Introduction

If you're sitting on idle cash in Singapore, the numbers aren't working in your favor. Fixed deposit yields have dropped from their 2023 peaks of 4.5%+ p.a. to roughly 1.10% p.a. today. The latest 6-month T-bill auction settled at just 1.40% p.a., and bank base savings rates remain stuck at 0.05%. The challenge now is earning meaningful returns without locking funds away or sacrificing flexibility.

Cash management accounts (CMAs) have emerged as the practical answer. These hybrid products sit between savings accounts and investment portfolios, investing your cash into low-risk money market funds and short-duration bonds. Yields typically range from 1.3% to 2.8% p.a., with no lock-in periods and MAS-regulated structures.

That said, the Chocolate Finance withdrawal crisis in March 2025 was a reminder that understanding how these products work matters just as much as comparing headline rates.

Key Takeaways

- Earn 1.3%–2.8% p.a. with cash management accounts (CMAs) versus the 0.05% bank base rate — by putting idle cash into money market and short-duration bond funds.

- Expect no SDIC insurance, but MAS-regulated platforms segregate client assets to protect against platform insolvency.

- Top picks span five platforms: Endowus Cash Smart, StashAway Simple Plus (2.8% yield), Syfe Cash+ Flexi, Chocolate Finance, and Tiger Vault.

- Each platform leads on a different dimension — yield, fees, debit card access, or brokerage integration.

- Compare net-of-fee yields, withdrawal speed, SRS compatibility, and underlying fund risk before choosing.

What is a Cash Management Account in Singapore?

A cash management account is an investment product, not a bank deposit. It's offered by MAS-licensed fintech platforms, robo-advisors, and online brokerages—not traditional banks. When you deposit SGD into a CMA, the platform invests it across a pre-selected portfolio of low-risk instruments such as:

- Money market funds (near-cash, minimal volatility)

- Short-duration bond funds (higher yield, modest interest rate sensitivity)

Returns fluctuate based on market conditions, unlike fixed deposits where rates are guaranteed. Platforms quote indicative annualised yields net of management and fund-level fees. Withdrawals can typically be made anytime, though processing takes 1–6 business days depending on the platform and fund redemption timelines.

CMAs are regulated under the Securities and Futures Act. All five platforms reviewed hold Capital Markets Services (CMS) licences from MAS and must segregate client assets from their own operating funds, which offers protection if the platform fails.

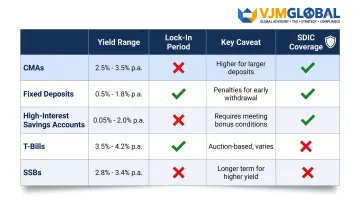

Comparison: CMAs vs Other Cash-Parking Options

| Option | Yield Range | Lock-In | Key Caveat |

|---|---|---|---|

| CMAs | 1.3%–2.8% | None | Returns not guaranteed |

| Fixed Deposits | ~1.10% (3-month) | Yes | Guaranteed but inflexible |

| High-Interest Savings Accounts | 0.05% base / up to 4%–8% bonus | None | Bonus rates require salary crediting, monthly spend, insurance |

| T-Bills | Market rate | 6 months | Government-backed, no credit risk |

| SSBs (e.g., SBJUN26) | 1.40% yr 1 / 2.14% avg over 10 yrs | Monthly redemption (with penalties) | Government-backed, less flexible |

One critical difference sets CMAs apart from all of the above: SDIC deposit insurance does not apply. The Singapore Deposit Insurance Corporation covers bank deposits up to S$100,000 per depositor per bank, but CMAs invest in unit trusts, placing them outside the DI Scheme entirely.

Best Cash Management Accounts in Singapore 2026

All accounts below are MAS-regulated, SGD-denominated, and selected based on competitive net yields, transparent fees, fund diversification, and accessibility to retail investors. Yields change with market conditions—verify current rates on each platform before investing.

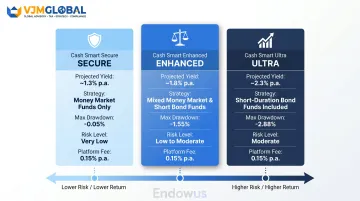

Endowus Cash Smart

Endowus is a MAS-licensed robo-advisor (CMS101051) offering three tiers of its Cash Smart account—Secure, Enhanced, and Ultra—catering to different risk-return preferences. All three accept cash and SRS funds, with a minimum investment of S$1,000.

Why the tiered structure matters:

The three-tier architecture lets you match risk appetite precisely. Cash Smart Secure invests only in money market funds for lowest risk. Enhanced adds the UOB United SGD Fund for balanced exposure. Ultra includes PIMCO Low Duration Income Fund and short-duration bond funds for highest yield, with correspondingly higher volatility.

Projected yields (as of 31 March 2026):

| Tier | Net Yield (p.a.) | Endowus Fee | Fund-Level Fee | Historical Max Loss |

|---|---|---|---|---|

| Secure | 1.3% | 0.15% | 0.13% | -0.05% |

| Enhanced | 1.8% | 0.15% | 0.24% | -1.55% |

| Ultra | 2.3% | 0.15% | 0.27% | -2.88% |

Key details:

- Underlying funds: Secure uses Fullerton SGD Cash Fund and LionGlobal SGD Enhanced Liquidity Fund; Ultra adds PIMCO Low Duration Income, LionGlobal Short Duration Fund, and UOB United SGD Fund

- SRS-compatible: Yes (all three tiers)

- Withdrawal timeline: 2-4 business days

- Custodian: UOB Kay Hian (assets held in investor's name)

Ultra's -2.88% maximum historical drawdown reflects its short-duration bond exposure. It's best suited for investors who can accept modest mark-to-market swings in exchange for the higher yield.

StashAway Simple Plus

StashAway (CMS100604) has operated since 2016 and offers two cash management products: Simple Plus (higher yield via short-duration bonds) and Simple (capital stability via money market funds). No minimum deposit is required.

The highest yield, with a catch:

At 2.8% p.a. yield to maturity (as of 24 April 2026), Simple Plus offers the highest projected return among reviewed CMAs. StashAway recommends a 12-month holding period because of its short-duration bond fund exposure. In Q1 2026, Simple Plus returned just 0.1% as rising yields created negative mark-to-market effects. Short-term performance can deviate sharply from the annualised YTM figure.

Projected yields (as of April 2026):

| Product | Yield | Management Fee | Fund-Level Fee (net of rebate) |

|---|---|---|---|

| Simple Plus | 2.8% YTM | 0.20% | 0.16% |

| Simple | 1.5% projected | 0.15% | N/A |

Underlying funds:

- Simple Plus: 60% LionGlobal Short Duration Bond Fund, 20% LionGlobal SGD Enhanced Liquidity Fund, 20% Amova AM Shenton Short Term Bond Fund

- Simple: 30% LionGlobal SGD Money Market Fund, 70% LionGlobal SGD Enhanced Liquidity Fund

Key details:

- Lock-in: None (but 12-month holding period recommended for Simple Plus)

- SRS-compatible: Yes

- Bonus: New investors get an extra 1% p.a. rate boost for 3 months on deposits up to S$10,000

Syfe Cash+ Flexi

Syfe is a Singapore-based digital wealth platform offering Cash+ Flexi as its primary cash management product. With one of the lowest management fee structures in the category, it appeals to cost-conscious investors.

Low fees, full liquidity:

Management fees range from just 0.05%-0.15% p.a., among the lowest in this category. Syfe also offers a Cash+ Guaranteed counterpart, which locks funds into fixed deposits for guaranteed (but lower) returns. Cash+ Flexi maintains full liquidity with no lock-in period.

Projected yields (as of May 2026):

| Product | Projected Yield | Management Fee | Lock-in |

|---|---|---|---|

| Cash+ Flexi SGD | 1.5%-1.6% p.a. | 0.05%-0.15% | None |

| Cash+ Flexi USD | 3.7%-3.8% p.a. | 0.15%-0.20% | None |

Underlying funds (SGD):

- 70% LionGlobal SGD Enhanced Liquidity Fund

- 30% LionGlobal SGD Money Market Fund

Key details:

- Minimum investment: None for SGD; US$10,000 for USD

- SRS-compatible: Yes (SGD portfolio)

- Withdrawal: Marketed as "next-day"; full processing may take 5-6 business days

- Unique feature: USD option at 3.7%-3.8% for investors seeking USD exposure

Syfe's fund mix mirrors StashAway Simple—making it the better fit for investors who prioritise capital stability and want to minimize fees rather than chase the highest yield.

Chocolate Finance

Chocolate Finance (CMS101452) is a MAS-licensed asset manager offering its Chocolate Managed Account as a cash management solution. Unlike robo-advisor platforms, it operates as a fund manager and differentiates itself through its Top-Up Programme and debit card integration.

Three features that stand out:

- Top-Up Programme: Guarantees minimum returns on the first S$50,000 (SGD and USD separately) by topping up any shortfall. Valid until 30 June 2026 or S$1.5B AUM. This is not a deposit guarantee.

- Chocolate Visa Debit Card: Earns 1 HeyMax mile per S$1 spent (up to S$1,000/month) with zero FX fees on overseas transactions — no other CMA on this list offers this.

- Performance-based fees: No platform fee until the target return is achieved; a 0-2% fee applies only when it's exceeded.

Target returns (as of May 2026):

| Currency | First S$20,000 | Next S$30,000 | Above S$50,000 |

|---|---|---|---|

| SGD | 2.5% p.a. | 2.2% p.a. | Up to 2.2% p.a. |

| USD | 4.1% p.a. | 3.8% p.a. | Up to 3.8% p.a. |

Note: Rates vary across Chocolate Finance website sections and change frequently. Verify current rates before investing.

Withdrawal timeline:

- Standard processing: 3-7 business days

- Instant withdrawals suspended since March 2025 crisis

March 2025 Crisis Context:

Over S$500 million in withdrawal requests were submitted in one week, driven partly by gaming of the miles reward system via AXS bill payments. MAS engaged on 12 March 2025 and confirmed customer assets remained safe in segregated accounts held at HSBC, State Street, BNP Paribas, and Citibank.

Tiger Vault

Tiger Vault is the cash management feature offered by Tiger Brokers, designed for existing account holders to earn returns on idle trading cash. It integrates directly with the brokerage platform and supports an auto-sweep function.

Built for active traders:

Tiger Vault is the only CMA that doubles as buying power. Up to 99% of holdings count toward equities, IPOs, and options trades. Active traders get yield on idle cash without giving up trading agility.

Available SGD funds:

- Phillip Money Market Fund "A"

- Fullerton SGD Cash Fund "A" Acc

- United SGD Money Market

- LionGlobal SGD Enhanced Liquidity Fund

Key details:

- Minimum investment: S$1

- Platform eligibility: Requires an existing Tiger Brokers account

- Subscription/redemption fees: Zero (fund-level expense ratios apply)

- Redemption: T0 funds settle same-day if submitted before 11:00 AM. Cash withdrawal to bank takes an additional 1-3 business days.

- Auto-sweep: Idle cash automatically invests; funds auto-redeem to cover trades

Note: Current yields are displayed within the Tiger app and are not published on the marketing website. The platform's "up to 4.5%" headline reflects December 2024 conditions and likely refers to USD fund yields.

How to Choose the Right Cash Management Account

The biggest mistake investors make is optimising solely for the highest advertised yield without accounting for total cost. Headline yields are gross or projected; fund-level fees and platform fees reduce actual returns. Always compare net-of-fee yields and check whether the yield is a 7-day annualised figure (which fluctuates daily) or a more stable yield-to-maturity projection.

Three Practical Selection Criteria

1. Risk Tolerance

Money market-only funds (Syfe Cash+ Flexi, StashAway Simple, Endowus Secure) carry lower yield volatility than short-duration bond fund blends (StashAway Simple Plus, Endowus Ultra). If you cannot tolerate any quarterly negative returns, stick to money market options.

2. Liquidity Needs

Consider how quickly you may need to access funds:

- Same-day: Tiger Vault (T0 funds, if submitted by 11:00 AM)

- 2-4 business days: Endowus

- 3-7 business days: Chocolate Finance (instant withdrawals suspended)

- Next-day (marketed): Syfe (actual processing may take 5-6 days)

3. Platform Fit

Existing brokerage users may find Tiger Vault more convenient (99% buying power integration). Standalone savers may prefer dedicated CMAs like Endowus or Syfe. If you value miles and zero-FX-fee spending, Chocolate Finance's debit card adds a practical perk.

SDIC and Regulatory Safety

CMAs are not SDIC-insured. However, MAS-regulated platforms must hold client funds in segregated accounts separate from the platform's own assets, which provides meaningful protection if a platform fails.

Custodian arrangements vary by platform:

- Endowus — assets held at UOB Kay Hian in the investor's name

- Chocolate Finance — institutional custodians include HSBC, State Street, BNP Paribas, and Citibank

For NRIs and cross-border investors: That regulatory safety picture gets more complex when funds move between Singapore and India. Holding foreign assets in CMAs can trigger disclosure requirements under Schedule FA or FEMA obligations back in India. If you're navigating this, VJM Global offers cross-border tax advisory for NRIs and OCIs, covering DTAA interpretation, FEMA compliance, and international tax planning.

Conclusion

In a rate-normalising environment, cash management accounts remain one of the most accessible ways for Singaporeans and Singapore-based individuals to make idle cash work harder—without the rigidity of fixed deposits or the complexity of equity investing. Even at 2026's compressed yields, CMAs delivering 1.3%–2.8% p.a. significantly outperform the 0.05% bank base rate and 1.10% fixed deposit rates.

Before choosing a CMA, assess your specific financial situation against these factors:

- Yield vs. liquidity trade-offs — higher rates often come with notice periods or caps

- Total fees — platform, withdrawal, and FX charges can erode stated returns

- Regulatory structure — MAS-licensed platforms carry different protections than fund-based wrappers

- Platform compatibility — check whether the CMA integrates with your existing bank or brokerage accounts

Yields and platform terms shift frequently. Always verify current rates directly with the provider before committing funds.

Frequently Asked Questions

What is the purpose of a cash management account?

A CMA is designed to generate higher returns on idle cash than a standard savings account by investing in low-risk instruments like money market funds and short-term bonds—while maintaining liquidity and no lock-in periods. It suits investors who want yield above bank rates without sacrificing flexibility.

Where to put excess cash in Singapore?

Main options include high-interest savings accounts, fixed deposits, T-bills, Singapore Savings Bonds, and cash management accounts. CMAs offer a strong balance of yield (1.3%–2.8% p.a.) and flexibility, making them well-suited for short-to-medium-term cash parking without lock-ins.

Can a foreigner open an investment account in Singapore?

Yes. Most MAS-regulated CMA platforms accept foreigners and PRs, subject to KYC/AML identity verification. Platforms that require Singpass are limited to Citizens and PRs; others accept passport and employment pass documentation.

What are the best cash management accounts?

Top options include Endowus Cash Smart, StashAway Simple Plus (2.8% p.a.), Syfe Cash+ Flexi, Chocolate Finance, and Tiger Vault. The best choice depends on your priorities—yield, fees, platform integration, or SRS compatibility.

Are cash management accounts safe in Singapore?

CMAs carry low risk because they invest in short-duration, investment-grade instruments. MAS-regulated platforms ringfence client assets in segregated accounts, protecting against platform insolvency. However, CMAs are not SDIC-insured and returns are not guaranteed, unlike bank deposits.

What is the difference between a cash management account and a fixed deposit?

Two key differences: (1) CMAs have no lock-in period and allow withdrawals anytime, while fixed deposits lock funds for a fixed tenor with penalties for early exit; (2) CMA yields are variable and market-linked, while fixed deposit rates are guaranteed for the agreed term.