Businesses often extend credit to clients as part of their sales strategy. They allow payment delays, issue invoices periodically, and receive funds after delivery. This structure fosters customer trust, supports long-term relationships, and promotes revenue continuity.

But it also introduces risk. Delayed payments strain cash flow and challenge operations. To manage this balance between trust and liquidity, companies need a reliable financial gauge. The accounts receivable turnover ratio provides that lens.

It measures how frequently a company collects its outstanding credit sales within a set period. This reveals operational health, highlights the efficiency of collection efforts, and reflects the strength of credit policies.

This article explains the accounts receivable turnover ratio formula, walks through practical examples, and shows how to interpret and improve it. You'll also learn how to convert the ratio into collection days and understand its limitations.

So, let’s dive right into the article.

What Is the Accounts Receivable Turnover Ratio?

The Accounts Receivable Turnover Ratio is a key financial metric used to measure how efficiently a company collects its receivables or outstanding debts from customers. In simpler terms, it tells you how many times a company’s accounts receivable are collected and converted into cash during a specific period, usually a year.

This metric acts as both a performance mirror and a risk signal. It can spotlight a well-run accounts receivable process or expose systemic inefficiencies. A business that regularly cycles through its receivables maintains momentum. It keeps cash flowing, shortens outstanding balances, and lowers the risk of bad debt.

In essence, the receivables turnover ratio blends speed with discipline. Companies that post strong turnover ratios often exhibit clear credit controls, proactive collection efforts, and sharper liquidity strategies.

Why It Matters?

Here's why it’s important:

How Quickly Customers Are Paying Their Bills: This ratio reveals how fast the company collects payments. A higher ratio indicates quicker payments, which improves cash flow. A lower ratio suggests delayed payments, potentially leading to cash flow issues.

The Effectiveness of Credit and Collection Policies: A higher ratio shows that the company’s credit and collection policies are effective, ensuring timely payments. A lower ratio may signal the need to adjust credit terms or strengthen collection efforts.

The Company’s Cash Flow Health: The ratio directly impacts cash flow. A low turnover ratio can signal potential cash flow problems, while a high ratio indicates healthy cash inflows, supporting day-to-day operations and business growth.

Risk Management: A low ratio might indicate that customers are struggling to pay, increasing the risk of bad debts. Monitoring this ratio helps identify at-risk customers early, allowing the business to take proactive measures.

Business Decision Making: Fluctuating or decreasing turnover ratios could indicate inefficiencies in the sales or billing processes. A consistently high ratio can support business decisions like expanding credit sales or adjusting payment terms.

Benchmarking Against Industry Standards: The ratio can be used to compare performance against industry peers. A higher ratio suggests the company is managing receivables better than competitors, while a lower ratio may indicate areas for improvement.

So, how do we calculate the accounts receivable turnover ratio? Let us understand all about this in detail below.

Accounts Receivable Turnover Ratio Formula

This ratio measures how effectively a business collects its credit sales from customers. In simple terms, it shows how many times in a given period the company collects its average accounts receivable.

Formula:

The formula to calculate the ARTR is:

Accounts Receivable Turnover Ratio= Net Credit Sales / Average Accounts Receivable

Where:

Net Credit Sales refers to the sales made on credit during the period, minus returns and allowances.

Average Accounts Receivable is the average of the opening and closing balances of accounts receivable for the period.

Understanding this formula enables businesses to fine-tune credit policies, identify cash flow gaps, and benchmark performance against industry standards.

Now, let us understand how to calculate the average accounts receivable.

How to Calculate Average Accounts Receivable?

Average Accounts Receivable is the mean value of A/R over a specific period. It is usually used to assess your company’s collection trends and calculate key ratios, such as Accounts Receivable Turnover.

To calculate average accounts receivable, use the following formula:

Determine the Opening Accounts Receivable- The opening accounts receivable is the balance of accounts receivable at the start of the period. It is typically found on the business's balance sheet for the previous period.

Determine the Closing Accounts Receivable- The closing accounts receivable is the balance at the end of the period you are analyzing. It can be found in the balance sheet for the current period.

Let us understand this with the help of an example given below.

Let’s break down the calculation for a clearer understanding. Suppose a business generates $500,000 in net credit sales, and its opening accounts receivable balance is $60,000 while the closing balance is $40,000. In that case, we first calculate the average accounts receivable by adding the opening and closing balances and dividing by 2:

This means the business collects its receivables 10 times per year. A higher turnover ratio indicates better efficiency in collecting payments. Now, let us discuss what higher and lower turnover ratios mean and how they impact your business financially.

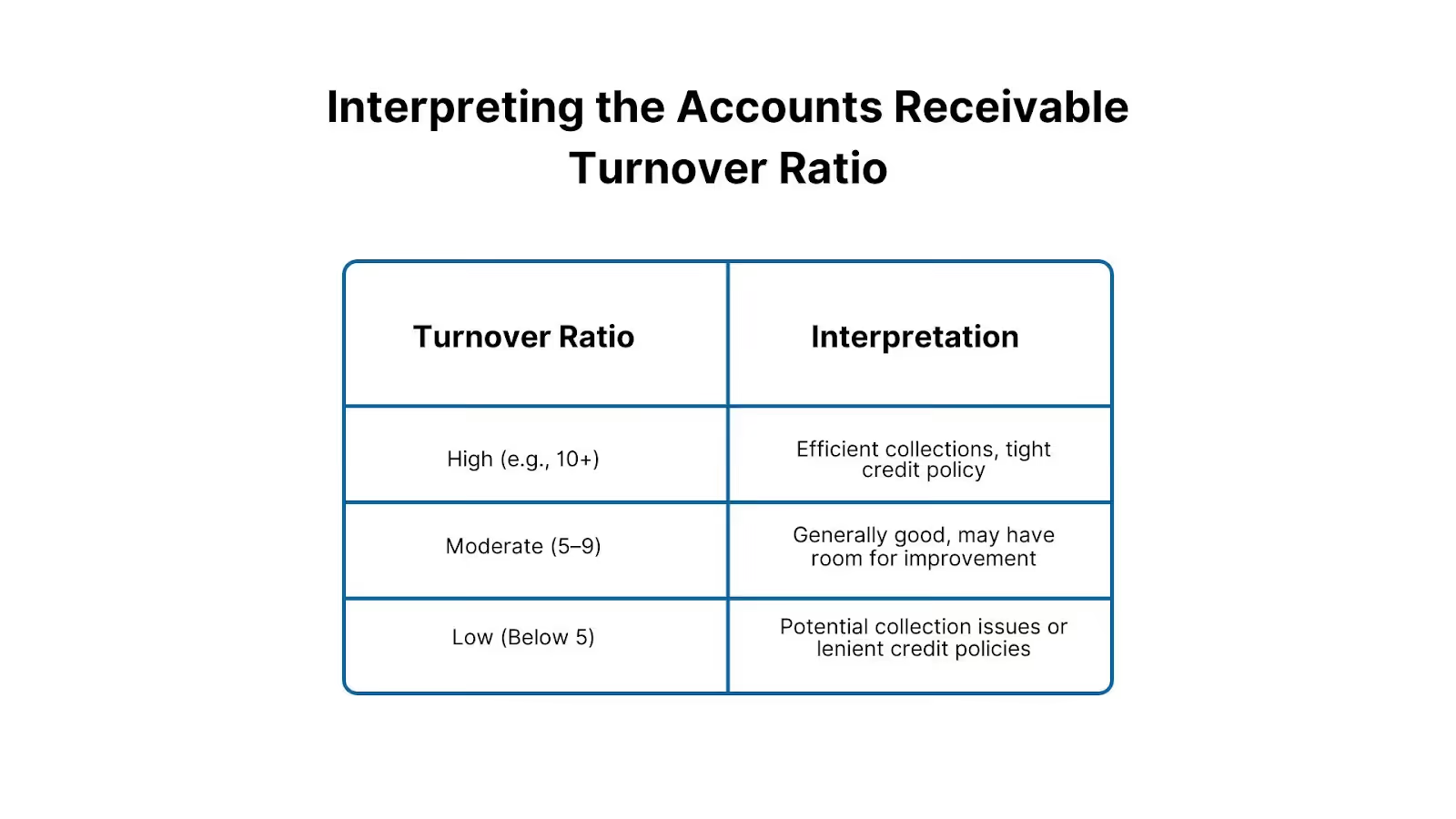

Interpreting the Accounts Receivable Turnover Ratio

Understanding how quickly your business collects money from customers is key to maintaining a healthy cash flow. This is where the Accounts Receivable Turnover Ratio plays an important role. It shows how efficiently a company turns its credit sales into cash. In other words, it tells you how fast your customers are paying what they owe.

Interpreting the Ratio:

Turnover Ratio

Interpretation

High (e.g., 10+)

Efficient collections, tight credit policy

Moderate (5–9)

Generally good, may have room for improvement

Low (Below 5)

Potential collection issues or lenient credit policies

High Ratio: A high ARTR is typically seen as a positive indicator, implying that the company is effectively collecting its debts and has a fast cash conversion cycle. It suggests that the company is managing its credit policies well and is likely to have better cash flow. A high turnover ratio indicates that the company is not offering overly generous credit terms to its customers.

Low Ratio: A low ARTR could signal that a company is facing difficulties in collecting its receivables, which may result in cash flow issues. It may also indicate that the company has extended too much credit to customers or that its collection efforts are not effective. In such cases, the company may want to review its credit policies or strengthen its collections process to improve liquidity.

Industry Benchmark: It's important to compare the ARTR (Accounts Receivable Turnover Ratio) with industry averages and competitors, as turnover ratios can vary widely across sectors. For instance, companies in industries with longer sales cycles, such as manufacturing, typically have a lower ARTR, often ranging between 5 to 10. In contrast, retail or consumer goods companies may have a higher ARTR, commonly falling between 10 to 15, due to faster sales and collection cycles.

Trends Over Time: Observing trends in the ARTR over multiple periods can provide valuable insights into the company's credit management practices. A declining ratio over time may highlight an emerging problem in collecting receivables, whereas an increasing ratio may indicate improvement in credit policy and collection efficiency.

Example:

Let’s say a company has net credit sales of $500,000 and an average accounts receivable of $100,000.

Receivables Turnover = $500,000 / $100,000 = 5

This means the company collects its receivables 5 times a year, or roughly every 72 days (365 ÷ 5). Now, let us understand how to calculate accounts receivable turnover in days. Here’s how to do it.

Accounts Receivable Turnover in Days

Accounts Receivable Turnover in Days is a key financial metric that tells you how long it takes a business, on average, to collect payments from its customers after a sale is made. A shorter collection period generally indicates stronger cash flow and better liquidity.

How is it calculated?

It’s derived using the formula:

Receivable Turnover in Days = 365 / Accounts Receivable Turnover Ratio

Where the Accounts Receivable Turnover Ratio is:

Net Credit Sales / Average Accounts Receivable

Example:

If your Accounts Receivable Turnover Ratio is 10, then:

365 / 10 = 36.5 days

So, on average, it takes the business 36.5 days to collect payment.

For most companies, reducing this number is key to maintaining a healthy financial position. A shorter collection cycle means faster access to working capital, fewer resources tied up in receivables, and less risk of non-payment. Conversely, if this figure stretches too long, it may signal inefficiencies in the invoicing process, weak credit terms, or slow-paying customers.

Monitoring this metric over time can help identify trends, support improvements in credit policy, and drive better forecasting for cash flow management. VJM Global aids this by offering tailored financial advisory services, including tax strategies, audits, and restructuring. Our expertise provides businesses with crucial insights to strengthen financial health, optimize forecasting, and improve decision-making, ensuring better long-term financial management.

Receivables Turnover Ratio vs. Asset Turnover Ratio

The Receivables Turnover Ratio measures how efficiently a company collects invoices, while the Asset Turnover Ratio evaluates how effectively all assets generate revenue. The former focuses on receivables, and the latter takes a broader view of asset efficiency, providing different insights into financial performance.

So, how can we improve the accounts receivable turnover ratio to ensure better financial discipline? Let's discuss this below.

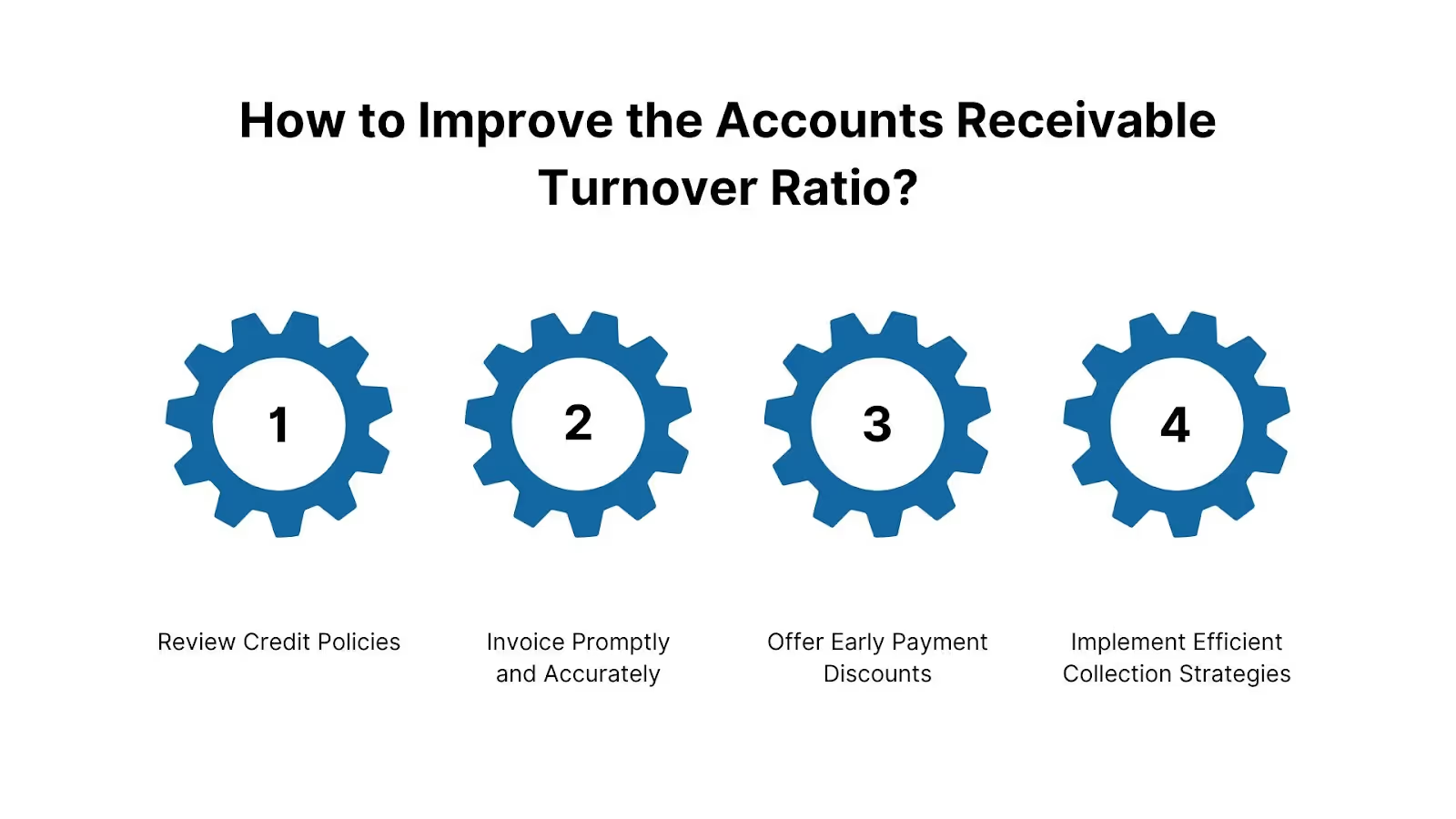

How to Improve the Accounts Receivable Turnover Ratio?

Improving your Accounts Receivable Turnover Ratio is essential for maintaining healthy cash flow and financial stability. Here are key strategies to help you collect receivables faster and more efficiently:

Review Credit Policies: Reevaluate your credit policies to ensure that credit is only extended to customers with a strong track record of timely payments. Consider conducting credit checks before approving terms, and establish clear guidelines for credit limits and repayment timelines. This minimizes the risk of delayed payments and bad debts.

Invoice Promptly and Accurately: Send invoices immediately after delivering a product or service, and double-check them for accuracy. Delays or errors in invoicing can create confusion, lead to disputes, and ultimately delay payments, so streamlining this process helps accelerate collections.

Offer Early Payment Discounts: Small discounts for early payments can encourage customers to pay their bills ahead of the due date. For instance, a 2% discount for payments made within 10 days encourages quicker cash inflow while still maintaining profitability.

Implement Efficient Collection Strategies: Set up a consistent follow-up process for overdue accounts, including reminder emails, phone calls, or even SMS alerts. If internal efforts are not effective, consider outsourcing collections to professionals who specialize in recovering outstanding receivables.

Use Technology to Streamline Payments: Integrate payment gateways and online invoicing tools into your accounting system to make it easier for customers to pay. Offering multiple digital payment options and automating reminders can significantly reduce payment delays and manual follow-up.

Customer Relationship Management (CRM): Maintain strong, transparent communication with clients about payment expectations. A good relationship makes it easier to resolve payment issues amicably and can increase customer accountability for paying on time.

Negotiate Better Payment Terms: If customers are consistently late, consider shortening payment cycles or offering installment plans. By aligning terms with your cash flow needs and customer payment behavior, you can better manage receivables and reduce payment delays.

Monitor Receivables Closely: Regularly review your accounts receivable aging reports to identify which accounts are overdue and need immediate attention. By prioritizing high-risk or large outstanding balances, you can act quickly to prevent larger financial issues.

Improve Your Credit Management: Periodically evaluate the creditworthiness of your clients and adjust their credit terms if needed. Monitoring payment trends and financial health ensures that you don’t overextend credit to risky customers, which helps maintain a higher turnover ratio.

Strengthen Internal Controls: Implement checks and balances by segregating duties among team members handling credit approvals, invoicing, and collections. Regular internal audits help identify inefficiencies or inconsistencies in the receivables process and allow for timely corrective action.

For U.S.-based businesses and CPA firms, managing receivables can become resource-intensive, especially with limited in-house staff or high operational costs. That’s where VJM Global steps in. Our team handles everything from timely invoicing and AR aging report reviews to payment tracking and customer follow-ups, all through cloud platforms like QuickBooks, Xero, and Gusto. With strong internal controls, familiarity with U.S. compliance norms, and efficient offshore workflows, VJM Global helps companies:

Reduce DSO (Days Sales Outstanding)

Maintain cleaner books with fewer overdue accounts

Improve reporting and visibility into receivables

Free up internal resources to focus on growth

Now, let us discuss the limitations of the accounts receivable turnover ratio.

Limitations of the Accounts Receivable Turnover Ratio

The Accounts Receivable Turnover Ratio is a helpful indicator of how effectively a company collects payments from its customers. However, it has several limitations:

Doesn’t reflect seasonal variations: The ratio is usually calculated on an annual basis, which may overlook seasonal peaks and dips. This can give a misleading picture of a company’s actual receivables performance.

Credit policies can influence ratios: A higher ratio reflects tighter credit policies rather than efficient collections. It doesn't necessarily mean the company is managing receivables well.

Ignores customer risk and concentration: The ratio doesn’t show whether receivables are spread across many customers or concentrated in a few high-risk clients. This could hide potential collection issues.

Averages can mask fluctuations: Using average accounts receivable may conceal significant short-term changes, especially if there is a spike in unpaid invoices toward the end of the period.

Doesn’t track trends over time: It provides a single data point, not a view of ongoing trends. You won’t see whether collections are improving or deteriorating.

Lacks industry context: The ratio only becomes meaningful when compared with industry benchmarks. A "high" or "low" ratio isn't always good or bad unless viewed in context.

Maximizing Cash Flow with VJM Global’s Accounts Receivable Turnover Optimization

Effective management of your accounts receivable turnover ratio (ARTR) is critical to maintaining a healthy cash flow. The AR turnover ratio measures how efficiently a business collects its outstanding payments, directly impacting its financial stability.

VJM Global offers tailored strategies and expert solutions to streamline AR processes, reduce overdue accounts, and improve liquidity, empowering businesses to enhance their AR turnover and achieve stronger financial growth.

Strategic AR Management: VJM Global offers expert services in designing tailored AR systems that boost your AR turnover. With guidance on setting credit policies and streamlining invoicing and collection processes, businesses can accelerate receivables, enhancing cash flow and financial health.

Invoicing & Payment Tracking Solutions: Automating the invoicing and payment tracking system is crucial to improving your AR turnover ratio. VJM Global implements innovative tools and processes that ensure timely payments, reduce overdue accounts, and increase overall turnover efficiency.

Credit Risk Assessment & Control: A thorough risk assessment is essential to maintaining a favorable AR turnover ratio. VJM Global conducts comprehensive credit evaluations, establishing customer credit limits and policies to prevent bad debts and ensuring your AR turnover stays on track.

Tax & Regulatory Compliance: Complex tax laws and GST regulations impact AR, so VJM Global ensures your AR management is compliant and your financial records are audit-ready. Proper compliance helps avoid penalties, ensuring smooth financial operations and consistent AR turnover.

Real-Time Insights for Decision-Making: By providing timely reports and dashboards, VJM Global gives you a clear view of your AR performance, including aging reports and collection trends. This enables data-driven decisions that further enhance your AR turnover and overall financial strategy.

Global AR Support: For U.S. businesses dealing with cross-border transactions, managing foreign receivables can be challenging. VJM Global simplifies this with expertise in handling foreign exchange, tax compliance, and risk mitigation, ensuring your global AR turnover is optimized for international markets.

VJM Global’s holistic approach to AR management helps you transform your receivables process into a powerful tool for improving your financial stability and growth.

Book a consultation today to discover how we can help you enhance your accounts receivable (AR) turnover ratio and optimize your cash flow.

VJM Global

Explore expert insights, tips, and updates from VJM Global