.avif)

Companies are under more scrutiny for revenue recognition in the modern, fast-changing financial reporting world. For U.S. businesses across industries, complying with ASC 606, the current revenue recognition standard, is critical to ensuring accurate financial statements and maintaining stakeholder trust.

ASC 606, introduced by the Financial Accounting Standards Board (FASB), provides a consistent framework that replaces diverse industry-specific guidelines with a unified, principle-based approach. By focusing on the transfer of control and performance obligations, ASC 606 enhances transparency and comparability across organizations.

In this blog, we will break down the core principles of ASC 606, walk through its five-step revenue recognition model, discuss implementation best practices, highlight common challenges, and explore how different industries apply this important standard.

ASC 606, or Accounting Standards Codification Topic 606, is a revenue recognition standard issued by the Financial Accounting Standards Board (FASB). It provides a unified framework for companies to recognize revenue from contracts with customers consistently across industries. ASC 606 replaced previous, more fragmented revenue recognition rules to improve transparency, comparability, and financial reporting accuracy.

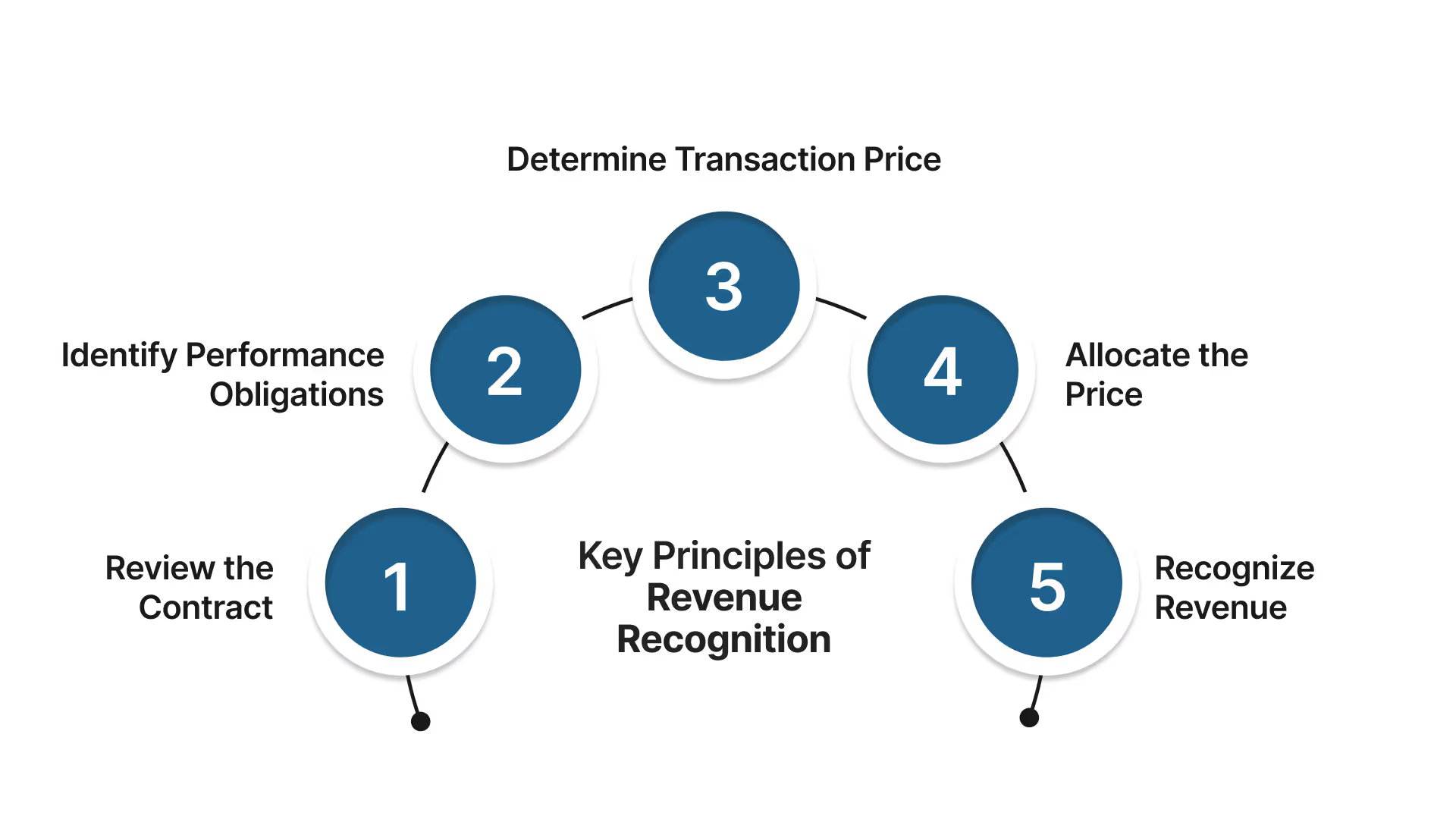

The standard requires companies to identify contracts, determine performance obligations, establish transaction prices, allocate prices to obligations, and recognize revenue when those obligations are satisfied. This approach ensures revenue is recorded when control of goods or services is passed to the customer, reflecting the true economic activity.

Understanding ASC 606 is essential for companies to comply with U.S. GAAP, provide clear financial information, and meet regulatory and investor expectations.

Revenue recognition sets the rules for when a business can count income from its sales, not just when money is received, but when the product or service is actually delivered. This approach prevents companies from inflating their financial health by recording sales too early and ensures earnings reflect real business performance.

By applying these standards consistently, companies provide clearer, more reliable financial reports. This transparency helps investors and stakeholders compare businesses fairly, building trust and reducing the risk of financial misrepresentation. Ultimately, revenue recognition grounds financial statements in the actual value created for customers and the marketplace.

Now that you understand what ASC 606 and revenue recognition are, let’s explore ASC 606 compliance matters for businesses.

Here are key reasons why ASC 606 compliance matters for businesses:

Next, let’s explore the core principles and the five-step revenue recognition model.

ASC 606 is built around five key steps that guide how companies recognize revenue consistently and accurately. These steps ensure revenue reflects when control of goods or services passes to customers, providing a clear picture of financial performance.

Before any revenue can be recorded, a valid contract must exist between the company and the customer. This is not just a simple signed document; it’s a legally enforceable agreement where both parties clearly understand their rights and obligations.

Look for:

Once the contract is established, identify all distinct goods or services promised to the customer, called performance obligations.

A good or service is distinct if:

Calculate the total amount the company expects to receive for transferring goods or services, excluding taxes collected for others.

This isn’t always straightforward and may include:

If multiple performance obligations exist, allocate the total transaction price fairly to each based on its standalone selling prices.

Consider:

Revenue is recognized when the customer gains control of the promised goods or services either over time or at a point in time.

Revenue over time applies when:

Now that you understand the five-step revenue recognition methodology, let's look at practical examples for adopting ASC 606 in your firm.

Also Read: Understanding US GAAP Revenue Recognition Standards

Implementing ASC 606 requires careful analysis and clear documentation of contracts, performance obligations, and transaction prices. Here are examples to illustrate key implementation steps:

Implementing ASC 606 can be complex, but following these best practices can guarantee a smooth transition and ongoing compliance:

Collect and organize all active contracts in a single system. This makes it easier to analyze terms, identify performance obligations, and ensure consistent application of the five-step model across business units. A central repository also helps surface high-risk contracts quickly during audits.

Accurate allocation of transaction prices depends on defensible SSPs. Companies should base SSPs on historical sales data when possible and establish clear, documented estimation techniques when observable prices aren’t available. Regularly reviewing these assumptions keeps allocations aligned with market conditions.

Contract amendments are one of the most complex aspects of ASC 606. Set policies for when a modification should be treated as a new contract versus a revision of the existing one. Consistent application avoids restatement risk and ensures recognition matches the economic substance of the change.

Revenue recognition isn’t just a finance issue. Sales, legal, operations, and finance must align on how obligations are structured and documented. Creating cross-functional review teams helps prevent conflicts between what is promised to customers and what is recorded in financials.

Areas such as variable consideration, overtime recognition, and allocation methods require significant judgment. Documenting assumptions, rationale, and calculations creates a defensible audit trail. Strong documentation also ensures new team members can apply policies consistently.

Automation tools in ERP or specialized revenue recognition software reduce manual effort, but their value lies in standardization and accuracy. Automated allocation, recognition schedules, and reporting help finance teams focus on analysis instead of repetitive tasks, while also improving audit readiness.

ASC 606 is not a one-time exercise. Regular training ensures staff understand evolving interpretations and company policies. Periodic internal reviews of recognition practices, disclosures, and contract terms help catch issues early and keep compliance aligned with business growth.

Effective ASC 606 implementation requires more than ticking boxes; it demands structured policies, cross-functional alignment, and continuous refinement. By treating these best practices as part of everyday operations, companies strengthen compliance and create more reliable financial reporting.

Next, let’s explore the most common obstacles companies face.

Also Read: Understanding Company Audits: Key Processes and Types

.avif)

One of the most frequent challenges is correctly defining distinct performance obligations within a contract. Bundled products or services can blur the lines, requiring careful judgment to decide what constitutes a separate obligation.

ASC 606 requires allocating the transaction price based on SSPs, which can be hard to determine for unique or highly customized offerings. Poor SSP estimates can lead to improper revenue allocation.

Handling renewals, upgrades, or changes in contract scope under ASC 606 adds complexity in determining if modifications are separate contracts or part of existing obligations.

Estimating variable considerations like discounts, bonuses, and penalties requires significant judgment, increasing room for error and audit challenges.

ASC 606 demands accurate, complete, and readily accessible data across contracts, pricing, and performance. Lack of integrated systems can cause errors and delays.

Now that you are aware of these challenges, let’s look at how VJM Global can help you with this.

VJM Global offers tailored accounting and audit support services that help U.S. businesses navigate the complexities of ASC 606 revenue recognition requirements with confidence and accuracy. Their deep understanding of both U.S. GAAP standards and Indian regulatory frameworks allows them to provide offshore solutions that meet high compliance standards while reducing operational costs.

At VJM Global, we provide U.S. companies with accounting outsourcing, audit support, and ASC 606 compliance services. Our offshore teams deliver efficient compliance management while optimizing costs.

Simplify ASC 606 revenue recognition and ensure smooth compliance. Contact VJM Global today to build a foundation for accurate financial reporting and growth.

Identify the contract, identify performance obligations, determine transaction price, allocate price, and recognize revenue when obligations are satisfied.

Yes, ASC 606 is a revenue recognition standard issued by the FASB under U.S. GAAP.

They align with ASC 606’s five steps: contract identification, performance obligations, transaction price, allocation, and revenue recognition.

Identifying the contract, determining performance obligations, measuring transaction price, and recognizing revenue upon satisfaction.