Introduction

Singapore companies operating in India face a compliance burden that looks nothing like ACRA back home. Regardless of your entity structure, Indian authorities require mandatory financial statement filings under two separate legal frameworks: the Companies Act, 2013 (Ministry of Corporate Affairs / Registrar of Companies) and the Foreign Exchange Management Act (FEMA), 1999 (Reserve Bank of India).

Most Singapore companies underestimate what this means in practice. Three realities catch finance teams off guard:

- Financial year mismatch: India mandates an April–March year, creating reconciliation headaches for Singapore parents on a January–December calendar

- AOC-4 filing window: Miss the 30-day deadline after your Annual General Meeting and penalties start at ₹10,000 plus ₹100 per day — with personal director liability

- FEMA's separate track: The Foreign Liabilities and Assets (FLA) Return is due July 15 each year; non-compliance can trigger penalties up to three times the investment amount

This guide breaks down exactly what to file, when to file it, and what's at stake if deadlines slip.

Key Takeaways

- Financial statements must be filed with the ROC using Form AOC-4 within 30 days of the AGM (typically by late October)

- FLA Return with RBI is due July 15 for every Indian entity that received FDI from Singapore

- XBRL filing becomes permanent once your subsidiary reaches ₹5 crore paid-up capital or ₹100 crore turnover

- Miss a deadline and you face a ₹10,000 base penalty plus ₹100/day — capped at ₹2 lakh for the company and ₹50,000 for directors

- India's mandatory April–March financial year doesn't align with Singapore's flexible year-end — plan your reporting calendar accordingly

Financial Statement Filing Requirements for Singapore Companies in India

Every company incorporated in India—including wholly owned subsidiaries of Singapore companies—must comply with Section 129 and Section 137 of the Companies Act, 2013. Section 129 mandates preparation of financial statements that "give a true and fair view" and comply with Indian Accounting Standards. Section 137 requires filing these statements with the ROC within 30 days of the AGM.

This obligation applies regardless of your parent company's location. Whether you're headquartered in Singapore, London, or Sydney, your Indian subsidiary follows Indian law.

Which Entity Types Are Covered

Private Limited Companies must file Form AOC-4 with the ROC. This is the most common structure for Singapore market entrants, and the filing covers:

- Balance Sheet as of March 31

- Profit & Loss Account for the financial year

- Cash Flow Statement (except for One Person Companies and small companies)

- Statement of Changes in Equity

- Auditor's Report

- Board's Report

Branch Offices and Liaison Offices operate on a separate compliance track. These are not incorporated entities, so they file under Sections 380-381 of the Companies Act rather than through Form AOC-4.

They also carry distinct FEMA/RBI reporting obligations. If you've set up a BO or LO instead of a subsidiary, your filing requirements differ significantly from everything described above.

Financial Statement Preparation Standards

Once you know your entity type, the next question is which accounting standard applies. Your Indian subsidiary's accounts must follow one of two frameworks:

- Indian Accounting Standards (Ind AS) — applicable to larger companies and those with listed debt or equity

- Companies (Accounting Standards) Rules, 2006 — applicable to smaller, unlisted companies

The format prescribed in Schedule III of the Companies Act (which governs how financial statements must be structured and presented) is mandatory for both. Singapore FRS or IFRS formats are not accepted for Indian statutory filings.

Key MCA Forms for Filing Financial Statements

The Ministry of Corporate Affairs uses different AOC-4 variants depending on company size, subsidiary structure, and accounting standards. Selecting the wrong form leads to rejection and restarts the penalty clock.

Form AOC-4 (Standard)

This is your primary form for standalone financial statements. It packages:

- All financial statements listed above

- Auditor's Report signed by a practicing CA

- Director's Report covering operations, governance, and material changes

Filing deadline: 30 days from the AGM date (not from the financial year end).

Form AOC-4 CFS (Consolidated Financial Statements)

If your Indian subsidiary itself holds sub-subsidiaries (Indian or foreign), you must file consolidated financial statements using AOC-4 CFS. This is in addition to—not a replacement for—the standalone AOC-4.

Common mistake: Singapore groups with multi-tier structures in India often file only the standalone statements and miss the CFS requirement entirely.

Form AOC-4 XBRL

For companies that meet certain thresholds, a third layer applies: XBRL tagging. XBRL (Extensible Business Reporting Language) filing is mandatory for:

- All listed companies and their Indian subsidiaries

- Companies with paid-up capital ≥ ₹5 crore

- Companies with turnover ≥ ₹100 crore

- Companies required to follow Ind AS

Critical rule: Once XBRL applies, it stays mandatory permanently—even if capital or turnover later falls below the threshold. Many Singapore subsidiaries cross the ₹5 crore capital mark at initial funding and unknowingly trigger a lifelong XBRL obligation.

XBRL preparation requires specialized tagging software — Iris, Webtel, and DataTracks are widely used — plus validation through the MCA's official tool. Allow 3–5 extra business days and factor in additional professional fees when XBRL applies.

Form MGT-7 / MGT-7A (Annual Return)

The Annual Return is a separate but mandatory filing — distinct from financial statements but filed on the same compliance calendar:

- MGT-7 for most companies (due 60 days from AGM)

- MGT-7A for small companies and OPCs (simplified version)

This form discloses shareholders, directors, and beneficial ownership. Your Singapore parent company and its nominated directors appear here, making accuracy essential for compliance and beneficial ownership disclosures.

Filing Deadlines, Fees, and Penalties

AGM-Linked Timeline

India's filing system chains to the Annual General Meeting:

Step 1: Hold AGM within 6 months of financial year end → By September 30 for April–March companies.

Step 2: File AOC-4 within 30 days of AGM → Outer limit October 29-30.

Step 3: File MGT-7 within 60 days of AGM → Outer limit November 29-30.

Exception: One Person Companies get 180 days from March 31 (until September 27) for AOC-4, bypassing the AGM requirement.

Practical implication: If your subsidiary delays its AGM to September 15 (common when audits run late), your AOC-4 deadline moves to October 15. But penalties begin accruing from the original deadline if the delay wasn't formally approved.

Government Filing Fees

| Authorized Share Capital | Fee Per Document |

|---|---|

| No share capital / < ₹1,00,000 | ₹200 |

| ₹1,00,000 to ₹4,99,999 | ₹300 |

| ₹5,00,000 to ₹24,99,999 | ₹400 |

| ₹25,00,000 to ₹99,99,999 | ₹500 |

| ₹1,00,00,000 or more | ₹600 |

Foreign subsidiaries with capital above ₹1 crore typically pay ₹600 per document — separate from CA/CS professional fees.

Late Filing Penalty Structure

Additional fee: ₹100 per day from the due date (no maximum cap during the delay period).

Section 137 penalties (post-2020 Amendment Act):

| Party | Base Penalty | Continuing Penalty | Maximum Cap |

|---|---|---|---|

| Company | ₹10,000 | ₹100/day | ₹2,00,000 |

| Directors | ₹10,000 | ₹100/day | ₹50,000 |

Note that earlier versions of the Companies Act prescribed penalties up to ₹10 lakh for companies and ₹5 lakh for directors. The 2020 Amendment decriminalized Section 137 and reduced these caps significantly — the table above reflects current law.

Personal liability risk: Singapore-based directors on Indian subsidiary boards are personally liable for filing defaults. "Officers in default" includes the Managing Director, CFO, or Board-designated director—or all directors if no one is specifically designated.

Who Must Sign AOC-4

The form requires:

- Digital signature of a Director (using DIN)

- Certification by a practicing Chartered Accountant, Company Secretary, or Cost Accountant holding a Certificate of Practice

Singapore companies must ensure they have a designated director with a valid DIN and a locally registered CA/CS in place before the filing season begins. VJM Global's practicing Chartered Accountants can handle AOC-4 certification for foreign-owned subsidiaries, so filings stay on schedule regardless of your team's location.

FEMA Compliance: Additional Reporting for Singapore Parent Companies

FEMA obligations run parallel to Companies Act filings: separate deadlines, separate penalties, separate portals. Missing either track creates compounding risk.

Foreign Liabilities and Assets (FLA) Return

Who must file: Every Indian entity that has received FDI (which includes all Indian subsidiaries of Singapore companies) must file the FLA Return with the RBI.

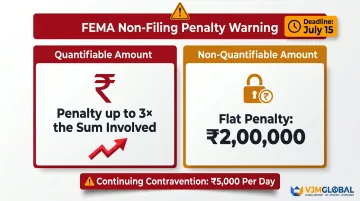

Deadline: July 15 each year for the position as of March 31.

Portal: FLAIR (Foreign Liabilities and Assets Information Reporting) at https://flair.rbi.org.in

Content: The return captures:

- Outstanding FDI equity received from the Singapore parent

- External Commercial Borrowings (if any)

- Trade credits and guarantees

- Overseas Direct Investment made by the Indian subsidiary

Penalty for non-filing: Up to three times the sum involved under Section 13 of FEMA, or ₹2,00,000 if the amount is not quantifiable. Continuing contraventions attract ₹5,000 per day.

Critical timing note: July 15 is the earliest major annual compliance deadline—far earlier than the October AOC-4 deadline. Missing it attracts the most severe penalties in the entire compliance calendar.

Annual Performance Report (APR)

Who must file: If your Indian subsidiary has made Overseas Direct Investment (invested in entities outside India), you must submit Form ODI Part II (Annual Performance Report) for each foreign entity.

Deadline: December 31 each year, covering the foreign entity's accounting period ending on or before the preceding March 31.

Submission route: Through your Authorised Dealer (AD) Category-I bank.

When this applies: Singapore-headquartered groups with multi-country structures trigger this requirement. For example, a Singapore parent → Indian subsidiary → Southeast Asian step-down subsidiary means the Indian entity must file an APR reporting on that downstream investment's performance.

Late submission fee: ₹7,500 per return, plus potential FEMA contravention penalties.

Managing both tracks is harder than it sounds. The FLA Return (RBI), AOC-4 (MCA), and APR (through your AD bank) fall under three different regulatory authorities with no shared deadline coordination. VJM Global maintains an integrated compliance calendar covering all FEMA and Companies Act obligations for foreign-owned Indian entities — so deadlines across all three frameworks are tracked together, not in isolation.

Common Mistakes and Practical Tips for Singapore Companies

Financial Year Mismatch

India mandates an April 1 – March 31 financial year for all incorporated entities. Singapore companies can choose any year-end — and that gap creates a recurring timing problem:

- Your Singapore group may consolidate on a December 31 year-end

- Your Indian subsidiary must close accounts on March 31

- Group consolidation requires either interim reporting from India (as of December 31) or a three-month lag in consolidating the Indian entity's audited accounts

Plan audit calendars 3-4 months in advance. If your Singapore audit closes in February for a December year-end, your Indian audit runs May–June for the March year-end — a completely different timeline. Coordinate with both audit teams before the financial year begins, not after.

Unadopted vs. Adopted Financial Statements

If financial statements are not formally adopted at the AGM — due to a qualified audit opinion, shareholder dispute, or procedural issue — they must still be filed within 30 days as "unadopted" statements. Once adopted at a subsequent meeting, the adopted version must be re-filed.

Singapore companies unfamiliar with this distinction often wait until adoption is complete, missing the interim 30-day deadline and triggering penalties in the process. VJM Global tracks AGM outcomes and handles both the initial unadopted filing and the re-filing once adoption occurs — so nothing falls through the gap.

Overlooking XBRL Applicability

Subsidiaries that cross the ₹5 crore paid-up capital or ₹100 crore turnover threshold mid-year often continue filing standard AOC-4 — unaware that XBRL is now mandatory. The result: filed forms are rejected, and by the time the error is caught and corrected, additional late fees have already accumulated.

Review XBRL applicability at the start of each financial year, particularly if you've recently capitalized the subsidiary or seen significant revenue growth. XBRL preparation takes 2-3 additional weeks for tagging and validation — catching the requirement late leaves very little room to course-correct.

Frequently Asked Questions

Where do companies file their financial statements in India?

Financial statements are filed electronically with the Registrar of Companies through the MCA21 portal at mca.gov.in, managed by the Ministry of Corporate Affairs. FLA Returns are filed separately with the RBI via the FLAIR portal—a distinct submission that Singapore parent companies must also track.

Who is required to file financial statements in India?

Every company incorporated under the Companies Act, 2013—including wholly owned subsidiaries and joint ventures of Singapore companies—must file financial statements. Filing requirements apply regardless of whether the entity is profitable or operational during the year.

For which companies is XBRL filing mandatory in India?

XBRL filing (Form AOC-4 XBRL) is mandatory for all companies listed on Indian stock exchanges and their subsidiaries, companies with paid-up capital ≥ ₹5 crore, companies with turnover ≥ ₹100 crore, and companies required to follow Ind AS. Once triggered, the obligation is permanent.

What is the due date for filing AOC-4 in India?

AOC-4 must be filed within 30 days of the AGM. Since the AGM must be held by September 30 for April–March companies, the standard deadline falls around October 29-30 each year. One Person Companies have an extended deadline of 180 days from March 31 (September 27).

What are the penalties for not filing financial statements in India?

A late additional fee of ₹100 per day applies from the due date. Section 137 prosecution can result in penalties of ₹10,000 + ₹100/day—capped at ₹2 lakh for the company and ₹50,000 for directors personally.

Does a Singapore company's branch office in India need to file financial statements differently?

Yes. Branch Offices are not incorporated entities and file under Sections 380-381 of the Companies Act, not the AOC-4 route. They must submit audited accounts of their Indian operations and the parent company's consolidated statements to the ROC, plus an Annual Activity Certificate to their AD bank under FEMA.

Singapore companies managing Indian subsidiaries must track overlapping MCA and FEMA deadlines across multiple forms—AOC-4, MGT-7, and FLA Returns—each with separate portals and timelines. VJM Global's team of Chartered Accountants, Company Secretaries, and FEMA specialists has handled this compliance framework for foreign-owned Indian entities for 30+ years. Contact us at info@vjmglobal.com to discuss your filing obligations.