%20(2).avif)

Why is a GAAP cash flow statement considered one of the most critical reports in financial analysis? A GAAP cash flow statement shows how money moves in and out of a business, providing clarity on financial health, compliance, and investor trust. For US companies and CPA firms, it is a standard reporting requirement, with the SEC mandating comparative cash flow information for at least two years under Regulation S-X Rule 3-02.

Have you ever found preparing or reviewing these statements overwhelming, especially during peak reporting or audit periods? This blog will walk you through the structure, preparation methods, reconciliation steps, analysis techniques, and common challenges of a GAAP cash flow statement. VJM Global can support US businesses and CPA firms with accurate, GAAP-compliant cash flow reporting tailored to your needs.

When you prepare financial reports, a cash flow statement is required under GAAP if your company falls under US reporting rules. The SEC enforces this to maintain transparency and comparability, placing the cash flow statement alongside the balance sheet and income statement in importance.

This statement shows cash inflows and outflows during a period, giving clarity on liquidity and the ability to meet obligations. Profitability alone is not enough, since a company may report net income but still face liquidity problems if operating cash flows are weak.

To comply with GAAP, you must organize the statement into three activity categories. Each category highlights a different part of the financial picture:

To better understand the role of the cash flow statement, it helps to compare it directly with the income statement and balance sheet. The table below shows how each report contributes to a complete financial overview:

By presenting all three reports together, you give stakeholders a full perspective of performance, stability, and cash availability.

Also Read: Understanding the Differences Between GAAP and GAAS

Understanding the structure sets the stage for breaking down the key components of a GAAP cash flow statement.

A GAAP cash flow statement is divided into three sections that separate the sources and uses of cash. Each section shows a different aspect of how money moves through your business, which allows stakeholders to evaluate financial stability and decision-making more accurately.

The operating activities section shows how much cash your core business generates or consumes. It focuses on everyday transactions that determine whether your operations can sustain themselves without relying on external funding.

Examples of cash inflows and outflows you would include are:

Because GAAP requires accuracy, you must also adjust net income for non-cash items. Common adjustments include depreciation, amortization, and deferred tax expenses. These items reduce or increase reported income but do not change actual cash flow.

This section is closely reviewed by auditors and investors. A consistent positive cash flow from operations demonstrates that your business can cover expenses, repay debt, and reinvest without relying on external financing.

Investing activities focus on how you allocate resources into long-term assets or recover funds from them. These transactions show whether you are expanding operations or liquidating assets for cash.

Cash flows in this section typically include:

The direction of these cash flows carries important meaning:

For example, if you purchase manufacturing equipment for $200,000, the outflow shows your commitment to expansion. If you sell unused office space, the inflow signals a shift to free up working capital.

Also Read: Understanding US GAAP Consolidation Accounting Rules

Once you know the components, the next step is deciding which preparation method works best under GAAP.

.avif)

When preparing a GAAP cash flow statement, you can select either the direct or indirect method. Both are compliant under GAAP, but they differ in how you present operating activities. Understanding these methods helps you decide which approach fits your reporting needs and the expectations of your stakeholders.

The direct method presents cash inflows and outflows as they occur. You show actual receipts from customers and payments to suppliers, employees, and other operating parties. This approach gives a clear view of how money moves through your operations.

Typical items listed under the direct method include:

Although this method offers transparency, it requires detailed records of all cash transactions, making preparation labor-intensive. For this reason, most US companies avoid it even though GAAP permits its use.

The indirect method starts with net income from the income statement and adjusts it for items that affect reported earnings but not actual cash. This method is widely adopted because it connects net income to cash flow from operating activities, a link that auditors and investors often find useful.

Key adjustments you make under the indirect method include:

The indirect method is preferred by most US firms and CPA firms because it aligns with data already available from accrual-based accounting. It reduces preparation time while still complying with GAAP requirements.

To make the difference clearer, here is a comparison of the two methods:

With the methods defined, you can move into the step-by-step process of preparing the full statement.

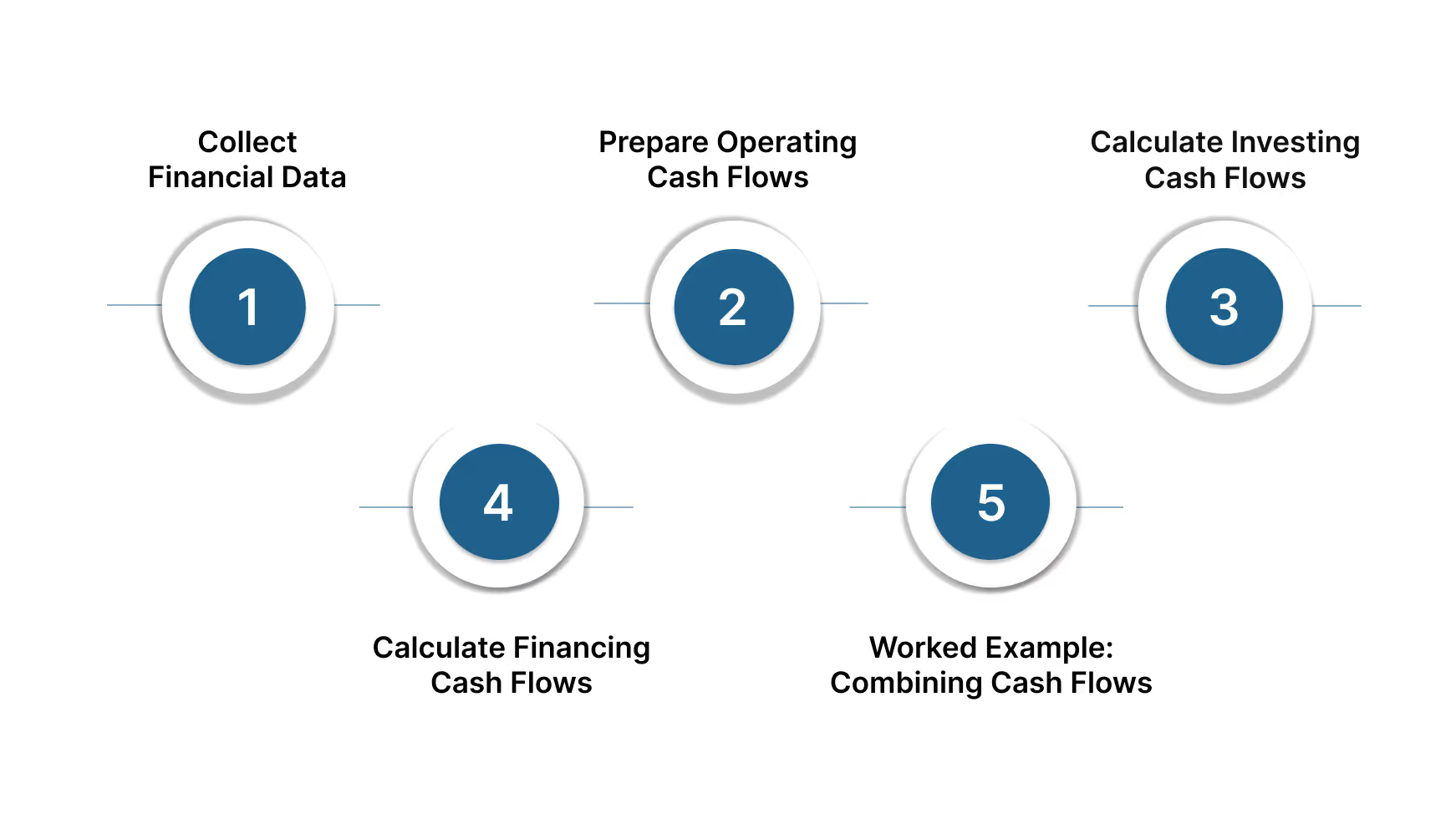

When you prepare a GAAP cash flow statement, breaking the process into steps helps you stay accurate and consistent. Each stage connects data from your financial reports to the three activity categories defined by GAAP. By following this method, you make sure your statement reflects actual cash flow rather than just accounting entries.

You begin by gathering information from your company’s financial statements. The income statement gives you net income, while the balance sheet helps you track changes in assets, liabilities, and equity between periods. Notes to the financial statements provide context, such as details on non-cash transactions or asset purchases.

For example:

This step focuses on cash generated or used by daily business activities. You can use either the direct or indirect method, both permitted under GAAP.

Example calculation (indirect):

Investing cash flows relate to long-term asset transactions. You record cash spent on buying property, plant, or equipment, as well as proceeds from selling assets or investment securities.

Examples include:

GAAP requires that you keep these separate from financing activities so readers can clearly see whether you are expanding, contracting, or liquidating investments.

Financing cash flows show how you raise and repay capital. You report activities like borrowing, repaying debt, issuing shares, and distributing dividends.

Examples include:

GAAP also requires disclosure of significant non-cash financing activities, such as converting debt into equity, even though they do not affect immediate cash balances.

Bringing the sections together shows the full effect of cash movement. Suppose your company reports the following in one year:

Your GAAP cash flow statement would look like this:

This total should match the change in your cash balance shown on the balance sheet, which serves as a validation check.

Finding it hard to keep GAAP cash flow statements accurate during busy cycles?

VJM Global can:

After preparing the statement, reconciliation and validation confirm the accuracy of your reported cash flows.

Preparing a GAAP cash flow statement is not complete until you reconcile and validate the figures. These checks confirm that the numbers align with your income statement and balance sheet, reducing the chance of audit issues or regulatory penalties. By focusing on reconciliation and validation, you give investors, auditors, and regulators confidence that your reporting is reliable.

You start by reconciling net income with net cash provided by operating activities. This step explains the differences between accrual-based earnings and actual cash. Adjustments are made for non-cash expenses and changes in working capital so the figures reflect real liquidity.

For example:

This reconciliation shows stakeholders how you move from reported profit to the cash actually generated by your business operations.

The ending cash reported in your cash flow statement must equal the cash balance on your balance sheet. This step acts as a built-in control check. If the numbers do not match, you know there is an error in classification, omission, or calculation.

Example validation:

When these figures align, you can confirm that the cash flow statement is consistent with the company’s overall financial position.

Accurate classification ensures compliance with GAAP and avoids red flags during audits. Misclassifying a loan repayment as an operating expense, or treating asset purchases as financing activities, can distort financial ratios and trigger regulatory concerns.

Key classification checks include:

By following GAAP standards for classification, you maintain consistency, improve comparability, and reduce the likelihood of costly restatements.

Also Read: Understanding US GAAP Revenue Recognition Standards

Once validated, the statement can be analyzed to reveal financial insights that support better decisions.

Analyzing a GAAP cash flow statement helps you interpret more than just numbers. By breaking down operating, investing, and financing activities, you can see whether cash is being generated sustainably, whether resources are being reinvested wisely, and how capital is being managed. Each section highlights different signals about stability, growth, and risk.

Operating cash flows show how much cash your business generates from core activities. Consistent positive cash flows in this section indicate that your company can cover expenses, repay debt, and invest without relying on external financing.

Key points to observe include:

Investment cash flows reveal how you are using funds for long-term assets or recovering value from them. These flows help you and your stakeholders understand if your business is positioned for expansion or contraction.

Points to consider:

By comparing these flows over multiple periods, you can distinguish between one-time asset sales and sustained growth investment.

Financing cash flows reflect how you manage your capital structure through debt and equity. They show whether you are raising funds, repaying obligations, or returning value to shareholders.

Important signals include:

While analysis brings value, you must also be aware of common challenges and how to solve them. Many US companies streamline this process by outsourcing accounting and tax services to India, gaining both cost savings and expert compliance support.

While analysis brings value, you must also be aware of common challenges and how to solve them.

Even if you follow GAAP rules closely, preparing a cash flow statement can bring several difficulties. These challenges usually come from handling non-cash adjustments, ensuring proper classification, and managing complex transactions. Addressing them correctly helps you maintain accuracy, avoid compliance risks, and present reliable information to auditors and investors.

Non-cash items affect net income but not cash, which means you must adjust them when preparing operating cash flows. If you do not account for them properly, your statement may overstate or understate liquidity.

Examples of common adjustments include:

Practical Solution: Create a checklist of recurring non-cash items from your financial notes. Review this list each reporting period to ensure all items are captured before finalizing the cash flow statement.

One of the most frequent errors is placing transactions in the wrong section. This misclassification can distort ratios and create confusion for stakeholders who rely on accurate breakdowns.

Examples of common misplacements include:

Practical Solution: Use a classification guide that aligns with GAAP standards. Train your accounting team with examples and review classifications at each reporting cycle to ensure accuracy.

Complex transactions often require special treatment under GAAP. If you overlook them or treat them incorrectly, your statement may conflict with your consolidated financials.

Examples to watch for include:

Practical Solution: Review guidance from the Financial Accounting Standards Board (FASB) on complex transactions and apply standardized templates for reporting. When needed, consult with external auditors or accounting advisors to confirm compliance.

Addressing these challenges naturally leads to exploring how VJM Global supports accurate GAAP cash flow preparation. Many US firms now outsource tax and accounting services to India for cost efficiency, accuracy, and faster turnaround, making it a strategic choice alongside in-house compliance efforts.

Addressing these challenges naturally leads to exploring how VJM Global supports accurate GAAP cash flow preparation.

Outsourcing in 2025 is about more than cost savings. It is about building a finance function that is reliable, scalable, and compliant. VJM Global works with US CPA firms and mid-sized businesses to handle operational challenges, ensure GAAP compliance, and strengthen financial control. By choosing to outsource from the US to India, you gain the advantage of dual expertise in both US and Indian frameworks while significantly reducing overhead costs.

By combining US GAAP expertise, cost efficiency, and scalable offshore teams, VJM Global strengthens the quality and reliability of your financial reporting process.

A GAAP cash flow statement gives you more than just numbers. It connects structure, preparation methods, reconciliation, analysis, and classification into a report that reflects true liquidity. Throughout this blog, you have seen how operating, investing, and financing activities shape the statement, how reconciliation validates accuracy, and how analysis uncovers financial stability or risk. You also learned about common challenges such as non-cash adjustments and classification errors, along with practical solutions to address them.

Compliance with GAAP is not optional. It is the foundation of credibility with auditors, investors, and regulators, and it directly affects decision-making. Are your GAAP cash flow statements accurate enough to support the decisions that shape your business’s future?

Feeling stretched during audit season or monthly reporting? VJM Global gives you the offshore support you need to manage reporting peaks while keeping compliance intact. Schedule a consultation today!

A: A company may report net income but negative operating cash flows. Outsourcing from the US to India can help identify these issues early with expert support.

A: Many fail to reconcile ending cash with the balance sheet. Outsourcing tax services from the US to India ensures accurate reconciliation and compliance.

A: Outsourcing from the US to India combines GAAP expertise with cost-effective execution, improving accuracy, saving time, and maintaining compliance for U.S. businesses.

A: Lenders examine cash flow to gauge repayment capacity. U.S. companies outsourcing to India gain accurate, timely statements that support financing.

A: Changes in receivables, payables, and inventory impact cash. Outsourcing to India ensures these adjustments are tracked correctly and efficiently.

A: Outsourcing to India combines GAAP expertise with cost-effective execution, improving accuracy, saving time, and maintaining compliance for U.S. businesses.