.webp)

Federal Excise Tax (FET) on trucks is a federal sales tax applied to the first retail sale of particular heavy trucks, tractors, and trailers.

If you’re a U.S. truck dealer, fleet owner, or a business that regularly purchases commercial vehicles, this tax directly affects your bottom line and compliance obligations.

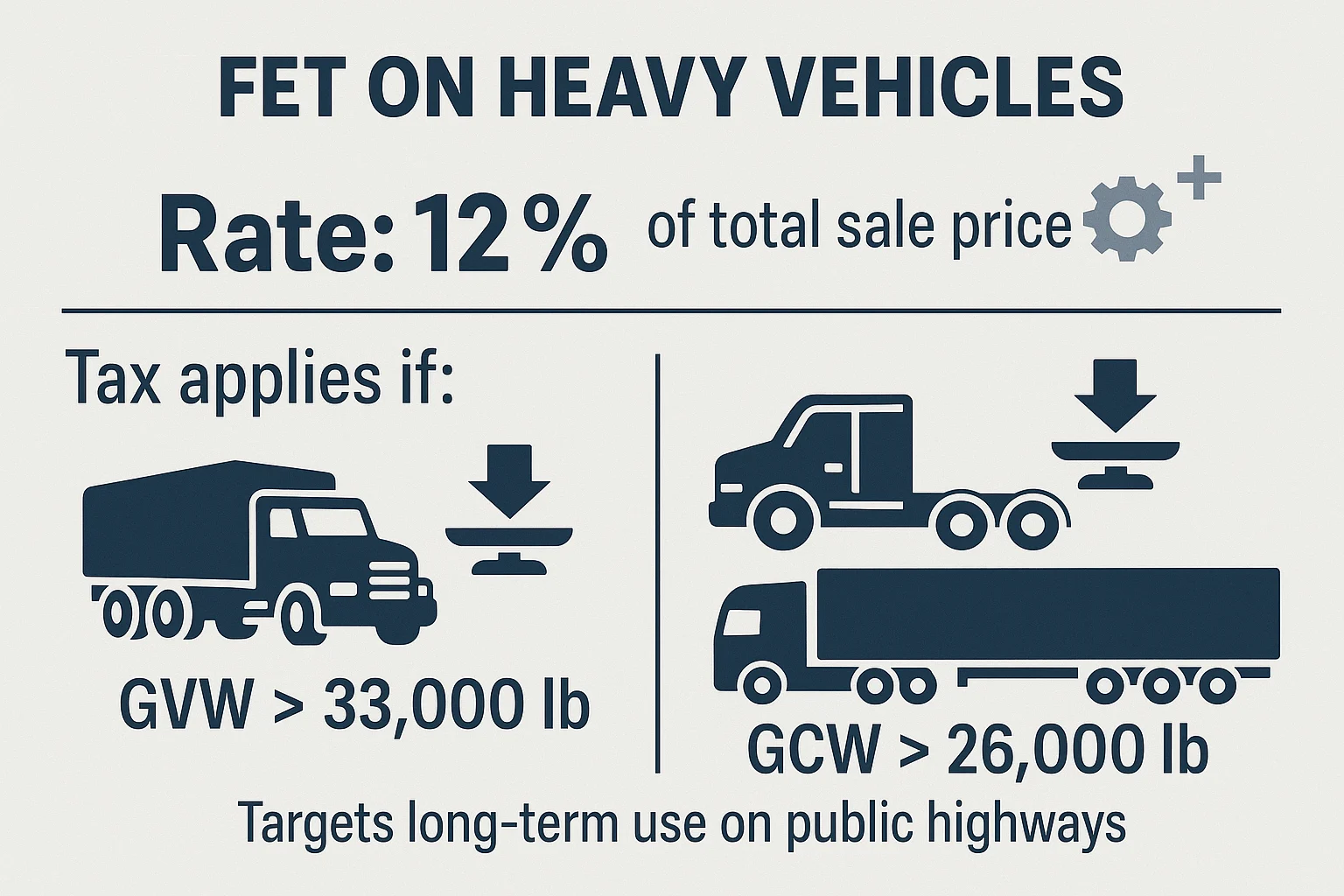

Under current IRS regulations, the FET is generally 12% of the total sale price of qualifying vehicles, including any parts or accessories sold as part of the transaction (IRS Form 720 Instructions).

Filing and paying it correctly is essential because mistakes can lead to penalties, delayed sales, or audit issues that disrupt operations.

Understanding when the tax applies, which transactions qualify for exemptions, and how to file accurately can save you time, money, and unnecessary stress. This blog will break down the essentials and give you a clear path to staying compliant.

The Federal Excise Tax on trucks is part of a group of federal taxes applied to specific goods and activities. It is not a general sales tax. Instead, it targets certain high-value, high-impact transactions that have a direct link to the federal highway system.

According to the IRS, the tax applies to the first retail sale of a “highway vehicle” that meets the weight and design criteria outlined in Internal Revenue Code Section 4051. This usually means trucks, tractors, and trailers built for commercial hauling rather than personal transport.

For trucks, the IRS describes a qualifying vehicle as one “primarily designed to carry a load over public highways,” other than passengers. Tractors are classified as vehicles “primarily designed to tow a trailer or semi-trailer over public highways” (IRS Form 720 Instructions). These definitions matter because they decide whether a transaction falls under FET rules.

Understanding these distinctions helps sellers and buyers avoid costly misclassification. If a vehicle meets the IRS definition and exceeds the weight thresholds, the sale will likely trigger the 12% FET, even if the parties are unaware of the requirement.

Also Read: Understanding US GAAP Revenue Recognition Standards

The Federal Excise Tax on trucks is part of a group of federal taxes applied to specific goods and activities. It is not a general sales tax. Instead, it targets certain high-value, high-impact transactions that have a direct link to the federal highway system.

According to the IRS, the tax applies to the first retail sale of a “highway vehicle” that meets the weight and design criteria outlined in Internal Revenue Code Section 4051. This usually includes:

These definitions matter because they determine whether a transaction falls under FET rules. Understanding them helps both sellers and buyers:

Precise classification from the start can make FET compliance much smoother for all parties involved. It also serves as the foundation for understanding the specific circumstances under which the tax must be calculated and paid.

The FET is triggered when a qualifying truck, tractor, or trailer is sold at retail for the first time. This point of sale, known as the “first retail sale,” is when the buyer takes ownership for use rather than resale. The seller is responsible for collecting the tax from the buyer and remitting it to the IRS.

Filing and payment are done using IRS Form 720, the Quarterly Federal Excise Tax Return. This form must be submitted along with the payment for the tax due in the applicable quarter. Accurate reporting is essential to avoid penalties or processing delays.

Quarterly filing deadlines for Form 720 are as follows:

Pro Tip: As a business, you should focus on maintaining clear transaction records, including invoices, bills of sale, and vehicle specifications, to support the information reported on Form 720.

This ensures the IRS can verify the accuracy of the filing if questions arise. Consistent, organized recordkeeping not only satisfies legal requirements but also makes it easier to determine eligibility for exemptions or special filing considerations.

Once you know when and how to file sets, you can better understand how the tax itself is calculated.

The standard FET rate for qualifying trucks, tractors, and trailers is 12% of the total sale price. This includes not only the base cost of the vehicle but also any parts or accessories sold as part of the transaction.

Weight is a key factor in determining whether a vehicle is subject to FET. The tax generally applies when:

These thresholds ensure the tax targets heavy commercial vehicles intended for long-term use on public highways. Accurately calculating the taxable amount helps prevent underpayment or overpayment.

It also allows businesses to identify when certain sales might qualify for exemptions, which can reduce costs and improve compliance confidence.

Also Read: Documents Needed for Private Limited Company Registration

In most cases, the sale of a used truck is not subject to FET because the tax only applies to the first retail sale. This means that once FET has been paid on a qualifying vehicle, subsequent sales generally fall outside its scope.

However, exceptions do exist, and sellers should confirm the tax status before finalizing any transaction. According to the IRS Form 720 Instructions, used truck sales may still trigger FET if:

Certain transactions are also excluded from FET, even for new vehicles, such as:

Clarifying whether a sale is considered “used” in the eyes of the IRS helps prevent unexpected liabilities and keeps both parties aligned on compliance responsibilities. With the path clear on how used truck sales are treated, the next step is to remember the exemptions that can take certain transactions entirely out of the FET picture.

The FET on trucks is more than just a cost of doing business; it plays a critical role in funding public infrastructure. A significant portion of the revenue collected through FET is directed to the Highway Trust Fund, which supports the construction, maintenance, and repair of the U.S. highway system.

According to the Federal Highway Administration, this fund helps cover the costs of:

By design, the FET ensures that those who use heavy commercial vehicles, and thereby place greater strain (by occupying more space) on public roads, contribute proportionally to their upkeep.

Understanding where these funds go offers a broader perspective on why the tax exists and how it connects private operations to national infrastructure priorities.

Also, Read:

FET rules can quickly become complex, especially when exemptions, modifications, or high-value transactions are involved. Missteps may lead to penalties or delays.

A qualified advisor can help you:

If your business deals in commercial vehicle sales, fleet operations, or exports, tax guidance is more than helpful. It protects your margins and your compliance.

Staying compliant with FET requirements takes more than knowing the 12 percent rate. It means understanding when the tax applies, how to calculate it accurately, and which exemptions can lawfully reduce your liability. It also calls for clear documentation and timely filing to keep your operations running without interruption.

VJM Global partners with U.S. businesses, truck dealers, and CPA firms to provide:

By combining deep tax knowledge with a focus on operational efficiency, we help you meet your obligations and protect your bottom line.

FET generally does not apply to standard operating leases. However, if the lease is structured in a way that effectively transfers ownership at the end of the term, the IRS may consider it a taxable sale.

Yes. Many lenders allow the FET amount to be included in the financing package for the vehicle. This means the buyer pays the tax over time as part of the loan, rather than in a single lump sum.

FET is a federal tax and is separate from state or local sales taxes. Both can apply to the same transaction, and each must be calculated and reported according to its own rules.

If substantial modifications are made before the first retail sale, their value is generally included in the FET calculation. Aftermarket work done after the sale typically does not trigger additional FET, but it may affect warranties or state regulations.

The IRS typically has three years from the date of filing Form 720 to audit an FET return. In cases of fraud or significant underreporting, the statute can be extended.

If a sale is rescinded and the vehicle is returned, the seller may be eligible to claim a credit or refund for the FET paid, provided proper documentation is submitted to the IRS.