Introduction

When Rajesh, an Indian software engineer working in California, received simultaneous tax demands from both the IRS and India's Income Tax Department on his US salary, he faced a common cross-border dilemma. The solution lies in a 1989 treaty many taxpayers don't know how to use: the India-USA Double Taxation Avoidance Agreement (DTAA).

This bilateral tax treaty, signed in September 1989 and effective from December 1990, establishes a legal framework preventing the same income from being taxed twice across borders. Relief comes through exemptions or foreign tax credits. To benefit, you need to know which income qualifies, what rates apply, and how to file the paperwork correctly.

This guide covers who qualifies for DTAA protection, which income types receive treaty benefits, applicable tax rates, and the exact filing process to claim relief.

TLDR: Key Takeaways on the India-USA DTAA

- Applies broadly: Covers individuals, companies, trusts, and partnerships earning income in both countries

- Protects most income types: Salaries, business profits, dividends (15–25%), interest (10–15%), royalties (10–15%), and capital gains

- Two relief methods: Exemption (income taxed in one country is exempt in the other) or tax credit (offset foreign tax paid against domestic liability)

- Documentation is mandatory: Proof of tax residency — specific forms differ for India filers vs. US filers

- Timing matters: File Form 67 before submitting your ITR to claim foreign tax credit in India

What Is the India-USA DTAA and How Does It Work?

If you earn income across both India and the US, you could face tax bills from both governments on the same money. The Double Taxation Avoidance Agreement (DTAA) is a bilateral treaty that prevents exactly this — stopping the same income from being taxed in both the source country (where income arises) and the residence country (where the taxpayer lives).

Consider an Indian resident receiving rental income from US property. Without the DTAA, they would owe US federal tax on that rent and Indian income tax on the same amount. The treaty eliminates this duplication.

Tax coverage differs by country:

- USA: Applies to Federal Income Tax under the Internal Revenue Code — but excludes accumulated earnings tax, personal holding company tax, and social security taxes

- India: Covers income tax, including surcharge and surtax

Two relief mechanisms:

- Exemption method: The income is taxed once — in the source country — and fully exempt from tax in the other

- Tax credit method: Tax already paid abroad is credited against the domestic tax liability — India primarily uses this approach

Under the credit method, the relief is capped at the Indian tax due on that foreign income — so the credit offsets tax owed but cannot generate a refund exceeding the actual foreign tax paid.

Who Does the India-USA DTAA Apply To?

The DTAA applies to residents of India or the USA — persons liable to tax in either country by reason of domicile, residence, citizenship, or place of management. Knowing whether you qualify determines which treaty benefits you can claim and how your cross-border income gets taxed.

Eligible entities include:

- Individuals (employees, freelancers, retirees)

- Companies (corporations, LLCs)

- Partnership firms

- Trusts

- Any entity earning income in both countries

Some individuals and entities qualify as tax residents in both countries simultaneously. In those cases, the DTAA provides a tie-breaker sequence to establish where you're treated as resident for treaty purposes:

Dual-resident tie-breaker rules:

- Permanent home available to you

- Center of vital interests (closer personal and economic relations)

- Habitual abode

- Nationality

- Mutual agreement between competent authorities

Not everyone with India-USA income exposure can access these benefits. The DTAA excludes:

- Persons taxed only on source-based income (not residence)

- Those unable to produce valid residency documentation

- Claims related to penalties or defaulted taxes

How Key Income Types Are Taxed Under the DTAA

Business Profits and Permanent Establishment (Article 7)

Business profits of a US entity are taxable in India only if the entity has a Permanent Establishment (PE) in India.

What constitutes a PE:

- Fixed place of business (branch, office, factory, workshop)

- Construction, assembly, or installation project lasting more than 120 days in any 12-month period

- Dependent agent operating on behalf of the enterprise

Only profits attributable to the Indian PE are taxable in India. US companies expanding into India must carefully structure operations to manage PE exposure. Misclassification can trigger back taxes, interest, and penalties under Indian domestic law.

Dividends, Interest, and Royalties (Articles 10, 11, and 12)

Dividends (Article 10):

Dividends paid by an Indian company to a US resident are taxable in both countries, but India's withholding is capped:

- 15% if the recipient company holds at least 10% voting stock

- 25% in all other cases

Interest (Article 11):

Interest arising in India and paid to a US resident is taxable in both countries, with India's withholding capped at:

- 10% for loans from banks or financial institutions

- 15% in all other cases

Penalty charges for late payment do not qualify as "interest" under this article — meaning they fall outside the withholding cap and are taxed under domestic rates instead.

Royalties and Fees for Included Services (Article 12):

Payments for royalties or technical services are taxable in both countries, with source-country withholding capped at:

- 10% for industrial, commercial, or scientific equipment use and ancillary services

- 15% for other royalties and technical services

US companies licensing software or technology to Indian entities should confirm whether payments qualify as royalties under Article 12 — the classification determines which withholding cap applies.

Capital Gains, Salaries, and Special Categories

Capital Gains (Article 13):

Each country may tax capital gains according to its domestic law. A US resident selling Indian property faces Indian tax rates:

- 12.5% LTCG (long-term capital gains, without indexation)

- 30% STCG (short-term capital gains)

Beyond capital gains, the DTAA also carves out specific exemptions for individuals on temporary assignments in either country.

Teachers and Professors (Article 22):

Visiting educators at recognized institutions are exempt from tax on teaching/research remuneration for up to 2 years.

Students and Apprentices (Article 21):

Students visiting solely for education are exempt from tax on maintenance, education, or training payments received from outside the host country. This exemption applies regardless of the amount received.

DTAA Tax Rates and How Double Taxation Relief Works

Withholding tax comparison:

| Income Type | DTAA Rate | Without DTAA (India) | Documentation Required |

|---|---|---|---|

| NRO deposit interest | 10–15% | 20% + surcharge/cess | TRC + Form 10F |

| Dividends | 15–25% | 20% + surcharge/cess | TRC + Form 10F |

| Royalties/FIS | 10–15% | 20% + surcharge/cess | TRC + Form 10F + W-8BEN/E |

How Each Country Provides Relief

Indian residents who paid US income tax claim a tax credit equal to the US tax paid—capped at the Indian tax payable on that same foreign income. This prevents over-crediting.

US residents claim a foreign tax credit for income tax paid to India. US corporations holding at least 10% voting stock in an Indian company can also claim credit for the underlying Indian corporate tax paid on dividend profits.

Choosing the Right Method

Determine whether your income benefits more from exemption or credit before filing. Choosing the wrong method—or missing the claim entirely—can result in significantly higher effective tax rates.

VJM Global's Chartered Accountants and CPAs work with US-based individuals and companies to identify the correct relief method, prepare supporting documentation, and ensure full DTAA compliance across both jurisdictions.

How to Claim DTAA Benefits: Documentation and Filing Process

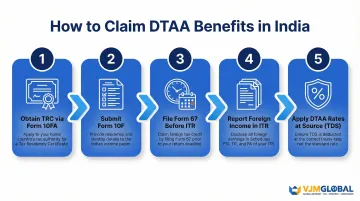

Step 1 — Obtain a Tax Residency Certificate (TRC)

Under Section 90(4) of the Income Tax Act, a TRC is mandatory to claim DTAA benefits.

- Indian residents: Apply via Form 10FA to obtain TRC from Indian authorities

- US residents: Use Form W-8BEN (individuals) or W-8BEN-E (entities) to certify US residency to Indian payers

Step 2 — Submit Form 10F

Along with the TRC, file Form 10F providing:

- Personal details and taxpayer identification number

- Residency period and address

- Attached TRC

Step 3 — File Form 67 Before Filing ITR

To claim foreign tax credit in India, Form 67 must be filed on the Indian income tax portal before submitting your ITR. It captures:

- Details of foreign income

- Taxes paid abroad

- Proof of payment

Step 4 — Report Foreign Income in ITR Schedules

Three schedules are relevant here:

- Schedule FSI: Declare foreign income, taxes paid abroad, applicable DTAA article, and relief claimed

- Schedule TR: Auto-populates from FSI data and reduces double taxation in your final tax calculation

- Schedule FA: Disclose all foreign assets held outside India

Step 5 — Apply DTAA Rates at Source (TDS)

When an NRI or foreign entity earns income in India, the Indian payer must deduct TDS. If the payee submits a valid TRC and Form 10F, the payer applies the lower DTAA rate instead of the standard domestic TDS rate.

Common error: Payers apply the standard domestic rate when DTAA documentation is missing or incorrectly submitted — resulting in excess TDS that must be reclaimed through ITR filing.

VJM Global works with US-based individuals and companies to review TDS documentation before payment, catch these errors early, and handle DTAA compliance filings end-to-end.

Frequently Asked Questions

What is the DTAA (income tax treaty) between India and the USA?

The India-USA DTAA is a bilateral tax treaty signed in 1989 and effective from December 1990. It prevents the same income from being taxed in both countries and covers individuals, companies, trusts, and partnerships resident in either India or the USA.

How can I avoid double taxation between India and the USA?

Claim DTAA benefits through either the exemption method (income taxed in one country is exempt in the other) or the tax credit method (tax paid abroad is credited against domestic tax). You must provide a valid TRC and Form 10F.

Is income earned in the USA taxable in India?

For Indian tax residents, global income including US-sourced income is taxable in India. However, under the DTAA, you can claim a credit for taxes already paid in the USA, eliminating double taxation on the same income.

Do people from India have to pay taxes in the United States?

Indian residents earning US-sourced income — such as dividends, royalties, or business profits from a US permanent establishment — are subject to US federal tax. The applicable DTAA article determines the withholding rate, and India allows a foreign tax credit for the US tax paid when filing Indian returns.

What types of income are covered or exempt under the India–USA DTAA?

The treaty covers salaries, business profits, dividends, interest, royalties, fees for technical services, and capital gains. Visiting teachers receive a 2-year exemption on teaching income; students are exempt from tax on maintenance funds received from their home country.

What does Article 12 of the India–USA DTAA cover?

Article 12 governs royalties and fees for included services arising in one country and paid to a resident of the other. It caps source-country withholding at 10% for equipment royalties and ancillary services, and 15% for literary, artistic, scientific, or industrial royalties and other included services.