Introduction

Singapore businesses expanding into the UK market frequently discover that UK VAT operates very differently from the GST framework they know at home. The structural gap between these two systems catches even experienced exporters off guard — and the consequences range from missed registration deadlines to unexpected penalty exposure.

The UK's 20% standard VAT rate is more than double Singapore's current 9% GST. More critically, while Singapore businesses register for GST only after crossing the SGD 1 million turnover threshold, non-UK businesses face a zero registration threshold: your first pound of UK taxable supply may trigger an immediate VAT obligation.

Post-Brexit rule changes have added further complexity for Singapore sellers, particularly around e-commerce, digital services, and low-value consignments. The obligations can arise before your second sale.

This guide walks Singapore businesses through UK VAT rates, registration rules for foreign sellers, compliance requirements including Making Tax Digital, and how the UK system differs from Singapore's GST framework—so you can avoid penalties and structure your UK market entry correctly from day one.

Key Takeaways

- UK VAT stands at 20% standard rate—more than double Singapore's 9% GST—with reduced (5%) and zero (0%) rates for specific categories

- Non-UK businesses have no registration threshold: even £1 of UK taxable supply requires VAT registration (UK-resident businesses don't register until £90,000)

- VAT returns filed quarterly via HMRC's Making Tax Digital platform, due one month and seven days after each period ends

- B2C digital services and goods under £135 require Singapore sellers to charge UK VAT at point of sale, while B2B services typically use reverse charge

What is UK VAT and How Does It Work?

If your Singapore business sells goods or services into the UK, you may have VAT obligations — even without a UK office. UK VAT (Value Added Tax) is a consumption tax collected at every stage of the supply chain, and it applies to overseas businesses the moment they cross certain thresholds or supply types. Introduced on 1 April 1973, VAT is now the UK's third-largest revenue source, generating an estimated £179.6 billion (14.6% of total government receipts) for 2025-26.

How the Input/Output Tax Mechanism Works

VAT-registered businesses charge output VAT on sales to customers and can reclaim input VAT paid on business purchases. The net difference — output tax minus input tax — is either paid to HMRC or reclaimed. This makes VAT broadly revenue-neutral for registered businesses; the end consumer ultimately bears the cost.

Example: A Singapore electronics exporter sells £10,000 worth of goods to a UK retailer and incurs £2,000 in UK logistics costs (subject to 20% VAT). The business charges £2,000 output VAT to the customer and reclaims £400 input VAT on logistics, paying HMRC £1,600 net.

Where that output VAT applies depends on what you're selling — and to whom.

Goods vs. Services: Place of Supply Rules

The rules differ significantly based on your supply type:

- Goods: VAT applies where goods are physically located at the time of supply. Ship products from Singapore into a UK warehouse before selling, and those sales trigger UK VAT obligations.

- B2B services: The UK customer typically accounts for VAT via the reverse charge mechanism — the Singapore supplier doesn't charge UK VAT; the UK business customer self-accounts for it (reports and pays it directly to HMRC) and can simultaneously reclaim it as input tax.

- B2C digital services: Digital services supplied to UK consumers are taxed based on the customer's location, requiring non-UK suppliers to register and charge UK VAT directly.

Four Critical VAT Categories

Singapore businesses will encounter:

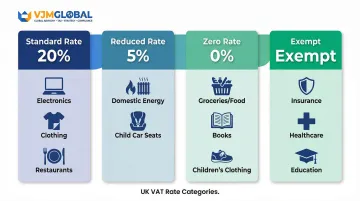

- Standard-rated (20%): Most goods and services

- Reduced-rated (5%): Domestic energy, children's car seats, certain property conversions

- Zero-rated (0%): Most food, children's clothing, books, newspapers, public transport

- Exempt: Insurance, financial services, healthcare, commercial land/buildings, education, gambling

Key difference for exporters: Zero-rated supplies allow input VAT recovery; exempt supplies do not. A Singapore food exporter making zero-rated sales can reclaim all input VAT on UK costs. A financial services provider making exempt supplies cannot — meaning any VAT paid on UK expenses becomes an unrecoverable cost that directly increases your operating overhead.

UK VAT Rates: A Breakdown for Singapore Businesses

The UK operates three primary VAT rates alongside exempt categories.

| VAT Rate | Applies To |

|---|---|

| Standard (20%) | Most goods and services: electronics, adult clothing, restaurant meals, hotel accommodation, professional services |

| Reduced (5%) | Domestic fuel and power, children's car seats, mobility aids, certain residential property conversions |

| Zero (0%) | Most food for human consumption, children's clothing and footwear, printed books, newspapers, passenger transport (10+ passengers) |

Exempt Supplies and Cash-Flow Impact

Exempt supplies—insurance, financial services, healthcare, commercial land/buildings, education, and gambling—fall outside the VAT system. Businesses making only exempt supplies cannot register for VAT or reclaim input VAT.

Example: A Singapore insurance broker expanding to the UK makes exempt supplies. Unlike a goods exporter who can reclaim VAT on office rent, professional fees, and equipment, the insurance broker absorbs these costs without recovery (typically 20% of the net price).

Low-Value Goods Rule for E-commerce

For consignments valued at £135 or less sold directly to UK consumers, the overseas seller (not the importer) charges and accounts for UK VAT at the point of sale. If selling via online marketplaces like Amazon or eBay, the marketplace is deemed the supplier and handles VAT obligations.

Recent VAT Scope Changes

From 1 January 2025, private school fees became subject to the standard 20% VAT rate, removing their previous exempt status. This illustrates how VAT scope can shift. Singapore businesses should track UK fiscal policy changes for any sectors they operate in — particularly education, healthcare, and financial services, where exempt status has historically been contested.

Zero-Rating vs. Exemption: Why It Matters

Zero-rating is commercially superior to exemption. Here's the practical difference:

- Zero-rated (e.g., books, children's clothing): Supplier charges 0% VAT but can fully reclaim input VAT on printing, shipping, and office costs

- Exempt (e.g., insurance, financial services): Supplier charges no VAT and cannot reclaim any input VAT — those costs are absorbed

For a Singapore publisher exporting books to the UK, zero-rated status means recovering all input VAT on fulfilment costs. An insurance firm in the same position recovers nothing.

UK VAT Registration Rules for Non-UK Businesses

The Zero-Threshold Rule

While UK-resident businesses only register once taxable turnover exceeds £90,000 per year, non-UK established businesses face a zero registration threshold—meaning any taxable UK supply, regardless of value, triggers an immediate registration requirement.

Who qualifies as "not established"? A business with no fixed establishment in the UK, not incorporated in the UK, and without a usual place of residence in the UK. This directly applies to most Singapore companies trading into the UK without a physical UK entity.

The Registration Process

Singapore businesses must:

- Apply to register with HMRC

- Obtain a UK VAT number (9-digit number prefixed with "GB")

- Set up a VAT online services account

- Appoint a UK tax agent or fiscal representative (optional but recommended)

Once registered, you'll need to decide how to manage ongoing HMRC correspondence. A tax agent manages HMRC correspondence and filings on your behalf. A fiscal representative takes on joint and several liability for your VAT obligations—HMRC can pursue them directly for unpaid VAT.

Compulsory vs. Voluntary Registration

Two registration routes apply to Singapore businesses:

- Compulsory registration: Triggered immediately when you make any taxable UK supply — no minimum threshold applies.

- Voluntary registration: Available even without taxable supplies. It allows input VAT reclaims on UK business costs and signals credibility to UK customers.

VJM Global's UK VAT Registration Support

VJM Global specializes in cross-border tax compliance for international businesses, with 30+ years of experience supporting foreign companies navigating complex regulatory environments. The firm's primary expertise is India-entry — helping businesses from Singapore, the UK, the US, and beyond establish compliant operations in India.

For Singapore businesses with UK VAT obligations, VJM Global can assess how your UK trading activity intersects with broader cross-border compliance requirements and connect you with UK-based VAT specialists for HMRC registration and filing support.

VAT Compliance: Returns, Digital Filing, and Penalties

VAT Return Cycle and Deadlines

Most businesses file quarterly VAT returns. Returns and payments are due one calendar month and seven days after the period end—not 30 days. If paying by Direct Debit, payment is taken three working days after the deadline.

Businesses with taxable turnover under £1.35 million can opt for the Annual Accounting Scheme, submitting one return per year (but must leave if turnover exceeds £1.6 million).

Making Tax Digital (MTD) Requirements

MTD is HMRC's mandatory digital reporting framework. Since 1 April 2022, all VAT-registered businesses must:

- Maintain digital VAT records (no manual spreadsheets submitted directly)

- Submit VAT returns using HMRC-compatible software (Xero, Sage, QuickBooks)

- Preserve a complete digital audit trail linking source transactions to filed returns

Singapore businesses without UK accounting infrastructure should budget for compliant software or outsourced bookkeeping from the outset. Cloud-based platforms mean your Singapore-based finance team can manage UK filings without needing a local office.

Penalty Regime

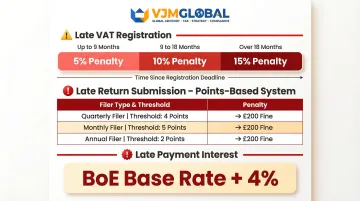

Late registration: Penalties of 5%–15% of unpaid VAT depending on delay length

- Up to 9 months late: 5%

- 9 to 18 months late: 10%

- More than 18 months late: 15%

Late return submission: Points-based system effective 1 January 2023

- Quarterly filers: £200 penalty at 4 points

- Monthly filers: £200 penalty at 5 points

- Annual filers: £200 penalty at 2 points

- Further £200 penalties apply for subsequent late submissions while at the threshold

Late payment: Interest charged from the first overdue day at Bank of England base rate plus 4%

These penalties compound fast — a business that misses its registration deadline by 10 months and then files late returns could face both a 10% registration penalty and accumulating points charges simultaneously. Direct Debit mandates eliminate late-payment interest with no extra effort, making them the simplest safeguard for businesses managing UK obligations remotely.

UK VAT vs. Singapore GST: Key Differences to Know

Rate Structures

Singapore GST currently stands at 9%/gst-rate-change/gst-rate-change-for-consumers1) on most goods and services with a relatively narrow scope. UK VAT operates at a 20% standard rate within a more complex tiered system:

- Standard rate (20%): Most goods and services

- Reduced rate (5%): Energy, children's car seats, some home renovations

- Zero rate (0%): Food, books, children's clothing

- Exempt: Financial services, insurance, education

Singapore businesses pricing products for the UK market must account for this much higher tax burden on customers—a £100 product becomes £120 inclusive of VAT.

Registration Thresholds

Singapore businesses register for GST only when turnover exceeds SGD 1 million annually/gst-registration-deregistration/do-i-need-to-register-for-gst). In contrast, non-UK businesses face the zero-threshold rule. Even a single taxable UK sale triggers immediate registration — a stark contrast to Singapore's GST framework.

Reverse Charge Mechanism for B2B Services

When a Singapore business supplies services to a UK VAT-registered business, the UK customer accounts for VAT via the reverse charge. The Singapore supplier charges nothing. For B2C digital services, the rules flip: the Singapore supplier must register and charge UK VAT based on the customer's UK location.

Overseas Vendor Registration Comparison

Singapore's Overseas Vendor Registration (OVR) regime applies only when two conditions are both met:

- Global turnover exceeds SGD 1 million

- Singapore-directed B2C sales exceed SGD 100,000

The UK imposes no equivalent thresholds for non-established businesses. Any taxable supply triggers registration.

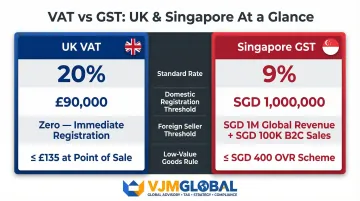

| Feature | UK VAT | Singapore GST |

|---|---|---|

| Standard Rate | 20% | 9% |

| Domestic Registration Threshold | £90,000 | SGD 1,000,000 |

| Foreign Seller Threshold | Zero (immediate registration) | SGD 1m global + SGD 100k SG B2C |

| Low-Value Goods | ≤£135 VAT at point of sale | ≤SGD 400 subject to OVR |

Frequently Asked Questions

What is the current standard VAT rate in the UK?

The standard rate is 20%, effective since 4 January 2011. Most goods and services are charged at this rate. The reduced rate of 5% applies to items like domestic energy and children's car seats, while 0% applies to essentials like most food and books.

How is VAT different from sales tax?

Sales tax is typically charged only at the final point of sale to the consumer. VAT is collected at every stage of the supply chain, but businesses reclaim the VAT they pay on inputs—making VAT revenue-neutral for most businesses except those in exempt sectors.

Do Singapore businesses need to register for UK VAT?

Yes, if making any taxable supply in the UK. Non-UK established businesses must register immediately due to the zero registration threshold, unlike UK-based businesses which only register once turnover exceeds £90,000.

What is the UK VAT registration threshold for foreign businesses?

For businesses not established in the UK, the threshold is zero—they must register as soon as they make any taxable supply in the UK, regardless of value.

Do Singapore businesses pay UK VAT on digital services sold to UK customers?

Yes. Singapore businesses selling digital services (software, e-learning, streaming) directly to UK consumers must register for UK VAT and charge 20%, regardless of their own location. B2B sales where the UK customer self-accounts under the reverse charge are generally exempt from this requirement.

Can Singapore businesses reclaim UK VAT on business expenses?

Non-UK businesses cannot reclaim UK VAT through a standard VAT return unless they are VAT-registered in the UK. If registered, input VAT on qualifying business expenses is reclaimable. Businesses not required to register have no reclaim route under current HMRC rules.