Introduction

Singapore's audit firms and corporate finance teams face mounting pressure from multiple directions. ACRA compliance deadlines arrive with unforgiving regularity, professional fees continue climbing, and the talent pool keeps shrinking in one of Asia's most stringently regulated financial hubs. ACRA's Audit Quality Indicators reveal the scale of the problem: attrition rates at non-Big Four firms auditing listed companies hit 49% in the 12-month period ending September 2022, up from 31% in 2020. That's not a staffing footnote — it's a structural vulnerability firms can't absorb during peak filing periods.

Cost reduction is the headline most firms hear first. But the operational case runs deeper: scalable capacity during ACRA filing windows, faster working paper turnaround, and senior auditors freed from preparation work to focus on judgment-intensive review.

This article covers which advantages actually move the needle and how Singapore firms are putting them to work.

Key Takeaways

- India's salary differential cuts audit staffing costs by up to 75% compared to Singapore hires

- The 2.5-hour time gap enables same-day turnaround—assign work in the afternoon, receive completed output by morning

- On-demand scalability handles ACRA filing surges without permanent headcount additions

- Indian teams trained in IFRS and Singapore Financial Reporting Standards maintain quality while your in-house staff focuses on client relationships

What Is Audit Support Outsourcing to India?

Audit support outsourcing means Singapore firms delegate specific audit functions to a qualified team based in India, operating as an extension of the in-house team. The scope typically covers:

- Working paper preparation and audit file assembly

- Financial statement reconciliation and variance analysis

- Compliance documentation and regulatory filing support

- Audit sampling design and substantive testing

- Vouching, confirmations, and data testing

These are high-volume, time-intensive tasks that consume junior and mid-level auditor capacity.

This is not about replacing statutory auditors, who must remain licensed in Singapore under ACRA regulations. Singapore's Accountants Act requires all statutory audits to be signed by a Public Accountant registered with ACRA. Outsourcing handles preparation and support work only; sign-off authority stays exclusively with the Singapore-registered PA.

Think of it as a delivery model that reallocates where effort goes. Senior auditors stay focused on client management, regulatory oversight, and complex professional judgments. The offshore team handles the groundwork.

VJM Global's audit support team, for example, prepares workpapers, runs confirmations, and executes data testing aligned to SFRS, IFRS, and PCAOB standards where applicable — giving Singapore teams more capacity for the work that requires local presence and professional judgment.

Key Advantages of Outsourcing Audit Support to India for Singapore Firms

The advantages below are grounded in operational outcomes Singapore firms track: cost per audit, turnaround time, audit quality scores, staff utilisation, and scalability during peak periods — not abstract efficiencies.

Advantage 1: Substantial Cost Savings Without Compromising Audit Quality

Singapore's professional accounting labour costs rank among the highest in Asia. According to the Robert Half 2026 Singapore Salary Guide, a Senior Accountant earns SGD 80,000–95,000 annually. Internal Audit is explicitly flagged as an in-demand role, with talent shortages driving salary inflation.

Outsourcing to India creates this cost advantage: Indian Chartered Accountants with equivalent qualifications deliver the same output at significantly lower cost due to wage structure differences. ICAI campus data from May 2025 shows newly qualified CAs averaging approximately INR 12.96 LPA (roughly SGD 20,700). At mid-range comparison—SGD 90,000 for a Singapore Senior Accountant versus SGD 20,700 for an Indian CA—the differential is roughly 75% on base salary alone.

Fully-loaded costs (including Singapore's employer CPF contributions of up to 17%, office space, benefits, and management overhead) reduce this gap, but the cost advantage remains substantial.

The compounding effect:

- Cost savings freed from audit overhead can be redirected toward advisory services, technology upgrades, or client acquisition

- Lower cost per file processed allows Singapore firms to take on more clients without proportionally increasing headcount

- Deloitte's 2024 Global Outsourcing Survey confirms 80% of executives plan to maintain or increase outsourcing investment, citing skilled talent access alongside cost as primary drivers

KPIs impacted:

- Cost per audit engagement

- Overhead-to-revenue ratio

- Staff utilisation rate

Best fit:

Small-to-mid-sized Singapore audit firms facing growing client workloads without the justification for additional full-time hires benefit most. The cost structure lets firms absorb volume increases without fixed overhead expansion.

Advantage 2: Access to IFRS/SFRS-Aligned Expertise and Specialist Audit Knowledge

India produces a large pool of audit-qualified professionals annually. ICAI is the second-largest professional accounting body globally with over 400,000 members and a combined network of 1.4 million members and students.

For context, Singapore's entire Public Accountant base stands at just 1,232 individuals as of March 2024 — India's qualified accountant population is roughly 10 times Singapore's entire ISCA membership of 38,000.

Singapore's financial reporting standards (SFRS) are substantively converged with IFRS, making Indian audit professionals directly applicable to Singapore engagements. The Accounting Standards Council confirms that SFRS(I) is essentially identical to IFRS.

ICAI's CA curriculum mandates Ind AS (Indian Accounting Standards converged with IFRS) at the Final examination level, meaning practising Indian CAs routinely work with IFRS-converged standards.

How this expertise gets delivered in practice:

Indian audit support teams can be briefed on Singapore-specific ACRA requirements, SSAs (Singapore Standards on Auditing), and client-specific templates, then integrated into existing workflows using shared platforms and SOPs. VJM Global's team, with 30+ years of audit and tax experience, demonstrates this depth—100+ accounting professionals trained in IFRS, U.S. GAAP, and PCAOB standards, capable of preparing GAAP/IFRS-compliant financial statements with full transparency.

What this means in practice:

- Deep specialist knowledge — industry-specific audit procedures, forensic audit support, IT audit documentation — becomes available without local recruiting

- Skills that are expensive or slow to build in-house are accessible on demand

- Teams trained in global standards reduce documentation errors and missed compliance checkpoints

KPIs impacted:

- Audit error rates

- Documentation quality scores

- Compliance pass rates

- Rework instances

Best fit:

Most impactful during complex or multi-entity audit engagements where Singapore firms need specialist capacity without permanent headcount. VJM Global's experience with group audits, multinational subsidiaries, and cross-border reporting reflects the depth of expertise available through Indian outsourcing partners.

Advantage 3: Faster Turnaround and On-Demand Scalability During Peak Audit Seasons

Speed and expertise reinforce each other — but scalability on short notice is where the time zone advantage becomes concrete.

Singapore Standard Time (SGT) is UTC+8. India Standard Time (IST) is UTC+5:30. The 2.5-hour difference allows meaningful same-day collaboration — Singapore teams can assign work in the afternoon and receive completed output the following morning. This creates an effective extended working day without overtime costs, unlike outsourcing to Western time zones with 8–12 hour gaps.

Indian outsourcing firms can deploy additional audit staff for peak ACRA filing windows or year-end surges within days — without the Singapore firm running a full hiring cycle. For context, non-listed companies must file annual returns within 7 months after financial year-end under Section 197 of the Companies Act. For a December year-end company, that deadline falls in July, coinciding with peak season for many firms.

The deadline stakes:

- Outsourcing absorbs ACRA filing volume spikes without sacrificing turnaround time or quality

- Missing deadlines carries escalating penalties: SGD 300 for up to 3 months late, SGD 600 beyond 3 months, plus composition sums of at least SGD 500 each for late AGMs and late annual returns

- Directors with three or more filing offences within five years face disqualification

- Consistent turnaround through outsourcing directly reduces this exposure

KPIs impacted:

- Audit cycle time

- On-time delivery rate

- Peak season capacity utilisation

- ACRA filing compliance rate

Best fit:

Firms with seasonal audit spikes — financial year-end clusters, IPO audit support, or multi-client concurrent audits — benefit most. India's talent pool (400,000+ CAs, 850,000+ active students) provides qualified professionals at a scale Singapore's market of 1,232 PAs cannot match, enabling rapid staffing during peak periods.

What Happens When Singapore Firms Avoid Outsourcing Audit Support

Singapore firms that build and maintain fully in-house audit support teams face escalating salary costs, benefits, and recruitment fees. This is particularly acute given the documented accounting talent shortage. ISCA identifies "Developing the Talent Pipeline" as a strategic priority, investing SGD 15 million in candidate support, while students increasingly choose Data Science and Environmental Sustainability over Accountancy.

Quality and Consistency Risks From Capacity Constraints

Without scalable support, in-house teams stretched thin during peak periods commonly produce:

- Higher error rates and incomplete documentation

- Increased rework that elevates overall audit risk

- Greater ACRA non-compliance exposure across client portfolios

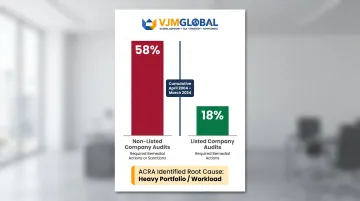

ACRA's Audit Regulatory Report 2024 makes this concrete: 58% of non-listed company audit inspections (cumulative April 2004 to March 2024) required remedial actions or sanctions, versus only 18% for listed company audits.

ACRA explicitly recommends that firms investigate root causes such as "heavy portfolio/workload" rather than defaulting to generic explanations like "lack of supervision." A peer-reviewed study by Christensen et al. (2021), published in Accounting, Organizations and Society and cited 178 times, confirms this: heavier team workloads are associated with lower audit quality, particularly when team members have lower performance ratings.

The Growth Ceiling That Follows

Capacity strain doesn't just create compliance risk — it caps growth. Firms that can't scale audit delivery affordably are limited in how many clients they can serve, which directly restricts revenue without outsourcing as a lever.

The opportunity cost is equally damaging: senior auditors and partners consumed by routine audit prep cannot focus on strategic advisory, business development, or quality review — the work where Singapore firms actually compete and differentiate.

How Singapore Firms Can Get the Most Value from Audit Support Outsourcing

Audit support outsourcing delivers the most value when the engagement is built on clear processes, consistent governance, and the right partner. Here's how Singapore firms can structure that from day one.

Define Clear SOPs During Onboarding

- Document client-specific templates and formats

- Align the offshore team on Singapore-specific requirements (ACRA filing formats, SSA documentation standards)

- Train on proprietary audit methodologies and platforms

- Establish communication protocols and escalation paths

VJM Global's onboarding process includes adaptation to client audit methodology, training in U.S. GAAP/IFRS/PCAOB standards, and assignment of a dedicated audit coordinator who acts as the primary point of contact.

Implement Ongoing Quality Governance

Once onboarding is complete, the focus shifts to maintaining consistent performance over time. SLA-based reporting, periodic quality reviews, and clear escalation protocols ensure the offshore team delivers reliably — not just at launch. Quality governance mechanisms should include:

- Turnaround time commitments with tracking

- Quality review checkpoints at multiple stages

- Real-time support for clarifying documentation

- Continuous improvement reviews at every level

Choose the Right Partner

Look for providers with demonstrable experience in IFRS/SFRS-aligned audit support, robust data security protocols (given Singapore's PDPA requirements), and proven retention records. Section 26 of the PDPA requires legally enforceable obligations ensuring comparable data protection for overseas transfers — satisfied through contractual clauses, Binding Corporate Rules, or compliance certifications.

VJM Global's 95% client retention rate and 30+ years of experience in audit and financial services set a strong benchmark for what Singapore firms should expect from an outsourcing partner. On the data security front, look for providers offering:

- NDAs and confidentiality contracts

- Secure platforms for storing and transmitting client data

- ISO 27001 certification, which provides a structured ISMS framework that inherently supports PDPA compliance

Conclusion

For Singapore firms, outsourcing audit support to India addresses the real operational pressures local audit teams face: rising workloads, a structural talent gap, and tightening ACRA deadlines. With only 1,232 PAs serving a market where 58% of non-listed audits show quality deficiencies — and annual attrition running at 49% — local hiring alone cannot close the gap.

Outsourcing rarely delivers its full value in a single engagement. The compounding benefits — cost efficiency, deeper expertise, and consistent turnaround — accumulate as processes mature and teams align. Firms that approach it as a long-term delivery model see far better outcomes than those treating it as a seasonal cost lever.

Firms that act now position themselves to handle growing audit workloads, meet ACRA deadlines reliably, and focus senior talent where it matters most: client relationships and complex, judgment-intensive work that no offshore model can replace.

Frequently Asked Questions

Is it legally permissible for Singapore firms to outsource audit support to India?

Yes. While Singapore's statutory audit sign-off must remain with a licensed Public Accountant under ACRA regulations, preparatory and support functions (working papers, reconciliations, documentation) can legally be outsourced to qualified professionals in India.

What types of audit tasks can Singapore firms realistically outsource to India?

Common tasks include:

- Working paper preparation, tie-outs, and reconciliations

- Audit sampling, substantive testing, and vouching

- Compliance documentation and confirmations

- Support for financial statement, compliance, and IT audits

How does the India-Singapore time zone difference affect day-to-day collaboration?

The 2.5-hour gap between IST and SGT creates substantial same-day overlap. Singapore teams can assign work in the afternoon and receive completed output the next morning. That's a more workable arrangement than outsourcing to Western time zones with 8–12 hour differences.

How do Indian audit support teams stay aligned with Singapore's ACRA and SFRS requirements?

SFRS is substantively converged with IFRS, which Indian CAs cover through mandatory Ind AS training. During onboarding, Indian outsourcing partners align their teams to ACRA documentation requirements and SSA standards, including Singapore-specific templates and formats.

What data security measures should Singapore firms require from an Indian outsourcing partner?

Require encrypted data transfer, role-based access controls, NDAs, and ISO 27001 certification. Contractual clauses must address PDPA Section 26, which mandates that overseas data transfers maintain protection comparable to Singapore's standards.

How quickly can an Indian audit support partner scale capacity for peak ACRA filing periods?

Established Indian outsourcing firms can typically onboard additional audit staff within days to weeks—far faster than local hiring cycles—making them particularly effective for absorbing Singapore's seasonal audit volume spikes during ACRA filing windows.