Introduction

Singapore's status as Asia's premier financial hub is undeniable. In 2024 alone, the Singapore Economic Development Board secured S$13.5 billion in fixed asset investment commitments, and the city-state now hosts regional headquarters for approximately 4,200 multinational firms — far surpassing Hong Kong's 1,336. With 628,081 registered business entities as of April 2026 and consistent monthly formations of 5,400-7,400 new companies, Singapore remains an irresistible destination for foreign businesses.

Yet navigating Singapore's accounting standards is non-negotiable for every business operating there. The core challenge most foreign companies face is a deceptively simple question: which framework applies to your entity? Singapore operates three distinct financial reporting frameworks — FRS (SFRS), SFRS(I), and SFRS for Small Entities — each with different eligibility criteria, compliance obligations, and technical requirements.

Non-compliance isn't just a paperwork issue. Penalties escalate from S$300 late fees to director disqualification, court prosecution up to S$5,000, and ultimately striking off the company register.

What follows covers the full landscape: which framework applies to your business type, how SFRS stacks up against IFRS and US GAAP, and the compliance obligations you can't afford to miss.

Key Takeaways

- Singapore uses three frameworks: FRS (private companies), SFRS(I) (SGX-listed firms, aligned to IFRS), and SFRS for Small Entities (qualifying smaller businesses)

- Standards are issued by the ASC under ACRA; the applicable framework is determined by entity type and size, and compliance is mandatory for all

- SFRS(I) mirrors IFRS almost exactly; FRS is broadly converged with IFRS but includes local adaptations for smaller entities

- Non-compliance triggers financial penalties (S$300–S$5,000), director disqualification after three convictions, and striking off for persistent non-filing

- Annual return filing deadlines are now measured from financial year-end (5–7 months depending on entity type), not from AGM date

Understanding Singapore's Accounting Standard Landscape

Historical Evolution: From SAS to SFRS(I)

Singapore's accounting standards journey reflects its broader economic strategy: global integration. The framework began as Singapore Accounting Standards (SAS), issued by the Institute of Certified Public Accountants of Singapore (ICPAS).

In 2003, Singapore rebranded the framework as Financial Reporting Standards (FRS), closely modelling it after International Financial Reporting Standards (IFRS). That shift reflected Singapore's determination to position itself as a transparent, investor-friendly hub where local financial statements could be compared directly with global peers.

By 2018, Singapore completed convergence with the introduction of SFRS(I) — Singapore Financial Reporting Standards (International) — mandatory for all SGX-listed companies for periods beginning on or after January 1, 2018. This framework is described by the IFRS Foundation as "identical to IFRS Standards," enabling companies to assert dual compliance.

The Accounting Standards Committee (ASC)

The Accounting Standards Act became effective on November 1, 2007, establishing the Accounting Standards Council to issue standards for companies, charities, co-operative societies, and societies.

On April 1, 2023, a major reform consolidated the Accounting Standards Council, Singapore Accountancy Commission, and ACRA into a single regulator. The Council was reconstituted as the Accounting Standards Committee (ASC) under ACRA, streamlining standard-setting and enforcement under one authority.

The ASC cannot provide individual application advice — its mandate is to issue frameworks, not interpret them for specific entities.

Legal Mandate: Non-Compliance Is Not Optional

Section 201 of the Companies Act imposes a clear obligation: all Singapore-incorporated companies and Singapore branches of foreign firms must prepare financial statements that comply with Accounting Standards and give a true and fair view. This obligation applies regardless of company size, industry, or revenue. Dormant companies meeting Section 201A criteria may be exempt, but active entities cannot opt out.

Four Active Frameworks

| Framework | Mandatory For | Key Characteristic |

|---|---|---|

| SFRS(I) | SGX-listed companies (from Jan 1, 2018) | Identical to IFRS; dual compliance assertion possible |

| FRS (SFRS) | Non-listed Singapore-incorporated companies | Default framework; ~40 standards converged with IFRS |

| SFRS for Small Entities | Qualifying small non-publicly-accountable entities | Simplified reporting based on IFRS for SMEs |

| Charities Accounting Standard | Eligible charities (alternative to FRS) | Sector-specific framework for non-profits |

Financial Reporting Surveillance Programme (FRSP)

ACRA runs an active enforcement mechanism: the Financial Reporting Surveillance Programme, which reviews selected financial statements for compliance quality. Since 2015, ACRA has published five FRSP reports (most recently in 2024), providing public guidance on common errors and compliance expectations. Companies whose statements are reviewed may face follow-up queries, restatements, or referrals for further regulatory action.

The Three Main Financial Reporting Frameworks Explained

Financial Reporting Standards (FRS)

FRS is the default framework for non-listed Singapore-incorporated companies. It comprises approximately 40 standards and over 20 interpretations, each numbered to correspond with IFRS equivalents.

Three standards have the most practical impact on day-to-day reporting:

FRS 109 (Financial Instruments)

This standard replaced IAS 39 and introduced a three-stage expected credit loss (ECL) model for impairment. Companies assess credit risk at initial recognition and recognize lifetime expected losses only when that risk increases significantly — unlike US GAAP's CECL model, which requires lifetime loss recognition from day one.

FRS 115 (Revenue from Contracts with Customers)

A five-step model governs revenue recognition: identify the contract, identify performance obligations, determine the transaction price, allocate that price to each obligation, and recognize revenue when obligations are satisfied. FRS 115 is principles-based with fewer bright-line rules than US GAAP's ASC 606 — companies apply judgment, not prescriptive thresholds.

FRS 116 (Leases)

Eliminates the operating/finance lease distinction for lessees, bringing all leases onto the balance sheet. This produces higher EBITDA for companies with significant lease portfolios (since lease expense is split between depreciation and interest) — a material difference from pre-FRS 116 reporting and a key divergence from older frameworks.

Singapore Financial Reporting Standards (International) — SFRS(I)

Introduced in 2017 and mandatory for all SGX-listed companies from January 1, 2018, SFRS(I) is effectively equivalent to IFRS as issued by the IASB. Differences are minimal — companies applying SFRS(I) may assert compliance with both IFRS and Singapore frameworks simultaneously.

SFRS(I) is the framework of choice for:

- SGX-listed companies (mandatory)

- Non-listed companies with significant cross-border operations

- Subsidiaries of foreign parents reporting under IFRS

- Companies planning future IPOs on international exchanges

Non-listed companies may voluntarily adopt SFRS(I) if it simplifies group consolidation reporting.

SFRS for Small Entities

Eligibility Criteria

To qualify for SFRS for Small Entities, a company must meet at least 2 out of 3 thresholds for 2 consecutive prior years and must not be publicly accountable:

- Total annual revenue not exceeding S$10 million

- Total gross assets not exceeding S$10 million

- Not more than 50 employees

Publicly accountable entities are ineligible, including:

- Public companies under the Companies Act

- Listed entities or those issuing securities publicly

- Banks, insurance companies, securities brokers, or mutual funds

- Charities under the Charities Act

A newly incorporated company is eligible in its first two years provided it is not publicly accountable.

Key Benefits and Trade-Offs

SFRS for Small Entities simplifies reporting by reducing disclosure requirements and relaxing recognition and measurement rules. For qualifying businesses, this means:

- Lower compliance costs

- Fewer detailed note disclosures

- Simplified accounting policies

Before adopting this framework, weigh these trade-offs:

- IPO plans disqualify eligibility — switching frameworks mid-way adds transition costs

- Banks and lenders often require full SFRS statements for creditworthiness assessments

- Moving from full SFRS to SFRS for SE requires staff retraining and software adjustments

- Subsidiaries should align with their parent's framework to simplify group consolidation

Charities Accounting Standard

Singapore's Charities Accounting Standard is issued by the ASC and governed by the Office of the Commissioner of Charities. It addresses unique accounting considerations for registered charities, including fund accounting, donation disclosures, and restricted vs unrestricted fund classification. Registered charities can choose between this framework and FRS — confirm your eligibility with the Commissioner of Charities before selecting an approach.

Key Principles of Singapore Financial Reporting Standards

All SFRS-family frameworks are built on the IASB Conceptual Framework for Financial Reporting. Understanding these core principles is essential for compliance:

Accrual Basis of Accounting Transactions are recorded when they occur, not when cash changes hands. Revenue is recognized when earned and expenses when incurred, regardless of payment timing. This applies to all financial statements except the statement of cash flows.

Fair Presentation and Going Concern Financial statements must reflect economic reality, not just legal form. Section 201(15) of the Companies Act requires directors to state whether there are reasonable grounds to believe the company can pay its debts as they fall due. This embeds the going concern assumption directly into statutory obligations.

Consistency Switching accounting policies year to year distorts comparability and misleads readers. FRS 1 / SFRS(I) 1-1 requires retrospective application and full disclosure when any policy change does occur.

Qualitative Characteristics

| Characteristic | Meaning |

|---|---|

| Relevance | Information must be capable of making a difference to decisions — materiality matters |

| Faithful Representation | Financial statements must reflect the economic substance, not just legal form |

| Verifiability | Disclosures must allow readers to confirm how figures were derived through audit trails |

| Understandability | Complex transactions must be explained clearly, even when technical |

| Comparability | Financial statements must be prepared consistently to allow comparison across periods and entities |

Completeness Financial statements must capture all material transactions. Singapore's deliberate convergence with IFRS, rather than maintaining standalone national standards, reinforces this requirement: consistent presentation makes Singapore-listed companies easier to evaluate alongside peers in London, Tokyo, or New York.

SFRS vs IFRS: What Foreign Businesses Need to Know

The Core Relationship

SFRS(I) is described by the IFRS Foundation as "identical to IFRS Standards" — companies applying SFRS(I) can assert compliance with both frameworks. FRS (SFRS) is substantially converged with IFRS, meaning companies with international operations or cross-border investors can largely rely on existing IFRS knowledge. But distinctions remain, and they matter.

Key Differences Between FRS and IFRS

| Area | Nature of Difference | Impact |

|---|---|---|

| IFRIC 2 | Not adopted in Singapore | No effect on Singapore-incorporated companies |

| IFRS 10 / IAS 28 modifications | Consolidation/equity method exemptions differ | Affects non-listed companies only |

| IFRIC 15 Accompanying Note | Additional guidance for property development agreements | Singapore-specific real estate provision |

| SFRS for Small Entities | Singapore-specific eligibility (S$10M thresholds, 2-year test) | No direct IFRS equivalent with identical scope |

| MAS Notice 612 | Modified loan loss provisioning for banks | Sector-specific (banks regulated by MAS) |

SFRS vs US GAAP: Critical Conceptual Differences

Many foreign businesses entering Singapore come from the US market. Three areas require close attention:

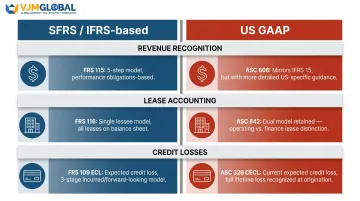

- Revenue Recognition (FRS 115 vs ASC 606): Both use a five-step model, but IFRS 15 is more judgment-based with fewer bright-line rules. US GAAP adds specific guidance for licensing, returns, and variable consideration.

- Lease Accounting (FRS 116 vs ASC 842): FRS 116 mandates a single lessee model — all leases on balance sheet. US GAAP retains dual classification (finance vs operating), which affects expense patterns and EBITDA reporting.

- Credit Losses (FRS 109 vs ASC 326): FRS 109 uses a three-stage expected credit loss (ECL) model, recognizing lifetime losses only when credit risk increases significantly. ASC 326 (CECL) requires lifetime expected losses from day one, front-loading recognition more aggressively.

Practical Guidance for Multinationals

Companies with a Singapore entity that is part of a global group often need dual reporting: SFRS-compliant financial statements locally while consolidating into IFRS or US GAAP at the group level. The process typically involves four steps:

- Prepare local statutory accounts under the applicable Singapore framework (FRS or SFRS(I))

- Prepare reconciliation adjustments for group consolidation (e.g., CECL vs ECL differences, lease classification)

- Add additional disclosures required by the parent's home framework but not by Singapore standards

- Train local finance staff on both frameworks to manage the reporting burden efficiently

Cross-border groups with Singapore subsidiaries should assess these differences early in their setup process — reconciliation gaps between SFRS and the group's home framework are easier to manage when systems and workflows are designed with them in mind from the start.

Compliance Requirements, Filing Obligations, and Penalties

Annual Reporting Obligations

All Singapore companies must prepare financial statements annually, hold an AGM, and file annual returns with ACRA. Key deadlines:

| Company Type | AGM Deadline | Annual Return Filing Deadline |

|---|---|---|

| Listed companies | Within 4 months after FYE | Within 5 months after FYE |

| Listed (with overseas branch register) | Within 4 months after FYE | Within 6 months after FYE |

| Non-listed companies | Within 6 months after FYE | Within 7 months after FYE |

| Non-listed (with overseas branch register) | Within 6 months after FYE | Within 8 months after FYE |

Critical Update: These deadlines are measured from financial year-end (FYE), not from AGM date. The previous formulation of "within one month of AGM" has been superseded.

Required Components of Financial Statements

Under Section 201 of the Companies Act and FRS 1:

- Statement of comprehensive income (profit and loss account)

- Statement of financial position (balance sheet)

- Statement of cash flows

- Statement of changes in equity

- Notes to financial statements, including accounting policies

- Directors' statement on true and fair view and solvency (signed by two directors)

XBRL Filing Requirements

Most Singapore-incorporated companies must file financial statements in XBRL format:

- Full XBRL: Most companies

- Simplified XBRL: Companies with revenue and assets each not exceeding S$500,000

- XBRL FSH: Banks and insurance companies

- Exempt (PDF only): Companies limited by guarantee; foreign companies with Singapore branches; companies using non-ASC standards (with ACRA approval)

Regulatory Bodies

Three key regulators oversee compliance:

- ACRA — Primary enforcer for accounting standards. Administers the Financial Reporting Surveillance Programme, processes annual return filings, and initiates prosecution for non-compliance.

- IRAS — Administers corporate income tax (filing due November 30 annually), GST, and withholding tax. Issues estimated Notices of Assessment when returns are not filed.

- SGX — Listed companies face additional governance requirements under the Code of Corporate Governance 2018, including Board oversight of financial reporting and a mandatory Audit Committee.

Penalties for Non-Compliance

| Penalty Type | Amount | Trigger |

|---|---|---|

| Late lodgement (up to 3 months) | S$300 | Late annual return filing |

| Late lodgement (more than 3 months) | S$600 | Late annual return filing |

| Composition sum | At least S$500 per breach | Out-of-court settlement |

| Court prosecution | Up to S$5,000 per charge | Conviction |

| Director disqualification | 5-year ban | 3+ filing convictions within 5 years |

| Striking off | Company removed from register | Repeated years of non-filing |

IRAS Penalties for Late/Non-Filing of Corporate Tax Returns

- Composition amount: Up to S$5,000 per offence

- Court conviction (failure to file for 2+ years): penalty of twice (2x) the amount of tax assessed, plus a fine of up to S$5,000

- Section 65B(3) notice to directors: failure to comply may result in a fine of up to S$10,000 and/or imprisonment of up to 12 months

A S$300 late-filing fee is manageable. Director disqualification is not. These penalties can escalate from an administrative fine to a 5-year ban within months if the initial breach goes unaddressed. Foreign businesses new to Singapore's enforcement environment often benefit from working with an accounting partner experienced in cross-border compliance — VJM Global, for instance, supports foreign companies navigating Singapore and Indian regulatory obligations through outsourced accounting and financial reporting services.

Frequently Asked Questions

Which accounting standards are used in Singapore?

Singapore uses three main frameworks issued by the Accounting Standards Committee (ASC): FRS (for most private companies), SFRS(I) (for SGX-listed companies, equivalent to IFRS), and SFRS for Small Entities (for qualifying smaller private businesses). A separate Charities Accounting Standard applies to eligible non-profit organisations.

Who issues accounting standards in Singapore?

Accounting standards are issued by the Accounting Standards Committee (ASC), a statutory body that operates under ACRA (Accounting and Corporate Regulatory Authority). The ASC formulates and reviews standards but does not provide individual application advice.

What is the difference between SFRS and IFRS?

SFRS (FRS) is modelled on IFRS but includes local adaptations, most notably the SFRS for Small Entities framework, and may have different effective dates for some standards. SFRS(I), used by SGX-listed companies, is substantially identical to IFRS and permits dual compliance assertion.

Is IFRS or GAAP better?

For businesses in Singapore, the relevant question is which framework applies locally: SFRS or SFRS(I) is the legal requirement, regardless of a parent company's home standards. IFRS is principles-based and globally widespread; US GAAP is rules-based and mandatory for US public companies. Neither applies directly in Singapore.

Is ACCA still recognised in Singapore?

Yes, ACCA qualifications are recognised in Singapore and members can practise accountancy there. Singapore's own professional body, the Institute of Singapore Chartered Accountants (ISCA), awards the CA (Singapore) designation and offers an Enhanced Pathway specifically for ACCA Members and Affiliates.