Introduction

Singapore businesses expanding into India face a complex accounting landscape that can catch even experienced CFOs off guard. While Singapore's Financial Reporting Standards (SFRS) align closely with IFRS, India operates under its own converged framework — Indian Accounting Standards (Ind AS) — featuring distinct rules, thresholds, and compliance obligations.

A Singapore parent company may prepare consolidated financials under SFRS, but its Indian subsidiary must simultaneously maintain standalone accounts under Ind AS. That means filing with India's Registrar of Companies (ROC) on an April–March financial year cycle and navigating India-specific carve-outs from IFRS that simply don't exist in Singapore.

Non-compliance can result in fines, director penalties, and operational disruptions that affect profit repatriation.

This guide explains what Ind AS is, who governs it, how it compares to SFRS, which Singapore-owned entities must comply, and what penalties apply for non-compliance.

Key Takeaways

- Ind AS is India's IFRS-converged framework with India-specific carve-outs that differ from SFRS

- Applicability depends on net worth and listing status — Singapore-owned subsidiaries face the same thresholds as Indian companies

- Three bodies govern Ind AS: ICAI formulates standards, MCA notifies them into law, and NFRA oversees compliance

- Key standards include Ind AS 110 (Consolidation), Ind AS 24 (Related Parties), Ind AS 115 (Revenue), and Ind AS 116 (Leases)

- Non-compliance triggers fines, director imprisonment, and reputational risk under the Companies Act, 2013

What Are Indian Accounting Standards (Ind AS)?

Indian Accounting Standards (Ind AS) are India's official accounting framework, notified by the Ministry of Corporate Affairs (MCA) under the Companies Act, 2013. Developed by the Institute of Chartered Accountants of India (ICAI), they govern how companies recognize, measure, present, and disclose financial transactions.

From Indian GAAP to Ind AS

India previously used Indian GAAP, its pre-IFRS framework. Ind AS was introduced through a phased rollout starting in 2016 as part of India's convergence with IFRS. Today, India runs a dual-standard system:

- Larger companies must use Ind AS

- Smaller entities may continue using the old AS framework

This differs from Singapore's single-framework approach where all reporting entities follow SFRS.

Active Standards

For Singapore businesses mapping their Indian operations against a known framework, the scope of Ind AS is worth understanding. India has notified 40 active Ind AS standards — Ind AS 11 on Construction Contracts was omitted after its scope was absorbed into Ind AS 115.

Key points about how these standards work in practice:

- Numbered to mirror their IFRS equivalents for easier cross-border comparison

- Contain India-specific carve-outs — for example, modifications to hedge accounting under Ind AS 109 and lease treatment under Ind AS 116

- Reflect local legal requirements under the Companies Act, 2013, which have no direct IFRS parallel

Who Governs Ind AS? The Regulatory Framework

Three key bodies oversee India's accounting standards:

ICAI (Institute of Chartered Accountants of India)

- Formulates standards through its Accounting Standards Board (ASB)

- Professional body representing India's chartered accountancy profession

NFRA (National Financial Reporting Authority)

- Established under the Companies Act 2013 to function independently of ICAI

- Oversees audit quality and recommends standards to MCA

- Has investigative and disciplinary powers over auditors and firms

MCA (Ministry of Corporate Affairs)

- Officially notifies standards, making them legally binding

- Issues implementation rules and clarifications

- Enforces compliance under the Companies Act, 2013

For Singapore businesses with listed Indian subsidiaries, there is an additional layer to navigate.

SEBI's Role for Listed Companies

The Securities and Exchange Board of India (SEBI) issues disclosure requirements for listed entities or companies planning to list on Indian exchanges. Singapore businesses with listed Indian subsidiaries must comply with both MCA's accounting rules and SEBI's presentation requirements when filing offer documents.

Ind AS vs. SFRS: Key Differences Singapore Businesses Must Understand

Foundational Similarity

Both SFRS and Ind AS converge with IFRS, sharing the same conceptual framework:

- Accrual accounting

- Fair value measurement

- Substance over form

This gives Singapore finance teams a useful starting point. That said, convergence is not the same as equivalence — the two frameworks diverge in ways that matter operationally.

India-Specific Carve-Outs

Ind AS contains carve-outs — intentional departures from IFRS driven by local regulatory, legal, or economic factors. Singapore businesses cannot assume their IFRS-compliant group policies will map cleanly to Ind AS.

Key examples:

- Ind AS 109 (Financial Instruments): Relaxes certain IFRS 9 hedge accounting requirements

- Ind AS 101 (First-Time Adoption): Offers a deemed cost approach on transition that differs from IFRS 1

- Treatment of foreign exchange differences: Specific carve-outs exist for long-term foreign currency monetary items

The Dual Reporting Challenge

A Singapore parent with an Indian subsidiary typically needs two sets of financials:

- Indian subsidiary's standalone Ind AS accounts (required by Indian law)

- SFRS-compliant consolidated accounts for the Singapore parent

Reconciling these two sets requires careful planning, particularly around:

- Deferred taxes (Ind AS 12)

- Employee benefits (Ind AS 19)

- Financial instruments (Ind AS 109)

Financial Year Misalignment

India mandates a financial year of April 1 to March 31 under the Companies Act, whereas Singapore companies commonly use January–December or other fiscal years.

This misalignment means:

- Indian subsidiaries close books and file on a different cycle

- Additional coordination needed for group consolidations

- Singapore finance teams must manage mid-year reporting for Indian entities

Foreign Exchange Accounting (Ind AS 21)

Ind AS 21 (Effects of Changes in Foreign Exchange Rates) is particularly relevant for Singapore businesses:

- Singapore-dollar transactions with the Indian subsidiary

- Inter-company loans denominated in SGD or other currencies

- Profit repatriation between Indian subsidiary and Singapore parent

Each of these must be accounted for under Ind AS 21, which can diverge from SFRS(I) 21 treatment in key respects. For India-based entities, functional currency determination under Ind AS 21 typically results in INR as the functional currency. This means all foreign currency transactions — including those with the Singapore parent — require translation accounting.

Ind AS Applicability: Which Singapore-Owned Companies Must Comply?

What Triggers Ind AS — It's Not Ownership

Ind AS applicability is NOT determined by ownership structure or parent company nationality. It is determined by the Indian entity's own net worth and listing status. A Singapore company's Indian subsidiary faces the same thresholds as any Indian company.

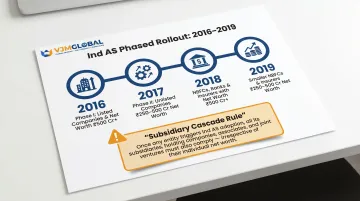

Phase I (Mandatory from April 1, 2016)

Applicable to:

- Companies with net worth of ₹500 crore or more

- Listed companies or companies in process of listing on Indian or overseas exchanges

Net worth for this threshold is calculated as:

- Standalone accounts as of March 31, 2014 (or first audited period after)

- Paid-up share capital plus reserves

- Less accumulated losses, deferred expenditure, and certain revaluation reserves

Phase II and Beyond

From April 1, 2017:

- Unlisted companies with net worth between ₹250 crore and ₹500 crore

From April 1, 2018:

- NBFCs, banks, and insurance companies with net worth of ₹500 crore or more

From April 2019:

- Smaller NBFCs (net worth ₹250–500 crore)

The Subsidiary Cascade Rule

Critical for Singapore holding structures: Once an Indian entity becomes subject to Ind AS, all of its subsidiaries, holding companies, associates, and joint ventures must also follow Ind AS — regardless of their individual net worth.

This can trigger Ind AS compliance for smaller Indian group entities that wouldn't otherwise meet the threshold on their own.

Voluntary Adoption

Companies below mandatory thresholds may voluntarily adopt Ind AS from April 1, 2015 onward. Important: Once adopted (voluntarily or mandatorily), a company cannot revert to the previous AS framework.

For Singapore businesses planning growth in India, early voluntary adoption can align reporting systems before mandatory deadlines arrive. Key considerations include:

- Assessing your Indian entity's current net worth against applicable thresholds

- Mapping which group entities fall under the subsidiary cascade rule

- Designing a transition roadmap before compliance becomes mandatory

VJM Global works with Singapore businesses navigating exactly these decisions — from threshold assessment to full transition planning for Indian entities.

Key Ind AS Standards Singapore Businesses Should Know

Ind AS 110 & 112: Consolidation and Disclosures

Ind AS 110 requires a parent to consolidate all entities it controls. For Singapore businesses:

- Indian subsidiaries must prepare standalone financial statements under Indian law

- Consolidation happens twice: at the Indian group level (Ind AS) and at the Singapore parent level (SFRS)

- Control assessments may differ between Ind AS 110 and SFRS 110

Ind AS 112 requires extensive disclosures about interests in subsidiaries, joint ventures, and associates — information that must appear in Indian statutory filings.

Ind AS 24: Related Party Disclosures

This standard requires extensive disclosure of transactions between the Indian entity and:

- Singapore parent company

- Fellow subsidiaries

- Key management personnel and their families

Common transactions requiring disclosure:

- Management fees

- Inter-company loans

- Service charges

- IP licensing fees

- Technical assistance payments

Compliance gap: Non-disclosure or under-disclosure of related party transactions is a frequent issue for foreign-owned entities in India. Singapore businesses often have regular inter-company arrangements that must be fully documented in the Indian subsidiary's financial statements.

Ind AS 115: Revenue Recognition & Ind AS 116: Leases

Ind AS 115 (aligned with IFRS 15) and Ind AS 116 (aligned with IFRS 16) apply in India with the same core principles Singapore businesses recognize from SFRS equivalents.

Key considerations:

- Follows the five-step revenue recognition model — the same framework Singapore businesses apply under SFRS 115

- Ind AS 116 took effect April 1, 2019, requiring lessees to recognize most leases on-balance-sheet

- India-specific implementation guidance applies to both; review ICAI materials for local interpretation

Ind AS 12: Income Taxes

Tax accounting adds another layer of complexity. Deferred tax positions under Ind AS 12 frequently diverge from what appears in Indian corporate tax returns — and those differences flow directly into the numbers your Indian subsidiary reports to Singapore. Key areas to watch:

- Cross-border profit repatriation structures

- Transfer pricing arrangements

- Tax incentive structures in India (such as SEZ benefits)

- Recognition of deferred tax assets and liabilities

Unrecognized deferred tax assets — common where future profitability is uncertain — can materially understate the Indian entity's balance sheet value at consolidation.

Navigating Ind AS Compliance as a Singapore Business

Practical Compliance Obligations

Singapore-owned Indian entities must:

Statutory Requirements:

- Appoint a qualified statutory auditor (Indian Chartered Accountant)

- Prepare standalone financial statements under Ind AS within prescribed timelines

- File financials with the Registrar of Companies (ROC)

- Obtain board-level approvals

- Maintain books of accounts under the Companies Act, 2013

Filing Deadlines:

- Financial statements must be filed with ROC within 30–60 days of the Annual General Meeting

- AGM must be held within six months of financial year-end (i.e., by September 30 for an April–March year)

Penalties for Non-Compliance

The Companies Act, 2013 provides for serious penalties:

Under Section 128 (Books of Account):

- Officers in default face fines and imprisonment

Under Section 137 (Filing of Financial Statements):

- Companies face fines of ₹1,000 per day of default

- Officers in default may face fines up to ₹5 lakh and imprisonment

Non-financial consequences:

- Inability to repatriate profits

- Difficulty securing future FDI approvals

- Reputational damage

- Operational disruptions

Managing Compliance from Singapore

Managing Ind AS compliance remotely from Singapore is challenging due to:

- Complexity of Indian regulatory requirements

- April–March financial year cycle misalignment

- Need for locally qualified Chartered Accountant sign-off

- Coordinating document sign-offs across time zones and local deadlines

These challenges are manageable with the right local partner. VJM Global supports foreign-owned Indian entities across bookkeeping, Ind AS-compliant financial statement preparation, and ROC filings — so Singapore businesses stay compliant without building a full in-house finance function in India.

Frequently Asked Questions

Which accounting standards are used in India?

India uses two parallel frameworks: the older Indian GAAP (Accounting Standards, or AS) for smaller companies, and the newer Ind AS (Indian Accounting Standards) for larger companies meeting net worth or listing thresholds. Ind AS is India's IFRS-converged framework notified by MCA.

Does India use GAAP, Ind AS, or IFRS?

India uses its own framework — Ind AS — which is converged with (but not identical to) IFRS. Full IFRS is not directly applicable in India. Smaller companies still use Indian GAAP (the older AS standards), unlike Singapore, where SFRS(I) mirrors IFRS word-for-word.

Who issues accounting standards in India?

ICAI's Accounting Standards Board (ASB) formulates the standards, NFRA recommends them to the Ministry of Corporate Affairs (MCA), and MCA officially notifies them under the Companies Act, 2013, making them legally binding.

Is Ind AS 115 the same as IFRS 15?

Ind AS 115 follows the same five-step model as IFRS 15 (Revenue from Contracts with Customers), with minor India-specific modifications. Singapore businesses familiar with SFRS 115 will find the principles familiar but should verify any local ICAI guidance before applying them.

How many accounting standards are there in India?

MCA has notified 40 active Ind AS standards (Ind AS 11 on Construction Contracts was omitted). Separately, ICAI has issued 31 older Accounting Standards (AS) that still apply to companies not subject to mandatory Ind AS.

How is NFRA different from ICAI?

ICAI (a statutory professional body) formulates accounting and auditing standards and regulates the CA profession, while NFRA (established under the Companies Act, 2013) is an independent government authority that oversees audit quality for large companies and can investigate and penalize auditors.