Introduction

The India-UK Double Taxation Avoidance Agreement (DTAA) is the primary bilateral tax treaty ensuring residents of both countries aren't taxed twice on the same income. Signed on January 25, 1993, updated by the 2013 Protocol, and modified by the 2020 Multilateral Instrument (MLI), it remains the governing framework for India-UK cross-border taxation.

Without it, dual tax obligations can erode up to 40% of cross-border income — a real cost that proper treaty protection prevents.

This guide is essential for:

- NRIs living and working in the UK

- UK businesses operating in India

- Indian professionals on UK assignments

- Companies earning income across both jurisdictions

We'll cover applicable tax rates, key articles governing different income types, special provisions, and the exact compliance steps to claim treaty benefits. Whether you're determining if your UK office creates a Permanent Establishment in India or calculating withholding tax on royalties, this guide gives you the answers.

TLDR: Key Takeaways

- The India-UK DTAA eliminates double taxation through tax credits in your country of residence

- Withholding tax is capped at 10–15% on dividends, interest, and royalties — rates vary by income type and payer (full breakdown in the guide)

- A Tax Residency Certificate (TRC) is mandatory to access treaty rates; without it, domestic withholding applies

- Post-2020 MLI updates added anti-avoidance rules that can deny treaty benefits if the main purpose of a transaction is to exploit the treaty

- Work in the other country fewer than 183 days a year? Employment income is typically taxed only in your home country — with conditions

What is the India-UK DTAA? History, Scope, and Taxes Covered

The India-UK Double Taxation Avoidance Agreement (DTAA) is a bilateral tax treaty that prevents the same income from being taxed twice — once in India and once in the UK. The current operative convention replaced the earlier 1981 agreement and comprises 31 Articles. Notified in India via Section 90 of the Income Tax Act, 1961 (Notification No. GSR 91(E), dated 11-2-1994), the treaty has the force of law in India.

Geographic Coverage

United Kingdom covers England, Wales, Scotland, and Northern Ireland — all four constituent nations fall under treaty protection. India refers to the territory of India as defined under its Constitution, including the territorial waters and continental shelf where Indian tax law applies.

Taxes Covered

| Country | Covered Taxes |

|---|---|

| United Kingdom | Income tax, corporation tax, capital gains tax, petroleum revenue tax |

| India | Income tax including surcharge |

The convention applies to any future taxes of substantially similar character imposed after the signing date.

Who Qualifies for Treaty Benefits?

Article 4 defines "resident of a Contracting State" as any person liable to tax by reason of domicile, residence, or place of management. Without established residency in a contracting state, treaty benefits do not apply.

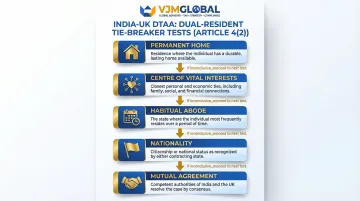

Dual Residency Tie-Breaker Rules

For individuals qualifying as residents of both countries, Article 4(2) applies a hierarchical test:

- Permanent home — the country where you maintain a dwelling that is continuously available to you, not just occasionally used

- Centre of vital interests — where your family, employment, business, and social connections are concentrated

- Habitual abode — the country where you physically spend more time, regardless of where your home is located

- Nationality — applied when habitual abode is inconclusive; the country of which you are a citizen

- Mutual agreement — if all prior tests remain unresolved, the tax authorities of both countries determine residency by direct consultation

For NRIs maintaining homes and financial ties in both countries, this hierarchy is decisive — it determines which country's domestic tax law governs your income and where treaty relief can be claimed.

Key Tax Rates Under the India-UK DTAA at a Glance

The table below shows the maximum withholding rates the source country can apply under the treaty. Where domestic law offers a lower rate, that lower rate applies instead.

| Income Type | Maximum Treaty Rate | Article Reference |

|---|---|---|

| Dividends (General) | 10% | Article 11(2)(b) |

| Dividends (Property Income/REIT) | 15% | Article 11(2)(a) |

| Interest (General) | 15% | Article 12(2) |

| Interest (Bona Fide Bank) | 10% | Article 12(3)(a) |

| Interest (Government/RBI) | 0% | Article 12(3)(b) |

| Royalties (Copyright/Patent/Know-how) | 15% | Article 13(2)(a) |

| Royalties (Equipment Use) | 10% | Article 13(2)(b) |

| Fees for Technical Services (General) | 15% | Article 13(2)(a) |

| Fees for Technical Services (Equipment-linked) | 10% | Article 13(2)(b) |

| Capital Gains | Domestic law applies | Article 14 |

| Employment Income | Residence country (conditions apply) | Article 16 |

Critical notes:

- These are ceiling rates – domestic law may impose lower rates, but the source country cannot exceed the treaty cap

- Treaty rates apply only when you're the beneficial owner of the income and provide a valid TRC

- Without a valid Tax Residency Certificate, India's default TDS rates apply — for example, 20% on royalties under Section 115A versus the 15% treaty cap, and 40% on interest for foreign companies versus the 15% treaty rate

How Key Income Types Are Taxed Under the India-UK DTAA

Dividends and Interest (Articles 11 and 12)

Dividends (Article 11):

When an Indian company pays dividends to a UK resident, both countries may tax the income. India's withholding is capped depending on the dividend type:

- 10% on general dividends

- 15% on property-income dividends from exempt investment vehicles

Indian residents receiving UK dividends are eligible for tax credits equivalent to what a UK resident would receive.

Interest (Article 12):

Interest is primarily taxable in the recipient's country of residence, but the source country retains limited taxing rights:

- 15% general cap on most interest payments

- 10% cap for interest paid to bona fide banking businesses

- 0% (exempt) when paid to governments or the Reserve Bank of India

- Fully exempt for export credit-backed loans guaranteed by UK Export Credits Guarantee Department or India's Export Credits and Guarantee Corporation/EXIM Bank

Royalties and Fees for Technical Services (Article 13)

The 2013 Protocol substantially revised these definitions, creating important distinctions.

Royalties fall into two categories:

- Copyright, patent, trademark, design, secret formula, or commercial/scientific experience – capped at 15%

- Industrial, commercial, or scientific equipment use – capped at 10%

Fees for Technical Services (FTS):

Payments qualify as FTS when services "make available" technical knowledge, experience, skill, know-how, or processes — meaning the recipient can apply that knowledge independently after the engagement ends. This includes development and transfer of technical plans or designs.

FTS rates mirror royalty treatment:

- 15% general cap

- 10% cap when equipment-linked

Explicit FTS exclusions:

- Teaching services in educational institutions

- Services for personal use of the payer

- Employee compensation

- Professional services under Article 15 (lawyers, accountants, architects, engineers)

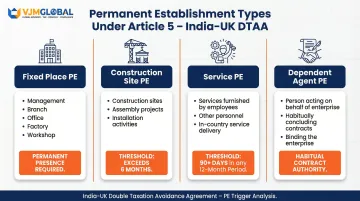

Business Profits and Permanent Establishment (Articles 5 and 7)

Article 7 establishes a fundamental principle: a UK enterprise's profits are taxable in India only if it operates through a Permanent Establishment (PE) in India. Without a PE, profits are taxable exclusively in the UK.

What constitutes a PE under Article 5:

| PE Type | Threshold |

|---|---|

| Fixed Place | Place of management, branch, office, factory, workshop |

| Construction Site | Exceeds 6 months duration |

| Service PE | Services furnished for more than 90 days in any 12-month period |

| Dependent Agent | Person habitually concluding contracts on behalf of the enterprise |

What does NOT create a PE:

- Facilities used solely for storage or display

- Fixed place used only for purchasing goods or collecting information

- Preparatory or auxiliary activities

Employment and Personal Services Income (Articles 15 and 16)

Dependent Personal Services / Employment Income (Article 16):

Employment income is taxable only in the employee's country of residence, unless work is physically performed in the other country. The other country's tax exemption applies only when all three conditions are met simultaneously:

- The employee is present there fewer than 183 days in the fiscal year

- The employer is not resident in that country

- Remuneration is not borne by a PE in that country

Note: If a UK employer has an Indian PE that bears the salary cost, the exemption fails — even if the employee spends only 100 days in India.

Independent Personal Services (Article 15):

Self-employed professionals (physicians, lawyers, engineers, architects, accountants) are taxable in the other country only if:

- Present there more than 90 days in a fiscal year, OR

- A fixed base is regularly available there

VJM Global assists UK businesses in structuring their India presence (liaison office, branch, or subsidiary) to correctly determine PE exposure and confirm DTAA applicability before operations begin.

Special Provisions: Students, Teachers, and Government Employees

Students and Trainees (Article 21)

Students: Indian students in the UK are exempt from UK tax on:

- Gifts from abroad for maintenance or education

- Scholarships

- Personal service income up to £750 per fiscal year

- Exemption applies for a maximum of 5 years

Trainees: Those under contract for up to 12 months are exempt on income up to £1,500.

Teachers and Researchers (Article 22)

Individuals visiting the other country to teach or conduct research at recognised educational institutions are exempt from tax on teaching/research remuneration for up to 2 years, as long as the research serves public interest.

Government Employees (Article 19)

Key rules for government employees:

- Salaries paid to nationals serving the home government in the other country are exempt from tax in that other country

- Pensions paid by a government are taxable only in the paying government's country

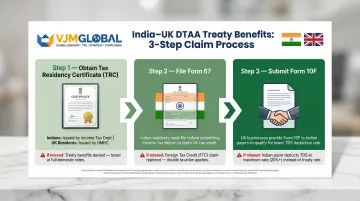

How to Claim DTAA Benefits Between India and UK

Step 1: Obtain a Tax Residency Certificate (TRC)

The TRC is your passport to treaty benefits. Issued by:

- Indian residents: Income Tax Department

- UK residents: HMRC

TRC contains:

- Name and address

- Residential status

- PAN or tax identification number

- Period of validity

Without a valid TRC, the payer must apply domestic withholding rates – often 20-30% – instead of the lower treaty rate.

Step 2: File Form 67 (For Indian Residents Claiming UK Tax Credit)

Indian residents claiming credit for UK taxes paid must file Form 67 on the Indian income tax portal before or at the time of filing their income tax return. This form discloses foreign income and the foreign tax credit being claimed.

Failure to file Form 67 on time results in denial of credit even if you're entitled under the DTAA.

Step 3: Provide Form 10F to Indian Payers (For UK Businesses/Individuals)

UK businesses and individuals receiving payments from India must provide Form 10F (self-declaration of residence status) along with the TRC to the Indian payer – bank, employer, or company. This enables the payer to deduct TDS at the lower treaty rate instead of the higher domestic rate.

Getting these three steps right — in the correct sequence and before the first payment is made — is what determines whether you actually receive the treaty rates the DTAA provides. VJM Global works with UK businesses on exactly this process, from TRC procurement through Form 10F submission, to make sure compliance is in place before it becomes a problem.

Impact of the 2020 Multilateral Instrument (MLI) on the India-UK DTAA

The OECD's Multilateral Instrument (MLI), ratified by both India and the UK, modified the 1993 India-UK DTAA effective:

- January 1, 2020 for withholding taxes

- April 1, 2020 for all other taxes in India

The MLI does not replace the original convention but applies alongside it as a synthesised text.

Key Changes Introduced by the MLI

The MLI introduced three substantive changes that affect how the treaty is applied:

- Principal Purpose Test (PPT): Treaty benefits can be denied if securing the benefit was one of the principal purposes of an arrangement. Structures lacking genuine commercial substance — set up primarily to exploit treaty access — face denial under this anti-avoidance rule.

- Dual-Resident Company Tie-Breaker: Previously, dual-resident companies defaulted to the country of "place of effective management." The MLI replaces this with a mutual agreement procedure, where competent authorities decide by consensus rather than applying a fixed automatic rule.

- Transparent Entities and PE Anti-Abuse: Updated provisions prevent treaty benefits from being claimed through transparent entities such as partnerships or trusts, and close off artificial permanent establishment arrangements.

The 2013 Protocol

The MLI sits on top of earlier amendments — most notably the 2013 Protocol (entered into force December 27, 2013), which amended Article 13 and updated definitions of royalties and technical services. The operative document today is the 1993 convention as amended in 2013, read together with the 2020 MLI synthesised text.

Frequently Asked Questions

What is the tax rate under the DTAA between India and the UK?

Key withholding tax rates are: dividends up to 10% (general) or 15% (property income), interest up to 15% (10% for banks, 0% for governments), royalties/technical fees 15% (10% for equipment royalties). Capital gains are taxed under the domestic law of the source country with no treaty cap.

How can I avoid double taxation between India and the UK?

The DTAA eliminates double taxation through the foreign tax credit mechanism (Article 24): tax paid in the source country is credited against tax liability in the country of residence, so you effectively pay tax only once. Obtain a TRC and file Form 67 (for India) to claim this credit.

Do I need to pay tax in India if I work in the UK?

Indian tax residents are taxed on global income, including UK salary. Tax paid in the UK is creditable in India under Article 24, so you pay tax only once. If you become a non-resident of India, Indian tax applies only to India-sourced income.

Is TDS applicable for services rendered outside India?

TDS under Section 195 applies to non-resident payments only when income arises in India. Services rendered entirely outside India are generally not subject to TDS — submit a TRC and Form 10F to claim the exemption or reduced rate.

What is Article 7 of the DTAA between India and the UK?

Article 7 governs Business Profits: a UK company's profits are taxable in India only if it has a Permanent Establishment (PE) in India, and even then, only profits attributable to the PE are taxed. Without a PE, all business profits are taxable exclusively in the UK.

What is the new agreement between India and the UK?

The most recent DTAA update was the 2020 Synthesised Text incorporating the OECD Multilateral Instrument (MLI), which introduced anti-avoidance rules including the Principal Purpose Test. Separately, India and the UK signed a trade agreement (CETA) in July 2025, though it remains distinct from the DTAA and is not yet in force.

Need help navigating India-UK DTAA compliance? VJM Global's team of chartered accountants and international tax specialists has helped 250+ UK businesses structure their India operations, claim treaty benefits, and manage cross-border tax obligations. From TRC procurement to Form 10F filing and PE determination, we handle compliance on both sides so you capture every benefit the treaty allows. Contact our expert team today.