Managing long-term projects often presents the challenge of mismatched timing between the completion of work and the receipt of payments. This discrepancy can make it difficult to accurately report revenue, justify profits, and effectively plan cash flow. For contracts that extend over several months or even years, a more reliable method is needed to align financials with the progress of the work. The percentage of completion accounting method offers a practical solution to this issue.

Most general and speciality commercial contractors use PoCM to report revenue on multi-month projects. This accounting approach lets you recognize revenue as a project progresses, not just when it's finished. It gives a more accurate view of your earnings, especially in construction, engineering, or custom manufacturing industries, where delivery takes time and every phase counts.

In this blog, you’ll see how it works, when to use it, and how it can give you better control over your financial reporting.

You use the percentage of completion accounting method to recognize revenue and costs during long-term contracts, typically those extending beyond one accounting period. This prevents revenue from piling up until the project ends and gives you a realistic financial snapshot.

This method allows U.S.-based businesses to recognize revenue and expenses as a project moves forward, providing a more accurate financial picture over the course of the contract. It is especially useful for U.S. companies working on long-term projects, where revenue and costs are tracked based on the progress made in completing the work.

You should use the percentage of completion accounting method as it provides a more accurate reflection of a project's financial status. It also matches revenue recognition with the progress of the work, and offers better financial visibility for projects that span multiple periods.

The Percentage of Completion Accounting Method works best in situations where long-term contracts or projects span multiple accounting periods, such as construction or large-scale manufacturing. You should choose this method when the project has a clearly measurable progress and a reliable basis for estimating its completion.

The Percentage of Completion Accounting Method is a widely used approach for recognizing revenue and expenses over the life of long-term projects. While this method can be extremely beneficial for U.S.-based businesses, there are certain challenges to keep in mind. U.S. companies need to accurately estimate the completion percentage and project costs to avoid overestimating or underestimating revenue.

Following this process, you recognize income as work progresses, giving you steadier profits and timely insights into each contract’s financial health.

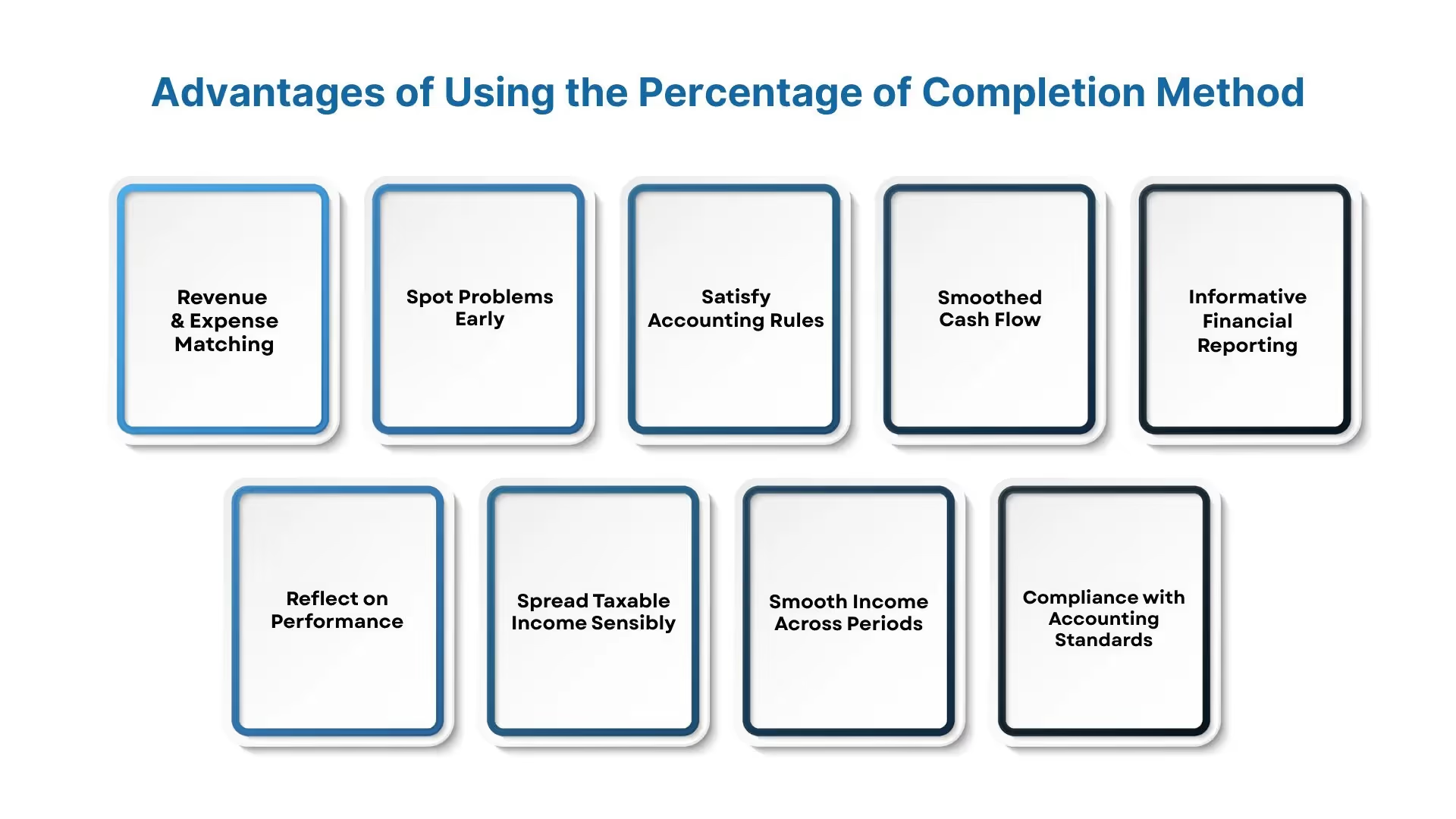

So, what do you gain by using this method? Let’s break down the practical benefits beyond just ticking compliance boxes.

The percentage of Completion Accounting Method provides a realistic view of income over multiple accounting periods. The benefits of using the percentage of completion method in accounting are as follows:

Also Read: Transfer Pricing: Cost Plus Method

Applying this method, you report revenue and costs as they accrue, offering you more predictable finances, enhanced transparency, and stronger credibility with stakeholders.

After learning the benefits, let’s examine the mechanics of how this method tracks and reports project progress.

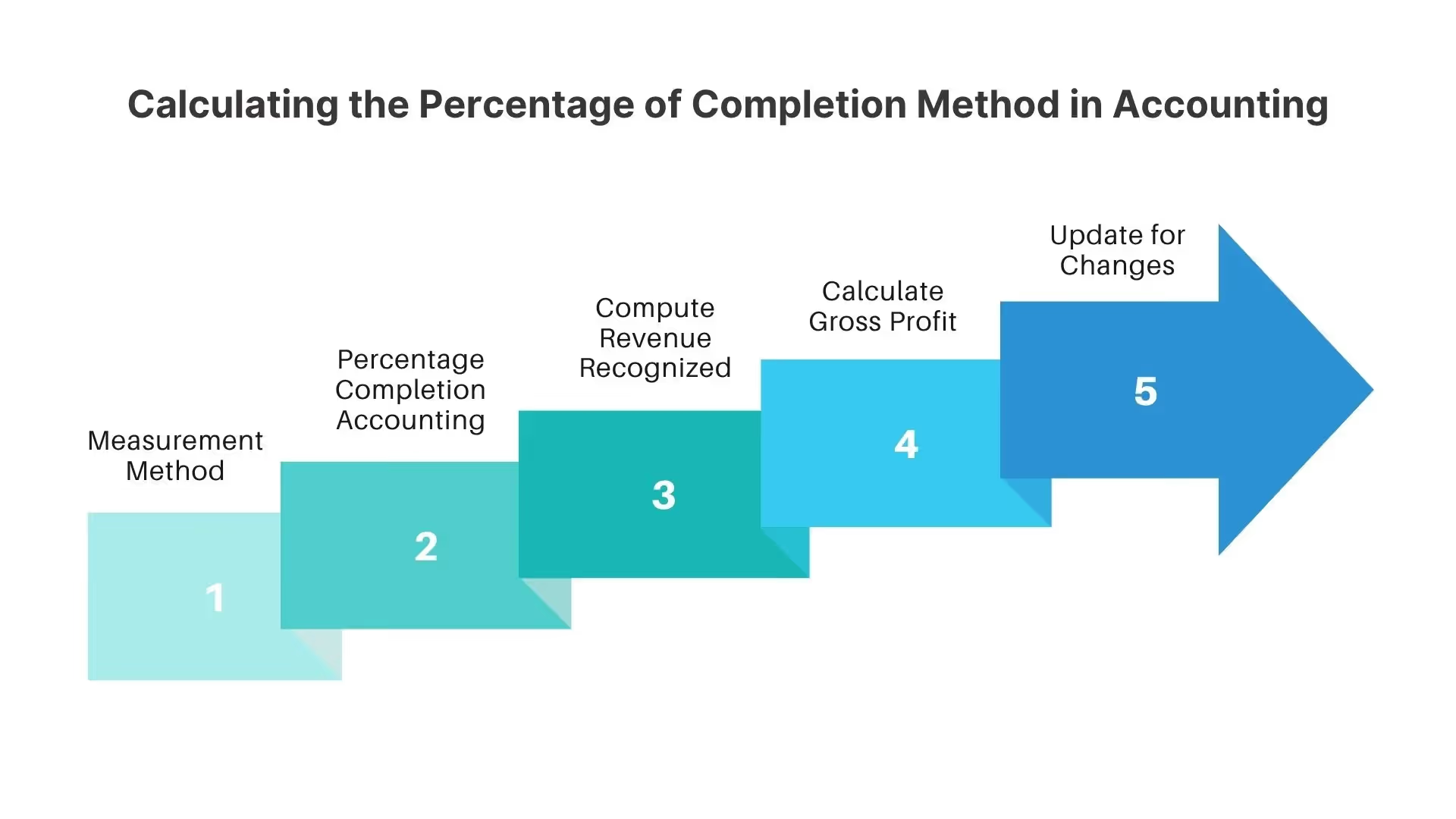

This Percentage of Completion Method Accounting is particularly beneficial for U.S. companies operating in sectors where projects span multiple fiscal periods. U.S. businesses can use this approach to reflect the ongoing progress of a contract, ensuring that financial reports more accurately match the actual work completed. You can follow a step-by-step process to recognize revenue as your project advances. Here's how you do it:

Divide your work into measurable stages, monthly or milestone-based, to record progress. These stages serve as the basis for revenue recognition.

Start by building a Work-in-Progress (WIP) schedule to track contract price (with approved change orders), total projected cost, actual costs to date, and billings submitted to the client. This schedule anchors your revenue calculation and shows any over- or under-billing.

Calculate progress with this formula:

Percent Complete = Costs to Date ÷ Total Estimated Cost

This tells you what portion of the job you’ve finished.

Recognize revenue by multiplying the completion percentage by the total contract value:

Revenue Recognized = Percent Complete × Contract Price

So if you're 50% done on a $120,000 contract, you record $60,000 in revenue.

Calculate over‑ or under‑billing as:

Revenue Recognized – Progress Billings

A positive result (underbilling) appears as an asset; a negative (overbilling) shows as a liability on your balance sheet.

Multiply the same percentage complete by the total estimated cost to calculate the current-period expense. Then, you subtract that from revenue to get profit.

Update costs, billing, and progress at the end of each reporting period, repeating steps 2 through 5 to keep financials current.

This method keeps your revenue reports in sync with the actual work done. You update estimates as work continues to maintain accuracy.

There’s more than one way to calculate progress. Let’s examine the different methods used to determine a project's progress.

The Percentage of Completion Accounting Method is ideal for U.S. businesses managing contracts that take more than one year to complete, such as large construction projects or multi-phase software development. For U.S. CPA firms handling these projects, this method ensures that revenue and costs are consistently recognized as the work progresses, reducing the risk of financial discrepancies. You can select the calculation method based on your project type and what you measure reliably:

Base completion on the costs spent compared to the total projected cost. This is the most widely used method, especially in construction, since costs mirror progress.

% Complete = Costs Incurred ÷ Total Estimated Cost

Example: If you’ve spent $40,000 out of an estimated $80,000 budget, you’re 50% complete.

Also Read: Cost Of Registration Of A Company In India

Measure progress by effort, like labor or machine hours, divided by total estimated hours. This works if hours relate closely to the outcome.

% Complete = Hours Worked ÷ Total Estimated Hours

Example: If your team logs 1,200 hours of an expected 2,400, you're at 50%.

Count the deliverables you’ve handed over out of the total in the contract. Use this when outputs are uniform and countable.

% Complete = Units Delivered ÷ Total Units

Example: If you finish 6 out of 10 identical houses, you’re 60% complete.

Under modern accounting frameworks (ASC 606 / IFRS 15), these two methods apply:

The comparison between the different methods of the percentage completion method is as follows:

Pick a method that aligns with how you track project progress and stick with it for similar contracts. This will give you consistent, clear revenue reporting as your work advances.

VJM Global helps software and service-based businesses apply the correct Percentage of Completion method, cost-to-cost, effort-based, or output-based, based on reliable project data. We handle revenue recognition and cost tracking across milestones, helping clients accurately report contract progress. Our accounting support has helped reduce revenue misstatements for clients managing multi-phase projects in India and abroad.

After learning your options, let’s run the numbers and calculate your revenue.

Follow a straightforward, structured process to calculate revenue recognition as your project progresses. The key steps of accounting for the percentage of completion calculation are:

Pick the approach that tracks your progress most accurately:

Choose your progress measure (cost-to-cost, efforts expended, or units delivered) and calculate:

Percent Complete = (Costs or Effort Incurred ÷ Total Estimated)

Then, apply it to both revenue and total expenses.

or:

= Hours Worked ÷ Total Estimated Hours

or:

= Units Delivered ÷ Total Units Expected

For example, if you’ve spent $4,000 out of an $8,000 estimated budget, you’re 50% complete.

Multiply the completion percentage by the total contract value:

Revenue to Date = Percentage Complete × Contract Price

For example, if your contract is $12,000 and you’re 50% complete, record $6,000 in revenue.

You may also compute the profit earned:

Gross Profit Earned = Revenue to Date – Costs Incurred to Date

For example, if that's $6,000 – $4,000, your gross profit is $2,000 this period.

Reassess total cost and revenue estimates each period. Adjust your calculations when estimates change.

By adhering to these steps, you align revenue and expenses with actual work. Companies using this method report revenue progressively, avoiding irregular spikes and offering clear financial insight.

This next step is about applying what you’ve calculated to your financial statements. Here’s how revenue and expenses show up on your books.

In the accounting percentage of completion method, you recognize revenue and expenses in line with project progress, with no waiting until final delivery.

Multiply the percentage completed by the total contract price to determine the revenue earned so far.

Example: If you've spent $4,000 of an $8,000 cost estimate (50%) on a $12,000 contract, you recognize $6,000 in revenue.

Use the formula:

Revenue to Date = % Complete × Contract Price

Expenses to Date = % Complete × Estimated Total Cost

Example: So if the contract totals $100,000 and you're 30% through, you recognize $30,000 revenue and expenses.

Apply the same percentage to recognize an equivalent portion of the total estimated cost:

Expenses to Date = Total Estimated Costs × Percent Complete

If the total estimated cost is $8,000 and the percent complete is 50%, you record $4,000 in expenses.

Also Read: ITC is not eligible for expenses incurred on CSR Activities.

Subtract amounts recognized in earlier periods from cumulative totals to determine what you book for revenue and expenses during this period.

Compare earned revenue to what you billed:

Example: If you’re 50% complete on a $100,000 contract but billed 60%, you've overbilled by $100,000 (10% × $100,000).

You match financial reports with actual performance by recording revenue and costs as work progresses. That clarity avoids sudden swings at the project end and keeps balance sheet figures current.

Before diving in, it’s worth knowing where things can go wrong. Here’s what to watch for and how to avoid common problems.

Using the percentage of completion accounting method, factor in its vulnerabilities and safeguards. By taking these steps, you maintain revenue accuracy, guard against misuse, and keep your cash flowing while using the percentage of completion accounting method.

Base revenue on cost and progress estimates. If you underestimate total costs or inflate progress, you risk misstating profits. You face the chance of recognizing too much revenue now and needing to reverse it later.

Because you book revenue based on estimates, inaccurate cost tracking or optimistic assumptions can lead to false profits or losses. Firms that misstate costs can skew earnings; infamously, Toshiba inflated profits before regulators stepped in.

Compare billed amounts with revenue recognized:

You might recognize revenue before cash arrives. That situation can strain liquidity, especially if clients delay payments or billing cycles stretch.

You must stick with one method: cost-to-cost, hours expended, or units delivered, and update estimates each period. Switching methods or failing to revise estimates introduces inconsistencies and audit risk.

When you adjust the scope or costs, you must recalculate progress. Frequent or late change orders complicate reporting and may require catch-up adjustments; these affect profit and asset/liability balances.

Since this method hinges on managerial estimates, you risk intentional or accidental manipulation, shifting revenue or costs across periods to smooth income. High-profile firms have misused this, drawing regulatory scrutiny.

Under GAAP (ASC 606) and IFRS 15, you can only apply this if:

You need detailed WIP tracking, real-time cost capture, and regular estimate reviews. Without strong internal controls and integrated systems, you struggle with accuracy and audit readiness.

By watching these areas, you reduce financial and regulatory risk and maintain stakeholder trust.

Now that the theory is clear, the following section covers where this method works in business situations.

The U.S. businesses will benefit from the method by keeping their financial statements more up-to-date and matched with the actual progress of a project, which is especially helpful for investors or stakeholders who need a real-time view of financial performance. These examples reveal how PoCM tracks income and costs in real time.

Apply this method to the bill based on tangible progress. For example, if you incur half of the estimated costs for a $800,000 project, you record 50% of revenue ($400,000) in that period. You track progress in your WIP report and adjust billings and revenue accordingly.

Use it for custom, multi‑phase contracts that are year‑long software builds. Rather than waiting for delivery, you log progress (e.g., module completion or hours spent) and recognize revenue monthly based on that progress.

Also Read: How to Start a Software Company in India

Use this for large manufacturing or shipbuilding contracts that span multiple periods. As milestones or stages are met, you report proportionate revenue and costs.

The tax and reporting requirements are as follows;

These applications offer practical insight into how this method is used in real work across industries like construction, technology, and heavy machinery while meeting regulatory requirements.

You might wonder why you’d use this instead of the completed contract method. The following section will help you decide between PoC and CCM.

You should pick the percentage of completion accounting method (PoCM) when you want to spread revenue and costs throughout a project rather than waiting until it finishes. Here's why many prefer it:

With PoCM, revenue and expenses are recognized gradually as you progress, delivering steadier financial results. By contrast, the completed contract method (CCM) holds everything until the project ends, causing sharp swings in income.

You show stakeholders, investors, lenders, and auditors how you perform during a project. CCM makes it difficult to evaluate your financial health midway through the project.

Under PoCM, you pay taxes gradually as you earn. CCM could push all tax liability into one year, which might hit you harder if tax rates rise.

Also Read: NO TDS on software purchase.

GAAP and IRS rules generally require you to use PoCM for long-term contracts unless you're small enough to qualify for CCM's exceptions. That makes PoCM your default choice in most cases.

CCM avoids estimation by waiting for actual costs and revenues, but PoCM gives a more accurate and relevant financial picture. The trade-off is between simplicity (CCM) and insight (PoCM).

If your estimates are sound and progress is measurable, PoCM gives you clearer, timelier insights than CCM. CCM remains an option when estimates are unreliable or you're legally small. Otherwise, PoCM makes your reporting more informative and consistent.

You don’t have to manage this alone. If you need help setting up or managing the process, here’s how our team at VJM Global can step in.

If you manage long-term contracts, especially in software development or services that span months, the percentage of completion method of accounting can clarify your revenue reporting. VJM Global helps software businesses apply this accounting method accurately and with compliance, no matter where they operate.

With deep expertise in U.S. GAAP and Indian accounting standards, VJM Global supports your business by:

From initial setup to monthly reporting, VJM Global makes it easier to manage long-term revenue contracts without guesswork. Book an appointment to see how their team can simplify PoC accounting and keep your business audit-ready.