When businesses provide products or services on credit, they create accounts receivable, money owed by customers. The key question is whether accounts receivable are debit or credit.

In this blog, we’ll explore why accounts receivable is considered a debit and its impact on your company's financial statements. You’ll also learn about the journal entries that affect accounts receivable and how to handle them properly.

Accounts receivable refers to the outstanding amounts of money a company is owed by its customers for goods or services that have been provided but not yet paid for. These amounts are classified as a current asset on the balance sheet, which means they are expected to be collected within the company’s operating cycle, typically within a year.

The importance of accounts receivable lies in its direct impact on cash flow. Efficient management of accounts receivable ensures that a company can maintain liquidity and support day-to-day operations without relying excessively on external funding.

In the accounting equation, Assets = Liabilities + Equity, accounts receivable falls under assets because it represents money that will be received by the business in the near future. Since accounts receivable is classified as a current asset, it contributes to the total value of the company’s assets, which in turn impacts the company’s financial health and ability to meet its obligations.

Accounts receivable plays a crucial role in a company’s cash flow. By keeping track of amounts due, companies can forecast future cash inflows and manage their working capital more effectively. A high accounts receivable balance might indicate that the business is experiencing delays in collecting payments, which could lead to cash flow issues.

Therefore, monitoring and managing accounts receivable is vital for sustaining smooth operations, especially for small businesses that need to maintain a steady flow of cash.

Now that we understand the importance of accounts receivable and its impact on the accounting equation and cash flow, let’s explore how accounts receivable is classified in accounting.

Must Read: Advantages of Partnering with an Outsourced Accounting Firm for Foreign Companies

Understanding the basics of debit and credit in accounting is essential to maintaining accurate financial records. These fundamental concepts ensure that the accounting equation remains balanced and that every transaction is properly recorded.

Double-entry accounting is a core principle in the accounting world, where every financial transaction affects at least two accounts. This system ensures that the accounting equation, Assets = Liabilities + Equity, remains balanced after every transaction. For example, when a business makes a sale on credit, both the Accounts Receivable (asset) and Revenue (equity) accounts are impacted, maintaining balance.

In double-entry accounting, debits and credits serve distinct purposes, and understanding their rules is crucial to proper record-keeping.

These rules ensure that every transaction keeps the accounting system balanced, and each debit has an equal and opposite credit.

Every account in the accounting system has a “normal balance” based on its classification as an asset, liability, or equity account:

Now that we’ve outlined the basics of debits and credits, let’s focus on a specific account, accounts receivable. So, is accounts receivable a debit or credit? Let’s break it down further.

Also Read: How to Choose the Right Bookkeeping Services for Your Business

When it comes to accounting, understanding whether accounts receivable is a debit or credit is a foundational concept. Since accounts receivable represents money that is owed to a business, it is classified as an asset, and like other assets, it is increased with a debit entry.

Therefore, accounts receivable is a debit.

As an asset account, accounts receivable increases when debited. When a business provides goods or services on credit, it essentially gains a future cash inflow, represented as an asset. Since assets increase with debits, the correct accounting entry is to debit the accounts receivable and credit the corresponding revenue account.

Here are two common journal entries that demonstrate the debit classification of accounts receivable:

These entries reflect the movement of money in and out of the business, ensuring that the company's books are balanced and accurate.

The movement of accounts receivable has a direct impact on the balance sheet and income statement. On the balance sheet, the increase in accounts receivable shows that the company has an outstanding amount due. Once the payment is received, the reduction in accounts receivable will shift the funds into cash or bank accounts.

Additionally, on the income statement, the credit entry to sales revenue increases the company's total income, contributing to net profit.

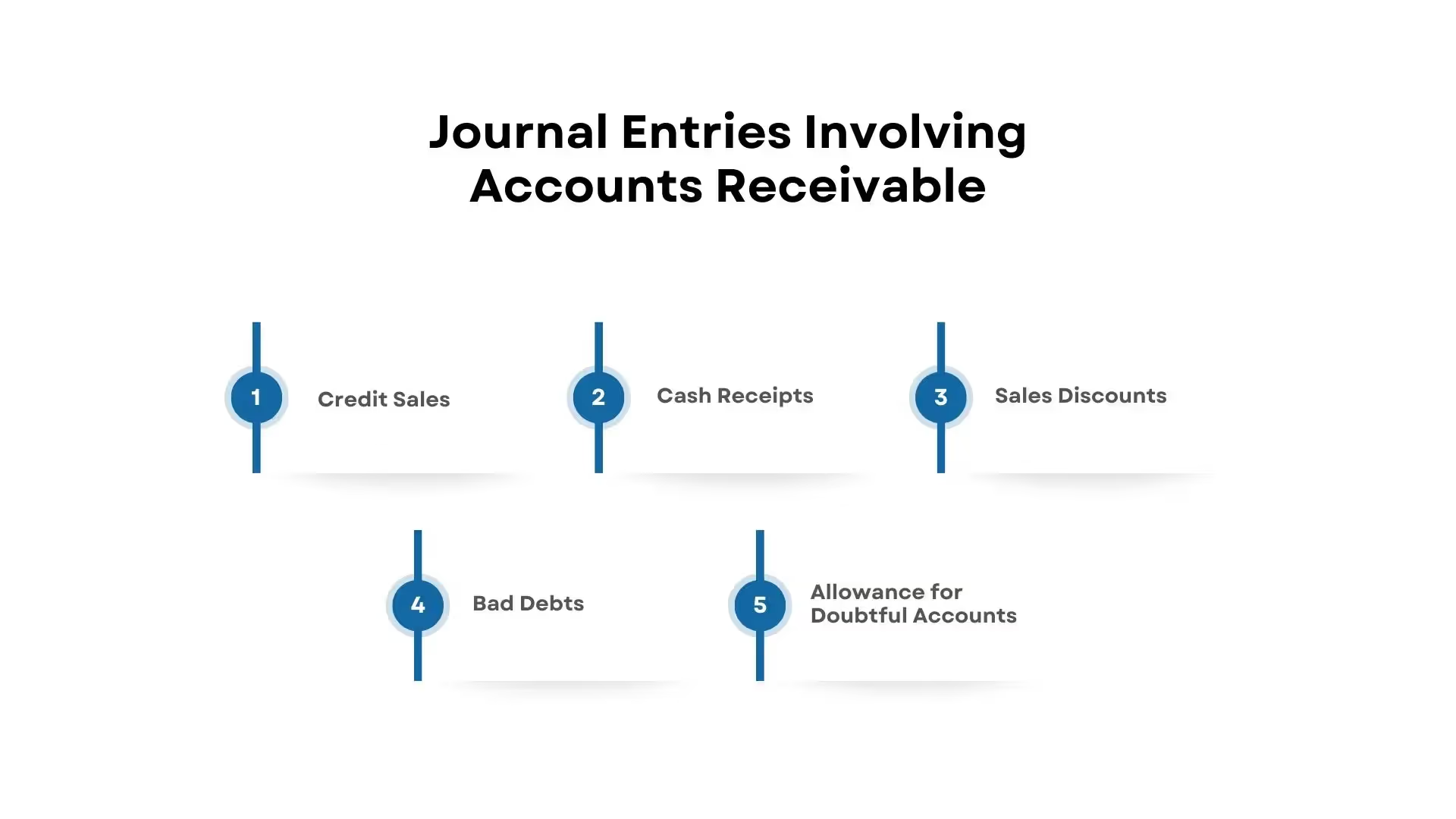

With a solid understanding of how accounts receivable is treated in journal entries, let’s look at some of the common journal entries involving accounts receivable to see how they’re applied in real-world scenarios.

Further Read: How Legal Process Outsourcing (LPO) Is Revolutionizing Businesses

When managing accounts receivable, businesses record various types of transactions that impact their financial statements. Understanding how to handle these journal entries is essential for accurate bookkeeping and financial reporting. Below are common journal entries involving accounts receivable:

When a business sells goods or services on credit, it recognizes revenue but doesn't receive payment immediately. The journal entry is as follows:

This entry reflects that the business is owed money for the goods or services provided, and it recognizes the revenue earned during the period.

When a customer makes a payment, the accounts receivable balance decreases, and cash or bank account increases. The journal entry looks like this:

This transaction confirms that cash has been received, reducing the outstanding amount that customers owe.

To encourage faster payment, businesses often offer discounts. If a customer takes advantage of this, the journal entry records the reduction in the amount due. The entry would be:

For example, if a customer owes $1,000 but is offered a 5% discount for early payment, the new receivable amount would be $950. This ensures that the business correctly reflects the discount given.

Occasionally, a business may find that it cannot collect the money owed by a customer. In such cases, the business writes off the bad debt. The journal entry typically includes:

By writing off the bad debt, the company acknowledges that it will no longer be receiving the money owed and adjusts its accounts accordingly.

Rather than writing off bad debts as they occur, businesses often set up an allowance for doubtful accounts to estimate future bad debts. This method provides a more proactive approach to managing uncollected debts. The journal entry is:

This allowance reduces the overall value of accounts receivable and accounts for anticipated future losses due to uncollectible debts. Each year, the business estimates how much of its accounts receivable may become uncollectible and adjusts the allowance accordingly.

Accounts receivable is classified as a current asset on the balance sheet because it represents money owed to the business that is expected to be received within a year. It’s an essential part of a company’s financial health and can significantly affect liquidity and working capital.

As the business provides goods or services to its customers, the outstanding invoices are recorded as accounts receivable. This is shown as an asset because it is money that is expected to be paid in the near future, contributing to the total value of the company’s assets.

The movement of accounts receivable is directly tied to a company’s cash flow. A high balance in accounts receivable means that the business has outstanding payments that need to be collected. If the collection period is longer than expected, this could lead to cash flow issues, preventing the business from having enough liquid capital to meet operational needs.

Several financial ratios depend on the value of accounts receivable. These ratios help assess how effectively a company is managing its receivables and can highlight potential liquidity issues.

Here is how an expert service provider can help to maintain healthy cash flow and optimize your debt management.

At VJM Global, we specialize in providing comprehensive financial solutions tailored to meet your business’s needs. Our services are designed to streamline debt management, optimize cash flow, and ensure financial stability through strategic insights and expert advisory.

Our Core Services Include:

If you’re looking for professional accounting services, contact VJM Global today to optimize your financial management and ensure your accounting records are in top shape.