ASC 740 is the U.S. GAAP standard for accounting for income taxes. It guides how companies recognize, measure, and disclose tax obligations in their financial statements. If you’re a growing SME, a CPA firm managing client audits, or a company preparing to expand into India, ASC 740 is critical.

It helps maintain accurate tax provisions and ensures compliance with regulatory expectations.

Applying it correctly ensures accurate tax provisions, strengthens transparency, and builds investor confidence. It also keeps you audit-ready and aligned with regulatory expectations.

Especially, with the recent changes under ASU 2023-09, both public and private companies must adapt their reporting to meet updated disclosure requirements.

Key Takeaways: ASC 740 Income Tax Accounting

ASC 740 governs how U.S. GAAP filers recognize, measure, and disclose income tax obligations and is essential for both public and private companies to apply accurately.

Deferred tax assets and liabilities are central to ASC 740, and valuation allowances must be applied when recoverability is uncertain using the "more-likely-than-not" threshold.

ASU 2023-09 introduces significant disclosure changes, including tax expense breakdowns by jurisdiction and detailed eight-category effective tax rate reconciliations, mandatory for FY 2024 public filers.

Common pitfalls include misclassifying temporary differences, misjudging valuation allowances, and failing to update provisions for tax rate changes, which remain leading causes of restatements.

Strong internal controls, early provision reviews, and coordinated audit preparation help companies reduce errors and ensure ASC 740 compliance.

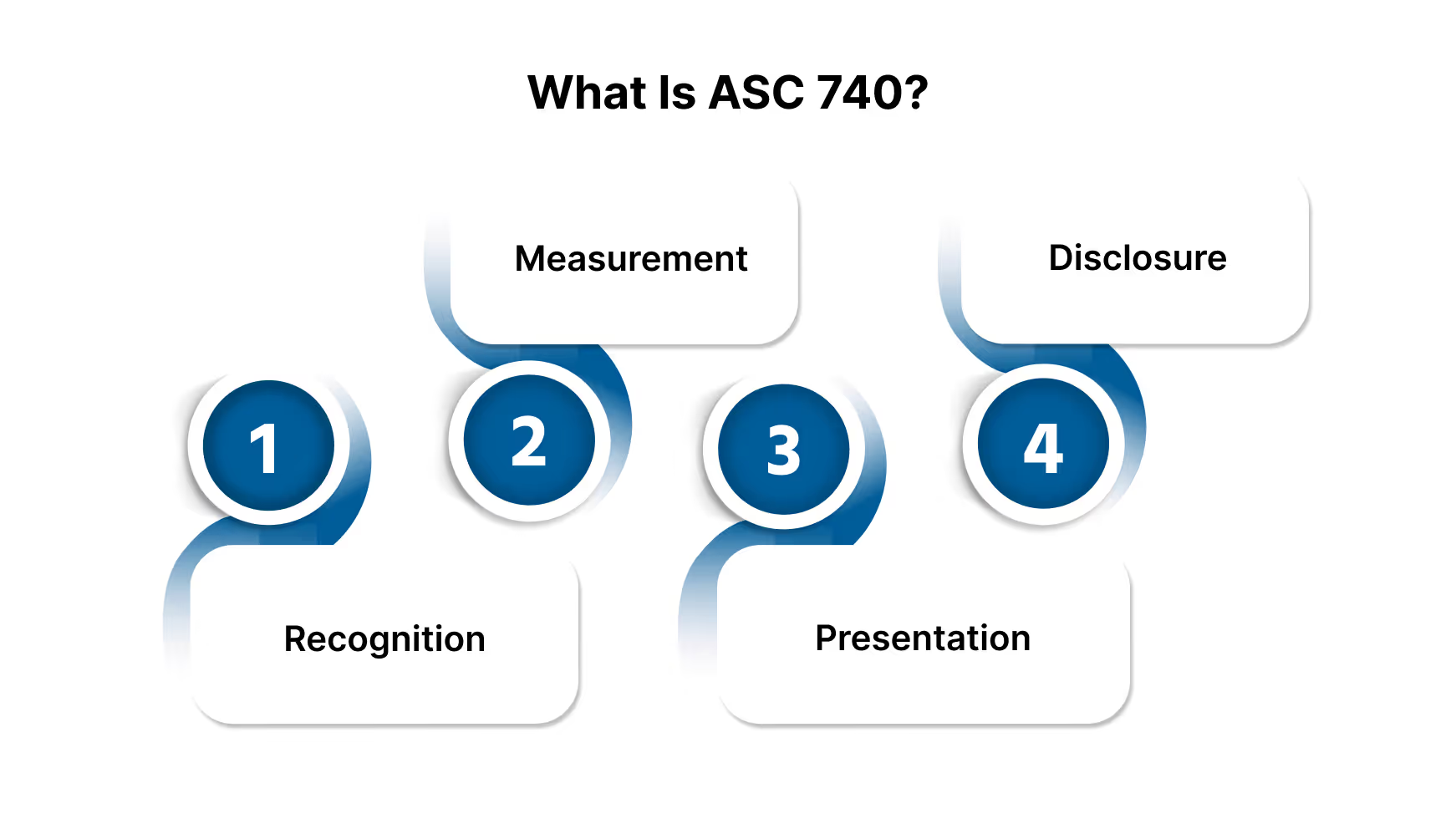

What Is ASC 740? (Definition and Purpose)

ASC 740 is the U.S. GAAP framework for accounting for income taxes. In essence, It establishes how companies recognize, measure, present, and disclose income tax obligations in their financial statements.

By standardizing tax accounting, ASC 740 ensures that stakeholders can rely on consistent, transparent financial reporting. It covers the following:

Recognition: When to record income tax liabilities or benefits.

Measurement: Determining the correct amounts for tax positions.

Presentation: How income tax impacts appear on financial statements.

Disclosure: Reporting details that investors and regulators expect.

ASC 740 gives businesses a transparent, dependable approach to handling income tax in their financial statements, making complex requirements far easier to manage.

However, it is also essential to understand why ASC 740 plays such a vital role in strengthening financial reporting.

Ensure error-free financial reporting with our seasoned accounting experts.

Accurate income tax accounting is more than a compliance exercise; it is a pillar of financial credibility.

In 2024, tax accounting errors, including misapplication of ASC 740, accounted for approximately 12% of all financial restatements by U.S. public companies (Alvarez & Marsal).

Here’s why ASC 740 is critical:

Investor Trust: Clear and accurate tax reporting reassures investors that your financial statements reflect reality.

Audit Readiness: Well-prepared provisions and reconciliations reduce audit findings and the risk of last-minute adjustments.

Regulatory Compliance: ASC 740 ensures alignment with U.S. GAAP and SEC expectations, mitigating the chance of penalties or public restatements.

Informed Decisions: Accurate tax data enables strategic planning for expansions, acquisitions, and financing decisions.

Treat ASC 740 as an opportunity to strengthen both reporting discipline and investor confidence, not simply as a box to check. But make sure that you double-check if it applies to your organization.

Who Does ASC 740 Apply To?

Accurately identifying which entities fall under ASC 740 is key to implementing tax accounting properly:

Public business entities under U.S. GAAP must follow ASC 740 for income tax accounting. This includes the asset/liability method for deferred taxes and detailed disclosure requirements introduced under ASU 2023-09.

Private companies and not-for-profit organizations preparing GAAP-compliant financial statements must also follow ASC 740. However, some disclosure mandates differ from public entities (FASB Improvements to Income Tax Disclosures and FASB Project Summary).

Foreign entities that report under U.S. GAAP, such as subsidiaries of U.S. firms or multinational firms listed in the U.S., must comply with ASC 740 (SEC Filing Example).

Partnerships are generally excluded unless taxed at the entity level rather than pass-through.

Pro Tip: Even private companies should maintain strong ASC 740 processes to prevent tax provision errors and reduce audit risk.

Knowing where your business fits under ASC 740 should be the ideal starting point for accurate and dependable tax reporting.

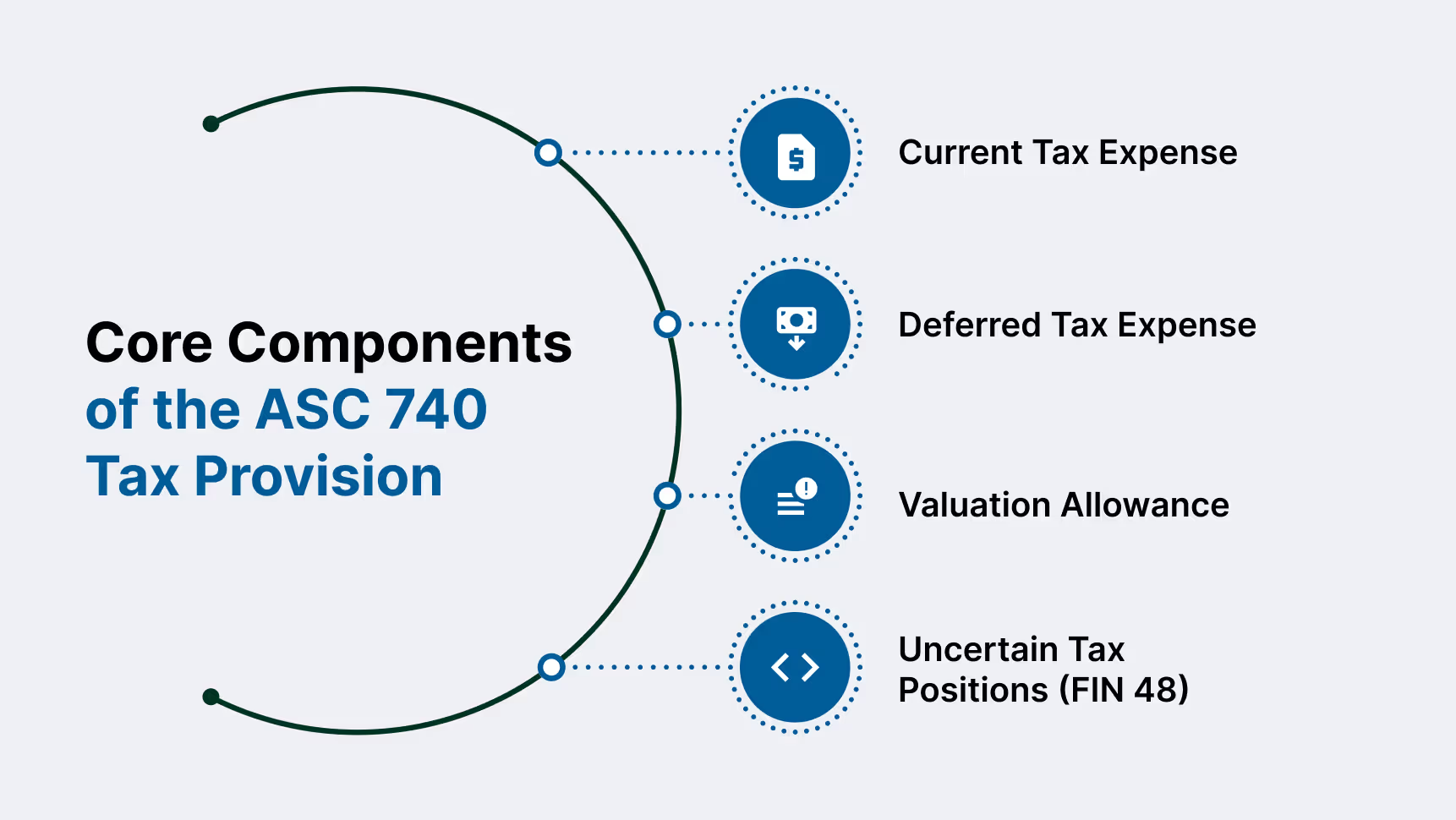

Core Components of the ASC 740 Tax Provision

[Infographic Here: Breaking Down the Key Elements of ASC 740]

The tax provision under ASC 740 is comprised of Current Tax, Deferred Tax, and Valuation Allowance, along with the specialized framework for Uncertain Tax Positions (FIN 48).

1. Current Tax Expense

Based on taxable income for the current year as reported on filed returns.

Adjusted for permanent differences, such as non-deductible expenses like fines or penalties that impact GAAP versus tax income.

2. Deferred Tax Expense

Arises from temporary differences between book and taxable income (for example, accelerated depreciation under tax rules).

Uses the asset/liability method outlined in ASC 740:

Deferred Tax Assets (DTAs): Represent future deductions, such as net operating loss carryforwards (NOLs).

Deferred Tax Liabilities (DTLs): Represent future taxable amounts created by differences like accelerated depreciation.

3. Valuation Allowance

A valuation allowance offsets DTAs that are unlikely to be realized, following the "more-likely-than-not" test in ASC 740-10-30.

Both positive and negative evidence (such as past profitability trends) must be evaluated objectively (RSM Valuation Allowance Guide).

4. Uncertain Tax Positions (FIN 48)

FIN 48 (codified in ASC 740-10) governs how companies recognize uncertain tax positions:

Recognition Step: Determine if a tax benefit meets the more-likely-than-not threshold.

Measurement Step: Record the most significant benefit that is more than 50% likely to be sustained.

Requires disclosure of tabular rollforwards, interest and penalty accruals, and positions under audit.

A well-structured tax provision under ASC 740 not only ensures compliance but also strengthens financial transparency and builds confidence with auditors, regulators, and investors alike.

ASC 740 Disclosure Updates (ASU 2023‑09)

[Infographic: Key Changes in ASC 740 Disclosures]

Starting in fiscal 2024 for public business entities and 2025 for private entities, ASU 2023‑09 introduces substantial enhancements to income tax disclosures under ASC 740. Its purpose is to improve transparency and provide investors and regulators with clearer insight into income tax metrics (FASB ASU 2023‑09 PDF).

New disclosure requirements include:

Tax expense breakdown by jurisdiction, including federal, state/local, and foreign taxes paid, with further breakdown when a jurisdiction exceeds a 5% threshold of total taxes paid.

Practical tax rate reconciliation across eight defined categories, disclosed using both percentages and reporting‑currency amounts (Deloitte Heads‑Up).

Disclosure of dollar amounts and percentages, enhancing comparability and insight into tax-related reconciling items (RSM June 2025 Guidance).

These updates require more granular tracking of tax data, stronger coordination among finance, tax, and audit teams, and enhanced documentation to satisfy heightened scrutiny.

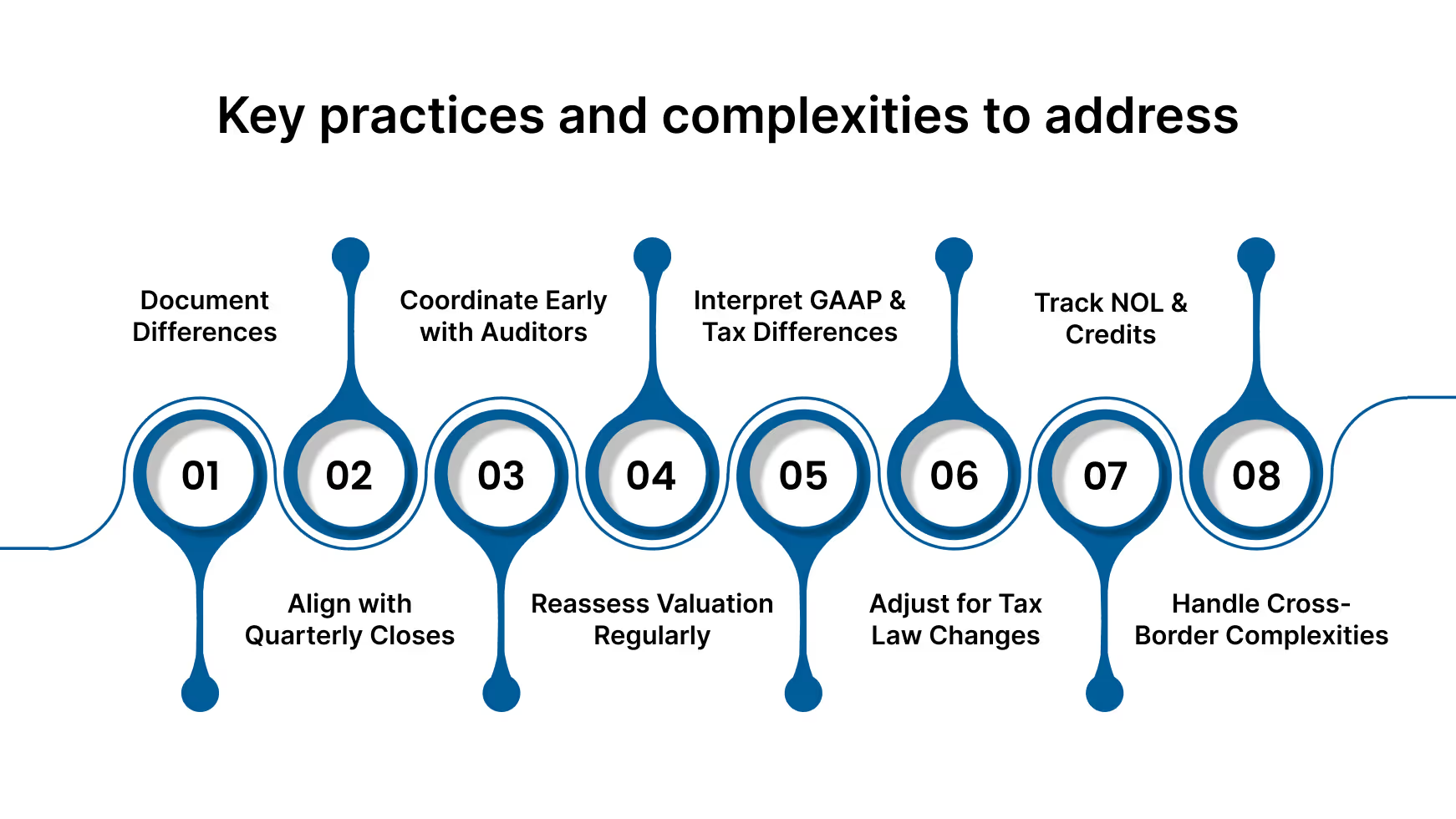

Internal Controls and Year-End Planning for ASC 740

[Infographic: Best Practices for ASC 740 Compliance]

Effective ASC 740 compliance depends on strong internal controls and proactive year-end planning. Robust processes reduce the risk of misstatements and eliminate last-minute tax provision adjustments.

For public companies, ASC 740 provision review is integral to SOX compliance frameworks, as outlined by the U.S. Securities and Exchange Commission (SEC).

These are some key practices and complexities to address:

Document Temporary Differences: Maintain detailed schedules for each deferred tax item to support accurate provision calculations and facilitate audit readiness.

Align Provision Timing with Quarterly Closes: Treat interim provision reviews as trial runs to identify issues early and prevent year-end surprises.

Coordinate with Auditors Proactively: Provide preliminary provision workpapers in advance to streamline review and reduce delays during audit season.

Reassess Valuation Allowances Regularly: Reevaluate evidence supporting deferred tax asset realizability, especially in volatile or loss-making periods.

Interpret GAAP and Tax Law Differences Correctly: Understand timing versus permanent differences to avoid errors in deferred tax calculations.

Incorporate Tax Law Changes Promptly: Adjust deferred balances for rate changes in the period they are enacted, consistent with IRS guidance.

Track NOL Carryforwards and Credits: Monitor expiration schedules and usage to ensure accurate deferred tax asset reporting.

Address Cross-Border Complexities: Apply U.S. GAAP correctly for foreign subsidiaries, including Section 987 translation rules and global minimum tax impacts.

Outsource your bookkeeping and save time without compromising accuracy. Let us handle the books.

Companies that integrate these practices into their tax provision process strengthen compliance, improve audit outcomes, and build confidence with investors and regulators.

How VJM Global Supports ASC 740 Tax Provision and Audit Compliance

VJM Global offers specialized accounting outsourcing and audit support tailored for U.S.-based companies and CPA firms navigating complex ASC 740 requirements.

With deep expertise in U.S. GAAP and a strong understanding of Indian regulatory processes, our offshore teams help reduce operational burden while maintaining full compliance with ASC 740 tax provision standards.

We assist with:

Preparing and reviewing income tax provisions under ASC 740 for public and private U.S. entities

Supporting CPA firms during peak seasons with offshore audit documentation, reconciliations, and footnote disclosures

Ensuring readiness for ASU 2023-09 disclosures, including jurisdiction-level breakouts and effective tax rate reconciliations

Facilitating cross-border reporting for U.S. companies with foreign operations subject to Section 987 or Pillar Two impacts

Our teams work seamlessly with in-house finance and tax departments, helping clients reduce errors, stay audit-ready, and meet evolving compliance expectations with confidence.

Ensure error-free financial reporting with our seasoned accounting experts.

FAQs on ASC 740 Income Tax Accounting

1. Who needs to follow ASC 740?

Any entity preparing financial statements under U.S. GAAP, including public, private, not-for-profit, and foreign subsidiaries of U.S. companies, must apply ASC 740.

2. What is the ‘more-likely-than-not’ threshold?

It means there is a greater than 50% chance a tax position will be sustained on its technical merits if challenged by tax authorities.

3. When do private companies need to adopt ASU 2023-09?

For fiscal years beginning after December 15, 2024, private companies must implement the enhanced disclosure requirements.

4. How does ASC 740 handle changes in tax rates?

Deferred tax assets and liabilities must be adjusted in the reporting period when a new tax rate is enacted, which affects that period’s tax expense.

5. What is FIN 48, and how is it related to ASC 740?

FIN 48, now part of ASC 740-10, sets out rules for recognizing, measuring, and disclosing uncertain tax positions.

VJM Global

Explore expert insights, tips, and updates from VJM Global

%20(5).avif)