Introduction

UK GAAP — Generally Accepted Accounting Practice — is the body of accounting standards governing financial reporting for UK-incorporated companies. Overseen by the Financial Reporting Council (FRC), UK GAAP is legally mandated under the Companies Act 2006 for most private companies operating in the United Kingdom. As of March 2025, over 5.4 million companies were registered in the UK, with around 3.4 million using FRS 102 or FRS 105 as their primary reporting framework.

This guide is essential reading for:

- UK-based businesses navigating compliance obligations

- Foreign companies establishing UK operations

- Accountants preparing statutory accounts

- Finance professionals selecting appropriate reporting standards

UK GAAP compliance is not optional. Non-compliance can result in penalties from HMRC, account rejection by Companies House, and director liability under the Companies Act 2006.

TLDR: Key Takeaways

- UK GAAP is legally required for incorporated businesses and consists primarily of Financial Reporting Standards (FRS 100–105)

- Listed companies must use UK-adopted IFRS; private companies typically follow FRS 102 or simplified variants

- The right standard depends on company size: micro-entities, small entities, and larger companies each follow a different FRS tier

- UK GAAP is closer to IFRS than to US GAAP, having been substantially revised in 2015 to converge with international standards

- Late filing triggers automatic penalties from £150 to £7,500 depending on company type

What Is UK GAAP and Why Does It Matter?

If your business is incorporated in the UK or the Republic of Ireland, UK GAAP is not optional — it is the governing framework that determines how your financial statements must be prepared. Built around the requirement to present a "true and fair view" of financial position, it sets the rules for what gets reported and how. Sole traders and unincorporated partnerships fall outside its scope, since the Companies Act 2006 applies only to incorporated entities.

The FRC's Regulatory Role

The Financial Reporting Council (FRC) is the independent body that sets, enforces, and updates UK GAAP standards. It investigates reporting failures, maintains investor confidence, and ensures financial transparency across UK markets. The FRC's most recent scheduled standards update — covering FRS 102 and FRS 105 — was published in 2024 and takes effect on 1 January 2026.

Legal Foundation and Consequences

The Companies Act 2006 makes UK GAAP compliance mandatory for incorporated businesses. Directors have a personal legal duty under Section 414 to ensure financial statements are accurate and present a true and fair view. Non-compliance carries serious consequences:

- Filing late costs private companies £150–£1,500 and public companies £750–£7,500

- Companies House can reject accounts that fail to meet compliance standards

- Directors face personal liability under Section 414 for misleading financial statements

- Non-compliance undermines stakeholder trust and can complicate future financing

Understanding these obligations is the starting point — the sections below cover which specific standards apply to your business and how to meet them.

Key Financial Reporting Standards Under UK GAAP: FRS 100 to FRS 105

UK GAAP comprises six core Financial Reporting Standards (FRS 100–105), each designed for different entity types and reporting needs.

FRS 100: Application of Financial Reporting Requirements

FRS 100 is the overarching application framework. It establishes the principles guiding which standard an entity should apply based on size, nature, and economic complexity. In practice, it determines whether a company falls under FRS 102, FRS 101, FRS 105, or full IFRS.

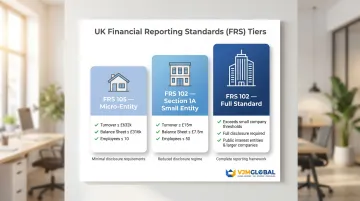

FRS 102: The Primary Standard for Medium and Large Private Companies

FRS 102 is the primary standard for most UK private companies. It covers recognition, measurement, presentation, and disclosure across key areas:

- Revenue recognition (aligned with IFRS 15's five-step model)

- Financial instruments

- Lease accounting (aligned with IFRS 16 principles)

- Employee benefits

FRS 102 Section 1A provides a reduced disclosure regime for small entities meeting specific thresholds. As of 6 April 2025, small companies must meet at least two of these criteria:

- Turnover ≤£15 million (increased from £10.2 million)

- Balance sheet total ≤£7.5 million (increased from £5.1 million)

- Number of employees ≤50

FRS 101: Reduced Disclosure Framework

FRS 101 is designed for UK subsidiaries of groups preparing consolidated accounts under UK-adopted IFRS. It allows subsidiaries to apply IFRS recognition and measurement principles while significantly reducing disclosure obligations, cutting compliance costs without compromising group-level transparency.

FRS 105: Micro-Entity Reporting

FRS 105 is the simplified standard for micro-entities. To qualify, companies must meet at least two of these thresholds:

- Turnover ≤£632,000

- Balance sheet total ≤£316,000

- Number of employees ≤10

Key simplifications under FRS 105:

- No cash flow statement required

- No deferred tax accounting

- Fixed assets recorded at cost (no revaluation option)

- Simplified disclosure notes

FRS 103 and FRS 104: Specialist Standards

These two standards address narrower reporting needs outside the scope of FRS 102:

- FRS 103 (Insurance Contracts): Sector-specific standard for insurance businesses

- FRS 104 (Interim Financial Reporting): Guidance for entities preparing interim reports

Statements of Recommended Practice (SORPs)

Beyond the six FRS standards, SORPs provide industry-specific guidance for sectors where general standards don't fully address unique operational or regulatory issues. The FRC currently recognises seven active SORPs covering:

- Charities (updated SORP effective 2026)

- Housing associations

- Pension schemes

- Investment funds

UK GAAP vs IFRS vs US GAAP: Key Differences Explained

UK GAAP vs UK-Adopted IFRS

Publicly listed companies on UK-regulated markets must use UK-adopted IFRS under the Companies Act 2006 and statutory instrument SI 2019/685. FRS 102, by contrast, is broadly based on IFRS for SMEs but includes UK-specific modifications — making it more practical for private companies operating under domestic rules.

Key distinctions:

- UK-adopted IFRS is broader and more complex; FRS 102 is designed for private companies with reduced disclosure requirements

- Lease accounting under FRS 102 Section 20 has aligned with IFRS 16, bringing most leases onto the balance sheet

- Revenue recognition in FRS 102 Section 23 now mirrors IFRS 15's five-step model

- Financial instruments: FRS 102 uses three simplified measurement categories, while full IFRS 9 applies a more complex classification and impairment model

UK GAAP vs US GAAP

Where IFRS alignment creates common ground between UK GAAP and international frameworks, US GAAP takes a fundamentally different approach — rules-based rather than principles-based, and governed by an entirely separate standard-setting body:

| Aspect | UK GAAP | US GAAP |

|---|---|---|

| Governing Body | Financial Reporting Council (FRC) | Financial Accounting Standards Board (FASB) |

| Terminology | Generally Accepted Accounting Practice | Generally Accepted Accounting Principles |

| Approach | Principles-based | Rules-based |

| Inventory Valuation | LIFO prohibited | LIFO permitted under ASC 330 |

| Alignment | Closer to IFRS | Independent framework |

When UK Businesses Must Convert to IFRS

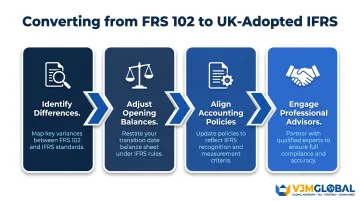

Understanding when the shift from FRS 102 to UK-adopted IFRS becomes necessary helps businesses prepare well in advance. Conversion is typically triggered when:

- Listing on a UK or international stock exchange

- Seeking investment from institutions or funds in IFRS-reporting jurisdictions

- Consolidating financial statements with an IFRS-reporting parent company

- Operating in sectors where lenders or regulators require IFRS-compliant reporting

Conversion steps:

- Identify recognition and measurement differences between FRS 102 and IFRS

- Adjust opening balances and comparative figures

- Align accounting policies with IFRS requirements

- Engage professional advisors experienced in IFRS transitions

The 8 Core Accounting Principles of UK GAAP

While not formally named as standalone rules in UK law, these eight foundational principles are functionally embedded throughout FRS 102:

Foundational Assumptions

- Economic Entity Assumption: Business finances are kept separate from the owner's personal finances

- Monetary Unit Assumption: All transactions are recorded in a stable currency — GBP for UK entities

- Time Period Assumption: Financial results are reported over defined intervals (monthly, quarterly, or annually)

- Cost Principle: Assets are initially recorded at historical cost, which remains FRS 102's default treatment

Transparency and Recognition Principles

- Full Disclosure Principle: All material information must be disclosed to stakeholders — covered under Section 2 of FRS 102

- Going Concern Principle: Accounts assume the business will continue operating (Section 3, paragraphs 3.8–3.9)

- Matching Principle: Expenses are recognised in the same period as the revenue they helped generate

- Revenue Recognition Principle: Revenue is recognised when earned, not when cash is received (Section 23)

Beyond these eight, FRS 102 codifies one additional rule worth noting: the non-offsetting principle (Section 2, paragraph 2.52; Section 3, paragraph 3.7). Assets and liabilities must be reported separately and cannot be netted against each other, except where the standard explicitly allows it.

Staying Compliant with UK GAAP: What Businesses Must Do

Core Compliance Obligations

Under the Companies Act 2006, incorporated businesses must:

- Prepare a complete set of financial statements (balance sheet, income statement, cash flow statement where applicable, statement of changes in equity, and notes)

- Maintain accurate accounting records

- File annual accounts with Companies House within statutory deadlines (9 months for private companies, 6 months for public companies under Section 442)

- Ensure directors sign off on accounts presenting a true and fair view (Section 414)

Common Compliance Pitfalls

- Insufficient training: Staff unaware of recent FRS amendments or Periodic Review changes

- Inconsistent policies: Applying accounting treatments differently across periods

- Legacy systems: Outdated software unable to handle updated recognition or measurement criteria

- Threshold reassessment failures: Not reviewing which FRS applies as the business grows (for example, exceeding micro-entity limits and continuing to use FRS 105)

Professional Support for UK GAAP Compliance

Many of the pitfalls above — missed threshold reviews, inconsistent policies, outdated systems — are easier to avoid with dedicated compliance support. Outsourcing accounting functions to specialists lets UK businesses and foreign companies operating in the UK stay current with FRC updates without diverting internal resources.

VJM Global has supported over 250 UK businesses with accounting outsourcing and compliance services, covering FRS transitions, Companies House filings, and HMRC alignment. VJM Global's team of chartered accountants ensures financial reporting meets UK GAAP standards, reducing the risk of penalties and account rejections.

Frequently Asked Questions

Does the UK follow IFRS or GAAP?

The UK uses both. Publicly listed companies on UK-regulated markets must follow UK-adopted IFRS, while most private incorporated companies follow UK GAAP (primarily FRS 102), which is governed by the FRC.

What accounting rules does the UK use?

UK incorporated businesses must follow Financial Reporting Standards (FRS 100–105) under UK GAAP, or UK-adopted IFRS for listed companies, all underpinned by the Companies Act 2006.

Is UK GAAP the same as US GAAP?

No. UK GAAP (governed by the FRC) aligns more closely with IFRS, while US GAAP (governed by FASB) is more rules-based. The two frameworks differ notably on inventory valuation, lease accounting, and disclosure requirements.

Is IAS the same as IFRS?

International Accounting Standards (IAS) were the predecessor to IFRS. Many original IAS standards remain in force under the IFRS umbrella, but IFRS is the broader, evolving framework that has superseded standalone IAS over time.

What are the basic accounting principles?

The eight core principles embedded in UK GAAP are: Economic Entity Assumption, Monetary Unit Assumption, Time Period Assumption, Cost Principle, Full Disclosure, Going Concern, Matching Principle, and Revenue Recognition.

What are the different types of accounting in the UK?

The main types are: financial accounting (governed by UK GAAP/FRS), management accounting, tax accounting (aligned with HMRC rules), and specialist reporting under SORPs for sectors such as charities, housing associations, and pension funds.