Accounts payable are the core of a company’s financial obligations. When businesses acquire goods or services on credit, they create accounts payable, an outstanding liability that reflects what they owe to their suppliers. These debts don’t stretch indefinitely. Repayment terms usually follow a short horizon: 30, 45, 60, or 90 days, depending on the agreement.

Accounts payable, or AP, are far more than a line item under current liabilities. They impact every part of an operation, from vendor trust and purchasing utilization to cash reserves and operational continuity. To manage AP effectively, one must manage the timing of cash outflows without compromising relationships or liquidity.

This article breaks down everything you need to know about AP. We’ll explore the definition and mechanics of accounts payable, examine how AP appears in accounting records, and discuss why managing AP strategically improves both financial reporting and supplier relationships.

What Are Accounts Payable (AP)?

Accounts payable refers to the outstanding balances a company must pay to suppliers for goods or services purchased on credit. These transactions do not involve immediate cash outflows, making AP a key tool in short-term financing.

On the balance sheet, accounts payable show up as a current liability, not as an asset. Unlike long-term debts, AP obligations mature within a few months, aligning with standard business cycles. Payment terms vary: Net 30, 1/10 Net 30, or similar structures dominate. These terms define when payment is due and whether early settlement discounts apply.

A rising AP balance may signal delayed payments or increased purchasing. A declining balance might suggest stronger cash positions or better settlement rates.

So, how do accounts payable work? Let us understand in detail.

How Accounts Payable Works?

Accounts payable help companies conserve cash by deferring outflows. Instead of paying upfront, businesses use AP to stretch liquidity while securing inventory or services. This mechanism acts as a form of interest-free credit, allowing the firm to hold onto its cash longer and use it for more immediate operational needs such as payroll, production, or marketing.

The key is timing. Businesses that align payment schedules with their revenue cycles unlock value from their payables. For example, a retailer receiving goods on Net 60 terms can sell inventory and collect revenue before the supplier’s invoice comes due. This sequencing strengthens working capital and shields the company from unnecessary borrowing.

Paying AP on time is more than a compliance task; it’s strategic. Vendors extend better terms to buyers with prompt payment records. Missed deadlines, however, can damage reputations and raise costs. Suppliers may impose late fees, demand advance payments, or revoke preferential treatment. In contrast, consistent and timely payments often lead to volume-based discounts, improved availability, and a competitive edge.

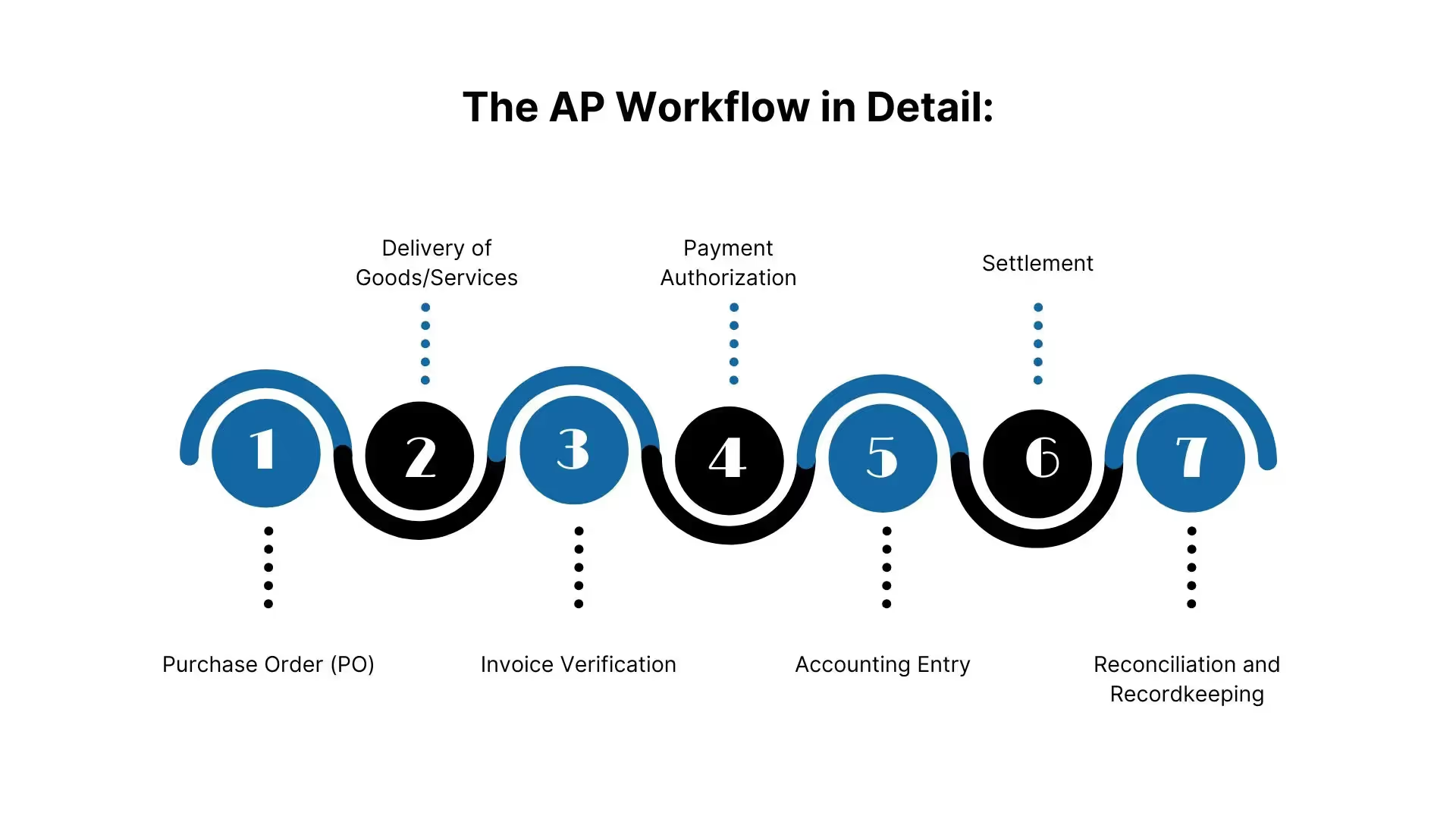

The AP Workflow in Detail:

Purchase Order (PO): The process begins with a formal PO outlining the specifics of the purchase. This document acts as both a record and a contract. It confirms product type, quantity, price, delivery terms, and payment schedule. POs ensure that procurement follows budget controls and approval hierarchies.

Delivery of Goods/Services: The vendor fulfills the PO. Goods arrive at the company’s receiving dock, or services get delivered as agreed. Upon delivery, staff log receipts, inspect items for quality, and match them to the PO.

Invoice Verification: The vendor submits an invoice, and the buyer performs a three-way match between the invoice, the PO, and the goods receipt. Finance staff confirm pricing accuracy, correct quantities, and fulfillment of service terms. Discrepancies get flagged for investigation before payment proceeds.

Payment Authorization: Verified invoices move into approval. Depending on internal policy, one or more approvers must sign off, often department managers or accounts payable personnel. This step enforces accountability and prevents unauthorized payments.

Accounting Entry: Once authorized, the system records the transaction in the general ledger. The payable account increases, and the corresponding expense or asset account gets debited. This accounting step ensures that financial records remain balanced.

Settlement: Payments are released based on the agreed-upon terms. Finance teams schedule disbursements to align with due dates. Most companies prefer electronic funds transfer (EFT) or automated clearing house (ACH) transactions, but some suppliers may still accept checks. Early payments might capture discounts; late payments could trigger penalties.

Reconciliation and Recordkeeping: After payment, the transaction is closed in the AP ledger. Documentation—including the PO, invoice, and proof of payment—is archived for audits and financial reporting. Periodic reconciliations ensure that reported AP balances match actual obligations.

Most AP agreements adhere to standard commercial terms written clearly to avoid disputes. The entire process benefits from automation, with enterprise systems handling invoice intake, flagging mismatches, and scheduling payments. This digital infrastructure ensures consistency, improves audit trails, and strengthens internal accountability.

Now, let us discuss how to record accounts payable correctly, in detail below.

Recording Accounts Payable

Accounts payable (AP) is a key component of accounting that follows the double-entry bookkeeping system. This system ensures that every transaction is recorded in two places: once as a debit and once as a credit.

This method maintains the balance of the accounting equation, which is Assets = Liabilities + Equity. In the case of accounts payable, when a company receives goods or services on credit, it records both an increase in assets (such as inventory or services received) and a corresponding liability in its accounts payable.

Let’s break this down with an example:

Imagine a business purchases $10,000 worth of materials from a supplier on credit. The accounting entries would look like this:

Debit Inventory (Asset Account): The company receives $10,000 worth of materials, which increases its inventory. This is recorded as a debit in the inventory account.

Credit Accounts Payable (Liability Account): Because the purchase was made on credit, the company now owes the supplier $10,000. This is recorded as a credit in the accounts payable account, which represents a liability to the business.

Thus, the journal entry for this transaction would be:

Date

Account

Debit

Credit

YYYY-MM-DD

Inventory

$10,000

YYYY-MM-DD

Accounts Payable

$10,000

This entry reflects the increase in inventory (asset) and the obligation to pay the supplier (liability).

The Importance of Accurate Accounts Payable Recording

An accurate recording of accounts payable is essential for maintaining the integrity of a company’s financial statements. The impact of this is far-reaching:

Financial Statement Accuracy: Properly recorded AP ensures the balance sheet reflects the true financial position, preventing misrepresentation of liabilities and assets. This helps stakeholders, like investors and creditors, make informed decisions.

Cash Flow Analysis: AP impacts cash flow by showing what the company owes. Accurate records help forecast when payments are due, ensuring sufficient liquidity and smooth operations.

Regulatory Compliance: Many regulations require precise AP reporting. Errors can lead to penalties, fines, or audits, putting the company at risk of non-compliance.

Audit Trails: Accurate AP records provide a clear audit trail, ensuring transparency and legitimacy for external auditors when verifying liabilities and vendor payments.

Vendor Relationships: Timely and accurate AP helps maintain good relationships with suppliers, which can lead to better payment terms, discounts, or preferential treatment.

Financial Planning and Budgeting: Accurate AP allows businesses to better plan for upcoming payments, prioritize cash outflows, and optimize working capital management.

Tax Implications: Correct AP ensures businesses don't miss out on tax deductions, reducing taxable income and the risk of issues during tax audits.

Internal Controls and Fraud Prevention: Proper AP records strengthen internal controls, making it easier to spot discrepancies or fraud and ensuring that payments are authorized.

Investment Decisions and Credit Ratings: Investors and financial institutions rely on accurate AP records to assess a company's creditworthiness. Reliable AP reporting can improve a company’s credit rating and investment attractiveness.

Timely Decision-Making and Business Strategy: Accurate AP helps management make informed decisions, ensuring the company is prepared to meet obligations and execute business strategies efficiently.

Common Mistakes and Their Consequences

When accounts payable are not recorded properly, the consequences can be serious:

Discrepancies with Vendor Statements: Inaccurate AP entries can lead to mismatches between company records and vendor statements, which can cause confusion and disputes with suppliers.

Consequence: Vendor disputes can lead to delayed shipments, loss of early payment discounts, and strained supplier relationships.

Missed Payment Deadlines: If accounts payable are not recorded correctly, the company might miss payment deadlines, leading to penalties or late fees.

Consequence: Missed payments can damage the company’s credit rating, increase borrowing costs, and harm relationships with suppliers.

Incorrect Tax Reporting: Mistakes in recording AP may result in incorrect tax liabilities, either overreporting or underreporting taxes owed.

Consequence: This can lead to fines, interest charges, and potential audits from tax authorities.

Inaccurate Financial Ratios: Errors in AP can distort financial ratios like the current ratio and debt-to-equity ratio, which are essential for assessing a company’s financial health.

Consequence: Misleading financial ratios may lead to poor investment decisions, misinformed lending, and incorrect financial assessments.

Inability to Manage Working Capital: Inaccurate AP recordings can distort working capital, making it difficult to track liquidity and plan for future expenses accurately.

Consequence: This can result in cash flow problems and leave the company unprepared for upcoming payments.

Internal Control Weaknesses: Incorrect AP entries can indicate weaknesses in the company’s internal controls, such as poor oversight or a lack of proper reconciliation.

Consequence: Weak internal controls increase the risk of errors or fraud going unnoticed, leading to financial loss or reputational damage.

Impact on Budgeting and Forecasting: If AP is not recorded accurately, it can throw off budgeting and forecasting efforts, leading to misallocated resources or unmet financial obligations.

Consequence: This can result in cash shortages, poor financial planning, and an inability to meet future payment obligations.

Distorted Profitability Analysis: Inaccurate AP can affect expense recognition, which in turn distorts profitability analysis and net income calculations.

Consequence: Misstated profitability can lead to poor business decisions and a distorted view of financial performance for investors.

Now, let us discuss how to manage accounts payable correctly in detail below.

Managing Accounts Payable

Efficient Accounts Payable (AP) management plays a crucial role in strengthening an organization's overall financial health. By ensuring that payments are made on time and accurately tracked, businesses can maintain smooth cash flow operations and build stronger vendor relationships.

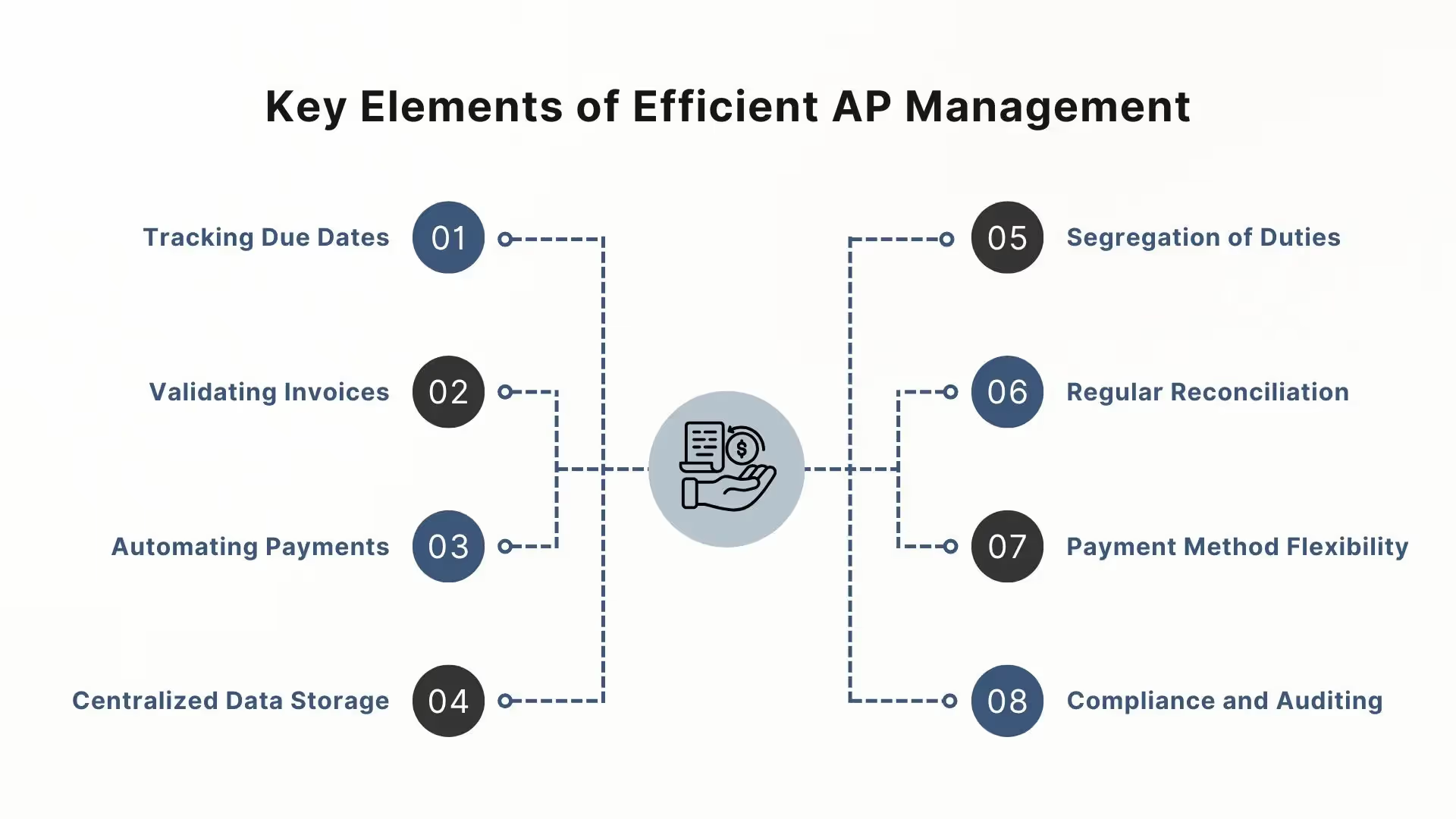

Key Elements of Efficient AP Management:

By implementing effective systems and practices, organizations can optimize cash flow, improve vendor relationships, and minimize financial risks.

Tracking Due Dates: AP systems track payment deadlines to avoid late fees and maintain smooth operations.

Validating Invoices: Invoices are verified for accuracy to prevent overpayments, duplicates, and errors.

Centralized Data Storage: All payment records and invoices are stored in one place for easy access and faster decision-making.

Segregation of Duties: Splitting tasks like approvals and payments helps prevent fraud and boosts accountability.

Regular Reconciliation: Frequent matching of AP records with statements ensures accurate reporting and detects issues early.

Payment Method Flexibility: Offering various payment options helps manage cash flow efficiently and reduces processing friction.

Compliance and Auditing: Following regulations and conducting audits helps identify risks and ensures legal and policy compliance.

VJM Global supports AP payment management with comprehensive audit services, identifying discrepancies and strengthening financial controls. Their expertise in GST, direct taxation, and international compliance ensures systems are accurate and aligned with global standards. With a focus on internal audits, they enhance efficiency, safeguard against errors, and ensure compliance, providing seamless AP operations for businesses.

Benefits of Effective AP Management:

Effective AP management offers a wide range of benefits that can significantly improve a company's financial stability, operational efficiency, and vendor relationships. By optimizing payment processes and leveraging best practices, organizations can ensure smoother cash flow, reduced risks, and greater control over their financial operations.

Avoiding Late Fees and Penalties: Timely payments help avoid late fees and protect the company’s financial reputation. Regular tracking and automation ensure no invoice is missed.

Prevention of Duplicate Payments: AP systems flag duplicate invoices, preventing overpayments and ensuring spending accuracy.

Fraud Prevention: Automation and built-in controls reduce the risk of fraud by verifying vendors and securing payment processes.

Improved Vendor Relationships: Consistent, on-time payments build trust with vendors, often leading to better terms, discounts, and priority service.

Enhanced Cash Flow Management: Efficient AP management offers clear visibility into obligations, helping forecast cash flow and avoid liquidity issues.

Better Credit Terms and Negotiation Power: A strong payment history boosts negotiation leverage, allowing access to extended terms and better credit limits.

Improved Financial Reporting and Analysis: Accurate AP data supports timely, reliable financial reports, enhancing analysis and strategic decision-making.

VJM Global helps by providing accounting outsourcing services that handle accounts payable efficiently, including prompt invoice processing, vendor reconciliations, and clear audit trails. Their expertise minimizes errors, boosts financial accuracy, and helps businesses generate reports that drive smarter, data-based decisions.

So, what exactly is the accounts payable aging report? Let us understand in detail below.

Accounts Payable Aging Report

The Accounts Payable Aging Report is a vital tool in managing AP effectively. It provides a breakdown of outstanding balances by due date, giving a clear picture of the company’s short-term financial obligations. By categorizing overdue payments, this report helps prioritize actions and ensures that cash flow is managed more efficiently.

Current: Amounts that are due for payment within the current period (typically within 30 days). This category represents obligations that are on track for timely payment and are often monitored to ensure that payments are made promptly.

30 Days Overdue: Balances that are overdue by 30 days, signaling the need for follow-up. At this point, the company may begin contacting vendors to discuss payment arrangements, which can help maintain good relationships and prevent further escalation.

60 Days Overdue: These are amounts that have been outstanding for 60 days and may require more urgent attention. Payments in this category often necessitate direct communication with vendors and may involve negotiating payment terms or identifying any issues causing delays in payment.

Beyond 60 Days: Payments that have been overdue for more than 60 days. These typically require escalation to higher management to prevent damaging vendor relationships and avoid potential disruptions in the supply chain. At this stage, more aggressive collection efforts or revised payment plans may be necessary.

Vendor Communication and Follow-Up: The Aging Report also helps prioritize vendor communication. Early-stage overdue payments (30 or 60 days) may prompt proactive discussions with suppliers to resolve payment issues before they escalate. Maintaining a record of these communications ensures better relationship management.

Now, let's discuss the basic differences between accounts receivable and accounts payable to better understand the terms.

Accounts Payable vs. Accounts Receivable

Many people often confuse accounts receivable (AR) and accounts payable (AP), but they serve different roles in a company's financial structure. Understanding the distinctions between the two is crucial for managing cash flow, maintaining operational efficiency, and ensuring overall financial health. Here's a breakdown of how they differ:

Accounts Payable (AP):

Definition: Accounts payable refers to the money a company owes to its suppliers, vendors, or creditors for goods or services that have been received but not yet paid for.

Impact on Cash Flow: AP reduces cash flow because the company must pay out money to settle these obligations. Timely payments are essential, as delaying can result in late fees or strained relationships with suppliers.

Balance Sheet Placement: AP is recorded as a liability on the company's balance sheet, indicating the debts the company needs to pay.

Management Strategy:

Payment Terms: AP management involves negotiating favorable payment terms with suppliers (e.g., "Net 30" or "Net 60") to control cash flow better.

Discounts: Companies may also take advantage of early payment discounts offered by suppliers to reduce overall costs.

Cash Flow Management: By carefully managing when and how AP is paid, companies can maintain liquidity without missing critical payments.

Supplier Relationships: Paying AP on time helps maintain strong vendor relationships, which can result in better terms or pricing in the future.

Strategic Importance:

Managing AP efficiently can help avoid liquidity problems, as businesses must ensure they can meet these obligations without depleting cash resources required for day-to-day operations.

Accounts Receivable (AR):

Definition: Accounts receivable represent the money owed to the company by customers who have purchased goods or services on credit but have not yet paid for them.

Impact on Cash Flow: AR increases cash flow when payments are collected, converting outstanding receivables into cash that can be used for operational needs or reinvestment.

Balance Sheet Placement: AR is recorded as an asset on the company's balance sheet, reflecting the expected future inflow of cash from customers.

Management Strategy:

Credit Risk Management: Before offering credit, businesses assess customers' creditworthiness to minimize the risk of bad debts. This includes using credit checks and third-party agencies to evaluate potential customers.

Timely Invoicing and Follow-Ups: Effective AR management involves issuing invoices promptly and following up with customers on overdue accounts.

Aging Reports: These reports categorize outstanding receivables based on the time overdue (e.g., 0-30 days, 31-60 days), allowing businesses to prioritize collections and address overdue debts before they become uncollectible.

Bad Debt Expense: Businesses must account for the potential of bad debts by creating an allowance for doubtful accounts, ensuring more accurate financial reporting.

Strategic Importance:

Efficient AR management ensures timely revenue collection, helping companies maintain a healthy cash flow and avoid financial strain. If left uncollected, AR can directly impact profitability and liquidity.

How VJM Global Helps You Master Accounts Payable Management?

Proper recording, diligent oversight, and timely settlement define the accounts payable process. Mastering AP isn’t optional; it’s vital for any business, large or small.

VJM Global provides expert guidance and strategic solutions to streamline your accounts payable processes. With services tailored to businesses of all sizes, they ensure that AP management aligns with best practices and regulatory requirements.

Expert AP Setup and Optimization: VJM’s professionals assist in designing an AP system that matches your business needs, ensuring timely and accurate payment cycles.

Invoicing and Payment Tracking: VJM helps automate invoicing, track outstanding bills, and manage payment schedules to avoid late fees and strengthen supplier relationships.

Tax Compliance and Regulatory Oversight: VJM’s expertise in GST and other financial regulations ensures your AP processes comply with local and international standards, reducing the risk of audits.

Cost Control and Cash Flow Management: By optimizing AP workflows, VJM Global helps businesses manage cash flow more effectively, minimizing unnecessary costs and enhancing liquidity.

With VJM Global’s support, you can transform your accounts payable from a routine task to a strategic advantage. Let them help you streamline payments and improve financial efficiency.