The most direct path into the Indian market for a Singapore entity is incorporating an Indian Private Limited Company (Pvt Ltd). It creates a fully independent legal presence — one that can hire employees, hold assets, enter contracts, and transact with Indian customers under a locally recognised structure.

This article covers what an Indian Pvt Ltd is, why it suits Singapore investors, its defining features, the complete step-by-step registration process (including the India-specific steps most guides skip), and post-incorporation compliance obligations.

Key Takeaways

- A Singapore company can own 100% of an Indian Pvt Ltd through the automatic FDI route in most sectors — no prior government approval required

- Minimum 2 directors (at least 1 Indian resident) and 2 shareholders; no statutory minimum paid-up capital since 2015

- Registration via the SPICe+ portal typically takes 7–15 business days with complete documentation in hand

- Singapore-based directors must obtain apostilled/notarised documents before any MCA filing begins

- After incorporation, file FC-GPR with RBI within 30 days; ongoing obligations include ROC filings, GST returns, and transfer pricing compliance

What Is a Private Limited Company in India?

Under Section 2(68) of the Companies Act, 2013, a Private Limited Company is a legally separate entity that restricts share transfers, caps membership at 200 shareholders, and prohibits public subscription of its securities. It is regulated by the Ministry of Corporate Affairs (MCA) and provides limited liability to all shareholders.

For a Singapore Pte Ltd entering India, the Pvt Ltd structure creates a fully operational Indian legal entity. That means your company can:

- Hire staff directly under Indian employment law

- Sign local contracts in its own name

- Hold intellectual property registered in India

- Open INR bank accounts with Indian banks

- Engage with Indian regulators independently

This is a structure Indian counterparties recognise and trust — which matters when closing commercial deals.

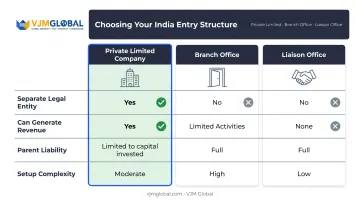

How It Compares to Other Entry Structures

| Structure | Separate Legal Entity | Can Generate Revenue | Parent Liability |

|---|---|---|---|

| Private Limited Company | ✅ Yes | ✅ Yes | Limited to capital invested |

| Branch Office | ❌ No | ✅ Limited activities | Parent bears full liability |

| Liaison Office | ❌ No | ❌ No | Parent bears full liability |

For Singapore companies planning full commercial operations in India, the Pvt Ltd structure is typically the starting point — and the table above shows why the alternatives fall short.

Why Singapore Companies Choose the Indian Private Limited Company Structure

100% FDI Through the Automatic Route

The DPIIT Consolidated FDI Policy Circular of 2020 permits 100% FDI under the automatic route in sectors not specifically restricted — meaning Singapore companies can own their Indian subsidiary outright without filing for government approval in most industries including IT, consulting, manufacturing, and e-commerce marketplaces.

Sectors where caps apply include:

- Defence — automatic route up to 74%; government route beyond that

- Print/digital news media — capped at 26% under government route

- Insurance companies — 49% automatic route

Always verify your specific sector's applicability before proceeding.

The India-Singapore DTAA Advantage

Under Article 10 of the India-Singapore Double Taxation Avoidance Agreement, dividends paid by the Indian Pvt Ltd to its Singapore parent are subject to a maximum 10% withholding tax at source, provided the Singapore entity is the beneficial owner. Compared to non-treaty jurisdictions, this rate makes profit repatriation considerably more tax-efficient for Singapore holding companies.

VJM Global advises Singapore-based groups on DTAA structuring, including the Most Favoured Nation (MFN) clause implications that apply to the India-Singapore treaty framework.

Operational Necessity

A Singapore entity alone cannot fulfill several commercial requirements in India. A locally incorporated Pvt Ltd is needed to:

- Directly employ Indian staff on Indian payroll

- Hold Indian intellectual property and trademarks

- Obtain sector-specific Indian licences (FSSAI, SEBI, telecom, etc.)

- Bid for Indian government contracts

- Receive domestic payments through UPI, NEFT, and regulated payment gateways

Foreign entities with approved Branch or Liaison Office status may open non-interest-bearing INR current accounts through authorised dealer banks — but a Pvt Ltd structure offers far broader operational scope and commercial credibility with Indian banks and enterprise customers.

Cost Efficiency

Many Singapore companies use the Indian subsidiary as a cost-effective delivery or operations arm while the Singapore entity retains the customer-facing or holding role. Indian office space, professional talent, and service provider costs are significantly lower than Singapore equivalents — a setup that lets companies scale their Asia-Pacific operations without proportionally scaling their cost base.

Key Features of an Indian Private Limited Company

Separate Legal Entity and Limited Liability

The Indian Pvt Ltd is legally distinct from both its Singapore parent and its individual directors. The Singapore parent's liability is capped at the capital it has invested in the Indian entity. The Indian company can sue and be sued in its own name: the parent company's balance sheet remains fully protected.

Shareholding and Governance

- Shareholders: Minimum 2, maximum 200; shares are not freely transferable and cannot be publicly offered

- Directors: Minimum 2, maximum 15 (extendable by special resolution); at least 1 must be an Indian resident (physically present in India for 182+ days in the previous calendar year)

- Meetings: At least 4 board meetings per year, with no more than 120 days between consecutive meetings

Singapore companies that lack an Indian resident director can engage a nominee director service — a standard, compliant approach used by many foreign subsidiaries.

No Minimum Paid-Up Capital

The Companies (Amendment) Act, 2015 removed the statutory minimum paid-up capital requirement. A company can technically be incorporated with ₹1. In practice, keeping initial authorised capital at ₹1 lakh minimises government registration fees while leaving room to increase later. Any capital actually brought in from Singapore must comply with RBI's fair market value pricing guidelines.

Perpetual Succession

The company continues to exist regardless of changes in directors or shareholders. This matters for Singapore holding companies that rotate directors over time or anticipate ownership restructuring — operations continue without interruption.

Corporate Tax Regime

Beyond structure and governance, tax exposure is a critical factor in the incorporation decision. The Indian Pvt Ltd is taxed on its India-sourced income, with two primary rate options:

| Regime | Base Rate | Effective Rate (with surcharge & cess) |

|---|---|---|

| Section 115BAA (concessional) | 22% | ~25.17% |

| Standard rate (turnover ≤ ₹400 cr) | 25% | Higher with surcharge |

All inter-company transactions between the Indian subsidiary and the Singapore parent (management fees, royalties, services, loans) must comply with India's transfer pricing rules under Sections 92 to 92F of the Income Tax Act.

Step-by-Step Registration Process for Singapore-Based Companies

The SPICe+ integrated form on the MCA portal bundles name reservation, incorporation, and simultaneous issuance of CIN, PAN, TAN, GSTIN, EPFO, and ESIC registrations into a single workflow. Before any MCA filings begin, however, Singapore-based applicants must complete a document authentication stage that adds meaningful lead time.

Apostillation and Notarisation of Singapore Documents

All identity and address documents of Singapore-based directors and shareholders must be notarised by a Singapore notary public and then apostilled by the Singapore Academy of Law (SAL), which has served as Singapore's designated apostille authority since 16 September 2021. Without apostilled documents, the MCA will reject the incorporation application.

Documents typically required include:

- Passport copies

- Proof of address

- Bank statements

Check SAL's current service page for turnaround times before planning your timeline.

Step 1: Obtain Digital Signature Certificates (DSC) for All Directors

Each proposed director — both Singapore-based and Indian resident — must hold a Class 3 DSC issued by a licensed Certifying Authority in India. Foreign nationals can complete this remotely via video verification. VJM Global handles DSC procurement as the first step in its incorporation process, VJM Global handles DSC procurement as the first step in its incorporation process, typically completed within 2 working days.

Step 2: Reserve the Company Name via RUN

Submit the proposed name through the MCA's RUN (Reserve Unique Name) service. The name must be unique and must not conflict with existing registered companies or trademarks. Prepare at least 2–3 name options to avoid delays if the first is rejected.

Step 3: File SPICe+ with MoA, AoA, and Supporting Documents

SPICe+ Part B is filed with the Memorandum of Association (INC-33), Articles of Association (INC-34), director and company secretary declarations, and an Indian registered office address proof (utility bill plus rent agreement or NOC from the property owner).

A practical note: Singapore companies without a physical Indian address at incorporation often work with service providers who offer registered address solutions. Contact VJM Global directly to confirm availability of this arrangement.

Step 4: FC-GPR Filing With RBI Post-Allotment

This is the step most guides overlook. Once shares are allotted to the Singapore parent, the Indian Pvt Ltd must file Form FC-GPR (Foreign Currency – Gross Provisional Return) with the RBI through its authorised dealer (AD) bank within 30 days of share allotment. Missing this deadline can trigger compounding charges under FEMA.

FC-GPR is a mandatory compliance obligation separate from the MCA incorporation process — and unique to foreign-invested companies.

Step 5: Open an Indian INR Current Account

After receiving the Certificate of Incorporation (which includes CIN, PAN, and TAN), the company must open an INR current account with an RBI-authorised AD bank. The foreign inward remittance from Singapore for share capital must flow through this account and be correctly reported as FDI. Singapore directors typically coordinate this remotely or with a visit to India for KYC.

VJM Global supports the complete registration journey — apostillation guidance, SPICe+ filing, FC-GPR compliance, and bank account coordination — giving Singapore companies one point of contact from entry to operation in India.

Post-Registration Compliance Obligations for Singapore-Owned Indian Companies

Annual ROC and Tax Filings

| Obligation | Form | Timing |

|---|---|---|

| Financial statements | AOC-4 | Within 30 days of AGM |

| Annual return | MGT-7 / MGT-7A | Within 60 days of AGM |

| Income tax return (audit) | ITR | By 31 October |

| Director KYC | DIR-3 KYC | By 30 September annually |

| Board meetings | — | Minimum 4 per year |

Non-compliance with ROC filings attracts additional fees that accumulate quickly. Filing on time is consistently the lower-cost, lower-risk approach.

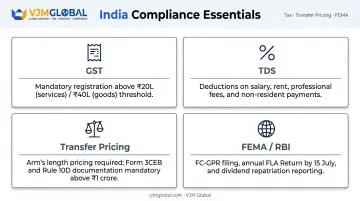

GST, TDS, and Transfer Pricing

- GST registration is mandatory once taxable turnover exceeds ₹20 lakh for services or ₹40 lakh for goods-only businesses (lower thresholds apply in special category states)

- TDS must be deducted and remitted on salary, rent, professional fees, and payments to non-residents

- Transfer pricing: All transactions between the Indian subsidiary and Singapore parent must be at arm's length and fully documented

- Under Section 92E, companies with international transactions must file Form 3CEB (certified by a Chartered Accountant); Rule 10D mandates formal transfer pricing documentation for transactions exceeding ₹1 crore

Ongoing FEMA Compliance

Beyond the initial FC-GPR filing, the Indian Pvt Ltd must:

- File the Annual Return on Foreign Liabilities and Assets (FLA Return) with the RBI — see the RBI FLA Return guidelines for submission details (due 15 July each year)

- Submit fresh FC-GPR filings for any subsequent capital infusion from the Singapore parent

- Comply with FEMA reporting requirements for dividend repatriation and any changes in shareholding structure

VJM Global provides end-to-end post-incorporation compliance support for Singapore-owned Indian subsidiaries, covering ROC filings, GST, TDS, transfer pricing documentation (including Master File, Local File, CbCR, and Form 3CEB), and RBI/FEMA reporting.

Frequently Asked Questions

Why are Indian companies registered in Singapore?

Indian-origin companies incorporate in Singapore to access international venture capital, benefit from Singapore's zero capital gains tax environment, and position the Singapore entity as a regional holding company for Asia-Pacific operations. This is the reverse of what this article covers — here, we address Singapore companies registering a subsidiary in India.

What is the role of a Singapore Pte Ltd in an India entry structure?

A Singapore Private Limited Company (Pte Ltd), regulated by ACRA under the Companies Act 1967, commonly serves as the holding entity above an Indian Pvt Ltd — with the Pte Ltd owning shares in the Indian operating subsidiary. This dual-entity structure is a standard approach for Singapore companies entering India.

Can a Singapore company own 100% of an Indian Private Limited Company?

Yes. A Singapore company can own 100% of an Indian Pvt Ltd through the automatic FDI route in most sectors, with no prior government approval needed. The investment must comply with FEMA pricing guidelines. The Indian company must also file Form FC-GPR with RBI within 30 days of share allotment.

How long does it take to register a Private Limited Company in India for a Singapore company?

The MCA filing process typically takes 7–15 business days once documents are ready. The pre-filing stage — apostillation of Singapore documents and obtaining DSCs for foreign directors — adds 5–10 additional days. Plan for a total timeline of 3–4 weeks from the start of document preparation.

What documents does a Singapore company need to register an Indian Pvt Ltd?

Core documents include:

- Apostilled passport copies and proof of address for all Singapore-based directors and shareholders

- Notarised copy of the Singapore parent company's Certificate of Incorporation

- Indian registered office address proof (utility bill plus rent agreement or NOC)

- Passport-size photographs of all directors

Is there a minimum capital requirement to register a Private Limited Company in India?

There is no statutory minimum paid-up capital since the 2015 amendment — a company can be incorporated with ₹1. However, any capital remitted from Singapore must be at fair market value per RBI pricing guidelines, and the authorised capital determines the government fee structure at incorporation.