Considering expanding R&D operations to India? US companies can capitalize on a favorable tax environment that offers a 100% deduction on eligible research expenses, covering in-house and partnered innovations.

India’s flexible regulations, cost-effective talent, and reduced customs and GST rates speed product development while minimizing overhead. This environment helps American firms diversify global R&D investments, improving cash flow and technological growth.

This guide explains how US companies can strategically benefit from tax incentives for R&D in India, going through the regulations to take full advantage.

Key Takeaway

Substantial Tax Benefits Under Section 35: US businesses in India can claim a 100% deduction on revenue and capital R&D expenditures, significantly lowering their taxable income and improving innovation cost-efficiency.

DSIR Recognition Opens Broad Incentives: Recognition by India’s DSIR allows zero customs duty on R&D imports, GST reductions, and access to government grants, accelerating cost savings and operational ease for US firms.

Extensive Deductible R&D Expenses: Eligible deductions cover operational costs like salaries, utilities, raw materials, and capital equipment, excluding land, allowing complete financial relief across diverse R&D activities.

Full Compliance and Documentation Requirements: Companies must maintain detailed financial, technical, and statutory records, including DSIR approval, and file annual returns like Form 3CL to sustain their eligibility for tax incentives.

Industry-Specific Incentives Improve Strategic R&D: Pharma, IT, electronics, aerospace, and renewable sectors benefit from customized incentives, such as weighted deductions, patent tax rates, and accelerated depreciation, driving more focused investment.

Understanding Tax Incentives for R&D in India

Tax incentives for R&D in India represent a comprehensive framework designed by the government to promote scientific research and development activities across industries. These tax incentives operate primarily through Section 35 of the Income Tax Act 1961, which provides substantial deductions for businesses and organizations investing in research activities.

The system aims to reduce the financial burden of R&D investments while encouraging companies to develop new technologies, products, and processes that can drive economic growth and technological advancement.

Tax incentives for R&D in India have gained significant momentum following the government's commitment to allocate ₹20,000 crore for private sector-driven research and development in Budget 2025-26, marking a substantial increase from previous allocations.

This framework contains various types of deductions, customs duty exemptions, and GST benefits that make India an attractive destination for both domestic and international companies seeking to establish research facilities.

What does Tax Incentive for R&D in India Mean for US Businesses?

Tax Incentive for R&D in India offers clear financial advantages to US companies investing in research activities within the country. Recognizing the specific provisions and benefits can help American firms effectively plan and allocate resources for their innovation efforts.

Below are key details tracing how these incentives apply to US businesses operating in India.

Section 35 Tax Deduction: US companies operating in India through subsidiaries or permanent establishments can claim a 100% deduction on both revenue and capital R&D expenditures under Section 35 of the Income Tax Act.

DSIR Recognition: Foreign firms registered in India, including US subsidiaries, qualify for Department of Scientific and Industrial Research recognition, showing benefits like tax deductions and customs duty exemptions on R&D imports.

Customs Duty and GST Benefits: DSIR-approved entities enjoy zero basic customs duty on equipment and inputs, plus reduced GST rates, 5% for interstate and 2.5% CGST plus 2.5% SGST on intrastate transactions.

Accelerated Depreciation: US companies can claim 100% depreciation on research assets in the first year, optimizing capital expense treatment.

Pre-Operational R&D Deductions: Research expenses incurred up to three years before starting business operations in India are deductible once operations commence.

Collaborative Research Contributions: Payments to approved Indian research bodies are deductible up to 100–150%, encouraging partnerships.

Expense Coverage: All operational expenses, including salaries, utilities, raw materials, and consumables, qualify for full deduction in the year incurred.

Exclusions and Documentation: Land costs are non-deductible, and detailed records and DSIR approvals are essential to claim benefits.

Access to Govt Support: DSIR-registered US subsidiaries may also access government grants, subsidized loans, and equity support for their R&D activities.

Plan ahead with expert insights that can help businesses go through global rules and minimise risks, and explore practical approaches in International Tax Planning Strategies for 2025.

Tax Incentives for R&D in India: Benefits Structure

Tax Incentives for R&D for US businesses in India come with a structured framework that defines how different research expenditures are recognized and deducted. Understanding the specific categories and their conditions can help set realistic expectations for tax planning and compliance.

Here’s a clear overview of the key benefits and requirements associated with these incentives.

Expenditure on Scientific Research

Tax Deduction Rate

Section Reference

Key Requirements & Conditions

Form Required

In-house revenue expenditure

100% of expenditure

Section 35(1)(i)

Must be related to business operations

Not specified

In-house capital expenditure (excluding land & building)

100% of expenditure (land cost excluded)

Section 35(1)(iv)

Separate books required; excludes land & building costs

Form 3CK for DSIR approval

Pre-commencement expenditure (within 3 years before business)

100% in the year the business commences

Section 35(1)(i)

Expenditure incurred within 3 years before business start

Not specified

Payment to an approved scientific research company (Indian entity)

100% of payment

Section 35(1)(iia)

An Indian company with scientific research as its main objective

Approval from the Income Tax Authority is required

Contribution to an approved research association/university

100%

Section 35(1)(ii)

The institution must be government-approved

Not specified

Payment to national laboratory/IIT/university

100%

Section 35(2AA)

Recognized by the prescribed authority with an approved program

Form 3CG for approval

Payment to specified person approved by prescribed authority

100%

Section 35(2AA)

Must be approved by the prescribed authority (DSIR)

Form 3CG for approval

In-house R&D by biotechnology/manufacturing companies

Capital expenditure on scientific research equipment

100% of capital expenditure

Section 35(1)(iv)

Equipment only; excludes land & building purchase

Form 3CK for expenditure > INR 1 crore

Historical Context

The tax incentives for R&D in India have undergone substantial modifications:

Pre-2017: 200% weighted deduction under Section 35(2AB).

2017-2021: Reduced to 150% weighted deduction.

2021-Present: Further reduced to 100% standard deduction.

This represents a policy shift from generous weighted deductions to a more balanced approach focusing on patent commercialization through the Patent Box Regime.

Step-by-Step Guide: How US Companies Can Benefit from R&D Tax Incentives in India

Tax incentives for R&D in India provide significant financial benefits to companies conducting scientific research and development activities. These deductions, primarily governed under Section 35 of the Income Tax Act, allow businesses to claim a 100% deduction on both revenue and capital expenditures related to approved R&D activities.

Before claiming any tax benefit, businesses must first check if they meet the core eligibility rules.

Eligibility Requirements

Here are the key requirements these businesses must satisfy.

Aspect

Details

Legal & Operational Status

Must be registered in India under the Companies Act, 2013, including partnerships or LLPs.

Business History

Three financial years must be completed since the start of operations.

R&D Infrastructure

Must have identifiable facilities, qualified personnel, and defined R&D programs.

Facility Size & Location

R&D activities must be carried out on the premises or in dedicated facilities of at least 1,000 sq. ft., in designated areas within India.

Technical Staff

Must demonstrate the availability of sufficient skilled personnel for R&D operations.

Fulfilling eligibility isn’t enough; businesses also need DSIR recognition to validate their in-house R&D units formally.

VJM Global’s international taxation experts help businesses manage complex cross-border compliance while providing eligibility requirements, DSIR recognition, and structured R&D infrastructure that are fully aligned with Indian and global regulatory standards. Talk to our experts!

DSIR Recognition Process

Securing DSIR recognition in India requires following a defined process that verifies the capabilities and compliance of in-house R&D units. Here’s an overview of the key steps involved.

Initial Registration: Register online at the DSIR website and submit an application for recognition of in-house R&D units through the dedicated portal.

Application Submission: Submit both soft copy and hard copy of the application with supporting documents to the DSIR office via speed post.

Meeting at DSIR: DSIR calls the applicant for a meeting with a walk-in video presentation and demonstration of the R&D center capabilities.

Recognition Decision: DSIR evaluates the application and either grants recognition or rejects it based on compliance with guidelines and infrastructure assessment.

Site Visit Possibility: DSIR team may conduct a physical visit to the R&D center, depending on the application requirements and verification needs.

With DSIR recognition in place, the next step for businesses is obtaining Section 35(2AB) approval to unlock deduction benefits.

Need an India subsidiary? We handle FDI approvals, taxation, and local compliance.

Section 35(2AB) Approval Process

Claiming tax benefits under Section 35(2AB) involves a formal approval process that confirms compliance and allows immediate deductions on R&D capital expenses. The main steps in this process are as follows.

Step

Description

Form 3CK Application

Submit Form 3CK to DSIR with detailed R&D information, audited financial statements, infrastructure details, and compliance certificates.

Agreement Execution

Sign a formal agreement with the Secretary, DSIR, establishing cooperation in research and the audit of financial accounts.

Form 3CM Receipt

The company receives an approval certificate in Form 3CM from DSIR for a specific period, as per DSIR guidelines.

Tax Benefit

Eligible to claim a 100% deduction on approved capital R&D expenses in the first year without waiting for depreciation.

Approvals remain valid only when backed by the right documents, making documentation a critical step for businesses.

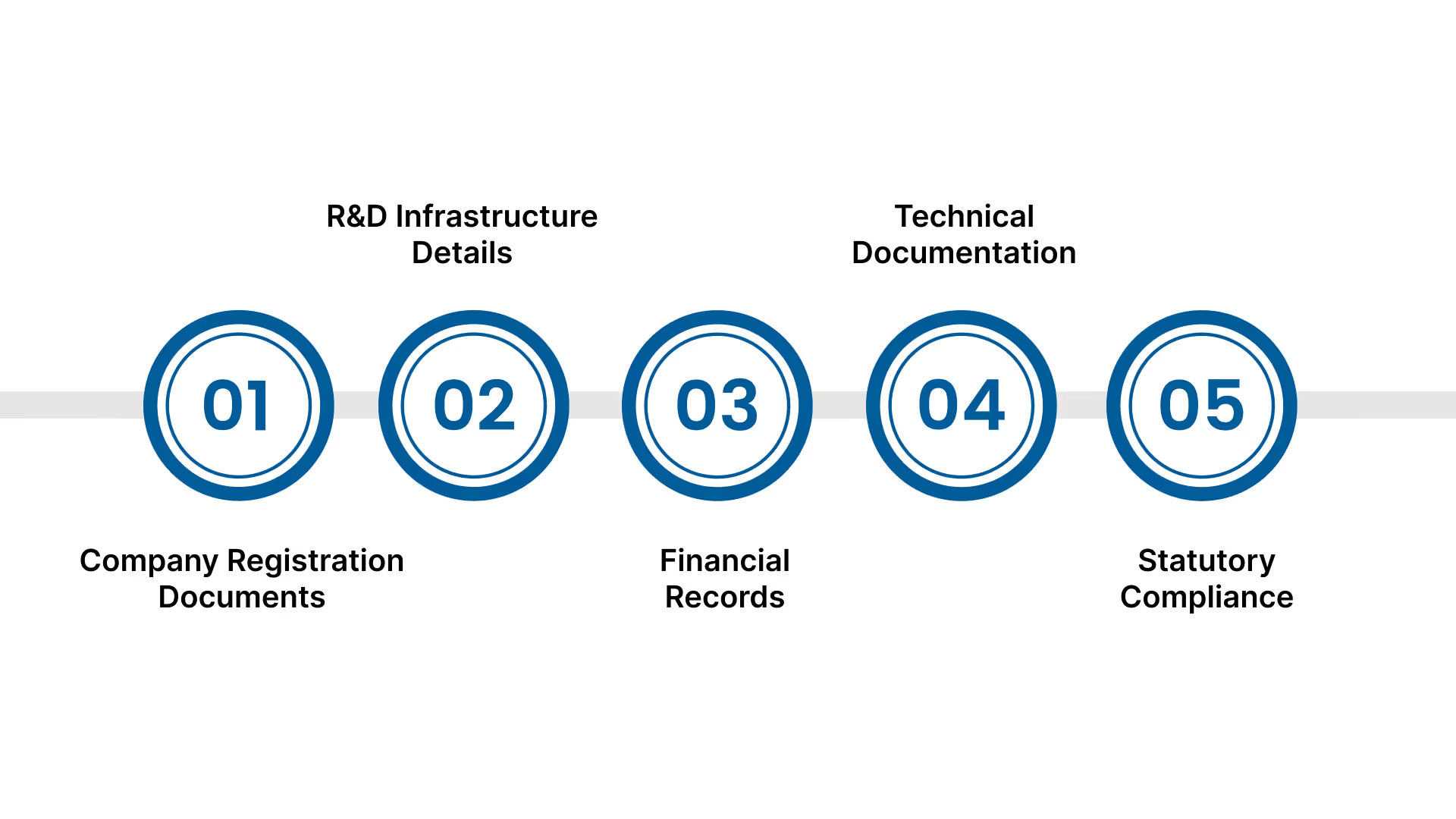

Documentation Requirements

The key documents that need to be maintained include the following.

Company Registration Documents: Copy of Memorandum and Articles of Association proving legal existence and corporate structure.

R&D Infrastructure Details: Complete description of R&D unit activities, scope, objectives, methods, and outcomes of research projects.

Financial Records: Three years of annual reports, financial statements, and a detailed breakdown of R&D expenses, including materials, salaries, and equipment costs.

Technical Documentation: R&D unit designs showing physical layout, infrastructure details, installation dates, equipment values, and personnel qualifications.

Statutory Compliance: Valid permits and licenses from statutory authorities for operations and R&D center establishment at a specific location.

Initial approval is just the start; ongoing compliance provides benefits for businesses to continue without interruption.

Annual Compliance and Reporting

Here are the main requirements for annual compliance and documentation.

Form 3CL Submission: Submit annual return in Form 3CL by October 31st each year, detailing R&D expenditures and activities for the approved period.

Separate Account Maintenance: Maintain separate accounts for each R&D center with an annual audit by statutory auditors and furnish a copy to DSIR.

Form 3CLA Certification: ANew form requiring certification by an accountant that accounts are maintained satisfactorily and expenditure aligns with DSIR guidelines.

Internal Audit Requirements: Conduct an internal audit of R&D expenses if required, providing compliance with approved expenditure categories.

Tax incentives aren’t limited to income tax; GST and customs benefits can reduce upfront spending for R&D projects.

GST and Customs Benefits

The following benefits help lower the upfront costs related to R&D activities.

Benefit

Description

Reduced GST Rate

Maximum 5% IGST on eligible R&D purchases instead of the standard 18%, reducing R&D project costs.

Customs Duty Exemption

Zero customs duty on imports of R&D equipment, spares, accessories, and consumables under specific notifications.

Import Procedures

Apply to Customs with a DSIR certificate confirming exclusive R&D use, equipment details, and all supporting documents.

Pharmaceutical Benefits

Duty-free import allowed for pharmaceutical reference standards and analytical equipment for biotechnology and pharma R&D.

Long-term benefits depend on strict record keeping and audits, as these form the backbone of compliance for businesses.

Use VJM Global’s deep expertise in GST impact analysis and customized solutions to get reduced GST rates, duty exemptions, and compliant import benefits that significantly lower overall R&D project costs. Get in touch with us!

Compliance and Record Keeping

The following facts cover essential compliance practices.

Audit Requirements: Mandatory audit and reporting for claiming deductions with proper maintenance of research cost records, including materials, salaries, and bills.

Documentation Standards: Keep detailed records of all R&D expenses with supporting invoices, technical reports, project information, and relevant papers.

Assessment Timeline: Income Tax Department typically conducts R&D assessment two years after filing, when scrutiny occurs, requiring Form 3CM presentation.

CBDT Dispute Resolution: In case of disputes with the assessing officer, matters are referred to the CBDT through the prescribed authority (DGIT Exemptions) in concurrence with the Secretary DSIR.

With VJM Global, entry to India is made simple; company registration, compliance, and ongoing support in one place.

Industry-Specific Opportunities for Tax Incentives for R&D in India

Tax Incentive for R&D in India varies notably across industries, reflecting the distinct demands and priorities of each sector. Recognizing how these incentives align with specific industry needs can clarify where the most relevant benefits lie.

The following breakdown highlights key opportunities available to different fields.

Industry

Tax Incentive Summary

Pharmaceuticals

150% weighted deduction under Section 35(2AB); duty-free import for research equipment; 10% patent box tax rate.

IT & Software

150% deduction on in-house R&D; tax exemptions in Special Economic Zones (SEZs) for export profits; 10% concessional tax on patent income.

Electronics

150% weighted deduction; $3 billion government incentives for indigenous technology; duty exemptions for design and prototyping.

Automotive

150% R&D deduction; 40% accelerated depreciation on indigenous technology machinery; EV R&D incentives.

Aerospace & Defense

Up to 45% capital subsidy; excise and utility duty exemptions; DRDO funding for MSMEs; patent-based benefits.

Renewable Energy

100% deduction on profits from solar/wind projects; accelerated depreciation on machinery; financial support programs.

Chemicals & Materials

150% deduction on R&D expenditure; import substitution incentives; tax benefits for environmental R&D compliance.

Agriculture & Food

Weighted deductions on crop breeding and processing R&D; concessional tax on patent income; export promotion incentives.

How VJM Global Can Support US Businesses Claim Tax Incentives for R&D in India

VJM Global offers specialized support to US businesses through India’s tax incentive framework for R&D. Our team simplifies complex regulatory and compliance needs, allowing firms to benefit from fiscal advantages fully.

In-depth Regulatory Knowledge: Comprehensive understanding of India’s tax laws, customs exemptions, and DSIR recognition procedures to optimize R&D claims.

End-to-End Compliance Support: Handling documentation, filing, and reporting requirements, minimizing operational burden on your teams.

Skilled Multidisciplinary Team: Experienced professionals across Delhi NCR and Mumbai provide timely, accurate, and client-focused service delivery.

Technology-Driven Processes: Using modern tools for efficiency and transparent communication throughout the engagement.

Position your R&D operations for success with VJM Global’s dedicated expertise. Contact us to start maximizing your tax incentives for R&D in India today.

Final Thoughts

The tax incentives for R&D in India framework offer US companies a strategic pathway to build innovation hubs in a cost-efficient setting. With 100% tax deductions, customs exemptions, and reduced corporate rates, the framework cultivates a fertile environment for research activities. Securing DSIR recognition for R&D operations opens further financial advantages while tapping into India’s skilled talent pool.

VJM Global specializes in guiding businesses through these regulatory nuances, helping maximize tax benefits and operational efficiency. Ready to use Tax incentives for R&D in India for your innovation goals?

Get in touch with us to start transforming your R&D investments into tangible growth.

FAQs

1. Can a US company claim tax incentives for R&D in India without establishing a permanent presence in India?

No, the company must establish a permanent establishment or subsidiary in India and obtain DSIR recognition for its in-house R&D unit to claim benefits under Section 35.

2. What is the minimum investment required to qualify for DSIR recognition?

There is no specific minimum investment threshold, but companies must demonstrate a dedicated R&D facility with qualified personnel and equipment suitable for their research objectives.

3. How does the 100% deduction compare to the previous super deduction scheme?

The current 100% deduction replaced the earlier 150-200% weighted deduction scheme that was phased out in 2020, making the benefits less generous but still substantial for R&D investors.

4. Are software development activities eligible for R&D tax benefits?

Yes, software development activities qualify if they involve the creation of new algorithms, technologies, or innovative solutions, and must be approved by DSIR as legitimate R&D activities.

5. Can R&D expenses be carried forward if they exceed current year profits?

Yes, unabsorbed R&D expenditure can be carried forward for up to eight years and utilized against future profits, providing flexibility for companies with initial losses.

VJM Global

Explore expert insights, tips, and updates from VJM Global

%20(3).avif)

.avif)