%20(11).avif)

Understanding financial consolidation can be a challenge for businesses, especially when it comes to managing interests in variable entities. ASC 810 plays a crucial role in determining how businesses disclose their interests and relationships with subsidiaries and variable interest entities (VIEs). Without a clear grasp of ASC 810, companies risk non-compliance, improper reporting, and financial misstatements, leading to potential audits, fines, and stakeholder distrust.

This blog will break down the key principles behind ASC 810, focusing on the requirements for consolidating financial statements and identifying VIEs. You will be given insights needed to ensure compliance and enhance financial reporting accuracy.

ASC 810 is a key U.S. GAAP standard established by the Financial Accounting Standards Board (FASB) to guide companies in consolidating financial statements. It ensures that businesses with multiple entities stay compliant when reporting financials, especially during mergers, acquisitions, or expansion efforts.

This standard is particularly relevant for industries like SaaS, where companies often have a complex network of investments and partnerships. ASC 810 helps businesses tackle situations involving acquisitions, joint ventures, or the use of Variable Interest Entities (VIEs).

ASC 810 provides two main models for consolidation:

These models are essential for understanding how control is determined and how consolidation should be applied.

Also Read: Understanding US GAAP Lease Accounting Standards: A Comprehensive Guide

Now that we’ve defined ASC 810, let’s understand how it can enhance the accuracy and transparency of your financial reporting.

ASC 810 provides clear guidance for consolidating financial statements across multiple entities, offering several benefits for SaaS companies:

Consolidating financial results into one set of statements offers investors a clear, unified view of the company’s performance. This reduces the complexity of analyzing multiple separate statements, helping investors make more informed decisions and assess risk with greater accuracy.

Adhering to ASC 810 ensures SaaS companies comply with U.S. GAAP, which is crucial for businesses with subsidiaries or joint ventures. Compliance builds trust and credibility with investors and regulators, protecting against legal risks and maintaining market confidence.

Consolidation directly affects key financial metrics such as revenue, profitability, and cash flow. Accurate consolidation ensures these metrics reflect the true financial health of the business, supporting strategic decision-making and capital-raising efforts.

A consolidated financial view helps identify inefficiencies, streamline operations, and allocate resources more effectively. By consolidating financial data, SaaS companies can align their resources more effectively across different business units and improve operational efficiency.

For companies involved in M&A, ASC 810 simplifies the integration process. It ensures accurate financial reporting, streamlines due diligence, and minimizes post-acquisition surprises.

ASC 810 strengthens financial transparency, compliance, and strategic planning, providing SaaS companies with a clearer path to growth and stability.

VJM Global can guide your SaaS company through the complexities of ASC 810, ensuring precise consolidation, full regulatory compliance, and a stronger financial strategy. Our expertise helps streamline the consolidation process, protect against financial misstatements, and provide clarity on key metrics that drive growth.

Next, let’s explore when a SaaS company should apply consolidation practices based on its financial structure and relationships.

A SaaS company must consolidate another entity’s financials if it has a controlling financial interest. There are two primary models used to assess control:

If a SaaS company owns more than 50% of the voting shares of another entity, it generally has control, and consolidation is required. The Voting Interest model assumes that ownership of more than half the voting shares gives the parent company control over the entity.

However, keep in mind that other contractual arrangements or circumstances could assign control to another party, even if the ownership stake is less than 50%.

In cases where contractual agreements define control, the VIE model applies. A VIE is an entity where the equity investors are not exposed to enough risk to absorb the expected losses or to enjoy the potential returns.

Instead, control is determined by operational or contractual arrangements. A SaaS company must consolidate a VIE if:

The VIE model ensures that companies consolidate entities that they truly control, even in situations where ownership doesn’t reflect control directly.

Here’s a comprehensive table summarizing the key differences between the Voting Interest Entity (VIE) model and the Voting Interest Entity model under ASC 810.

Each model addresses different types of control and helps determine the right approach for consolidating financials based on the nature of the entity’s structure and governance.

Also Read: Understanding the Differences Between GAAP and GAAS

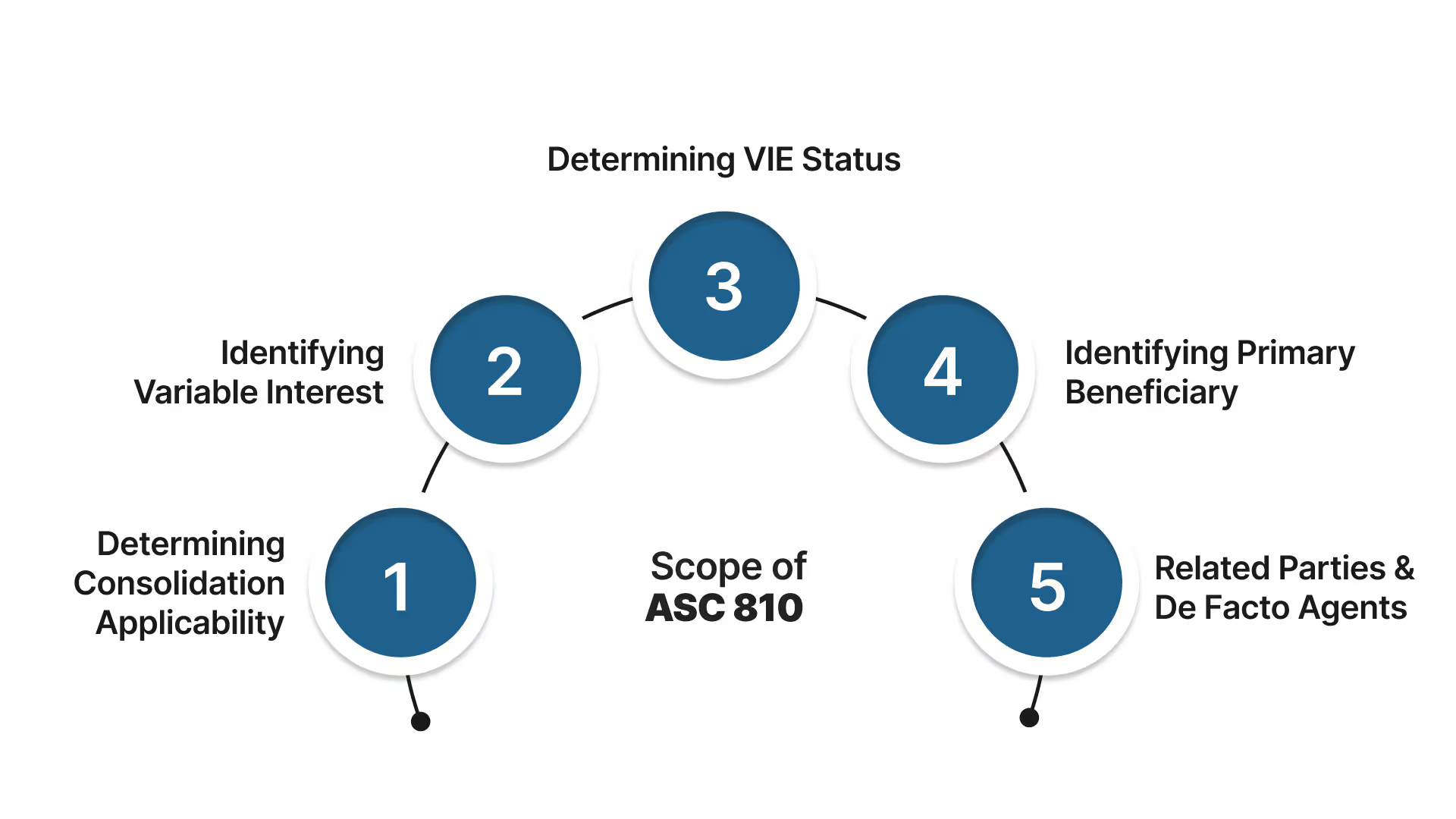

Now that we understand when consolidation is necessary, it’s essential to understand the scope of ASC 810 and its application to your company’s specific situation.

ASC 810 provides clear guidelines for determining when and how a company must consolidate its financial statements. Here's a breakdown of how it works:

Before applying ASC 810, the first step is to determine if both the reporting entity and the legal entity are within the scope of the consolidation guidance and the VIE model.

Most legal entities fall under ASC 810's general consolidation guidance, with some exceptions. If the entity falls under the VIE model, further steps must be taken.

Variable interests refer to any contractual, ownership, or pecuniary interests that change in value in response to changes in the net assets of a legal entity. Common stock is a simple example. As the value of the company’s assets changes, the stock’s value fluctuates with it.

Once a reporting entity identifies a variable interest, the next step is determining if the legal entity qualifies as a VIE. A legal entity is considered a VIE if:

If the legal entity is outside the scope of the VIE model, the voting model applies. Under the voting model, the reporting entity consolidates the legal entity if it holds a majority of the voting rights.

If the entity is identified as a VIE, the next step is to determine the primary beneficiary, i.e., the reporting entity that consolidates the VIE. A reporting entity consolidates a VIE when it has:

Related parties and de facto agents are critical in the VIE model. These entities may not be able to fully pursue their interests independently of the reporting entity, so it's crucial to assess them under ASC 810.

To determine whether an entity is within the scope of ASC 810, ask the following questions:

To determine whether an entity is a VIE, check for characteristics like:

Understanding the scope of ASC 810 is essential for accurate financial reporting, ensuring compliance, and making informed decisions about consolidation and variable interest entities.

Need guidance tackling ASC 810 and its complexities?

At VJM Global, we specialize in helping businesses like yours understand and implement the right consolidation strategies. Let us help you determine if your entity is subject to ASC 810’s VIE model and guide you through the process of compliance. Get started today for expert support and tailored solutions.

Also Read: Lease Taxation Explained: ASC 842 Impacts, IRS Rules, and State Tax Considerations

With ASC 810’s scope in place, let’s take a look at how VJM Global can help you tackle the complexities of financial consolidation.

At VJM Global, we specialize in helping businesses tackle the complexities of financial consolidation under ASC 810. Here’s how we can support you:

Partner with VJM Global to tackle ASC 810’s complexities and ensure your financial consolidation is handled efficiently and accurately.

ASC 810 plays a critical role in ensuring accurate financial consolidation, particularly when dealing with variable interest entities and voting interest entities. Understanding the scope, identifying variable interests, and applying the correct consolidation model are key to maintaining compliance and transparency in financial reporting.

If your business is handling the complexities of ASC 810, VJM Global is here to offer expert guidance and support. Reach out to us today to get started.

ASC 810 provides the accounting guidance for consolidating financial statements, focusing on when and how to consolidate entities based on their structure, such as variable interest entities (VIEs).

The VIE model applies to entities where equity holders lack decision-making rights or the ability to absorb losses. In contrast, the voting interest model applies to entities controlled through voting rights.

An entity is a VIE if it lacks sufficient equity to finance its activities or if the equity holders lack the power to direct significant economic activities.

The primary beneficiary is the reporting entity that has both the power to direct the significant activities of the VIE and the economics (i.e., the right to absorb losses or receive benefits).

ASC 810 ensures that your financial statements accurately reflect the control over and financial interests in subsidiaries, leading to more transparent and compliant reporting.