Expanding into the UAE’s real estate market is an exciting opportunity, but tackling it’s financial environment is not straightforward. For U.S. businesses and investors, understanding local tax regulations, VAT requirements, and compliance with authorities like RERA and the Federal Tax Authority is essential.

A single misstep could lead to costly errors in profitability or legal standing, making a well-informed approach to real estate accounting even more critical.

This guide will walk you through the must-know accounting essentials for real estate in the UAE, from managing property sales and rental income to understanding how VAT impacts your bottom line. Whether you're managing a single property or a growing portfolio, we’ll give you the resources to simplify your accounting and set yourself up for success in this dynamic real estate market. Let’s get started.

Real estate accounting is the backbone of managing property finances. It involves tracking every transaction, from property sales to maintenance costs. Given the substantial sums of money involved in real estate management, precise accounting is crucial for ensuring the financial health of the business.

In the UAE, the real estate sector is booming, even amidst rising inflation. Dubai, in particular, continues to attract both local and international investors. With this growth comes an increased need for strict compliance with federal regulations.

However, managing real estate finances can be challenging due to the sheer volume of transactions and regulatory requirements. For U.S.-based companies, transitioning from U.S. GAAP to the UAE's IFRS-based accounting standards requires careful attention to key local regulations.

Also Read: Key Differences Between US GAAP and IFRS Explained

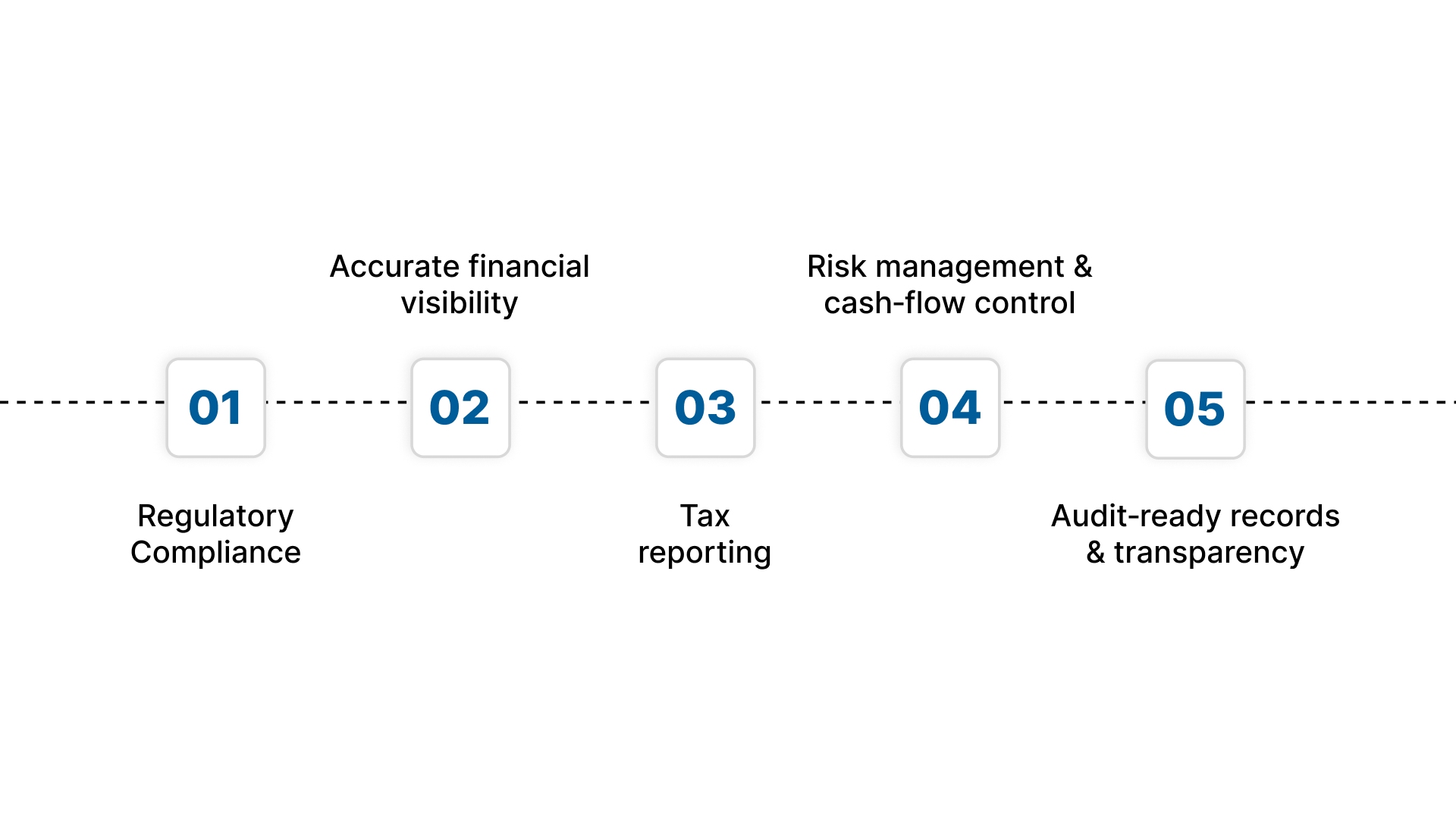

Properly managed financial records help track performance and ensure your business operates efficiently and remains compliant with local regulations. Here's why good accounting practices are essential for real estate businesses in the UAE:

Accounting for real estate in the UAE establishes clarity, supports compliance (in both the UAE and the U.S.), and enables informed decision‑making.

At VJM Global, we provide VAT compliance support, financial reporting services, and audit preparation to ensure your real estate operations are fully compliant. Our team helps U.S. investors with cross-border tax planning and efficient bookkeeping, so you can focus on growth while we handle the financial complexities.

Also Read: Top 10 Proven Real Estate Financial Planning Tips to Maximize Investment Returns

With an understanding of why accounting matters, we can now look into the specific regulations and compliance requirements that govern the UAE real estate market.

The UAE’s real estate industry is governed by several key regulatory bodies that ensure transparency, financial accountability, and compliance.

A comparable structure exists in the U.S., where bodies like the Financial Accounting Standards Board (FASB) and the Internal Revenue Service (IRS) set accounting and tax rules for real estate businesses.

All real estate companies must maintain their financial books in accordance with International Financial Reporting Standards (IFRS), which apply to both large developers and SMEs.

However, for small- to mid-sized businesses, IFRS for SMEs is often adopted, simplifying reporting while still ensuring compliance with key regulatory principles. Companies must keep their books in order for periodic audits by authorities like RERA.

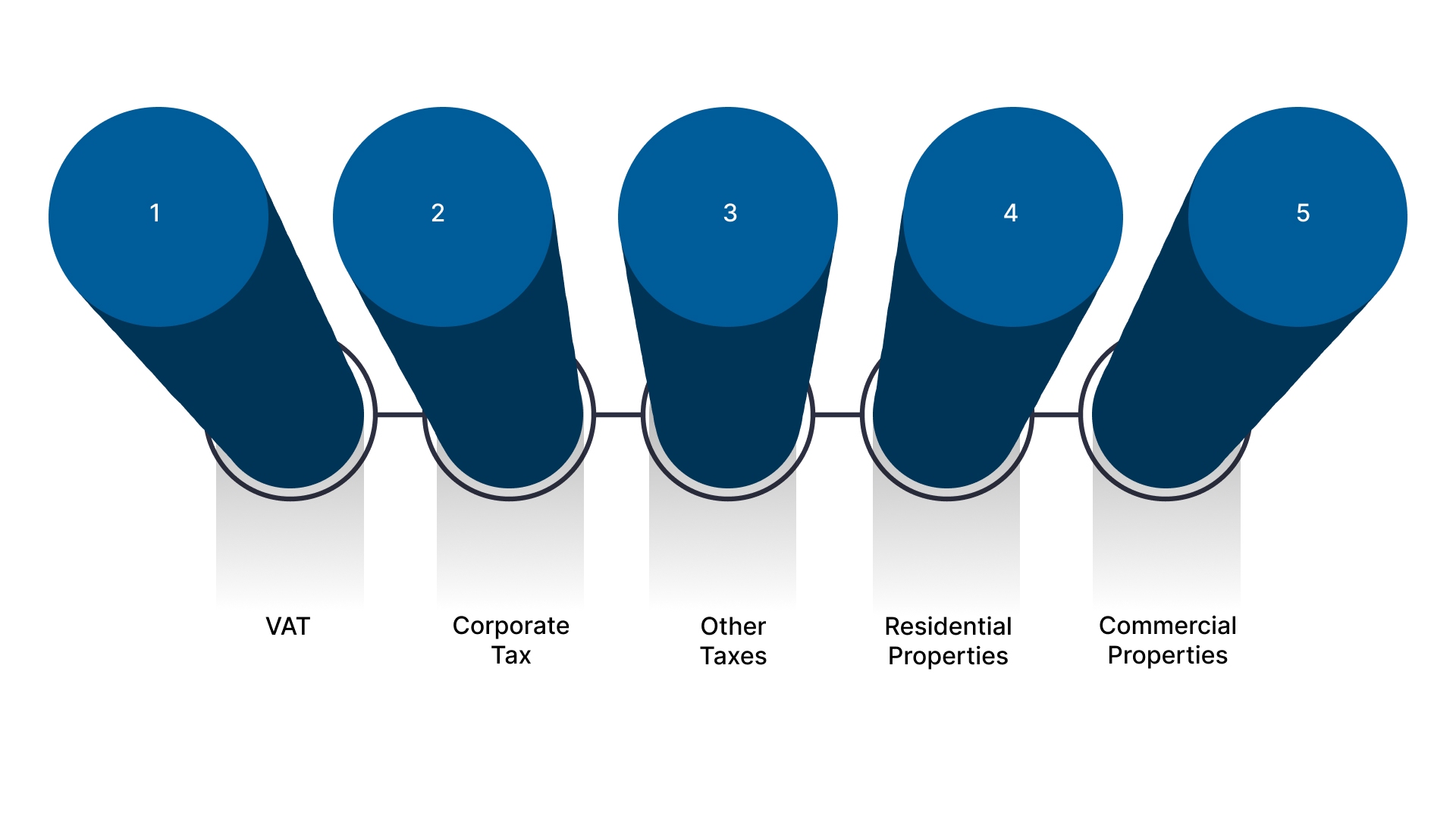

Since the introduction of VAT in 2018, UAE property businesses must be aware of how VAT impacts various transactions:

Failing to comply with VAT regulations can lead to significant penalties. Companies must also ensure timely VAT registration with the FTA.

In 2023, the UAE introduced a new corporate tax regime that impacts property businesses. The corporate tax rate is 9% for taxable income exceeding AED 375,000. Various deductions, such as maintenance and financing costs, may apply to reduce taxable income.

In Dubai, Law No. 8 of 2007 regulates key aspects of real estate accounting, including escrow account management, revenue recognition for pre-sale transactions, and strata title financial statements. The Dubai Land Department also issues guidelines related to property registration and rental return reporting.

Revenue recognition in Dubai real estate is based on the type of sale:

For developers, agents, and firms, revenue is recognized based on the stage of delivery or project completion.

Real estate companies must maintain meticulous expense records to ensure accurate financial statements:

Proper management of real estate assets such as land, buildings, machinery, and improvements is essential. These assets must be tracked, depreciated, and accounted for to ensure financial statements accurately reflect their value.

Under IFRS 16, all leases (except short-term or low-value leases) must be accounted for as finance leases, with both right-of-use assets and lease liabilities recorded on the balance sheet. Depreciation and interest expenses are also recognized.

RERA mandates that developers set up escrow accounts for each project. These accounts must be used only for project-related expenses and reported regularly for transparency. Similarly, trust accounts hold service fees collected for owners' associations, which also require detailed tracking.

Also Read: How to Start a Real Estate Business in Dubai

By adhering to these accounting standards, real estate businesses in the UAE can maintain transparency, ensure compliance, and position themselves for sustainable growth in a dynamic market.

Knowing the regulations is just one part of the equation; it's equally important to implement best practices to ensure smooth and efficient financial management.

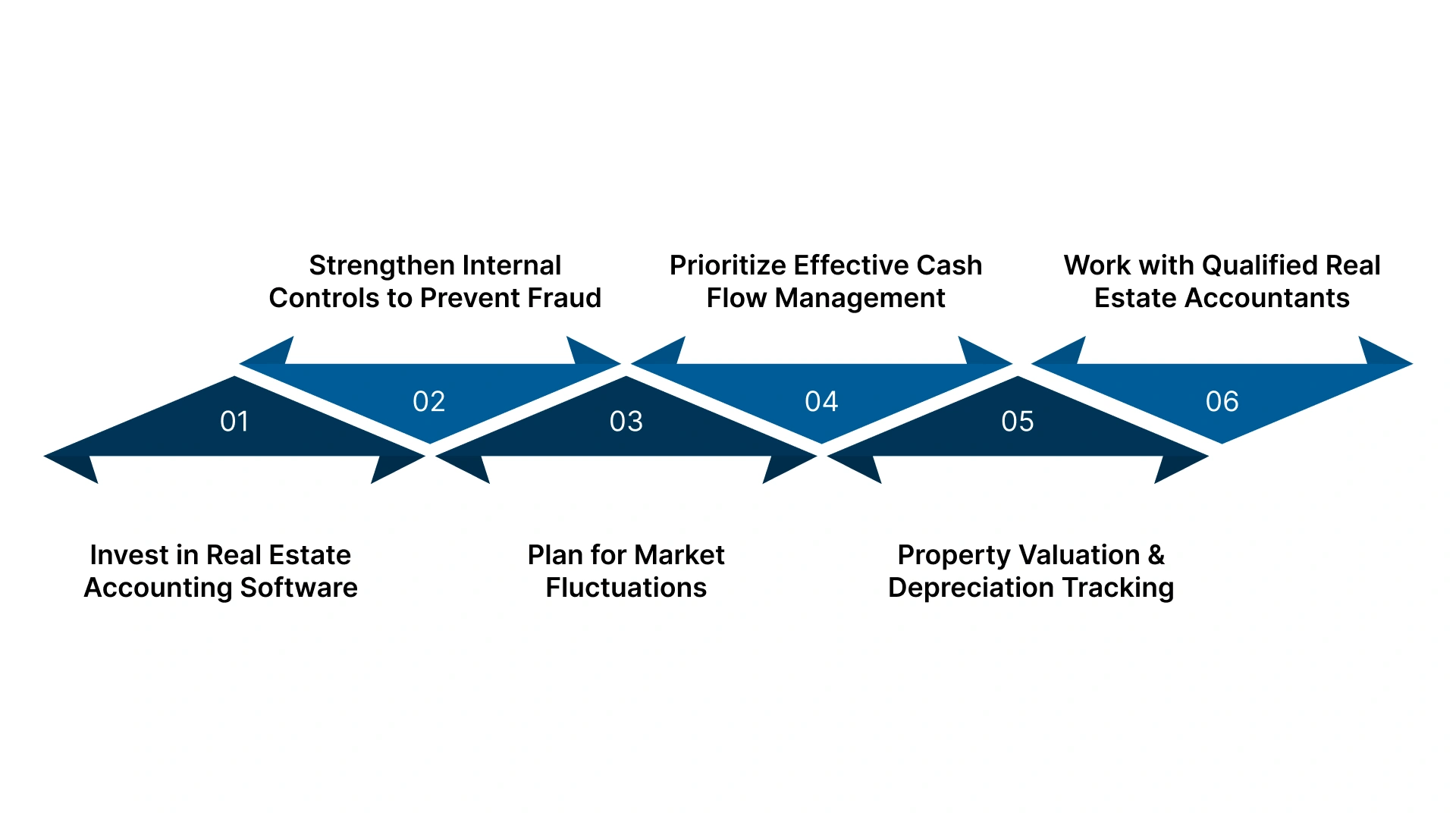

Successfully managing real estate accounting in the UAE demands adherence to strict regulations, efficient use of technology, and a proactive approach to financial planning. Here are some effective best practices:

Handling a large number of properties, transactions, and clients manually can lead to costly errors. Real estate companies should invest in advanced accounting software or ERP systems that centralize financial data across departments and offer a real-time view of the business. These systems can automate repetitive tasks, like tracking rents and depreciation, reducing the risk of human error.

Implementing reliable internal controls is essential to safeguard against financial discrepancies. Regular internal audits ensure that financial records match actual transactions, helping to identify any irregularities early.

Segregating financial duties across your team minimizes the risk of conflicts of interest and unauthorized access to funds.

The UAE’s real estate market is subject to frequent shifts due to economic changes, policy updates, and demand fluctuations. Analyzing past data helps predict cash flow trends and prepares businesses for market downturns.

Conducting scenario analysis can further help in assessing how changes such as interest rate adjustments or new regulations may impact your business.

Maintaining healthy cash flow is critical for real estate businesses, especially when managing a high volume of transactions. Timely collection of rental payments and lease dues is essential to keep operations running smoothly.

Automated systems for invoicing and reminders can help improve payment consistency. In addition, managing vendor payments effectively ensures that long-term relationships are maintained, costs are controlled, and services remain of high quality.

Accurate property valuation is essential to both financial reporting and profitability in the UAE’s real estate sector. Conducting annual property assessments ensures that asset values reflect the market reality and prevent over- or undervaluations on your balance sheets.

Tracking depreciation as per UAE tax regulations also helps accurately manage tax liabilities and avoid reporting errors.

Given the complexity of real estate accounting in the UAE, it’s essential to work with professionals who understand local regulations, tax structures, and market dynamics. At VJM Global, we specialize in offering expert accounting services tailored to the real estate sector.

Our team of UAE-certified accountants is well-versed in local laws, such as RERA regulations and VAT requirements, ensuring your operations are fully compliant and financially sound. Get started today.

Implementing these best practices streamlines your real estate accounting, ensures compliance with UAE regulations, and positions your business for sustained growth in the competitive UAE property market.

Also Read: Real Estate Bookkeeping: A Complete Guide

Finally, let's discuss the most common mistakes businesses make in real estate accounting and how to avoid them.

Investing in real estate in the UAE can be highly profitable, but it’s crucial to avoid common accounting pitfalls that can hurt your bottom line. Here are some mistakes to watch out for:

Being mindful of these common mistakes and taking proactive steps helps avoid costly errors and maximize your returns in the UAE real estate market.

The UAE’s real estate market offers vast potential, but tackling its accounting complexities requires a strategic, informed approach. Whether you're a U.S. investor or a business looking to expand, ensuring your financials align with local tax laws, VAT regulations, and compliance standards is key to success.

At VJM Global, we specialize in guiding U.S.-based businesses through the intricacies of real estate accounting in the UAE. Here’s how we can help:

Partner with VJM Global today for expert accounting support, compliance, and financial management tailored to your UAE real estate business needs. Contact us now.

The primary challenge is managing the complexity of multiple transactions, such as leases, escrow funds, and off-plan project financing, while ensuring accurate reporting and regulatory compliance.

Yes, if the taxable supplies exceed AED 375,000 annually, real estate businesses must register for VAT. This includes sales, leasing, and certain construction services. VAT registration is crucial for staying compliant and allows businesses to reclaim VAT on expenses.

Escrow accounting involves placing project funds into a RERA-approved account, ensuring they are used solely for the intended project. It’s mandatory for developers in Dubai handling off-plan projects to ensure financial transparency and protect buyer interests.

Effective bookkeeping allows you to claim deductions on property-related expenses like depreciation, maintenance, and interest on loans. Additionally, tax-efficient strategies such as planning for tax deferral and understanding local tax incentives can help lower overall liabilities.

Real estate businesses are required to keep financial records for at least five years under UAE tax regulations. This ensures compliance and supports audits, tax filings, and legal requirements in case of disputes or financial reviews.