Introduction

A US software company contracts with an Indian client for cloud hosting services worth $50,000. The American finance team expects the full payment—but instead receives $40,000. Why? The Indian client withheld 20% tax at source under India's TDS (Tax Deducted at Source) regime. Had the company understood India's withholding tax (WHT) rules and obtained a Tax Residency Certificate to claim benefits under the India-US treaty, the effective rate could have been just 10%—a difference of $5,000.

This scenario plays out regularly for unprepared US, UK, and Australian businesses doing business with India. Whether your Indian contracts involve royalties, technical service fees, interest, or dividends, missing the treaty claim means overpaying—and recovering withheld tax after the fact is a slow, bureaucratic process.

This guide covers what foreign companies need to know before they sign:

- Domestic WHT rates for residents and non-residents

- Treaty rates under India's 90+ Double Taxation Avoidance Agreements (DTAAs)

- Finance Act 2025 changes effective April 1

- Compliance steps to claim treaty benefits and protect cash flow

What Is Withholding Tax in India?

Withholding tax in India — officially called Tax Deducted at Source (TDS) — is an advance tax collection mechanism. Any person (individual, company, or entity) making specified payments must deduct tax before releasing payment and remit the deducted amount directly to the Indian government on the recipient's behalf.

Legal Basis and Scope

WHT in India is governed by the Income Tax Act, 1961. The regime applies to both domestic and cross-border payments, covering:

- Interest (on loans, deposits, bonds)

- Royalties (IP licensing, patents, trademarks)

- Fees for Technical Services (FTS) (consultancy, engineering, managerial services)

- Dividends (profit distributions)

- Rent (land, buildings, machinery)

- Professional/contractual payments (freelancers, contractors)

- Capital gains (sale of shares, property)

- Winnings from online gaming and other specified income

Who Must Comply?

- Indian businesses making payments to resident vendors or contractors

- Indian entities paying foreign companies for services, royalties, or interest

- Non-resident companies with Indian operations or a permanent establishment making specified payments

Once you establish who must deduct, the next question is how much. The applicable WHT rate is always the lower of the domestic Income Tax Act rate or the relevant DTAA treaty rate. For non-residents, correctly invoking a tax treaty requires meeting specific procedural requirements — including furnishing a Tax Residency Certificate (TRC) and Form 10F — before the lower rate applies.

WHT Rates on Payments to Indian Resident Companies

India applies different WHT rates and thresholds depending on payment type. WHT is triggered only when cumulative payments to a single payee within the financial year (April 1 to March 31) exceed the prescribed limit.

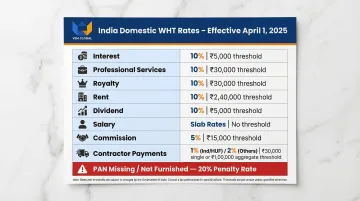

Domestic Resident WHT Rates (Effective April 1, 2025)

| Payment Type | Threshold (INR) | WHT Rate | Section |

|---|---|---|---|

| Purchase of goods | 5,000,000 | 0.1% | 194Q |

| Interest (bank/co-operative/post office) | 50,000 | 10% | 194A |

| Interest (senior citizens) | 100,000 | 10% | 194A |

| Interest (other cases) | 10,000 | 10% | 194A |

| Professional services | 50,000 | 10% | 194J |

| Technical services | 50,000 | 2% | 194J |

| Royalty | 50,000 | 10% | 194J |

| Commission/brokerage | 20,000 | 5% | 194H |

| Rent (land/building/furniture) | 50,000/month | 10% | 194-I |

| Rent (plant/machinery) | 50,000/month | 2% | 194-I |

| Contract payments | 30,000 (single) / 100,000 (annual) | 2% | 194C |

| Dividend income | 10,000 | 10% | 194 |

| Winnings from online gaming | No threshold | 30% | 194BA |

CRITICAL THRESHOLD RULE: Once total payments cross the threshold, WHT applies to the entire amount, not just the excess. If you pay a vendor INR 49,000 across the year, no WHT applies. If the next payment brings the total to INR 51,000, you must deduct WHT on the full INR 51,000.

The PAN Requirement

Every recipient (deductee) must furnish their Permanent Account Number (PAN) to the payer. If the recipient fails to provide a PAN, the WHT rate jumps to the higher of:

- The prescribed rate (from the table above)

- The rate in force for that payment type

- 20%

For a professional services payment where the normal rate is 10%, failure to provide PAN triggers 20% withholding—doubling the deduction.

Higher TDS for Non-Filers (Repealed April 1, 2025)

A separate compliance layer — now removed — previously targeted taxpayers who hadn't filed returns for three consecutive years.

Until March 31, 2025, Sections 206AB and 206CCA imposed higher TDS rates on "specified non-filers" — individuals or entities who had not filed income tax returns for the past three consecutive years. The rate was the higher of:

- Twice the prescribed rate

- Twice the rate in force

- 5%

The Finance Act 2025 has omitted Sections 206AB and 206CCA effective April 1, 2025. Payers no longer need to verify a deductee's return-filing history before applying the standard WHT rate.

Special Cases

- Call center companies qualify for a reduced 2% WHT rate on contract payments

- Cash withdrawals exceeding INR 20 million (for filers) or INR 10 million (for non-filers) attract 2%–5% WHT

WHT Rates on Payments to Non-Resident Companies

Unlike resident payments, there is no minimum threshold for non-residents. Tax must be deducted from the first rupee of payment.

Non-Resident WHT Rates (Effective 2025)

| Payment Type | Domestic WHT Rate | Section |

|---|---|---|

| Interest on foreign currency loans/bonds | 5% | 194LC |

| Interest on IFSC long-term bonds (issued before July 1, 2023) | 4% | 194LD |

| Interest on IFSC long-term bonds (issued after July 1, 2023) | 9% | 194LD |

| Interest (non-specified, foreign currency) | 20% | 195 |

| Royalty and fees for technical services (FTS) | 20% | 195 |

| Dividend income | 20% | 195 |

| Long-term capital gains (other than equity) | 12.5% | 195 |

| Long-term capital gains (equity shares/equity funds) | 12.5% | 195 |

| Winnings from online gaming/horse races | 30% | 195 |

| Other income | 35% | 195 |

The Finance Act 2023 Rate Increase

Before April 1, 2023, royalties and FTS paid to non-residents were subject to just 10% WHT. The Finance Act 2023 doubled this rate to 20%, raising the cost of India-sourced income for foreign service providers.

This change has made claiming DTAA treaty benefits essential for most non-residents, as treaty rates typically range from 10% to 15%—half the domestic rate.

Surcharge and Health & Education Cess

The base WHT rates above are further increased by:

- Surcharge: 2% (for income up to INR 10 million) or 5% (above INR 10 million)

- Health & Education Cess (HEC): 4% of the total tax plus surcharge

Effective rate calculation example (20% base rate):

- Base WHT: 20%

- Add 2% surcharge: 20% + (20% × 2%) = 20.4%

- Add 4% HEC: 20.4% + (20.4% × 4%) = 21.216% effective rate

For higher income levels with 5% surcharge, the effective rate becomes 21.84%.

Return Filing Exception for Non-Residents

If WHT is correctly deducted at the domestic rate on dividends, interest, royalties, or FTS, and the non-resident has no other Indian-source income, they are not required to file an Indian tax return. This exception simplifies compliance for these payment scenarios. That said, claiming treaty benefits does require return filing, which is covered in the next section.

PAN Requirement for Non-Residents

Non-residents without a PAN face WHT at the higher of the prescribed rate, rates in force, or 20%. The government has issued rules allowing PAN exemption in certain notified cases, but eligibility depends on the specific payment type and bilateral agreements in place. A qualified international tax advisor — such as VJM Global's cross-border tax team — can confirm whether the exemption applies to your situation.

How DTAA Treaty Rates Can Reduce Your WHT Liability

India has signed Double Taxation Avoidance Agreements (DTAAs) with over 90 countries. Under Section 90 of the Income Tax Act, a non-resident can choose to be taxed under domestic law or the applicable DTAA—whichever is more beneficial.

Crucially, surcharge and cess do not apply when the treaty rate is used, making treaty claims even more attractive.

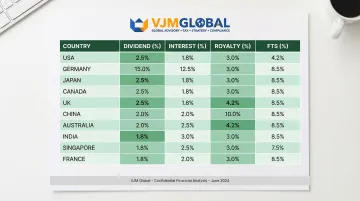

DTAA Treaty Rates by Country

| Country | Dividend | Interest | Royalty | FTS |

|---|---|---|---|---|

| United States | 15% / 25% | 10% / 15% | 10% / 15% | 10% / 15% |

| United Kingdom | 10% / 15% | 10% / 15% | 10% / 15% | 10% / 15% |

| Australia | 15% | 15% | 10% / 15% | 10% / 15% |

| Singapore | 10% / 15% | 10% / 15% | 10% | 10% |

| UAE | 10% | 5% / 12.5% | 10% | No FTS article |

| Germany | 10% | 10% | 10% | 10% |

| Netherlands | 10% | 10% | 10% | 10% |

| Japan | 10% | 10% | 10% | 10% |

| Canada | 15% / 25% | 15% | 10% / 15% | 10% / 15% |

| France | 10% | 10% | 10% | 10% |

Example: A UK consultancy receives INR 10,00,000 (£10,000) in fees for technical services from an Indian client.

- Domestic rate: 20% base + surcharge + cess = 21.216% effective = INR 2,12,160 (£2,122)

- India-UK DTAA rate: 15% (no surcharge/cess) = INR 1,50,000 (£1,500)

- Tax savings: INR 62,160 (£622) or 29% reduction

Documentation Required to Claim DTAA Benefits

To claim the lower treaty rate, the non-resident must provide:

Tax Residency Certificate (TRC) — issued by your home country's tax authority (such as US Form 6166 or the UK Certificate of Residence), confirming tax residency during the relevant financial year

Form 10F — filed electronically on the Indian income tax portal with your name, address, tax ID, and residency period. Indian PAN registration is required before filing

No Permanent Establishment Declaration — a signed statement confirming you have no fixed place of business in India, such as a branch or office

The Compliance Trade-Off

Claiming DTAA benefits triggers mandatory Indian tax return filing, PAN registration, and digital signature requirements—even if you have no other Indian-source income.

Whether the effort is worthwhile depends on the numbers. Treaty rates typically reduce withholding by 5%–10% on the gross payment. Weigh that against the compliance cost of Indian registration, Form 10F filing, and tax return preparation. For ongoing engagements or large payments, the savings justify the effort. For one-off small transactions, accepting the domestic rate is often simpler.

VJM Global has guided 500+ US, UK, and Australian businesses through this process—handling TRC coordination, Form 10F filing, PAN registration, and refund claims under one roof.

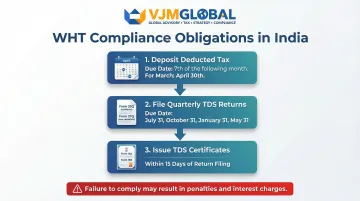

Compliance Requirements for WHT in India

Payer's Obligations

The entity deducting WHT must:

Deposit deducted tax with the Indian government by:

- The 7th of the following month (for April–February deductions)

- April 30 (for March deductions)

File quarterly TDS returns:

- Form 26Q for payments to Indian residents

- Form 27Q for payments to non-residents

- Due dates: July 31, October 31, January 31, and May 31

Issue TDS certificates:

- Form 16A (for most payments) or Form 16B (for immovable property purchases)

- Must be issued within 15 days of filing the quarterly return

Late deposit or filing attracts interest at 1%–1.5% per month, with penalties up to the full amount of TDS.

Deductee/Payee's Obligations

Recipients should:

- Verify deductions by checking Form 26AS (Annual Tax Statement) or the Annual Information Statement (AIS) on the income tax portal

- Claim credit for WHT when filing their annual tax return

- File refund claims if WHT was over-deducted

Refund process for non-residents:

- File an Indian income tax return (ITR) electronically

- Attach supporting documents (TDS certificates, invoices, treaty claim documents)

- Open an Indian bank account to receive the refund

- Wait 6–12 months for processing (longer if incomplete or under scrutiny)

Certificate for Lower or Nil WHT

Cash flow disruption is a real concern when WHT is deducted at full rates across multiple payments. Non-residents (or residents) can apply under Section 197 to the local Indian tax officer for a certificate authorizing WHT at a lower rate or nil.

Benefits:

- Correct WHT rate applied from the first payment

- No need to wait 6–12 months for a refund

- Reduced compliance friction for both payer and recipient

Process: Submit an application online with supporting documents (TRC, treaty claim justification, financial statements). The officer typically responds within 30–60 days.

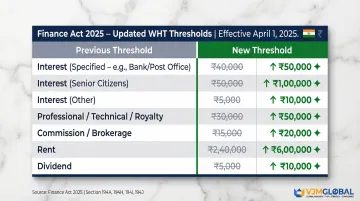

Finance Act 2025: Key Changes to India's WHT Regime

The Finance Act 2025 introduces significant threshold revisions effective April 1, 2025, reducing compliance burdens and easing WHT obligations for domestic transactions.

Threshold Revisions (Effective April 1, 2025)

Updated thresholds:

- Interest (specified): Raised from INR 40,000 to INR 50,000

- Interest (senior citizens): Raised from INR 50,000 to INR 100,000

- Interest (other cases): Raised from INR 5,000 to INR 10,000

- Professional, technical, and royalty payments: Standardized at INR 50,000 (previously INR 30,000 for professional services)

- Commission/brokerage: Raised from INR 15,000 to INR 20,000

- Rent (land/building/furniture and plant/machinery): Changed from an annual INR 240,000 limit to INR 50,000 per month or part of a month

- Dividend income: Raised from INR 5,000 to INR 10,000

These changes reduce unnecessary WHT deductions on smaller transactions and ease compliance for small vendors. Finance and accounts payable teams should verify that ERP systems already reflect the new thresholds — any outstanding configurations need immediate reconciliation.

Omission of Higher TDS Provisions for Non-Filers

Sections 206AB and 206CCA, which imposed higher TDS/TCS rates on specified non-filers, are entirely omitted effective April 1, 2025. Payers no longer need to verify deductees' filing history before applying WHT rates.

Removal of TCS on Sale of Goods

Section 206C(1H), which mandated 0.1% TCS on the sale of goods exceeding INR 50 lakh, is removed effective April 1, 2025. This eliminates the compliance overlap with Section 194Q (which requires buyers to deduct TDS on large purchases).

Updated LRS and Overseas Tour Package TCS

Liberalized Remittance Scheme (LRS):

- New threshold: INR 10 lakh (raised from INR 7 lakh)

- Education/medical remittances: 5% TCS above INR 10 lakh

- Other purposes: 20% TCS above INR 10 lakh

Overseas tour packages:

- Up to INR 10 lakh: 5% TCS

- Above INR 10 lakh: 20% TCS

Foreign exchange platforms and travel booking systems should already reflect these revised rates. Confirm current configurations align with the updated thresholds to avoid over- or under-collecting TCS.

Frequently Asked Questions

How is withholding tax calculated in India?

WHT is calculated by applying the prescribed rate under the Income Tax Act—or the lower applicable DTAA rate—to the gross payment amount. For non-residents, the base rate is increased by surcharge (2%–5%) and Health & Education Cess (4%) to arrive at the effective rate, unless a DTAA rate is claimed.

Who needs to pay withholding tax?

The obligation to withhold (deduct) and deposit WHT falls on the payer—any person, company, or entity making specified payments to residents or non-residents. The recipient (deductee) then claims credit for the deducted tax when filing their return.

Do I have to withhold taxes from payments to a foreign company?

Yes. If an Indian entity (or a non-resident with a business connection in India) makes a payment for Indian-sourced income to a foreign company—such as royalties, FTS, interest, or dividends—WHT must be deducted at source, typically at 20% under domestic law or a lower DTAA rate if applicable.

How are dividends taxed in India?

Dividends paid to Indian residents attract 10% WHT above the ₹10,000 threshold. For non-residents, dividends are subject to 20% WHT under domestic law, or a lower rate (typically 5%–15%) under an applicable DTAA. The Dividend Distribution Tax (DDT) regime was abolished from April 1, 2020.

Can I claim foreign withholding tax back?

Yes. A non-resident can file an Indian income tax return to claim a refund if WHT was over-deducted (for example, if the domestic rate was applied instead of the lower DTAA rate). The process typically takes 6–12 months and requires an Indian bank account and PAN; incomplete filings or scrutiny cases can extend this timeline.

How do I get a withholding tax certificate in India?

Payers issue Form 16A (non-salary payments) or Form 16B (immovable property) as the TDS certificate following their quarterly TDS return filing. Non-residents seeking a reduced rate can apply under Section 197 for a lower/nil deduction certificate before payments are made.

VJM Global helps US, UK, and Australian businesses manage India's WHT obligations—covering DTAA treaty claims, TDS compliance, PAN registration, and refund filings. With 30+ years of experience and 100+ tax professionals, we handle the complexity so you stay compliant and minimize your liability. Contact us today to get started.