Introduction

When a London-based manufacturer acquires a subsidiary in Mumbai, or a New York tech firm launches operations in Bangalore, finance teams quickly discover that the same business transactions can produce strikingly different financial statements. The reason comes down to which accounting framework applies: International Financial Reporting Standards (IFRS) or US Generally Accepted Accounting Principles (US GAAP).

These aren't minor stylistic differences. They reflect fundamentally different philosophies about how financial information should be measured, presented, and disclosed.

The stakes are high. IFRS is used in more than 140 jurisdictions worldwide, while US GAAP remains mandatory for all publicly listed American companies. For anyone involved in cross-border investment, M&A activity, or multinational finance, understanding these differences goes well beyond compliance. It directly affects reported profits, asset valuations, tax strategies, and how a business looks to outside investors. This guide breaks down the key divergences and what they mean in practice.

Key Takeaways

- US GAAP is a rules-based framework governed by FASB; IFRS is a principles-based framework governed by the IASB

- Key practical differences cover inventory methods (LIFO allowed under GAAP, banned under IFRS), asset revaluation, R&D capitalization, and cash flow classification

- US companies report under GAAP domestically; international operations, including India's Ind AS, align closely with IFRS

- Full convergence remains unlikely, though both frameworks now align on revenue recognition and lease accounting

IFRS vs US GAAP: Quick Comparison

| Dimension | US GAAP | IFRS |

|---|---|---|

| Governing Body | Financial Accounting Standards Board (FASB) | International Accounting Standards Board (IASB) |

| Geographic Use | United States (mandatory for public companies) | 140+ jurisdictions globally |

| Framework Approach | Rules-based (detailed prescriptive guidance) | Principles-based (broad objectives, professional judgment) |

| Inventory Methods | LIFO, FIFO, Weighted Average permitted | LIFO prohibited; only FIFO or Weighted Average |

| Asset Revaluation | Prohibited (historical cost only) | Permitted for PP&E and certain intangibles |

| R&D Cost Treatment | Expensed as incurred (narrow exceptions) | Research expensed; development capitalized when feasible |

| Cash Flow Classification | Rigid rules (interest/dividends fixed categories) | Flexible policy elections for interest and dividends |

While this table captures structural differences, the practical impact on financial statements can be substantial. A US manufacturer using LIFO inventory accounting may report materially lower profits than an IFRS peer using FIFO during inflationary periods. A UK subsidiary revaluing fixed assets to fair value under IFRS will also show a higher asset base than a comparable US entity reporting at historical cost — a gap that directly affects balance sheet ratios, loan covenants, and acquisition pricing.

For US, UK, or Australian businesses establishing Indian operations, this matters immediately: India's Ind AS framework follows IFRS with limited carve-outs, meaning financial statements prepared under US GAAP will require careful reconciliation before they can satisfy Indian statutory reporting, FDI compliance, or local audit requirements.

Understanding US GAAP and IFRS

What is US GAAP?

US GAAP (Generally Accepted Accounting Principles) is the rules-based accounting framework mandated for all publicly listed US companies. The Financial Accounting Standards Board (FASB) maintains and updates these standards, which the Securities and Exchange Commission (SEC) enforces for domestic public filers.

The rules-based approach means:

- GAAP provides detailed, prescriptive guidance for nearly every transaction scenario

- Offers high consistency and comparability across US companies

- Can require complex workarounds when real-world transactions fall outside established rules

- Creates extensive codification covering revenue recognition, balance sheet classification, inventory methods, and disclosure requirements

Private US companies aren't legally required to follow GAAP, though most do to maintain credibility with lenders, investors, and potential acquirers.

What is IFRS?

IFRS (International Financial Reporting Standards) is the principles-based accounting framework issued by the International Accounting Standards Board (IASB). It's designed to create a common global accounting language across jurisdictions.

The principles-based nature means:

- IFRS sets broad objectives and underlying economic logic rather than detailed rules

- Leaves more room for professional judgment in applying standards

- Requires companies to provide detailed disclosures explaining how they applied principles to their specific circumstances

- Focuses on the substance of transactions over strict form

IFRS is the required or permitted standard across the EU, most of Asia, South America, and Africa. For foreign companies entering the Indian market specifically, this global reach has a direct implication: India's Ind AS (Indian Accounting Standards) is substantially converged with IFRS, meaning companies already reporting under IFRS will find the transition to Indian compliance considerably more straightforward.

Key Differences Between IFRS and US GAAP

Inventory Valuation

Under US GAAP (ASC 330):

- Companies may use LIFO (Last-In, First-Out), FIFO (First-In, First-Out), or weighted average costing

- LIFO can significantly reduce taxable income during inflationary periods

- Once inventory is written down, it cannot be written back up

Under IFRS (IAS 2):

- LIFO is strictly prohibited

- Only FIFO or weighted average methods allowed

- Inventory write-downs can be reversed if market conditions improve

Why this matters: Academic research analyzing 177 companies that abandoned LIFO found median additional tax costs of $5.25 million during inflationary periods. US companies using LIFO must make significant adjustments when comparing financials with IFRS-reporting peers or when transitioning to IFRS for international operations.

Asset Revaluation and Impairment

Under US GAAP (ASC 360):

- Fixed assets and intangibles recorded at historical cost only

- Values can only decrease through depreciation or impairment

- Once written down, assets cannot be revalued upward—even if market conditions improve

Under IFRS (IAS 16, IAS 40):

- Companies can elect to revalue PP&E and certain intangibles to fair value

- Investment properties can be carried at fair value with changes flowing through income

- Impairment losses can be reversed (except for goodwill) if recoverable amount increases

Why this matters: European REIT Unibail-Rodamco-Westfield carries its €48.9 billion investment property portfolio at fair value under IAS 40. A comparable US GAAP company would report those same properties at historical cost minus depreciation, producing book values that diverge significantly from current market reality.

This gap is particularly consequential for capital-intensive industries—manufacturing, real estate, infrastructure—where asset values fluctuate substantially with market conditions.

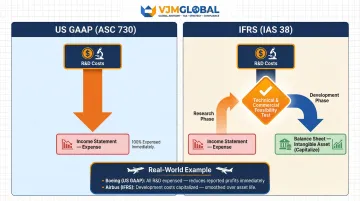

R&D Cost Treatment

Under US GAAP (ASC 730):

- All research AND development costs expensed as incurred

- Narrow exceptions exist for internal-use software

Under IFRS (IAS 38):

- Research costs expensed

- Development costs must be capitalized once technical feasibility is established

Example: In 2023, Airbus capitalized €1.7 billion in development costs on its balance sheet under IFRS, amortizing these over the estimated production run. Boeing, reporting under US GAAP, expensed its development costs immediately. For analysts benchmarking the two companies, this means Airbus shows higher near-term assets and smoother earnings—not because its economics differ from Boeing's, but because the accounting frameworks treat identical activities differently.

Cash Flow Statement Classification

Under US GAAP (ASC 230):

- Interest paid and received: operating activities

- Dividends received: operating activities

- Dividends paid: financing activities

- No flexibility—classifications are prescribed

Under IFRS (IAS 7):

- Companies can classify interest and dividends in operating, investing, or financing sections based on their elected accounting policy

- Must apply consistently once elected

Why this matters: A 2017 academic study analyzing European IFRS companies found that 76% classified interest paid as operating, while 23.5% classified it as financing. Portugal Telecom classified interest paid as financing and interest received as investing; under US GAAP rules, its operating cash flow would have been 16% lower.

Analysts comparing IFRS and US GAAP companies on operating cash generation need to manually reclassify these line items before the numbers are meaningfully comparable.

Financial Statement Presentation

Two key structural differences:

Balance sheet ordering:

- GAAP: Lists assets from most to least liquid (current assets first)

- IFRS: Lists from least to most liquid (non-current assets first)

Comparative periods:

- GAAP: SEC requires three years of income statements and cash flows

- IFRS: Requires only two years of comparative data

Mezzanine equity: US GAAP permits a "mezzanine" classification between liabilities and equity for instruments redeemable outside the company's control (such as redeemable preferred stock). IFRS strictly classifies instruments as either liabilities or equity with no middle ground.

Which Accounting Standard Applies to Your Business?

The applicable standard is primarily determined by where your company is incorporated and whether it's publicly listed.

Core decision rules:

- US domestic public companies: Must follow US GAAP

- Companies incorporated or listed outside the US: Generally follow IFRS or a local variant converged with IFRS

- US subsidiaries of foreign IFRS parents: Often maintain dual-reporting capability

India-Specific Considerations

India uses Ind AS (Indian Accounting Standards), which is substantially aligned with IFRS. The phased implementation began in 2016:

- Phase I (April 1, 2016): Mandatory for companies with net worth ≥ ₹500 crore

- Phase II (April 1, 2017): Extended to listed companies and companies with net worth ≥ ₹250 crore

US or UK companies setting up subsidiaries or joint ventures in India will typically deal with Ind AS for statutory reporting, while maintaining GAAP or IFRS-based consolidated accounts at the parent level. That dual-reporting obligation is where cross-border complexity most often surfaces — and it connects directly to the reconciliation challenges that arise in M&A and investment contexts.

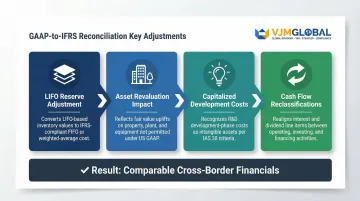

Cross-Border M&A and Investment Scenarios

Understanding reconciliation adjustments becomes essential when:

- A US company acquires an IFRS-reporting target

- Foreign investors analyze US-listed versus internationally listed companies

- Financial analysts compare cross-border peers

Key reconciliation items include LIFO reserve adjustments, asset revaluation impacts, capitalized development costs, and cash flow reclassifications.

For US, UK, and Australian companies establishing operations in India, managing both Ind AS statutory filings and parent-level GAAP or IFRS reporting simultaneously is a common challenge. VJM Global's team of Chartered Accountants and CPAs handles exactly this — statutory Ind AS compliance in India alongside consolidated reporting for the parent entity.

Conclusion

Neither IFRS nor US GAAP is universally "better"—each reflects the regulatory environment and reporting culture where it was developed. US GAAP's rules-based precision offers consistency and reduces interpretive ambiguity. IFRS's principles-based flexibility better accommodates diverse global business models and emerging transaction types.

For businesses operating internationally, the key is understanding which standard applies and where the two diverge. Getting this right matters in practical terms:

- Avoids costly restatements when financials are reviewed across jurisdictions

- Supports accurate comparisons for investors, lenders, and acquirers

- Reduces compliance risk during audits and regulatory filings

As cross-border business, investment, and M&A activity intensifies, fluency in both frameworks is now a core operational requirement.

That's where specialized advisory makes a difference. Firms like VJM Global work with international businesses to ensure accurate, compliant reporting across both frameworks—covering local statutory requirements and parent-level consolidation in the same engagement.

Frequently Asked Questions

What are the major differences between IFRS and US GAAP?

GAAP is a rules-based, US-specific framework governed by FASB, while IFRS is a principles-based framework adopted globally and governed by the IASB. The most significant practical differences include inventory methods (LIFO banned under IFRS), asset revaluation permissions, R&D capitalization rules, and cash flow classification flexibility.

How to know if a company uses GAAP or IFRS?

Check the company's annual report or financial statement notes, which explicitly state the accounting framework used. US publicly listed companies use GAAP; companies listed on non-US exchanges or in countries like the UK, EU, Australia, or India (Ind AS) typically follow IFRS or a converged variant.

Does the USA use IFRS or GAAP?

The US requires domestic public companies to use US GAAP, governed by FASB and enforced by the SEC. Foreign private issuers listed on US exchanges are permitted (but not required) to report under IFRS without reconciliation to GAAP.

Why doesn't the U.S. use IFRS?

The 2012 SEC Staff Report cited deeply entrenched GAAP infrastructure, concerns about shifting from rules-based to principles-based standards, regulatory sovereignty issues, and high transition costs for US companies. The SEC has maintained a supportive but non-committal stance on convergence.

Is US GAAP more conservative than IFRS?

In certain areas, GAAP is more conservative—it prohibits asset revaluation upward and inventory write-down reversals. However, IFRS can be more conservative in other contexts, such as requiring mandatory capitalization of development costs meeting specific criteria.

What are the 5 major GAAP principles?

The five foundational GAAP principles are:

- Revenue Recognition: Revenue recorded when earned, not when cash is received

- Matching Principle: Expenses matched to the revenues they helped generate

- Full Disclosure: All material information disclosed in financial statements

- Cost Principle: Assets recorded at historical cost, not current market value

- Going Concern: Assumes the entity will continue operating into the foreseeable future