

Lease accounting standards are crucial for determining how organizations recognize, measure, and report lease transactions in their financial statements. These standards help ensure that both lessees and lessors accurately classify leases, account for lease agreements, and recognize their financial obligations.

In recent years, new standards like ASC 842 and IFRS 16 have introduced significant changes, particularly the requirement to record most leases on the balance sheet. Companies must also consider aspects such as remeasurement, lease incentives, and impairment when assessing the financial impact of their leases.

Here are the main components of lease accounting standards:

These components are essential for ensuring that companies report their leases in a consistent, transparent way, adhering to regulatory requirements. As lease accounting standards evolved, the shift to ASC 842 under US GAAP brought significant changes, especially in how leases are presented on financial statements. Let’s explore how this shift has reshaped lease reporting and its impact on organizations.

Historically, under US GAAP lease accounting, leases were classified as either operating leases or capital leases. Capital leases were recorded on the balance sheet, while operating leases were disclosed in the notes to the financial statements. The issue with this model was that operating leases, which represented a significant liability, were often not reflected on the balance sheet, leading to an incomplete financial picture for investors and stakeholders.

In 2016, the Financial Accounting Standards Board (FASB) introduced ASC 842, a new standard for lease accounting. The primary goal of ASC 842 was to bring most leases onto the balance sheet, addressing concerns regarding transparency and comparability.

This marked a major change in how companies report lease obligations. Let’s take a closer look at the key principles introduced under ASC 842.

ASC 842, the latest update to US GAAP lease accounting, introduces significant changes for both lessees and lessors. It focuses on the recognition, measurement, and presentation of leases in financial statements, ensuring more transparency in financial reporting.

Below are the key aspects of lessee and lessor accounting under ASC 842:

Under ASC 842, all leases must be classified as either finance leases or operating leases. The lessee must recognize a right-of-use (ROU) asset and a corresponding lease liability for both finance and operating leases. This was a major shift from previous US GAAP lease accounting rules, where only finance leases were recognized on the balance sheet.

Finance leases are accounted for by the lessee as both an asset and a liability on the balance sheet. The ROU asset is amortized, and the lease liability is settled over time with interest expense recognized in the income statement.

The accounting for lessors under ASC 842 is similar to previous US GAAP lease accounting guidance. A lease can be classified as a sales-type lease, direct financing lease, or operating lease. The classification depends on the transfer of risks and rewards related to ownership. If the lease meets the criteria of a sales-type or direct financing lease, the lessor recognizes the lease receivable and derecognizes the leased asset.

While ASC 842 provides clear guidance on US GAAP lease accounting, it's essential to understand how it compares to the IFRS 16 standard. Let's dive into the key differences between these two accounting frameworks and how they impact financial reporting.

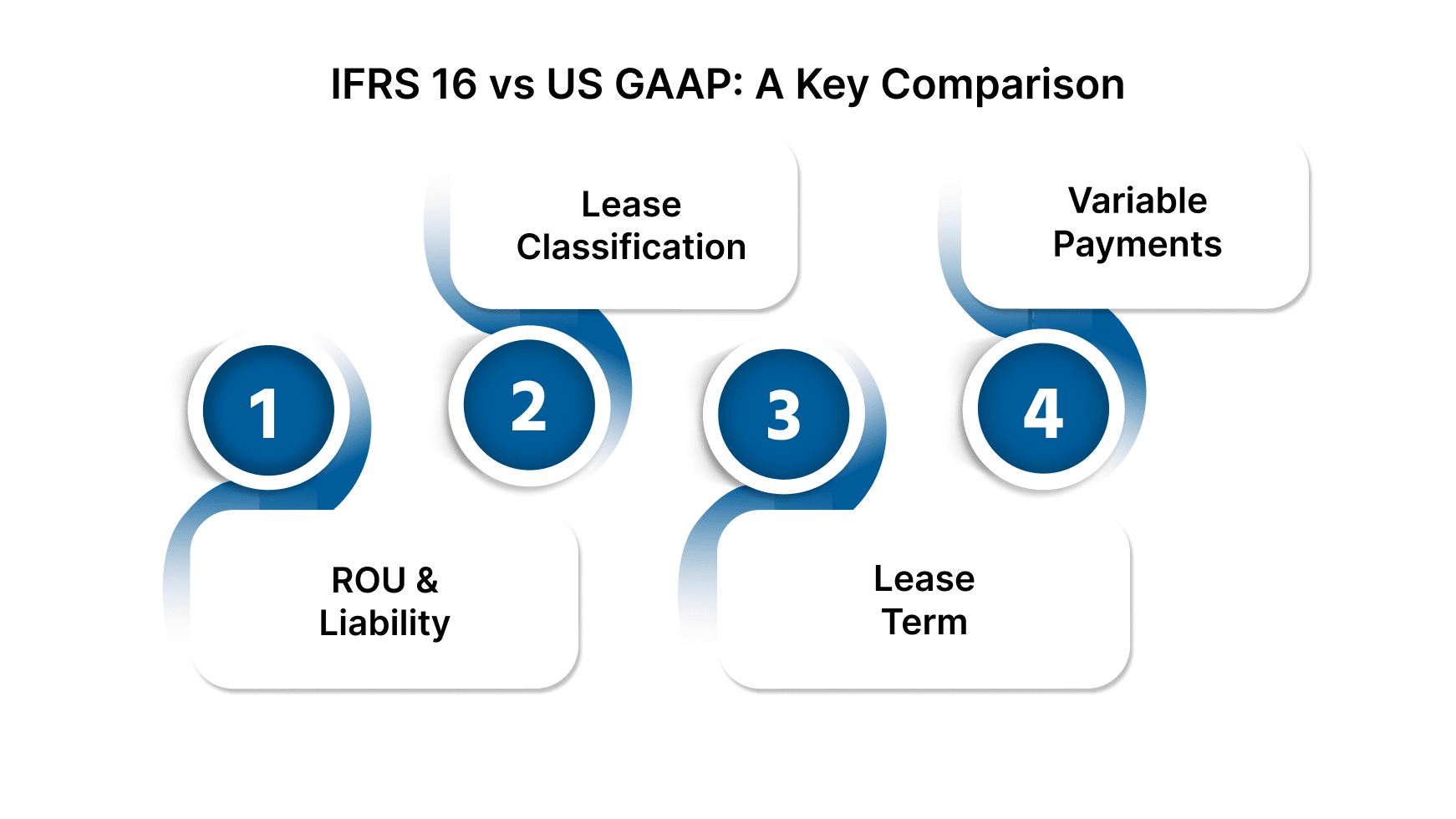

One of the main points of confusion for businesses operating internationally is the difference between IFRS 16 and US GAAP lease accounting. Both standards aim to bring leases onto the balance sheet but approach the implementation differently.

Both ASC 842 and IFRS 16 require lessees to recognize a right-of-use asset and lease liability. However, IFRS 16 mandates that lessees recognize these for all leases, without exception, while US GAAP lease accounting makes a distinction between finance and operating leases. In essence, IFRS 16 eliminates the distinction between operating and finance leases, requiring lessees to recognize the ROU asset and lease liability for all leases, regardless of classification.

As mentioned, finance leases under US GAAP are similar to capital leases in the old system, and these leases are accounted for with separate recognition of interest and amortization expenses. For operating leases, only one lease expense is recognized, typically a straight-line amount over the lease term.

In contrast, under IFRS 16, there is no concept of operating leases, meaning all leases, regardless of their length or type, are treated similarly to finance leases under US GAAP. This results in a greater recognition of liabilities on the balance sheet under IFRS 16 compared to US GAAP, particularly for companies with a large number of operating leases.

IFRS 16 requires lessees to consider the non-cancellable period of the lease, along with any extension options that are "reasonably certain" to be exercised. This can result in a longer lease term and, consequently, higher lease liabilities and ROU assets.

Under US GAAP lease accounting, lessees must also consider the lease term and any renewal options. However, US GAAP is more conservative regarding the assumption that renewal options will be exercised, which could lead to lower lease liabilities and ROU assets compared to IFRS 16.

Another key difference is the treatment of variable lease payments. Under IFRS 16, variable payments that depend on an index or rate are included in the calculation of lease liabilities. In contrast, US GAAP lease accounting only includes variable payments that depend on an index or rate when the variability is predictable.

After exploring the key differences between IFRS 16 and US GAAP, let's focus on the specific considerations businesses must address under US GAAP lease accounting. This will help ensure compliance and accurate financial reporting.

ASC 842 brings key changes for businesses. It affects how leases are classified and reported. Companies must adapt their processes and review lease details carefully. Here are some important points to keep in mind. Let’s explore the key considerations that organizations need to address to ensure proper lease classification and compliance.

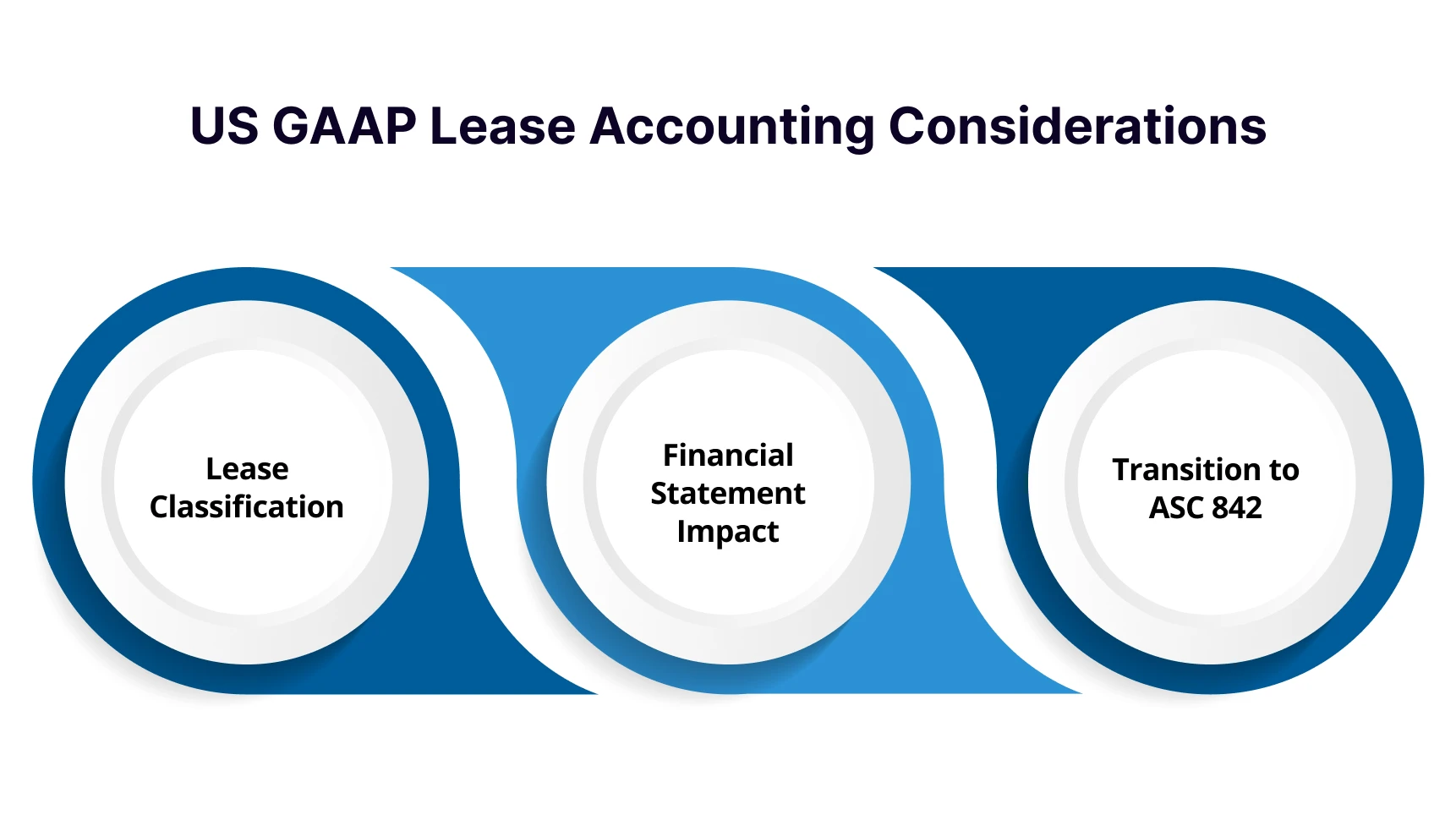

Under ASC 842, businesses need to carefully evaluate whether a lease should be classified as a finance lease or an operating lease. This classification will significantly impact how the lease is accounted for in the financial statements. It is crucial for businesses to review lease contracts thoroughly and ensure the correct classification based on the specific criteria outlined in the standard.

One of the most significant changes under ASC 842 is that it brings operating leases onto the balance sheet. This means that businesses that previously had operating leases off the balance sheet now have to account for them as ROU assets and lease liabilities. This can impact financial ratios, such as debt-to-equity and return on assets, which may be of concern for businesses that rely heavily on leases.

For businesses transitioning to ASC 842 from the old lease accounting standard (ASC 840), there are some challenges. The transition requires careful analysis of existing leases and the application of new accounting policies. Companies may need to modify their internal systems to comply with the new reporting requirements. The transition period can be particularly challenging for businesses with a large portfolio of leases.

Understanding the practical implications of US GAAP is only part of the picture, global businesses also need to weigh how it compares to IFRS 16 when choosing the right path forward.

Let’s explore which framework might serve businesses better.

While IFRS 16 and US GAAP both aim to increase transparency in lease accounting, there are notable differences in the way they treat leases. For businesses that operate internationally or engage in cross-border leasing, understanding the distinctions between these standards is crucial.

Ultimately, the choice between IFRS 16 and US GAAP will depend on the company's geographical location, the complexity of its lease portfolio, and its accounting and reporting needs. Understanding these differences is just the first step, let’s now explore how businesses can effectively implement US GAAP lease accounting in practice.

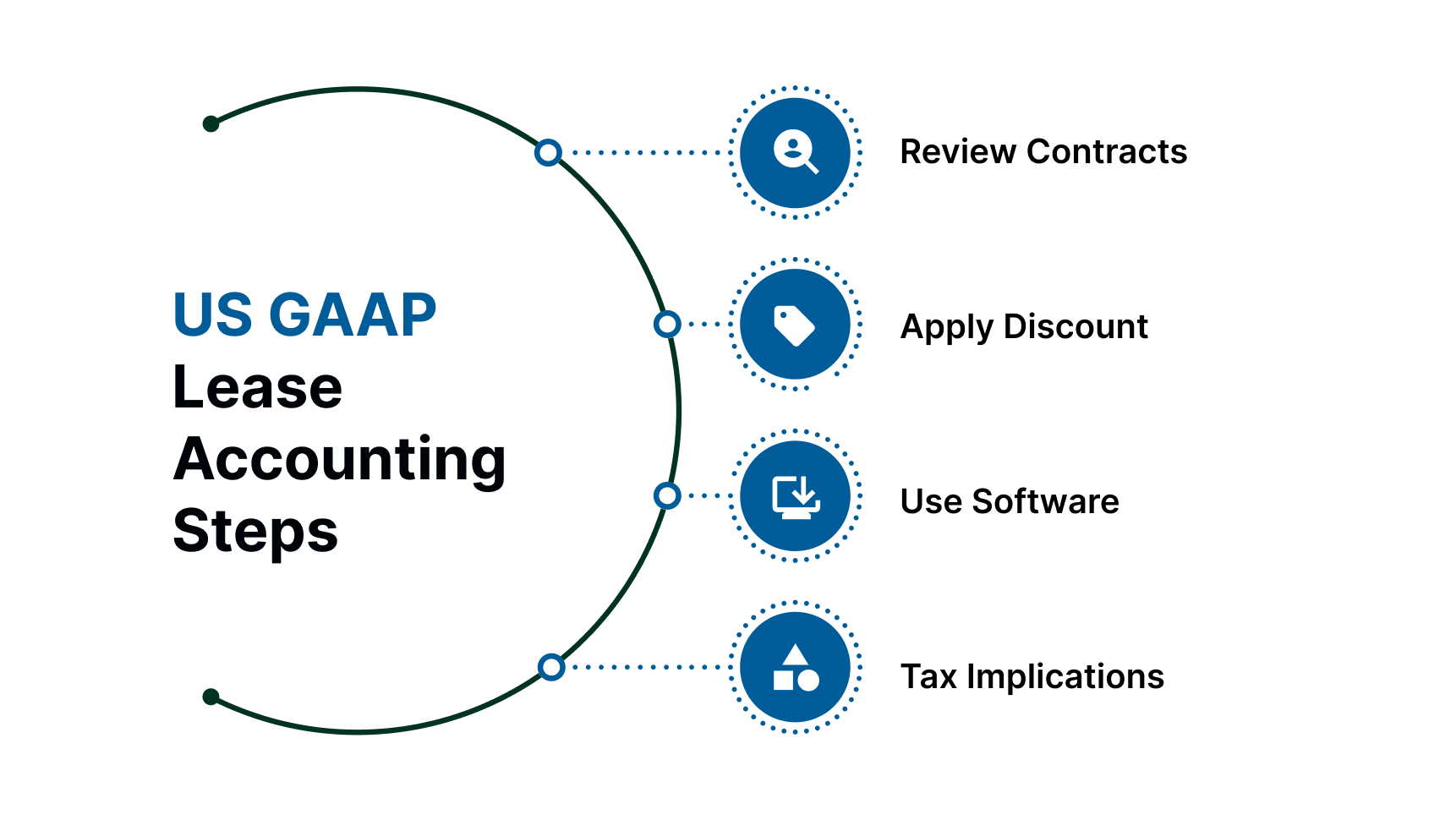

Implementing US GAAP lease accounting isn’t just about compliance, it’s about transforming how lease obligations are captured, measured, and reported. To ensure a smooth transition and maintain accuracy, businesses must follow a few key practical steps. Here’s what to prioritize as you align with the new standards:

Adapting to the new US GAAP lease accounting standards, particularly ASC 842, can be complex for businesses. With the introduction of significant changes, including the recognition of operating leases on the balance sheet and the classification of leases as either finance or operating, companies must adjust their financial reporting practices. This can be a challenge, especially for organizations with a large portfolio of leases or those operating internationally.

VJM Global partners with businesses to navigate these changes, ensuring that they comply with the latest standards while minimizing the impact on their financial performance.

Here's how VJM Global supports businesses in adapting to US GAAP lease accounting:

With the evolving nature of US GAAP lease accounting standards, partnering with VJM Global ensures that your business stays compliant, efficient, and ready for future growth.

Ready to optimize your lease accounting processes? Connect with us today and learn how our experts can help streamline your transition to ASC 842 while maintaining financial accuracy.

Want to Deepen Your Accounting Strategy?

Check out our other resources:

Finance leases are recorded on the balance sheet with both an asset and a liability. Operating leases also appear on the balance sheet but with a single straight-line lease expense. This distinction impacts how leases are treated in financial statements.

ASC 842 requires operating leases to be brought onto the balance sheet. This increases the transparency of liabilities and assets. It may affect financial ratios and require changes to internal systems.

A lease is classified as a finance lease if it transfers ownership or includes a bargain purchase option. It can also be based on the lease term or the present value of payments. These criteria determine its accounting treatment.

IFRS 16 treats all leases as finance leases, regardless of type. US GAAP distinguishes between finance and operating leases. This affects how payments are recorded and reported.

VJM Global provides a thorough lease portfolio review and accurate implementation of ASC 842. They offer ongoing support for remeasurement and lease modifications. Their expertise helps businesses stay compliant and efficient.