Introduction

Imagine a Singapore-based software company invoicing an Indian client for ₹50 lakh in consultancy fees. Singapore withholds 15% tax on the payment. The same income is then taxed again in India when the company files its return.

Without relief, the effective tax burden reaches 32–35%, eroding nearly a third of revenue to duplicate taxation. This is not a hypothetical edge case. It reflects the daily reality for thousands of businesses across the India-Singapore corridor, where bilateral trade reached USD 34.26 billion in FY 2024-25. Singapore has channeled nearly USD 174.89 billion into India over the past 25 years, accounting for 24% of total FDI inflows.

The India-Singapore Double Taxation Avoidance Agreement (DTAA), in force since 1994, was designed to resolve exactly this problem. It allocates taxing rights between the two countries, caps withholding tax rates on cross-border payments, and provides mechanisms for foreign tax credits.

Recent amendments through the 2019 Multilateral Instrument (MLI) added anti-abuse layers (including the Principal Purpose Test and stricter Limitation of Benefits provisions) to prevent treaty shopping while protecting legitimate commerce.

This guide covers:

- Scope of the treaty and who qualifies

- Withholding tax ceilings by income type

- Permanent establishment thresholds

- Capital gains rules post-April 2017

- Step-by-step procedures to claim benefits

- Documentation requirements to survive Indian tax audits

TLDR: Key Takeaways

- The India-Singapore DTAA caps withholding tax on dividends, interest, and royalties/FTS at 10–15%—versus India's standard 20% domestic rate

- Benefits require proof of tax residency via a Tax Residency Certificate (TRC) and submission of Form 10F before income is received in India

- Post-April 2017, India can tax capital gains on shares in Indian companies, with grandfathering for pre-2017 investments subject to strict anti-shell company rules

- The 2019 MLI introduced the Principal Purpose Test (PPT), allowing denial of benefits if obtaining treaty relief was a primary purpose of the arrangement

- Singapore companies face Permanent Establishment (PE) risk after just 90 days of service activities in India (or 30 days when serving a related enterprise)

What Is the India-Singapore DTAA and What Does It Cover?

The India-Singapore DTAA was signed on 24 January 1994, replacing an earlier 1981 agreement, and entered into force on 27 May 1994. Protocols in 2005, 2011, and 2016 (effective from 1 April 2017) have amended it since.

The Multilateral Instrument (MLI) updated the treaty in 2019. India ratified the MLI on 25 June 2019; its provisions took effect for withholding taxes on 1 January 2020, and for other taxes on 1 April 2020.

Taxes Covered:

- India: Income tax, including any surcharge

- Singapore: Income tax under the Income Tax Act

The treaty automatically extends to any substantially similar taxes enacted after its signing date.

Beyond the tax types each country applies, the treaty also defines which categories of income it covers between the two countries:

Income Categories Governed by the Treaty:

- Business profits

- Dividends

- Interest

- Royalties and fees for technical services (FTS)

- Capital gains

- Employment income (salaries and wages)

- Directors' fees

- Income from immovable property (rental income)

- Pensions and annuities

- Income of artistes and sportspersons

Residency and Tie-Breaker Rules

Treaty benefits are available only to residents of one or both contracting states—persons liable to tax in that state based on domicile, residence, or place of management. Incorporation in Singapore or India does not automatically confer treaty eligibility; tax residency must be substantiated with a valid Tax Residency Certificate.

Tie-Breaker Rules for Dual Residents:

For Individuals:

- Permanent home available

- Centre of vital interests (personal and economic ties)

- Habitual abode

- Nationality

- Mutual agreement between tax authorities

For Companies:

- Residency defaults to the state where the place of effective management is located

Key Withholding Tax Rates Under the India-Singapore Treaty

Under the DTAA, the source country can tax cross-border payments, but the treaty imposes maximum withholding tax ceilings. These caps apply only when:

- The recipient is the beneficial owner of the income

- The recipient meets treaty eligibility conditions

- The income is not attributable to a Permanent Establishment (PE) in the source country

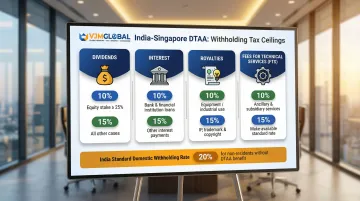

Dividends

India to Singapore:

- 10% if the Singapore recipient holds at least 25% of the Indian company's equity

- 15% in all other cases

Since India abolished the Dividend Distribution Tax (DDT) in 2020, dividends are now taxed at the shareholder level, making these treaty caps especially significant. That context also shapes what happens in the reverse direction.

Singapore to India:

- Singapore does not impose withholding tax on dividends

- Indian residents are subject only to Indian domestic tax law

Interest

Withholding tax is capped at:

- 10% when paid on a loan from a bank or similar financial institution (including insurance companies)

- 15% in all other cases

These caps do not apply if:

- The interest is connected to a PE in the source country

- The interest amount exceeds arm's-length terms

Royalties and Fees for Technical Services

Royalties:

- 15% for intellectual property (copyrights, patents, trademarks, know-how, secret formulas)

- 10% for payments relating to the use of industrial, commercial, or scientific equipment

FTS rates follow a parallel structure but hinge on a specific threshold: whether the service actually transfers technical knowledge.

Fees for Technical Services (FTS):

- 15% for managerial, technical, or consultancy services that "make available" technical knowledge or involve transfer of a technical plan

- 10% for services that are ancillary and subsidiary to equipment royalties qualifying for the 10% rate

⚠️ Warning: Misclassifying income is a common compliance error. Treating royalties as business income, or conflating FTS with ordinary service contracts, can trigger higher withholding or outright denial of treaty benefits. Indian tax authorities look at the economic substance of an arrangement, not just how a contract labels it.

Permanent Establishment: When Does Your Business Create a Taxable Presence?

Under the Singapore-India tax treaty, the concept of Permanent Establishment (PE) determines whether India can tax a Singaporean company's business profits — and vice versa. A PE is defined as a fixed place of business through which an enterprise wholly or partly carries on its business.

Standard PE Examples:

- Place of management

- Branch office

- Factory or workshop

- Mine, quarry, or extraction site

- Warehouse (used for third-party storage)

- Farm or plantation

- Sales outlet

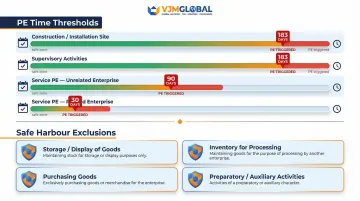

Critical Time-Based Thresholds

| PE Category | Threshold |

|---|---|

| Construction/Installation Site | More than 183 days in a fiscal year |

| Supervisory Activities | More than 183 days in a fiscal year (in connection with a construction project) |

| Service PE (Unrelated) | More than 90 days in a fiscal year |

| Service PE (Related Enterprise) | More than 30 days in a fiscal year |

Not every business activity triggers PE status. The treaty carves out specific activities that are considered preparatory or auxiliary — and therefore safe.

Safe-Harbour Exclusions (Do NOT Create a PE):

- Storage, display, or delivery of goods

- Maintaining inventory solely for processing by another enterprise

- Purchasing goods or collecting information

- Preparatory or auxiliary activities

These thresholds matter because they determine where your profits get taxed. Without a PE, a Singaporean company's business profits remain taxable only in Singapore. Once a PE is triggered, India can tax the profits directly attributable to that establishment.

Capital Gains Under the India-Singapore Treaty

The April 2017 Watershed

The 2016 Protocol fundamentally changed how capital gains on shares are taxed:

Shares Acquired Before 1 April 2017:

- Gains are taxable only in the seller's country of residence (Singapore) — grandfathering applies

- Shell companies cannot claim this benefit under the Limitation of Benefits (LOB) clause

Shares Acquired On or After 1 April 2017:

- India may tax gains on shares in an Indian company

- Transitional period (1 April 2017 – 31 March 2019): India's tax rate was capped at 50% of the otherwise applicable rate

- Post-31 March 2019: Full domestic Indian rates apply

Other Capital Gains Categories

| Gain Type | Treaty Treatment |

|---|---|

| Immovable Property | May be taxed in the country where the property is situated |

| Business Assets (part of PE) | May be taxed in the PE's country |

| Ships/Aircraft (International Traffic) | Taxable only in the seller's country of residence |

Prashant Kothari ITAT Ruling (June 2025)

The Mumbai Tribunal ruled that the Limitation of Relief provision does not apply to deny capital gains treaty benefits. The reasoning: Article 13 allocates taxing rights between the two countries (specifying who can tax, not who is exempt), so it does not constitute an "exemption" that LOB can override. For Singapore-resident investors holding Indian shares, this means LOB cannot be used to strip away their treaty protection on capital gains.

Limitation of Benefits for Grandfathered Shares

That said, the LOB test still governs whether grandfathered share gains qualify for treaty benefits. A company is deemed a "shell" if its annual operational expenditure is:

- Less than S$200,000 in Singapore, or

- Less than INR 50 lakh in India

Both thresholds are measured over the preceding 24 months.

Exception: Companies listed on a recognised stock exchange are exempt from the shell company test.

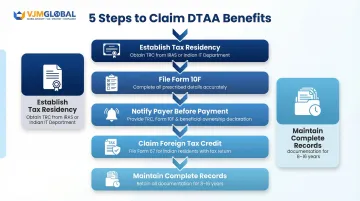

How to Claim DTAA Benefits: Documentation and Step-by-Step Process

Step 1 — Establish and Document Tax Residency

- Singapore residents: Obtain a Tax Residency Certificate (TRC) from IRAS

- Indian residents: Obtain TRC from the Indian Income Tax Department

The TRC is the foundational document confirming eligibility and must be obtained before or at the time income is received, not retrospectively.

Step 2 — Complete Form 10F for Indian Filings

Under Indian tax rules, if the TRC does not contain all prescribed details (name, address, Tax Identification Number, residency period, income specifics), the non-resident must file Form 10F.

Without Form 10F, the payer will apply domestic Indian withholding rates (20%) rather than the treaty cap.

Two additional filing requirements apply:

- CBDT mandates electronic filing of Form 10F — no exceptions

- Manual filing relaxations for non-residents without a PAN ended on 30 September 2023

Step 3 — Notify the Payer Before Payment

Provide the payer (the entity remitting income in India) with:

- Your TRC

- Form 10F

- Declaration of beneficial ownership and treaty eligibility

The payer is responsible for withholding at the correct treaty rate. If they withhold at full domestic rates instead, recovering the overpayment means filing for a tax refund — a slower, avoidable process.

Step 4 — Claim Foreign Tax Credit at Filing

The credit claim process differs depending on which country taxed the income.

Indian residents taxed in Singapore:

- Claim credit by filing Form 67 alongside the Indian Income Tax Return

- Attach proof of Singapore tax paid

- Critical deadline: Form 67 must be filed before the end of the assessment year to avoid disallowance

Singapore residents taxed in India:

- Claim credit through Singapore tax return

- Credit limited to the lower of:

- Singapore tax attributable to that income, or

- Indian tax actually paid

Step 5 — Maintain Complete Records

Keep the following on file:

- TRCs

- Form 10F

- Contracts and invoices

- Proof of payment

- Correspondence with tax authorities

Retention periods vary by income type:

- Standard records: 8 years from the end of the relevant assessment year

- Foreign income or assets: up to 16 years

Inadequate documentation is the most common reason treaty benefits are denied during Indian tax audits.

If navigating this process feels complex, VJM & Associates LLP has handled DTAA compliance for businesses operating across India, Singapore, the UK, the US, and Australia for over 30 years — covering TRC documentation, Form 10F filing, and tax credit claims through to audit support.

Anti-Avoidance Provisions and the 2019 MLI Updates

The 2019 MLI introduced two primary anti-abuse mechanisms:

1. Principal Purpose Test (PPT)

If it is reasonable to conclude that obtaining a treaty benefit was one of the principal purposes of a transaction, that benefit may be denied—unless granting the benefit aligns with the treaty's object and purpose.

Inserted as Article 29A, the PPT applies prospectively to all treaty benefits except grandfathering provisions.

2. Limitation of Benefits (LOB) for Capital Gains

A shell or conduit company cannot claim grandfathered capital gains benefits.

Shell Company Definition: A company whose annual operational expenditure falls below S$200,000 in Singapore or INR 50 lakh in India over the preceding 24 months qualifies as a shell entity for this purpose.

Exception: Companies listed on a recognised stock exchange are exempt.

What This Means for Legitimate Businesses

Companies with:

- Genuine operations

- Real employees

- Substantive decision-making in their country of residence

are not affected by these provisions. PPT and LOB are designed to catch structures where tax savings are the sole driver — not businesses with real commercial substance.

When disputes do arise over treaty application, taxpayers have a formal resolution path.

Mutual Agreement Procedure (MAP)

Article 27 allows taxpayers to present cases of taxation inconsistent with the treaty to their competent authority within three years from the first notification of the action.

Note: While Singapore opted into the MLI's mandatory binding arbitration (Part VI), India did not. Therefore, mandatory binding arbitration does not apply to the India-Singapore DTAA.

Frequently Asked Questions

Does India have a double taxation agreement (DTAA) with Singapore?

Yes. The DTAA between India and Singapore has been in force since 27 May 1994, applying to residents of one or both contracting states. It has been updated multiple times and last amended through the 2019 Multilateral Instrument.

What does the India-Singapore tax treaty cover?

The treaty covers a broad range of income types: business profits, dividends, interest, royalties, fees for technical services, capital gains, employment income, directors' fees, rental income, and pensions. Taxing rights are allocated between the two countries based on the nature of each income type.

What is double taxation and how does India handle it?

Double taxation occurs when the same income is taxed in two countries. India addresses this through its network of DTAAs (including with Singapore) and by allowing foreign tax credits. Residents can deduct taxes paid abroad from their Indian tax liability on the same income, subject to limits.

What is an example of double taxation?

An Indian company receives interest from a Singapore borrower. Singapore withholds tax on the payment, and India also taxes that same interest as part of the company's total income — resulting in double taxation on a single receipt without treaty relief.

Is there withholding tax in Singapore and what are the rates?

Singapore imposes withholding tax on certain payments to non-residents (interest, royalties, technical fees) but does not withhold on dividends. Under the India-Singapore treaty, withholding on these payments is capped at 10–15% depending on income type, subject to eligibility conditions.

Do Indians have to pay tax in Singapore?

Indian residents earning income in Singapore are generally subject to Singapore tax on Singapore-sourced income. However, the DTAA ensures they are not taxed twice—any Singapore tax paid may be credited against Indian tax on the same income. The 183-day rule for employment income may exempt short-term workers from Singapore tax.