Accurate financial reporting builds trust, drives decisions, and ensures compliance. That’s why accrual accounting plays a central role in how U.S. businesses manage and present their finances. Unlike cash accounting, which records transactions only when money changes hands, accrual accounting aligns income and expenses with the periods they impact, providing a clearer view of performance.

According to a 2024 report, 82% of small businesses now use cloud-based accounting software, reflecting a strong shift toward automation and structured financial practices that support accrual-based accounting. If you operate a growing business or seek funding, you can’t ignore the importance of this approach. In fact, Generally Accepted Accounting Principles require the accrual basis of accounting for most organizations in the U.S. This article explores how accrual accounting works, when to use it, and why it remains the preferred method under GAAP.

Accrual accounting is a method of financial recording that recognizes revenues and expenses when they are earned or incurred, regardless of when the actual cash is received or paid. Unlike cash-basis accounting, which records transactions only when money changes hands, accrual accounting provides a more accurate picture of a company’s financial health by matching income with the expenses incurred to generate that income within the same period.

For US businesses and entrepreneurs, understanding and implementing accrual accounting is crucial, especially as companies grow and seek to maintain compliance with Generally Accepted Accounting Principles (GAAP). The accrual method provides a clearer understanding of long-term profitability, cash flow management, and financial obligations, making it easier to plan, budget, and attract investors or lenders.

Now, let's examine the types of accruals in accounting and their significance to your business in detail below.

Accrual accounting plays a crucial role in providing an accurate financial picture of a business by recognizing revenues and expenses when they are earned or incurred, rather than when cash is actually exchanged. For U.S. businesses and entrepreneurs, understanding the different types of accruals is essential to ensure compliance with Generally Accepted Accounting Principles (GAAP) and to maintain clear, transparent financial records that support informed decision-making and accurate tax reporting.

Here are the main types of accruals that businesses commonly encounter:

These are revenues that a business has earned by delivering goods or services but has not yet received payment for by the end of the accounting period. For example, a software consulting firm in New York may complete a project in June but invoice the client in July. Under accrual accounting, revenue is recognized in June, reflecting the actual timing of work performed rather than the receipt of payment.

Why it matters: Recording accrued revenues guarantees entrepreneurs reflect all earned income in the correct period, which improves financial forecasting and tax planning.

Accrued expenses represent costs a business has incurred but not yet paid. This can include wages owed to employees, utilities used but not yet billed, or interest on loans that have accumulated and remain unpaid by the end of the period.

For example, a small manufacturing business in Ohio might have employees who worked the last week of the month but won’t receive paychecks until the following month. Recording accrued wages in the current month guarantees that expenses align properly with the period during which the labor was provided.

Why it matters: Properly accruing expenses helps maintain an accurate liability picture and prevents underreporting costs, which can distort profitability.

These are taxes that a business owes but has not yet paid. This includes income taxes, payroll taxes, or sales taxes collected but not remitted to the appropriate authorities. For US businesses, accurately accruing taxes at period-end guarantees compliance with IRS regulations and prevents surprises during tax audits or filings.

Why it matters: Failing to accrue taxes can result in underreporting liabilities, which can trigger penalties, interest charges, and increased audit risks. Accurate accruals help businesses stay compliant and prepared for upcoming tax payments.

Accrued interest refers to interest expenses or income that accumulate over time but have not been settled by payment. For example, suppose a business has a loan with monthly interest due on the 15th but its accounting period ends on the 30th. In that case, it needs to record interest expense for the unpaid portion as accrued interest.

Why it matters: This type of accrual ensures that interest costs are matched with the periods to which they relate, providing a more accurate representation of financing costs.

If a business occupies leased premises but the rent payment is due after the accounting period closes, it should recognize the rent expense for the period in which the space was used. For entrepreneurs operating retail stores or offices in the US, this aligns expenses with the benefits received.

Why it matters: Accruing rent ensures that occupancy costs are recorded in the correct accounting period, supporting accurate profit-and-loss reporting. It also prevents overstating cash reserves and underestimating liabilities.

So, how does accrual accounting work in business? Let us understand this in detail below.

Also Read: What Are the Key Considerations in Accounting for Startup Costs in 2025

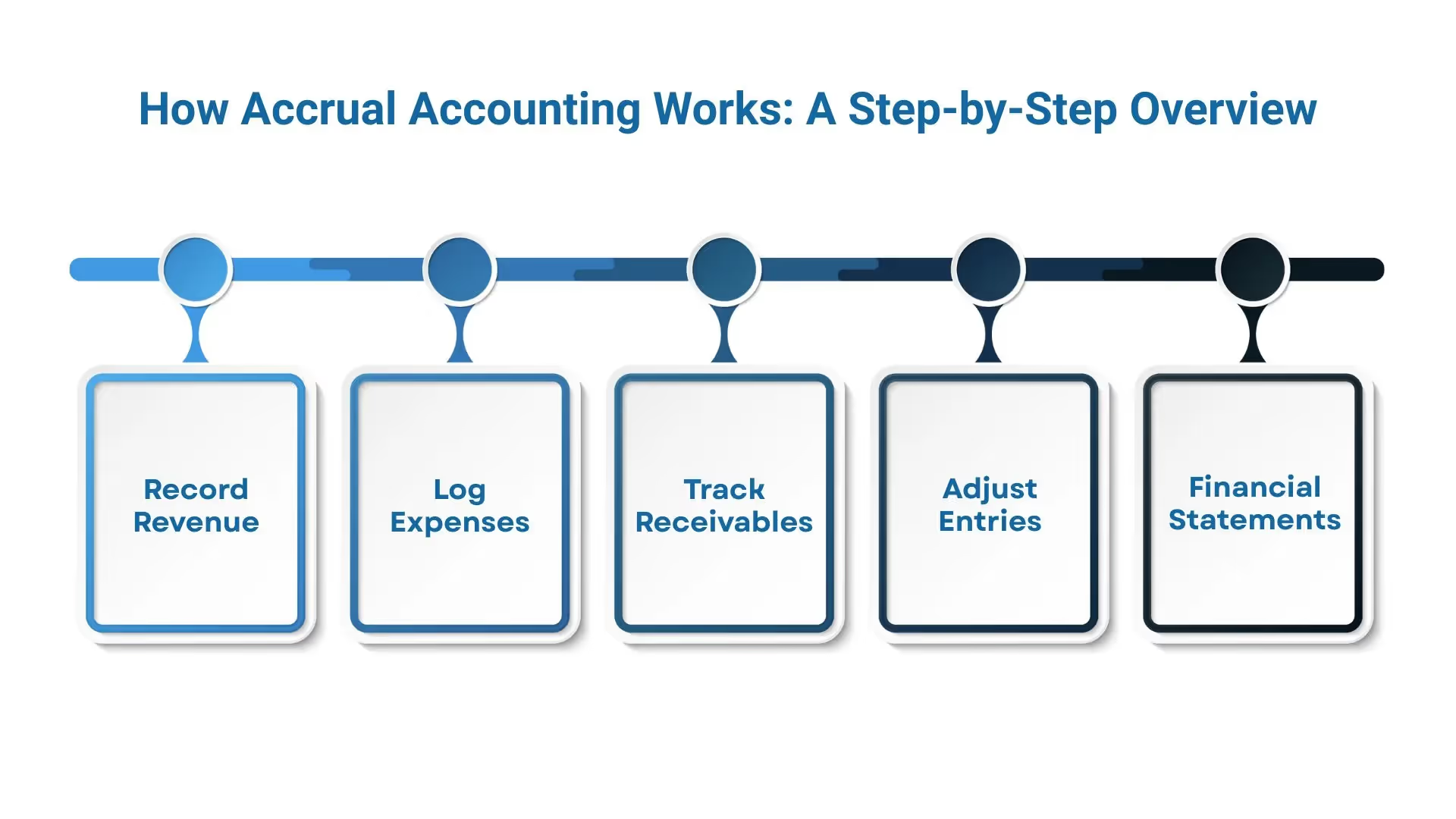

Accrual accounting works by recording financial transactions at the time they happen, not when the cash is actually received or paid. This means you recognize revenues when you deliver goods or services, and you record expenses when you incur them, regardless of whether money has exchanged hands. This system gives you a clear and timely view of your company’s financial position and performance.

Here’s how accrual accounting works step by step for US businesses and entrepreneurs:

Now, let us explore what purpose accruals in accounting serve for the financial stability of your business.

Accrual accounting plays a crucial role in helping U.S. businesses and entrepreneurs gain a clear and accurate picture of their financial health. Here’s why accruals matter:

So, what is the difference between accrual accounting and cash accounting? Let us understand the difference below.

Suggested Read: Benefits of Offshore Accounting for Business Success

Choosing the right accounting method is a foundational decision for any business. In the US, small businesses often start with cash accounting because it’s simple and easy to manage. But as a company grows, accrual accounting becomes critical for accurate financial planning, compliance, and scalability.

Cash accounting may be suitable for small businesses with simple transactions. However, as operations scale, accrual accounting provides the rigor and visibility necessary to manage growth effectively.

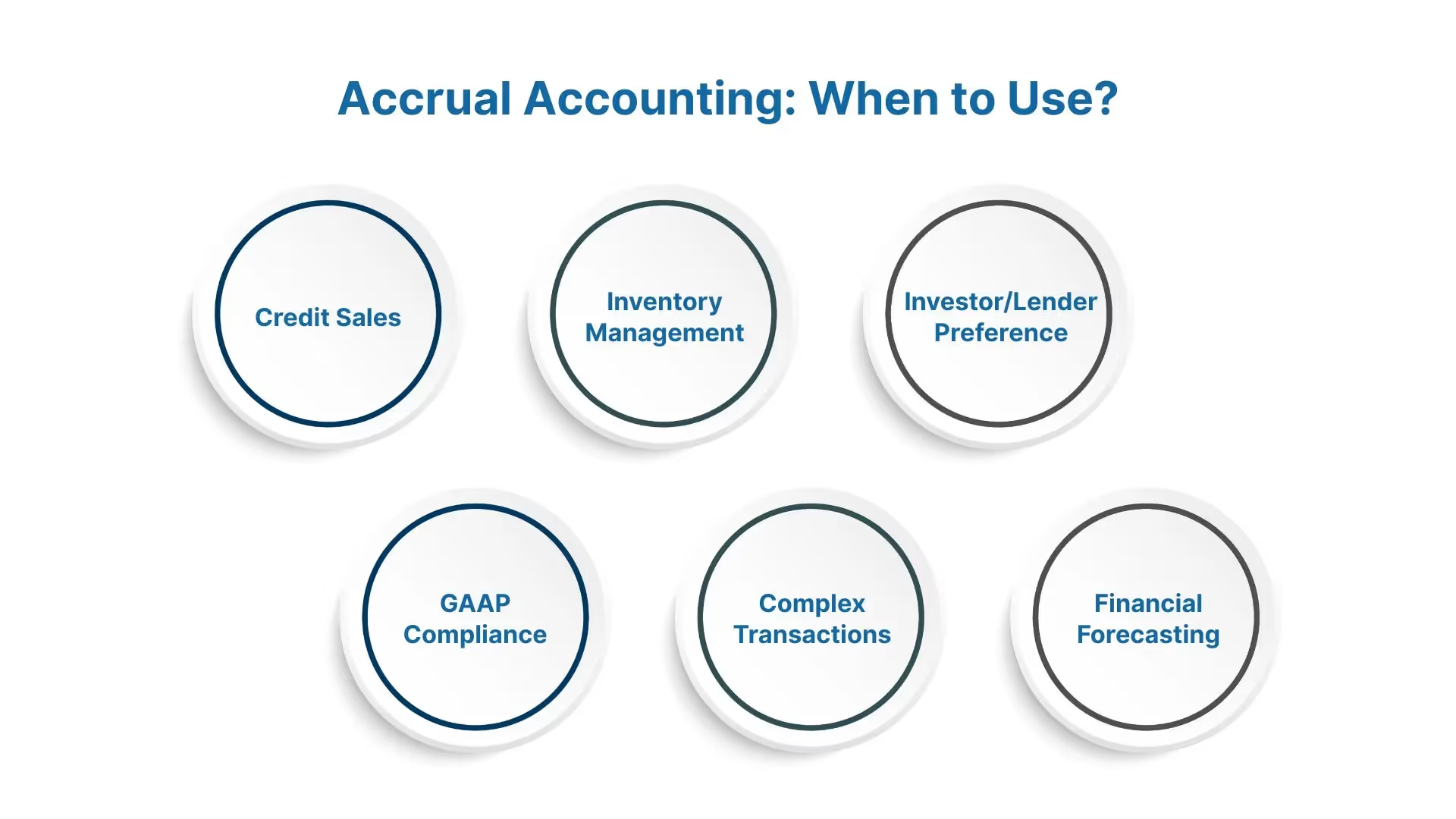

So, when should businesses use accrual basis accounting? Let us explore the situations below.

Accrual basis accounting records revenues and expenses when they are earned or incurred, regardless of when the cash actually changes hands. This method provides a more accurate picture of a company’s financial health over time. It is especially valuable for many US businesses and entrepreneurs. Here’s when you should consider using accrual accounting:

If your business offers products or services on credit, meaning you invoice customers and expect payment at a later date, accrual accounting helps you track those sales as soon as the transaction occurs. This prevents revenue from being delayed until cash is received and gives a clearer view of your earnings and outstanding receivables.

Businesses that maintain inventory must account for the cost of goods sold (COGS) in the same period as the related sales. Accrual accounting matches inventory expenses with revenues, reflecting the true profitability of your sales. It also guarantees compliance with IRS regulations, especially if your business's gross receipts exceed $25 million annually.

Investors and lenders typically prefer financial statements prepared under accrual accounting because they offer a comprehensive snapshot of business performance and financial position. This transparency can improve your chances of securing funding, as it highlights not only cash flow but also liabilities and earned revenues.

Most larger businesses in the US and publicly traded companies are required to follow GAAP, which mandates the use of accrual accounting. Adopting this method early can make future transitions easier if your company plans to grow or go public.

Accrual accounting is better suited for businesses with multiple revenue streams, long-term contracts, or deferred expenses, as it provides a more accurate representation of their financial position. It provides a more detailed and precise matching of income and expenses to the appropriate periods. This is essential for accurate financial analysis and decision-making.

Because accrual accounting accounts for earned revenue and incurred expenses regardless of the timing of cash flow, it offers a clearer view of future cash requirements. This insight helps you plan budgets, manage working capital, and make strategic decisions with confidence.

So, why do companies find accrual accounting important for the financial stability of their business? Let us understand below.

You Might Also Like: How to Manage Accounting for Small Businesses

Accrual accounting is the preferred method for many U.S. businesses because it provides a more accurate and comprehensive view of a company’s financial position. Unlike cash basis accounting, which records income and expenses only when money changes hands, accrual accounting tracks transactions when they’re earned or incurred, regardless of when payment happens.

This approach helps businesses stay compliant, manage cash flow more effectively, and plan for long-term growth.

If you’re asking, “Is accrual basis GAAP?” or “Does GAAP require accrual accounting?” the answer is yes. For most U.S. companies, accrual accounting is required by GAAP to produce accurate, compliant reports.

Now, let's understand how accounting software helps businesses with accrual-based accounting in more detail below.

For US businesses and entrepreneurs, managing finances accurately is critical. Accrual-based accounting records revenues and expenses when they’re earned or incurred, not when cash changes hands. It offers a clearer financial picture, but it's complex to handle manually. That’s where accounting software comes in.

1. Automates Complex Transaction Tracking: Accrual accounting requires precise tracking of receivables and payables. Software automates this by recording revenue when invoices are issued and expenses when bills are received, regardless of payment timing. This reduces manual work, minimizes errors, and keeps financials accurate.

2. Improves Financial Reporting Accuracy: Most US businesses must follow GAAP, which often requires accrual accounting. Software generates real-time reports such as income statements and balance sheets based on up-to-date data. This helps with smarter decisions, better tax planning, and investor readiness.

3. Simplifies Tax Preparation and Compliance: Accrual accounting affects taxable income reporting. Software maintains detailed records as income and expenses accrue, helping businesses comply with IRS rules, reduce audit risks, and simplify multi-state or complex tax filings.

4. Improves Cash Flow Management: Accrual accounting gives a full financial view, but it can complicate cash flow. Software tools such as aging reports help track unpaid invoices and upcoming bills so entrepreneurs can plan and avoid cash shortfalls.

5. Supports Scalability for Growing Businesses: As businesses grow, so do transactions and complexity. Accounting software scales easily, integrating with systems like payroll, inventory, and CRM. This keeps accrual records accurate as operations expand.

6. Enables Remote Access and Collaboration: Many US entrepreneurs work remotely or with dispersed teams. Cloud-based accounting tools offer real-time access from anywhere. This enables collaboration with accountants and advisors to keep accrual data current.

With the right accounting software, US businesses can streamline accrual-based accounting, improve compliance, and make informed financial decisions for long-term growth. And that's where VJM Global comes in. Let us explore how it helps businesses achieve financial stability.

Also Read: Guide to Outsourcing in Finance and Accounting Functions

Accrual accounting offers a comprehensive view of a company’s financial health by recognizing revenues and expenses when they are incurred, not just when cash changes hands. This approach provides a more accurate reflection of business performance and financial position, essential for informed decision-making.

By capturing all economic activities in real-time, accrual accounting enables businesses to monitor profitability, manage cash flow projections, and comply with regulatory requirements. It supports transparency and accountability, which are critical for stakeholders, including investors, lenders, and management teams.

VJM Global empowers U.S. CPA firms with offshore accounting solutions tailored to mastering the complexities of accrual accounting and enhancing financial reporting accuracy.

As regulatory demands increase and client expectations evolve, partnering with VJM Global gives your CPA firm a strategic advantage, offering high-quality accrual accounting support while optimizing costs and operational efficiency.

Ready to elevate your firm’s accrual accounting capabilities? Connect with VJM Global today and discover how our offshore accounting professionals can help you enhance financial accuracy, reduce costs, and provide superior client service.

Ans. Accrual accounting records revenues and expenses when they are earned or incurred, regardless of when cash is exchanged. Cash accounting only records transactions when cash is received or paid. Accrual accounting provides a more accurate picture of a company’s financial health over time.

Ans. Companies use accrual accounting because it matches revenues with related expenses in the same period, giving a clearer view of profitability and financial position. This approach is essential for larger businesses, investors, and lenders who require reliable and timely financial information.

Ans. Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) require accrual accounting for publicly traded companies and many larger private firms. Smaller businesses may be permitted to use cash accounting unless regulations or lenders require the use of accrual methods.

Ans. Accrual accounting improves decision-making by reflecting all earned revenues and incurred expenses within the correct accounting periods. This comprehensive view helps managers assess performance, forecast cash flow needs, and plan investments more effectively.

Ans. Accrual accounting can be complex to implement and maintain due to the need to estimate accrued revenues and expenses, as well as track receivables and payables. It also requires more robust accounting systems and expertise, which may increase operational costs for smaller businesses.