When analyzing a company's financial health, one question often stands at the forefront: What are the three financial statements that comprehensively convey the complete narrative? While many focus on just one or two, understanding the connections between the Income Statement, Balance Sheet, and Cash Flow Statement is essential for a complete picture of a business's financial performance. These three key documents don't operate in isolation; instead, they are intricately linked, each feeding into and informing the others.

By grasping how they work together, you unlock the ability to read between the lines of financial data, revealing insights that go beyond what meets the eye. Whether you’re an analyst or looking to understand a company's true financial position and performance, this integrated approach is for you. Let’s explore how these three financial statements are interwoven and why their connections matter more than the statements themselves.

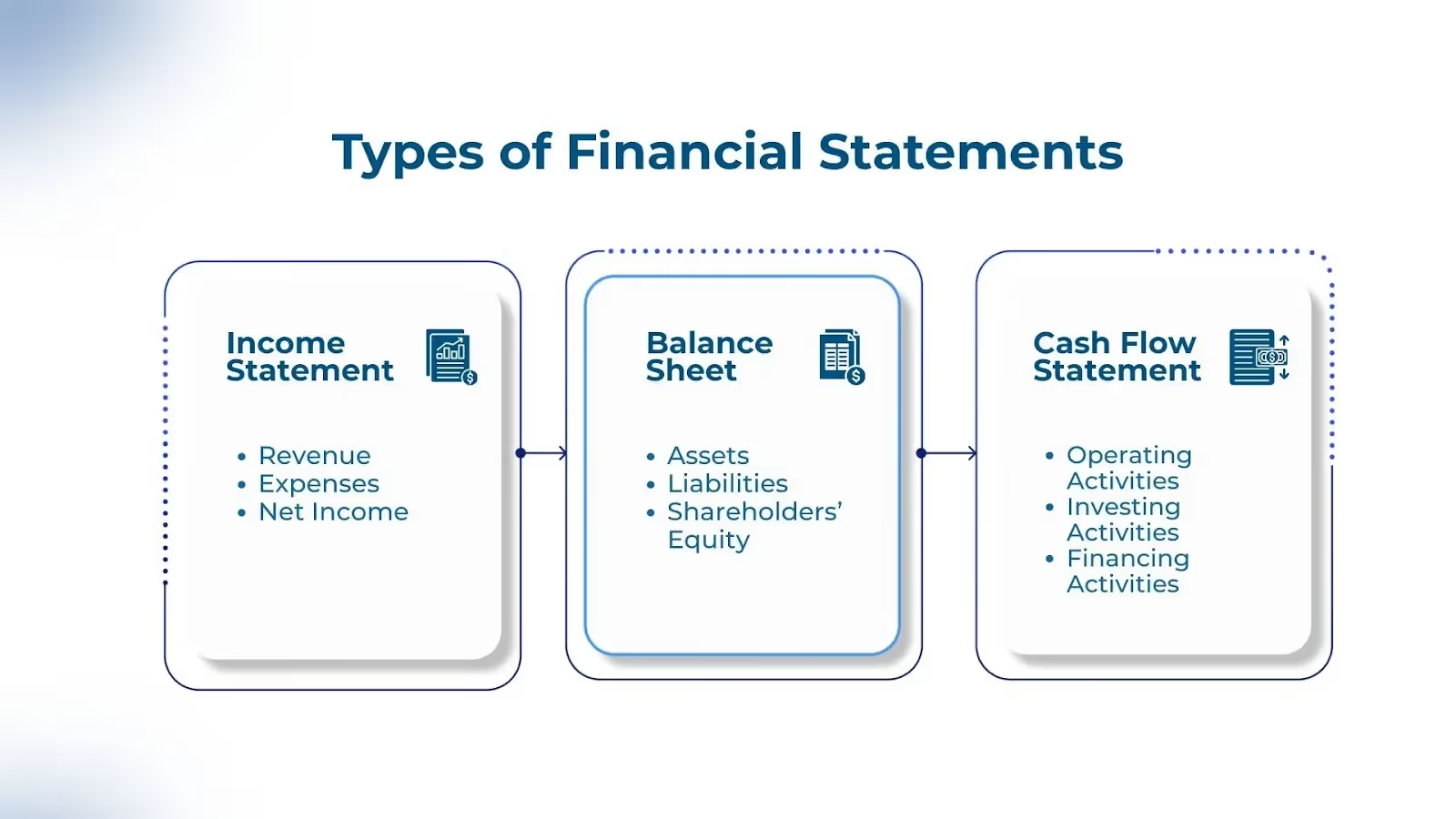

The three key financial statements are (1) the Income Statement, (2) the Balance Sheet, and (3) the Cash Flow Statement. These statements are essential for evaluating a company's financial performance and position. They provide a comprehensive snapshot of a business's financial health and are used by internal management and external stakeholders, such as investors, analysts, and creditors.

To better understand how each of these statements contributes to a company’s financial overview, let’s begin by taking a closer look at the Income Statement.

The Income Statement is like the report card for a company’s performance over a specific period. It shows whether a company is profitable by comparing its revenues to expenses. The statement outlines revenue, cost of goods sold, gross profit, operating expenses, and net income. These components tell a clear story of how much money came in and how much was spent, leading to either a profit or a loss.

For example, imagine a business selling products. The revenue comes from sales, but the company incurs costs (e.g., raw materials and labor) to make these products. These costs are subtracted to find the gross profit. After that, the company subtracts its operating expenses (like rent and salaries), and what’s left is the net income, which shows the final profit or loss.

The Income Statement follows accrual accounting rules. This means it doesn’t wait for cash to change hands; it records revenue when earned and expenses when incurred, making it different from the cash flow statement. The net income from this statement connects directly to both the Balance Sheet and the Cash Flow Statement. It affects retained earnings in the Balance Sheet and is the starting point in the Cash Flow Statement.

Now that we’ve looked at how a company earns and spends, let’s take a step back and see the bigger picture through the Balance Sheet.

The Balance Sheet is a snapshot of a company’s financial health at a specific time. It’s divided into three key sections: assets, liabilities, and shareholders' equity. These components offer a clear picture of what a company owns, what it owes, and the value left for its shareholders.

At the core of the Balance Sheet is the accounting equation: Assets = Liabilities + Equity. This simple but powerful formula ensures that the balance sheet "balances." On one side, you have everything the company owns (assets), and on the other, you have how it financed those assets through debt (liabilities) or the owners' contributions (equity).

The purpose of the Balance Sheet is to provide an overview of the company’s financial position. This includes its ability to meet short-term obligations, invest in growth, and generate profits. For example, if a company’s assets outweigh its liabilities, it’s in a healthy position. But if liabilities are high, it could signal financial strain.

Changes in assets and liabilities directly affect other financial statements, particularly the Income Statement and Cash Flow Statement. For instance, when a company takes on more debt, it may affect its net income and cash flow due to interest payments. Similarly, asset changes, like increasing inventory, could affect cash flow.

It’s time to explore how cash actually moves in and out of the business with the Cash Flow Statement.

The Cash Flow Statement is crucial for assessing a company's liquidity and financial flexibility. Unlike the Income Statement, which includes non-cash items, the Cash Flow Statement focuses solely on actual cash inflows and outflows during a period. It categorizes these cash flows into three main sections: operating activities, investing activities, and financing activities.

Starting with net income from the Income Statement, the Cash Flow Statement adjusts for non-cash items, such as depreciation, and changes in working capital, which are reflected in the Balance Sheet. This approach ensures the statement accurately portrays the company’s actual cash movements, giving an accurate picture of its liquidity.

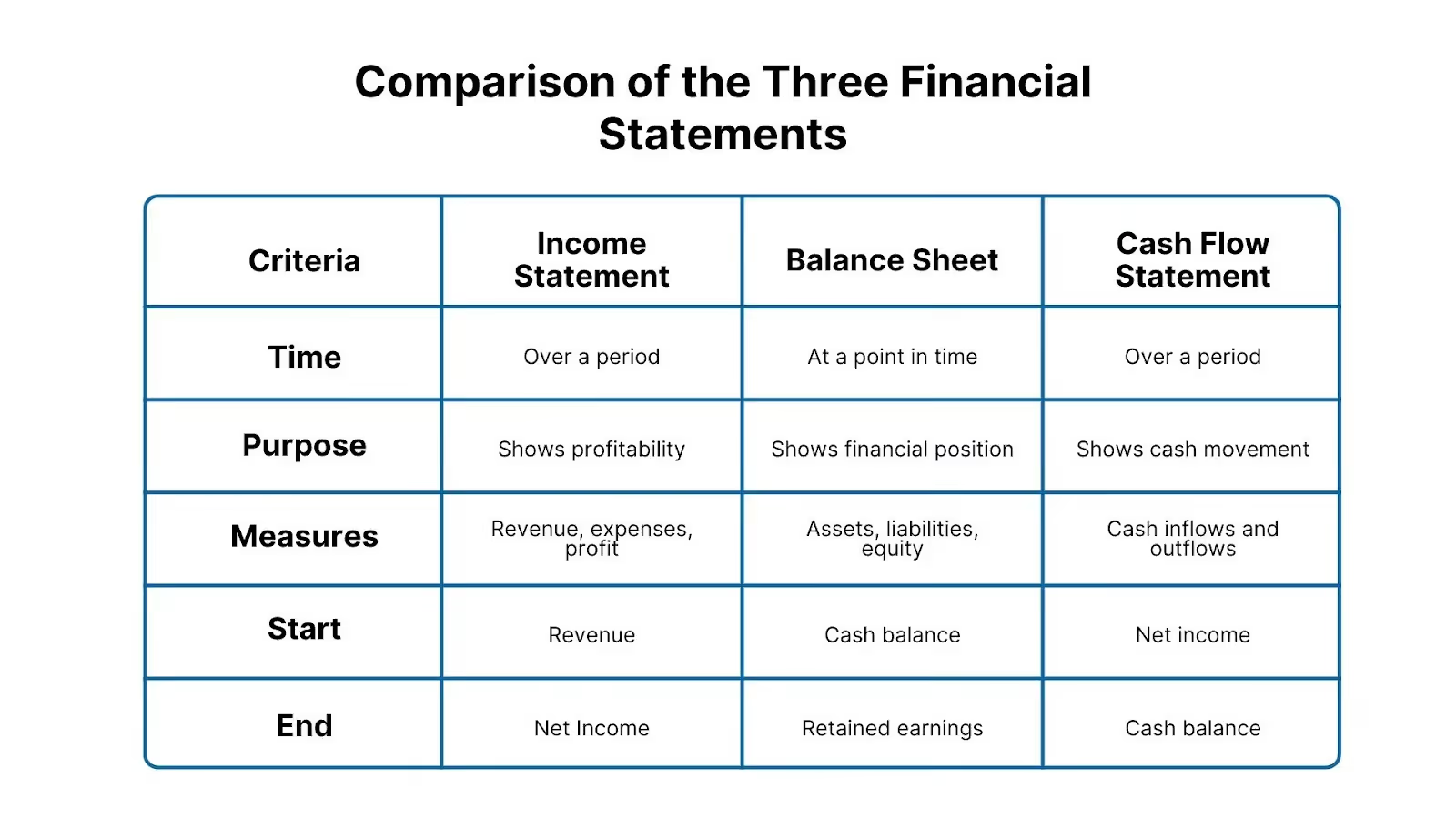

Having explored the Cash Flow Statement, it's time to compare all three financial statements to see how they work together to provide a complete picture of a company’s financial health.

After comparing the three financial statements, let's examine how they relate to one another and function as a whole to present a comprehensive financial picture.

The Income Statement, Balance Sheet, and Cash Flow Statement rely on the principles of accrual accounting, which creates a strong link between them. Each statement provides valuable information, but the interplay among them offers a comprehensive view of a company’s performance and position. Here's how each one connects:

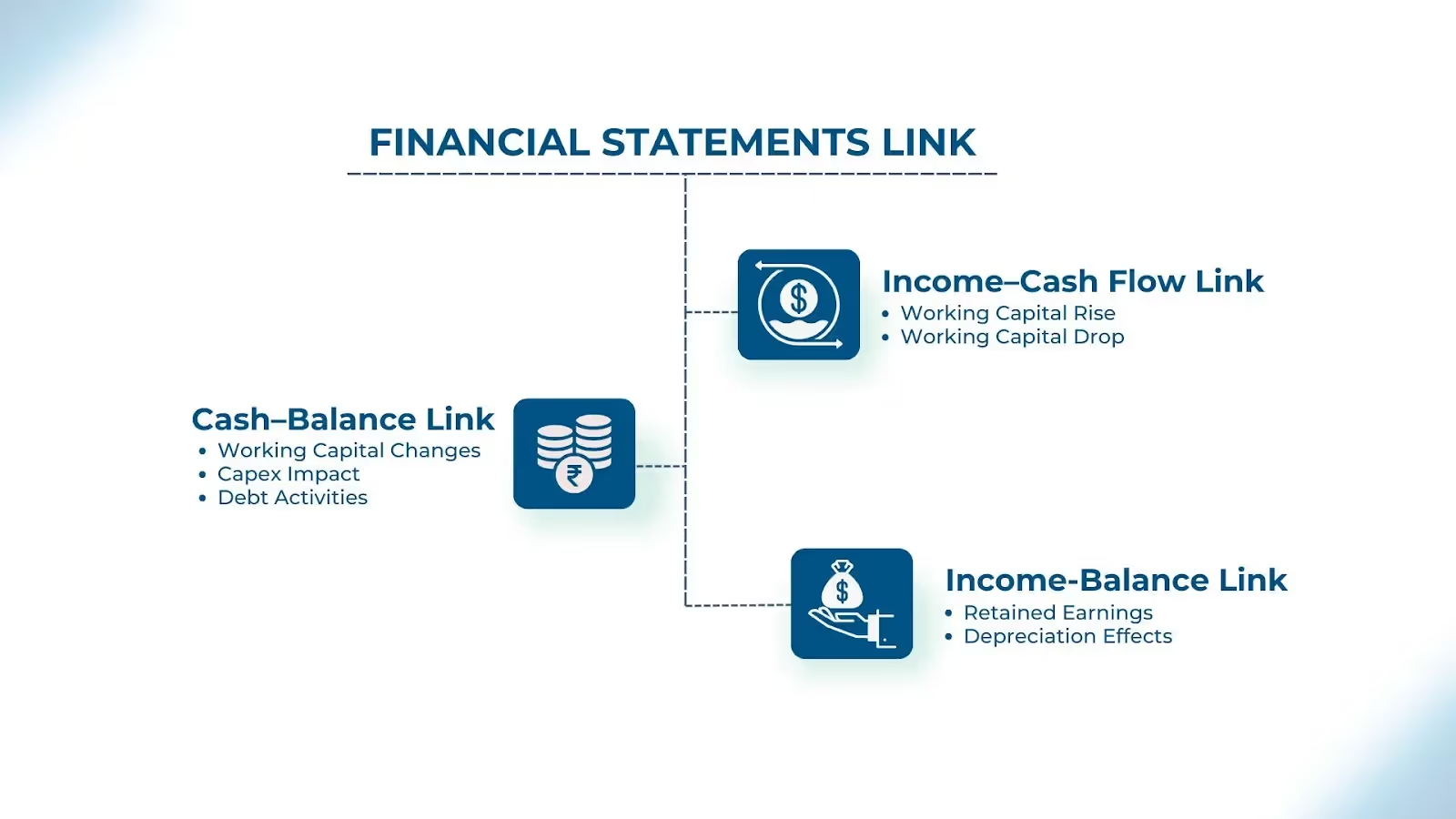

The Income Statement and Cash Flow Statement are directly linked through net income. The net income at the bottom of the Income Statement is the starting point for the Cash Flow Statement.

From this point, the Cash Flow Statement adjusts for non-cash items like depreciation and amortization (D&A), which are expenses that reduce net income but don’t impact cash. Additionally, it accounts for changes in working capital, such as increases in accounts receivable or inventory, which represent cash outflows or inflows.

For example:

By adjusting for these items, the Cash Flow Statement provides an accurate picture of the cash a company actually generated or used during a period, despite the accrual accounting in the Income Statement.

The Cash Flow Statement and Balance Sheet are closely connected through changes in working capital, capital expenditures (Capex), and financing activities. Here's how they link:

The Income Statement and Balance Sheet are primarily linked through retained earnings. Here's how this connection works:

The formula for retained earnings is:

Retained Earnings = Beginning Balance + Net Income – Dividends

If the company earns a profit, it adds to the retained earnings, increasing shareholders’ equity; if there is a loss, retained earnings decrease.

Having understood how the three financial statements are linked, let's examine how these core statements are utilized in financial modeling.

Financial modeling is about predicting a company’s future performance. You must integrate the Income Statement, Balance Sheet, and Cash Flow Statement to create an accurate model. These three financial statements work together, providing a complete structure for any monetary model.

The first step in financial modeling is to create line items for each of the three statements. These line items serve as the building blocks for the model. After setting up the structure, you'll reconcile the data across all statements to ensure consistency.

For example, net income from the Income Statement should match the starting point on the Cash Flow Statement, and the ending cash balance from the Cash Flow Statement must match the cash on the Balance Sheet.

Once the statements are aligned, assumptions are prepared based on historical data. These assumptions help forecast future performance.

Forecasting is central to financial modeling. You can predict future economic outcomes by analyzing historical trends from all three statements. For example, if sales have grown consistently at 10% annually, you can project future sales revenue using the same rate. Similarly, stable operating expenses can be projected using past trends.

The Cash Flow Statement plays a key role, especially in understanding how working capital and capital expenditures changes will impact cash flow. This is important for assessing whether the company will have enough cash to cover its obligations and fuel future growth.

Building a detailed model often requires supporting schedules for more complex items. For example:

Understanding the three financial statements can seem complex, but it doesn’t have to be overwhelming. With a solid grasp of their interconnections, businesses can make better financial decisions and ensure a clearer path to future growth. Each statement provides unique insights, and when combined, they offer a complete picture of a company’s performance and financial health.

Maintaining accurate financial records and regularly reviewing them allows companies to prevent errors and anticipate challenges. If your business needs expert guidance in structuring or interpreting these financial statements, VJM Global is here to help.

Our team offers specialized support for financial modeling, ensuring alignment with industry standards and providing the insights you need to make informed decisions. Reach out for personalized assistance. We're here to guide you through the intricacies of financial analysis, allowing you to concentrate on what truly matters.