.avif)

When you're a partner in a business, you'll encounter a tax form that is as important as a W-2 or a 1099, but often far more complex: Schedule K-1 (Form 1065). This form is an essential piece of the tax puzzle for millions of Americans. If you're a partner or work with partnership tax filings, you'll need a solid understanding of this document.

In this blog, we'll break down the purpose of the K-1, show you how to use the form to file your personal tax return, and highlight the common pitfalls and limitations that can arise. This guide will help you confidently address the complexities of partnership tax reporting. So, let's start with the basics: what exactly is this form and why is it so vital?

Schedule K-1 is a tax document prepared by a partnership and issued to each individual partner to report their share of the business's income, losses, deductions, and credits. A partnership is considered a "pass-through" entity, meaning the business itself doesn't pay income tax.

Instead, the profits and losses are passed through to the partners, who are then responsible for reporting and paying taxes on their share on their individual tax returns. The K-1 is the detailed roadmap that tells you exactly what to report.

Understanding the K-1 is especially important for small to mid-sized businesses and the accounting professionals who support them, as it's the central document that connects the business's financial health to each partner's personal tax situation.

The Schedule K-1 is a vital tool for ensuring that a partnership's financial results are properly allocated to its partners for tax purposes. Its core role is to accurately inform each partner of their specific share of the business's tax attributes for the year.

The partnership first calculates its total income, deductions, and credits on its main tax return, Form 1065. It then uses the Schedule K-1 to divide these amounts among all the partners, based on the terms of the partnership agreement. This process reports a partner's share of specific items, including:

This detailed information is the key link that enables you to report your portion of the business's earnings and losses on your personal tax return (Form 1040), preventing the double taxation of income at both the entity and individual levels. To fully grasp the K-1, it is essential to understand the type of entity that issues it.

The concept of a "pass-through entity" is central to understanding the Schedule K-1. Unlike a traditional C-corporation, which pays its own corporate income tax on profits before distributing dividends to shareholders, a pass-through entity avoids this extra layer of taxation. For this reason, these entities are also sometimes referred to as "flow-through" entities.

The business itself does not pay federal income tax. Instead, all profits, losses, deductions, and credits generated by the business are "passed through" directly to the partners. These partners then report their proportional share on their individual tax returns. This is why a Schedule K-1 is so crucial—it provides the precise numbers needed to calculate the tax liability at the individual level.

Common types of pass-through entities include:

It is important to note that a partner is taxed on their share of the entity’s income, whether or not they receive a cash distribution. For example, a partnership might choose to retain profits for business growth, but the partners must still pay taxes on that income. The K-1 will reflect these non-cash earnings, ensuring all tax attributes are correctly reported. The K-1 itself is broken down into specific sections that make this reporting possible.

For a smooth tax filing process, it's essential to have your business structure and accounting in order from the start. VJM Global can provide expert Business setup Advisory and Accounting Outsourcing to help ensure your financials are always K-1 ready.

Also Read: Why Do Global Companies Trust Indian Outsource Accounting Firms?

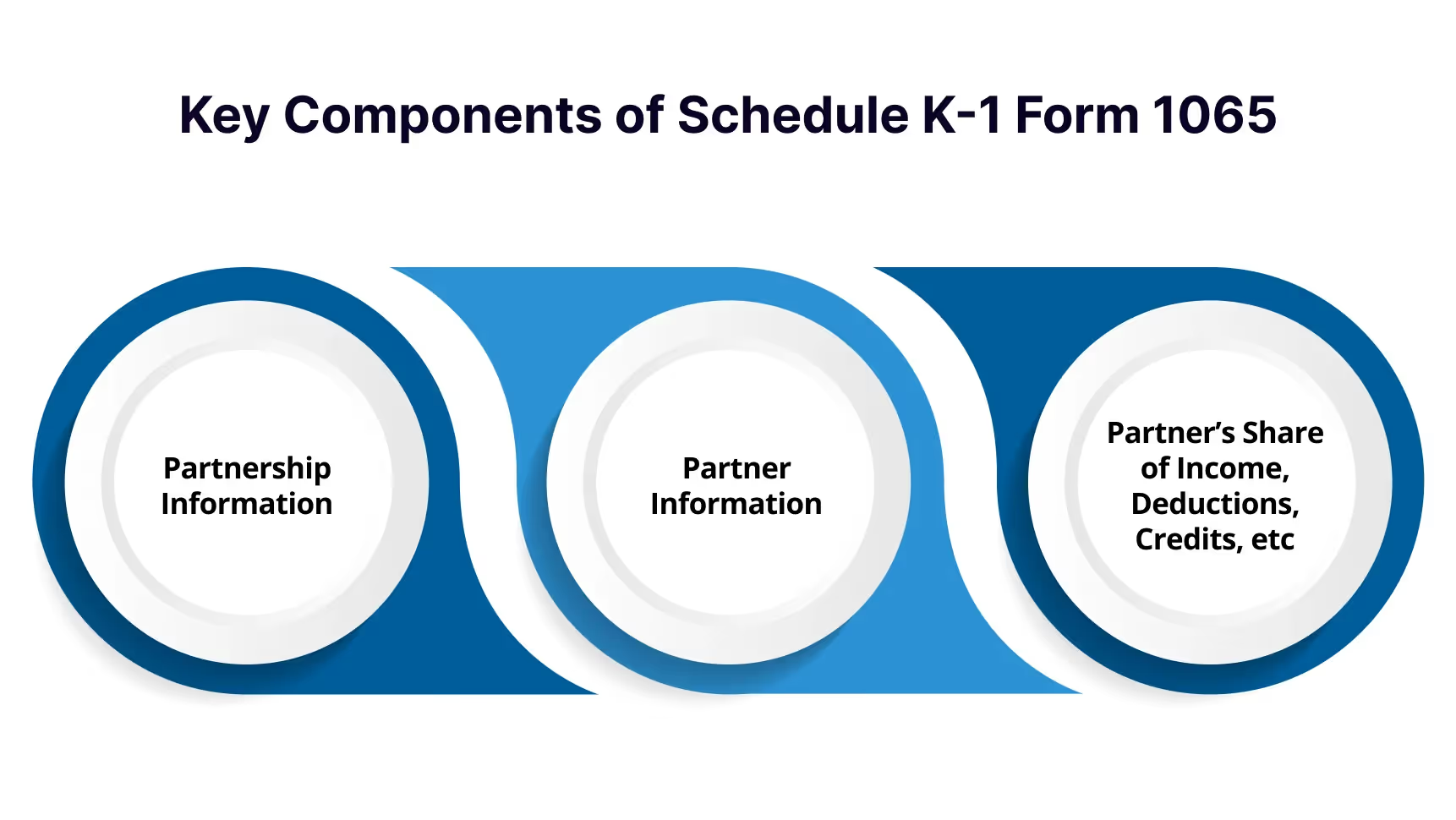

The Schedule K-1 is divided into three distinct parts, each providing a specific piece of information vital for accurate tax reporting.

Each line item in Part III corresponds to a specific line on your personal Form 1040, which makes the K-1 an indispensable guide for accurately preparing your tax filing. Now that we have covered the components, let's look at the practical application of the K-1 when you prepare your return.

The complexity of Part III can be daunting. Rather than manually transferring figures, consider a seamless approach. VJM Global specializes in comprehensive Direct Taxation and International Taxation services, helping you report these details with confidence and accuracy.

Also Read: International Tax Planning Strategies for 2025

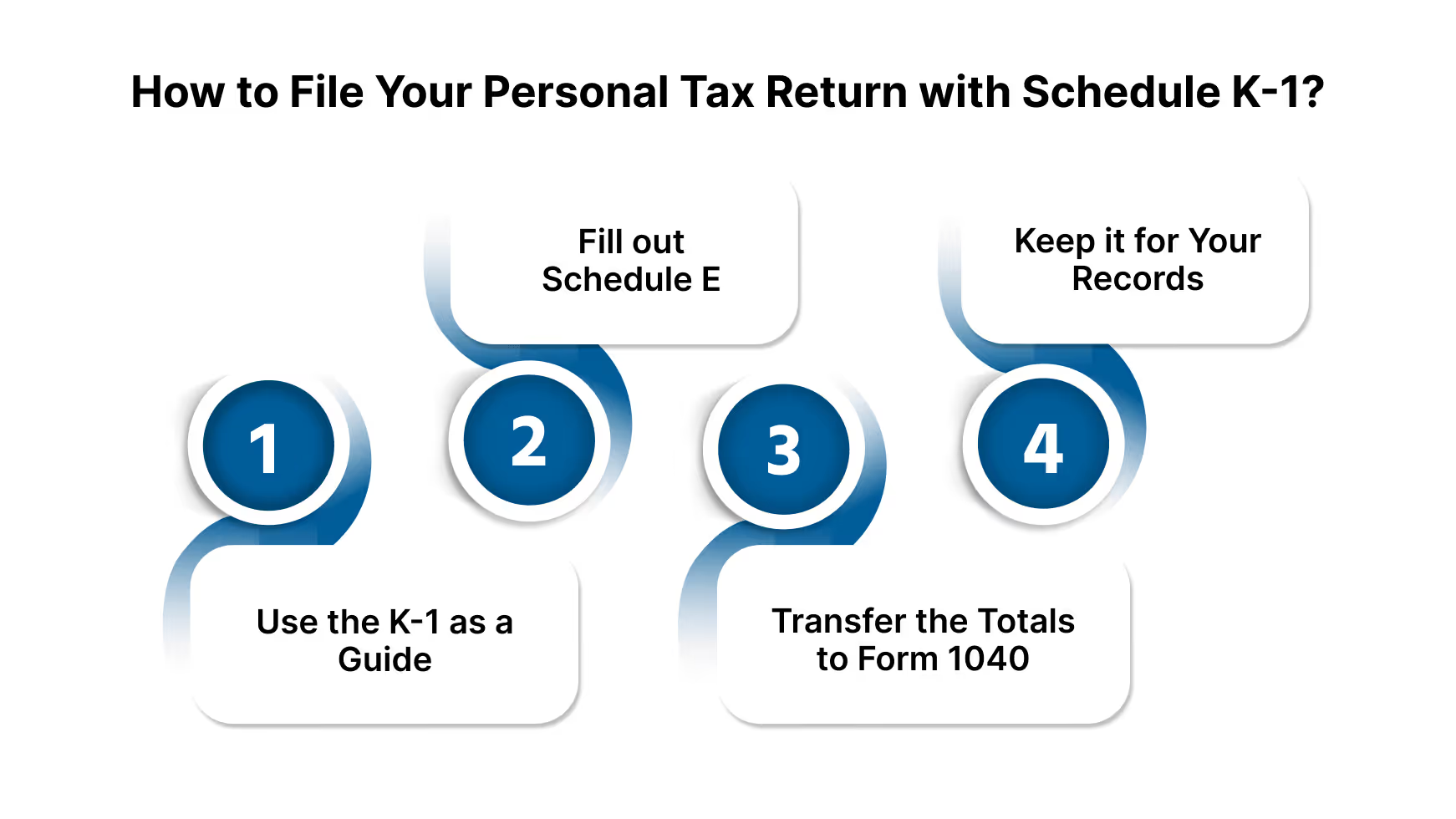

When it comes to filing your personal tax return (Form 1040), the Schedule K-1 is not a form you attach and submit to the IRS. Instead, it serves as a detailed reference document. You will use the information from Part III of the K-1 to fill out a separate form, most commonly Schedule E (Supplemental Income and Loss).

Here's a general overview of the process:

Navigating the complexities of a K-1 can be challenging, and it's always a good idea to consult a tax professional to ensure everything is reported correctly. The partnership is required to send the K-1 to you by March 15th, but extensions are common, so it's not unusual to receive it later. While the process may seem straightforward, there are a number of common pitfalls and limitations that partners often encounter.

While the Schedule K-1 reports your share of a partnership's financial results, receiving a loss on the form doesn't automatically mean you can deduct it on your personal tax return. The IRS imposes a series of rules that limit the amount of a loss you can claim in a given year. These limitations are applied in a specific order and can be a common source of confusion for partners.

Understanding these rules is vital for correctly reporting your partnership income and losses and avoiding potential issues with the IRS. In addition to these rules, partners may also face challenges related to the form's timely delivery or accuracy.

Navigating complex loss limitations is challenging. VJM Global’s experts offer clear guidance to help you apply the rules correctly, maximize deductions, and stay compliant.

It's common for partners to face challenges with their Schedule K-1, particularly regarding delays in receiving the form or discovering errors once they have it. Knowing how to handle these situations is critical to ensure a smooth tax filing process.

The Schedule K-1 is a cornerstone of tax reporting for partnerships and their partners, but it is not a simple form. While it provides the crucial link between a business's financial results and an individual's tax return, its complexity, combined with the various IRS limitations on deducting losses, makes accurate reporting a challenge.

Understanding the concepts of a pass-through entity, the different parts of the K-1, and the potential pitfalls related to basis, at-risk, and passive loss limitations is essential. However, the intricacies of tracking your partnership basis and correctly applying these rules can be overwhelming for many partners.

Consulting a qualified tax professional is often the best course of action to ensure that you are complying with all tax laws and accurately reporting your income and losses. For peace of mind and expert guidance on everything from managing your K-1 to comprehensive business tax planning, consider reaching out to the dedicated team at VJM Global.

Contact us today to outsource your firm’s accounting!

A. It's used by a partnership to report each partner's share of income, losses, deductions, and credits. This allows the individual partners to correctly report their earnings on their personal tax returns. It is a fundamental part of the pass-through tax system for business partnerships.

A. Yes, the k 1 tax form is essential. It provides the specific numbers from the partnership's financial results that you must report on your individual Form 1040. Without it, you cannot accurately complete your personal tax return.

A. The initial deadline for the partnership to issue the Form 1065 Schedule K-1 is typically March 15th. However, partnerships often file an extension for Form 1065, which can delay the delivery of the k1 tax document until a later date.

A. The capital account reported on a sch K-1 is often a starting point, but it's not the same as your adjusted basis. The adjusted basis is a critical metric for a k 1 for partnership and includes additional factors like partnership debt and other adjustments.

A. Form 1065 is the partnership's main tax return, which reports the business's overall financial results to the IRS. The schedule k of form 1065 summarizes all partners' shares of the business's profits and losses, serving as a summary before the individual K-1 forms are issued.

A. If you receive a corrected k 1 tax document, you should use the new form to amend your tax return if you have already filed. The original is no longer valid for filing purposes, but you should retain both forms for your records.