%20(14).avif)

In India, Corporate Social Responsibility (CSR) activities are governed by the Companies Act, 2013, which outlines specific guidelines for businesses to contribute to social, environmental, and community development.

For companies wishing to engage in CSR activities, CSR-1 registration has become a critical requirement, with the average actual CSR spend per company increasing to INR 54 Cr in FY 2023-24 from INR 22 Cr in FY 2014-2015. This process ensures transparency, compliance, and effective channeling of funds into sustainable and impactful projects.

In this blog, we will break down everything you need to know about the CSR-1 form applicability, including the detailed steps for registration and CSR activities that are eligible for funding and common challenges businesses face during CSR registration.

The CSR-1 form is a registration form required for organizations that intend to receive Corporate Social Responsibility (CSR) funding from companies in India. It serves as a mandatory compliance requirement for NGOs, trusts, societies, and Section 8 companies, organizations that wish to accept CSR funds from businesses in India.

CSR-1 registration ensures that the receiving organizations meet the legal criteria set out by the Ministry of Corporate Affairs (MCA) and are eligible to participate in CSR funding programs. It allows businesses and corporate donors to trust that the funds they allocate for CSR activities will be utilized for the intended social causes in a transparent and accountable manner.

Registering a new business demands airtight compliance. VJM Global simplifies it for your companies through end-to-end audit, tax, and regulatory support. From FEMA advisory to GST audit and transfer pricing management, we ensure every compliance box is checked before your operations go live.

IMAGE CTA 8

According to Section 135 of the Companies Act, 2013, CSR provisions are applicable to companies meeting the following criteria:

These companies must allocate at least 2% of their average net profits over the last three financial years to CSR activities.

Also Read: Offshoring Audit Work from the US to India: Key Challenges and Fixes

Filing the CSR-1 form is an essential step for organizations to become eligible for CSR funding. The form requires the following details:

Now that we understand the CSR-1 form, let’s explore who is eligible to apply for this registration.

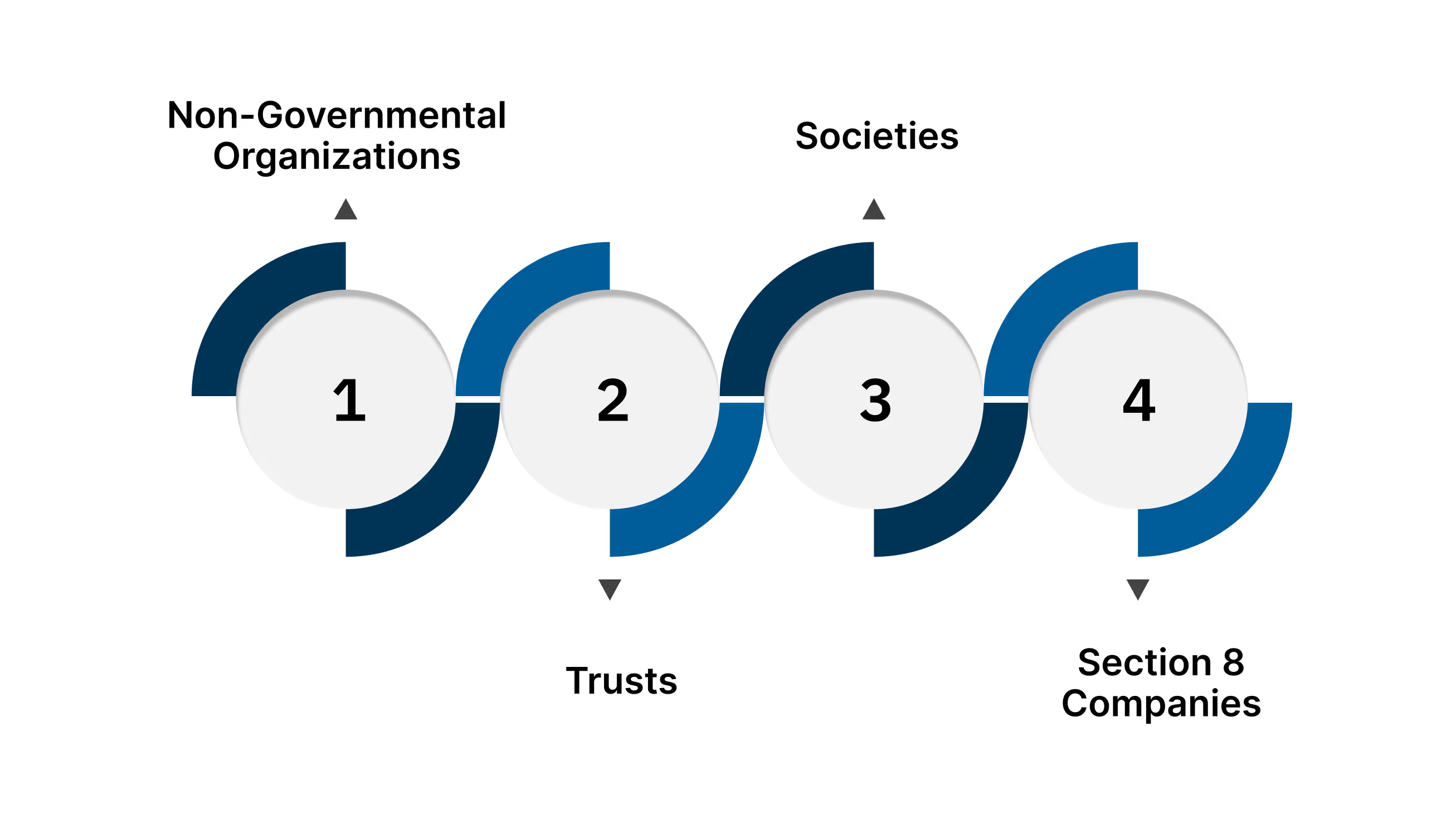

Several types of entities can apply for CSR-1 registration to be eligible for CSR funding, including:

These entities must submit their application to the Ministry of Corporate Affairs (MCA), providing the necessary documents and certifications to qualify for receiving CSR funds.

Next, we’ll examine why CSR-1 registration is important for businesses looking to contribute to social causes in India.

CSR-1 registration is a crucial step for entities seeking CSR funds in India. Here are the key reasons why registration is vital:

Also Read: What Is a Fractional Controller and Why US Firms Outsource to India

Now, let’s take a closer look at which CSR activities are eligible to receive funds under the CSR-1 registration process.

Under Schedule VII of the Companies Act, 2013, eligible CSR activities include various social, environmental, and educational initiatives. Here are the main categories:

Indian law, through Schedule VII, encourages businesses to focus their CSR funds on these impactful areas to promote overall development in the country.

Now that we know which activities are eligible for CSR funding, let’s explore the step-by-step guide to registering for CSR-1.

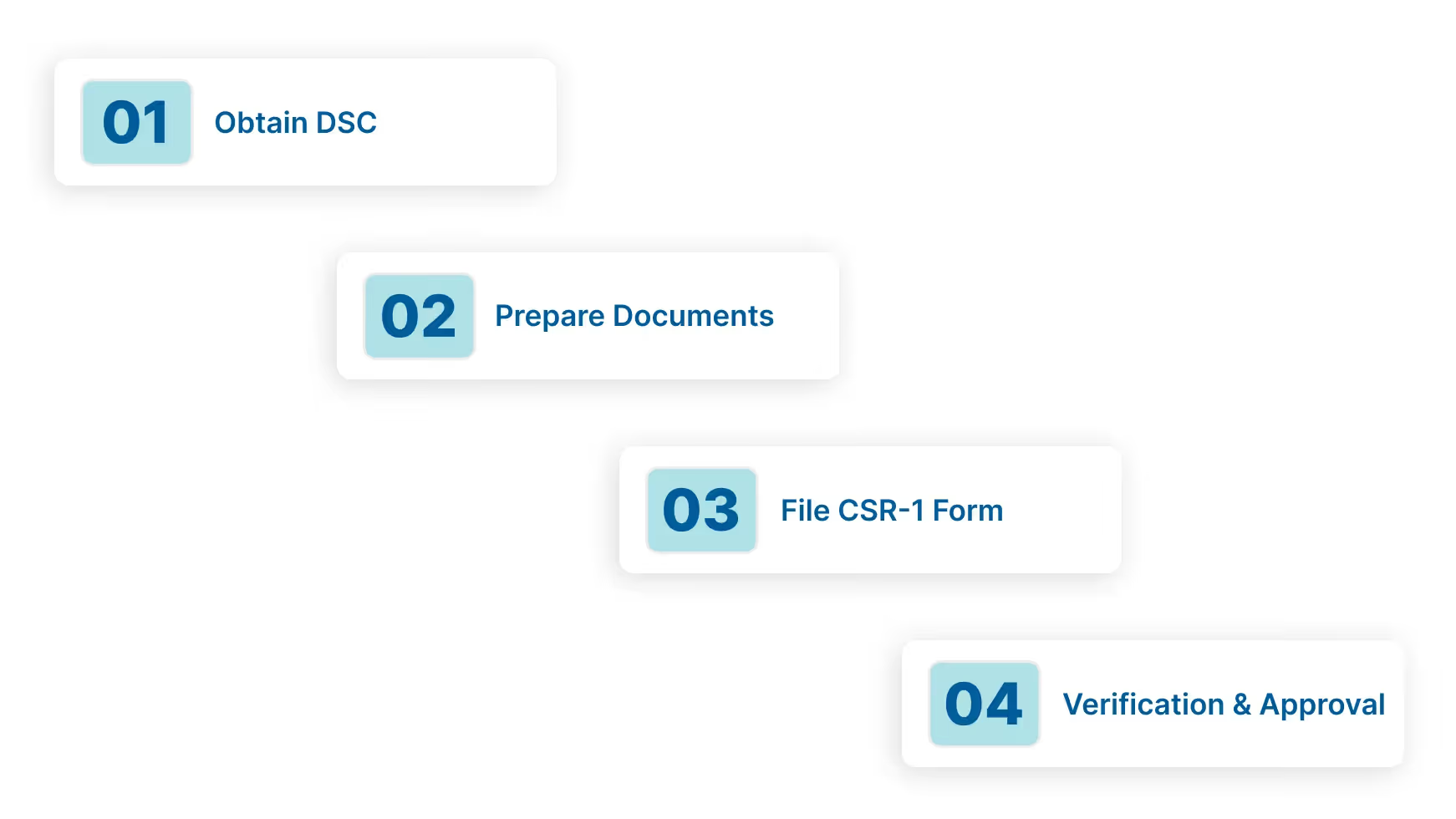

Registering for CSR funding involves several steps. Here’s how organizations should approach the process:

The authorized representative must obtain a Digital Signature Certificate (DSC) to sign the CSR-1 form. The DSC is an electronic signature used for official submissions and ensures data authenticity.

To ensure smooth registration, the following documents must be submitted:

Visit the MCA portal and log in. Select CSR-1 registration, fill out the application form, and upload the necessary documents. The form must be submitted with the DSC of the authorized representative.

Once the MCA receives the CSR-1 form and documents, they will verify the application. Upon approval, the CSR-1 Registration Certificate will be issued. This certificate validates the entity’s eligibility for CSR fund allocation.

VJM Global can help you handle corporate tax planning, internal audits, and cross-border transaction compliance. Our experts help align your financial reporting with accounting and taxation frameworks, minimizing legal exposure and maximizing operational efficiency.

IMAGE CTA 7

Also Read: Complete Restaurant Bookkeeping Guide: US to India Expansion

Now that we know how to register, let's look at the penalties for not adhering to CSR in India.

For companies involved in Corporate Social Responsibility (CSR) activities, non-compliance with the CSR provisions under the Companies Act, 2013, can result in significant legal and financial consequences. Specifically, Section 135(7) of the Act stipulates penalties for failure to adhere to CSR requirements, which must be carefully navigated by foreign businesses to avoid costly fines and reputational damage.

According to Section 135(7) of the Companies Act, if a company fails to comply with CSR provisions, it faces the following penalties:

This penalty structure highlights the seriousness of CSR compliance in India and underscores the importance of proper financial planning and reporting for U.S. businesses involved in CSR activities.

Not only is the company itself liable, but the directors and officers in default are also subject to penalties under the same provisions. As per Section 135(7), every officer of the company who is in default shall be liable to the following penalties:

Also Read: Food and Beverage Accounting: A U.S. Guide to Overcoming Global Challenges

Next, let's look at how CSR-1 registration connects with other essential government registrations in India.

Several additional government registrations are required for businesses engaging in CSR in India:

Let’s now explore some of the common challenges businesses face during CSR-1 registration and how to overcome them.

While CSR-1 registration is essential for receiving CSR funds, businesses often face various hurdles during the application process. Understanding these challenges will help you overcome them effectively.

1. Documentation Issues: Missing or incorrect documents may delay the registration process.

Solution: Ensure all documents are accurate and validated by a practicing professional.

2. Name Mismatch with MCA Records: Discrepancies between your company name in the MCA database and the submitted documents can delay the process.

Solution: Cross-check business names with MCA records before submission.

3. Digital Signature Errors: DSC errors may prevent the submission of CSR-1 forms.

Solution: Verify DSC and ensure it's correctly linked to the authorized representative.

4. Delayed Approval: Approval may take longer than expected due to document verification.

Solution: Submit applications well in advance and follow up regularly with MCA.

Also Read: How to Manage Café Accounting: Owner's Guide from the US to India

The following section outlines the statutory provisions and authorities responsible for CSR oversight.

The CSR-1 registration process in India is governed by specific laws and regulatory authorities to ensure transparency and compliance with corporate social responsibility guidelines.

With the legal foundation clarified, the focus now shifts to what lies ahead in India’s CSR system.

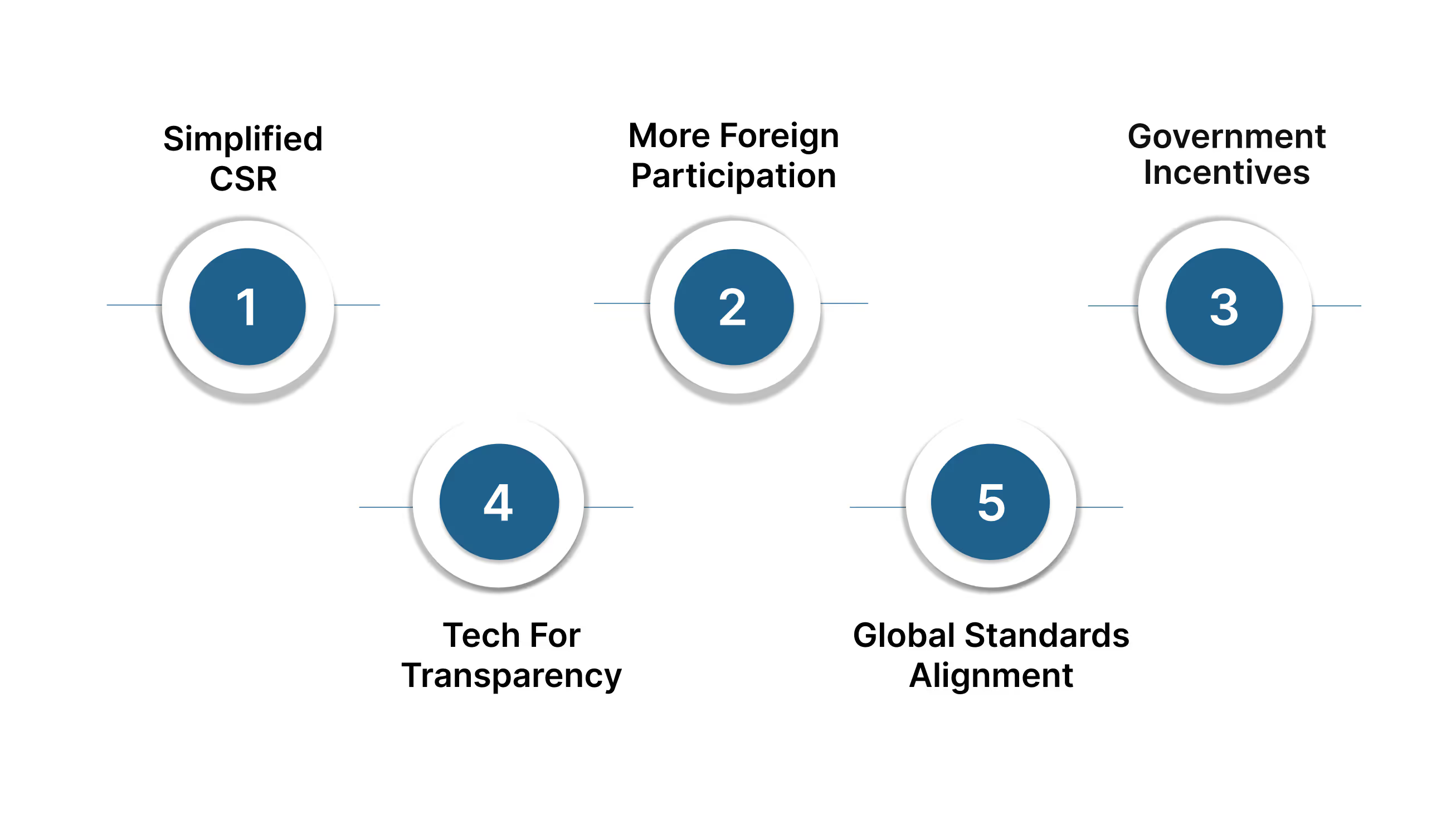

As India continues to promote CSR-driven initiatives, the CSR-1 registration process is expected to change. Here’s a look at how CSR funding may progress in the coming years.

Also Read: Top Bookkeeping and Accounting Practices for US Law Firms

Let's now examine how VJM Global can assist your US entity in entering India while upholding full compliance.

Expanding your business comes with immense growth potential but also complex compliance obligations across taxation, auditing, and cross-border transactions. VJM Global acts as your compliance partner, helping you meet every legal and regulatory requirement with precision and confidence.

1. U.S. Business Setup & Structuring in India: VJM Global assists your company in selecting the most compliant business structure, liaison office, branch office, or subsidiary, while aligning with RBI, FEMA, and MCA norms. Our experts ensure you meet all legal and financial prerequisites from day one.

2. GST Compliance & Advisory Services: Our GST specialists manage everything from registration, audits, and refunds to strategic advisory. We conduct GST impact analysis and provide ongoing outsourcing support, allowing you to stay tax-efficient and compliant while focusing on your core business operations.

3. Audit & Assurance for Risk-Free Operations: We conduct comprehensive internal, statutory, and management audits to strengthen financial governance. Our audit framework ensures adherence to the Companies Act, 2013 and Indian Accounting Standards (Ind AS), helping businesses maintain transparency and investor trust.

4. Direct & Cross-Border Taxation Expertise: VJM Global simplifies corporate tax, transfer pricing, and withholding compliance under the relevant tax laws. Our FEMA and DTAA advisory ensures that cross-border transactions between your company branches remain tax-efficient and fully compliant.

5. Strategic Risk, Assurance & Transaction Advisory: From due diligence audits to mergers, acquisitions, and joint ventures, we guide businesses through every strategic move. Our insights help mitigate risks, maintain compliance, and ensure smooth business expansion.

At VJM Global, we go beyond compliance; we help your business operate confidently with clarity, control, and complete compliance.

Businesses must understand the applicability of the CSR-1 form for compliance and efficient engagement in corporate social responsibility activities. With proper registration and adherence to Indian CSR regulations, your company can make a significant social impact while building its reputation in India.

VJM Global provides continuous oversight for your companies, offering statutory audits, due diligence reviews, and GST representation before tax authorities. In case your entity is setting up a subsidiary, joint venture, or branch office, we ensure full compliance with the regulatory, tax, and corporate laws, from incorporation to daily operations.

Contact VJM Global and let our experts handle every regulatory detail with precision.

CSR-1 registration ensures that nonprofit organizations are eligible to receive CSR funds from companies in India by ensuring compliance with the Companies Act, 2013.

Only NGOs, trusts, societies, and Section 8 companies working on charitable activities are eligible for CSR-1 registration to receive CSR funding in India.

Foreign entities or U.S. businesses cannot directly apply for CSR-1 registration, but can partner with local registered NGOs to receive CSR funds in India.

Yes, any organization intending to receive CSR funds from Indian companies must complete CSR-1 registration as per Section 135 of the Companies Act, 2013.

Documents such as PAN, registration certificates, details of board members, DSC, and certification from CA/CS/CMA are required for CSR-1 registration.