Introduction

Singapore accounts for approximately 24% of total FDI into India (around USD 174.886 billion over 25 years) and 27.83% of India's trade with ASEAN as of 2024-25. That corridor runs both ways. Thousands of Indian companies now operate Singapore subsidiaries, branches, or holding companies to access Southeast Asian markets, benefit from its business-friendly tax regime, and build international credibility.

What many Indian finance teams underestimate is that Singapore runs its own Singapore Financial Reporting Standards (SFRS) — closely modelled on IFRS but meaningfully different from India's Ind AS framework. The gap matters in practice.

Non-compliance is not a paperwork inconvenience. ACRA's Financial Reporting Surveillance Programme actively reviews financial statements, and penalties range from composition fines to court summons and director arrest warrants.

This guide covers Singapore's three financial reporting frameworks, key compliance timelines, penalties for non-compliance, and a practical comparison with Indian accounting standards to help Indian businesses manage dual-jurisdiction reporting without costly errors.

TLDR

- Singapore companies must follow Singapore Financial Reporting Standards (SFRS), mandatory for fiscal periods beginning after 1 January 2003

- Three frameworks apply: full SFRS (default), SFRS(I) (mandatory for SGX-listed companies from 2018), and SFRS for Small Entities (qualifying private businesses only)

- Financial statements require accrual accounting and annual ACRA filing; most companies need statutory audits

- Indian businesses face dual compliance: Ind AS for the Indian parent, SFRS for the Singapore entity — with key differences in revenue recognition, leases, and financial instruments

What Are Singapore Accounting Standards?

Singapore's accounting standards are called the Singapore Financial Reporting Standards (SFRS), formulated by the Accounting Standards Committee (ASC) and enforced by the Accounting and Corporate Regulatory Authority (ACRA). SFRS is closely modelled on the International Financial Reporting Standards (IFRS), with the intent to achieve full convergence over time.

For Indian businesses already familiar with Ind AS (which is also IFRS-converged), SFRS will feel familiar in structure. That said, "converged" does not mean "identical": both Ind AS and SFRS carry jurisdiction-specific carve-outs and modifications that create reconciliation requirements for cross-border entities.

Here's what Indian businesses need to know about SFRS at a glance:

- Comprises approximately 41 active standards covering distinct accounting topics—inventories, leases, employee benefits, revenue recognition, financial instruments, and consolidated accounts

- Applies to all Singapore-incorporated companies and Singapore branches of foreign firms (including Indian companies) for financial periods beginning on or after January 1, 2003

- Compliance is mandatory, not optional—failure to comply triggers ACRA enforcement action

Regulatory Bodies at a Glance

Two key bodies govern Singapore's financial reporting ecosystem:

Accounting Standards Committee (ASC):

- Develops and issues all Singapore accounting standards (SFRS, SFRS(I), SFRS for Small Entities, Charities Accounting Standard)

- Conducts public consultations before finalising new standards

- Does not perform enforcement

Accounting and Corporate Regulatory Authority (ACRA):

- Enforces compliance with accounting standards under the Companies Act

- Administers the Financial Reporting Surveillance Programme (FRSP), which selects and reviews financial statements for compliance

- Issues enquiry letters, findings letters, warning letters, composition fines, and court summons for non-compliance

- As of August 2025, FRSP scope expanded to include SGX-listed business trusts, REITs, and foreign-incorporated companies

Singapore's Three Financial Reporting Frameworks

Singapore offers three distinct financial reporting frameworks. The right one for your Singapore entity depends on listing status, company size, and public accountability — and choosing incorrectly creates consolidation headaches later.

| Framework | Applies To | Effective Date | IFRS Relationship |

|---|---|---|---|

| Full SFRS (FRS) | All Singapore-incorporated companies (default) | January 1, 2003 | Modelled on IFRS but not identical |

| SFRS(I) | SGX-listed companies (mandatory); others may opt in | January 1, 2018 | Word-for-word identical to IFRS |

| SFRS for Small Entities | Qualifying small private companies | January 1, 2011 | Simplified framework based on IFRS for SMEs |

Full SFRS

Full SFRS applies by default to all Singapore-incorporated companies, including subsidiaries and branches of Indian parent companies, unless they qualify for a simplified framework.

Required financial statements under full SFRS:

- Statement of comprehensive income

- Statement of financial position (balance sheet)

- Statement of cash flows

- Statement of changes in equity

- Notes to the financial statements (including accounting policies, judgements, and estimates)

SFRS (International) — SFRS(I)

SFRS(I) was introduced in 2017 to achieve full convergence with IFRS and became mandatory for all SGX-listed companies for annual periods beginning on or after January 1, 2018. Non-listed companies may voluntarily adopt SFRS(I).

This framework matters most for Indian businesses eyeing an SGX listing. Key reasons to consider it:

- Identical to IFRS word-for-word, so international investors can read your financials without adjustment

- Simplifies cross-border comparability when your Indian parent also reports under IFRS-aligned standards

- Eases capital-raising with institutional investors already familiar with IFRS reporting

For companies that won't pursue a listing and want reduced compliance costs, there's a third option.

SFRS for Small Entities

This simplified framework became effective January 1, 2011 and is available to companies that qualify as "small entities." To qualify, a company must meet at least two of three criteria:

- Total annual revenue not exceeding SGD 10 million

- Total assets not exceeding SGD 10 million

- Not more than 50 employees

The entity must also not be publicly accountable. That rules out:

- A public company

- A charity under the Charities Act

- An entity trading debt or equity instruments in public markets

SFRS for Small Entities reduces disclosure requirements and simplifies measurement rules, which lowers compliance costs. However, it may be unsuitable if:

- The Indian parent company consolidates under full Ind AS (mixing frameworks complicates consolidation)

- External lenders or investors demand full SFRS statements

- The Singapore entity plans to expand, pursue funding, or IPO in the future

If your Indian parent already prepares consolidated accounts under full Ind AS, aligning the Singapore subsidiary with full SFRS (rather than SFRS for SE) makes year-end consolidation cleaner and reduces reconciliation complexity.

Key Principles Behind Singapore Financial Reporting Standards

Singapore's financial reporting framework shares common ground with Ind AS — but the specific application rules matter. Indian finance teams setting up Singapore entities need to understand these core principles before configuring their chart of accounts or choosing accounting software.

The SFRS framework is built on the following principles:

- Accrual basis: Revenue and expenses are recorded when transactions occur, not when cash changes hands. Your Singapore accounting setup must properly reflect accruals, deferrals, and provisions — not just cash flows.

- Comparability: Financial statements must enable meaningful comparison across periods and between entities. Consistent classification and presentation from period to period is required, not optional.

- Relevance: Information must hold predictive and confirmative value for decision-makers. Disclosures that don't serve this purpose create noise, not clarity.

- Verifiability: Methods and assumptions must be disclosed so that independent readers — including ACRA reviewers and external auditors — can verify your figures without requiring insider knowledge.

- Accuracy and neutrality: Statements must be complete, free from material error, and free from bias. This standard applies equally to first-year filings and ongoing compliance.

Financial Reporting and Compliance Requirements in Singapore

What Annual Reports Must Include

Singapore companies must prepare comprehensive annual reports containing:

- Statement of comprehensive income

- Statement of financial position (balance sheet)

- Statement of cash flows

- Statement of changes in equity

- Shareholder details

- Dates of annual returns and Annual General Meeting (AGM)

- Details of company officers (directors and company secretary)

Filing Timelines

| Obligation | Deadline | Notes |

|---|---|---|

| ECI filing with IRAS | Within 3 months of financial year-end | Waiver applies if revenue ≤ SGD 5M AND ECI is nil |

| Annual return (listed companies) | Within 5 months of financial year-end | Filed with ACRA |

| Annual return (non-listed companies) | Within 7 months of financial year-end | Filed with ACRA |

| Accounting record retention | Minimum 5 years | From end of relevant transaction year |

Audit Requirements

Most Singapore companies must undergo an annual statutory audit. However, two categories are exempt:

- Dormant companies — exempt under Section 205B of the Companies Act

- Qualifying small companies — exempt under Section 205C; must be a private company meeting at least two of these three criteria for the immediate past two consecutive financial years:

- Annual revenue ≤ SGD 10 million

- Total assets ≤ SGD 10 million

- 50 or fewer employees

For company groups, the entire group must meet these thresholds on a consolidated basis.

Indian businesses operating lean Singapore entities should verify their audit exemption status with a Singapore accounting professional before assuming exemption.

Penalties for Non-Compliance

Singapore enforces financial reporting compliance rigorously:

| Offence | Penalty |

|---------|---------|

| Late annual return (up to 3 months late) | SGD 300 late lodgement penalty |

| Late annual return (more than 3 months late) | SGD 600 late lodgement penalty |

| Companies Act breach (court conviction) | Fine up to SGD 5,000 per charge |

| Failure to attend court (director) | Warrant for arrest |

| Non-filing of tax returns for 2+ years | Fine up to SGD 5,000 plus twice the tax assessed |

Foreign Branch Filing Requirements

For Indian companies operating Singapore branches (as opposed to subsidiaries), you must file:

- Audited financial statements for both the head office (India) and Singapore branch each year

- Dormant branches are permitted to file unaudited statements

Timelines per Companies Act Section 373(3):

- Within 60 days (approximately 2 months) after the head office AGM

- If no AGM is required: within 5 months after the financial year-end (referencing the public company timeline under Section 197)

In practice, delays in your Indian head office AGM can push your Singapore branch filing deadline closer to — or past — the penalty threshold, making AGM scheduling a compliance matter on both sides.

SFRS vs. Indian Accounting Standards: What Indian Businesses Should Know

India follows Ind AS (for listed and large unlisted companies) or older AS standards (for smaller entities), both broadly IFRS-converged but with carve-outs and modifications. Singapore's SFRS/SFRS(I) more closely tracks pure IFRS, creating reconciliation requirements for Indian businesses.

Key Differences Indian Finance Teams Must Manage

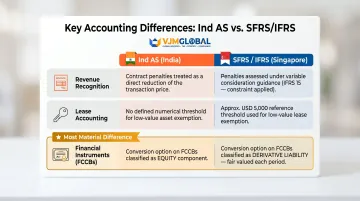

Revenue Recognition:

- Ind AS 115 treats penalties in customer contracts as direct reductions of the transaction price

- SFRS(I) 15 handles penalties under general "variable consideration" guidance

- Presentation: Ind AS 115 prescribes "Contract Asset" / "Contract Liability" labels on the balance sheet; SFRS(I) 15 allows alternative descriptions like "Accrued Income"

Lease Accounting:

- Ind AS 116 does not specify a numerical low-value asset threshold; judgment applies in Indian context

- IFRS 16 / SFRS(I) 16 references approximately USD 5,000 as the low-value threshold in its Basis for Conclusions

- Ind AS 116 contains specific transitional provisions for long-term government land leases (common in India); SFRS(I) 16 applies standard treatment

Financial Instruments (FCCBs): This is the most material difference for Indian companies raising capital:

- Ind AS 109: Foreign Currency Convertible Bond (FCCB) conversion options are classified as equity if the exercise price is fixed in any currency

- IFRS 9 / SFRS(I) 9: Conversion options must be classified as derivative liability if the exercise price is in a foreign currency

For Indian companies issuing FCCBs, this means reclassifying equity-treated conversion options as derivative liabilities under SFRS(I) 9 — a change that can introduce meaningful P&L volatility in Singapore reporting.

Practical Differences in Reporting

Currency and Presentation: Singapore does not mandate SGD presentation. IRAS allows companies to prepare financial statements in their functional currency, which may be non-SGD. However, SGD remains the most common presentation currency.

Financial Year-End Flexibility: India typically follows an April-March fiscal year. Singapore allows companies to choose any financial year-end date, though they must file ECI within three months and annual returns within prescribed timelines from that year-end.

Disclosure Requirements: Full SFRS disclosure requirements may be more extensive than what Indian SMEs are used to under older AS standards. Indian businesses upgrading from AS to Ind AS may find SFRS disclosure expectations familiar, but those still on AS frameworks will face a steeper compliance curve.

Managing Dual Compliance

Indian businesses running Singapore subsidiaries face dual compliance obligations:

- Prepare Ind AS-compliant consolidated accounts for the Indian parent

- Ensure the Singapore entity's standalone accounts comply with SFRS

This requires:

- Managing differences in revenue recognition, lease accounting, and financial instrument classification

- Handling currency translation (INR to SGD) in consolidation

- Eliminating inter-company transactions correctly under both frameworks

- Reconciling Ind AS carve-outs with SFRS requirements

Cross-border accounting specialists with experience in both Indian and Singapore frameworks — VJM Global works specifically with Indian businesses expanding internationally — can reduce errors in consolidation, currency translation, and inter-company eliminations.

Practical tip: If your Indian parent consolidates under full Ind AS, aligning your Singapore subsidiary with full SFRS (rather than SFRS for SE) makes consolidation cleaner. The frameworks are both IFRS-converged, reducing reconciliation complexity at year-end.

Frequently Asked Questions

What accounting standards are used in Singapore?

Singapore uses the Singapore Financial Reporting Standards (SFRS), modelled on IFRS. Three frameworks exist: full SFRS (default for all companies), SFRS(I) (mandatory for SGX-listed companies from 2018, word-for-word identical to IFRS), and SFRS for Small Entities (for qualifying small private businesses meeting size and public accountability criteria).

Is IAS 1 replaced by IFRS 18?

Yes, IFRS 18 (Presentation and Disclosure in Financial Statements) replaces IAS 1 and is effective for annual periods beginning on or after January 1, 2027. Singapore has adopted the equivalent SFRS(I) 18 and SFRS 118 on the same timeline, so Indian businesses with Singapore operations should begin preparing in 2025 to meet the 2027 effective date.

Do Indian companies with Singapore subsidiaries need to follow both Ind AS and SFRS?

Yes. Indian parent companies must prepare Ind AS-compliant consolidated statements, while their Singapore entities independently comply with SFRS for standalone reporting. This means managing two sets of standards, reconciling key differences (revenue recognition, financial instruments), and eliminating inter-company transactions on consolidation.

What is the difference between SFRS and SFRS(I)?

SFRS is the traditional Singapore standard, closely following IFRS with some local modifications. SFRS(I) is a word-for-word adoption of IFRS, mandatory for SGX-listed companies from January 1, 2018. SFRS(I) is preferred for entities seeking cross-border capital or planning an SGX listing due to full international comparability.

Which Singapore companies are exempt from statutory audit?

Dormant companies and qualifying small companies are exempt under Singapore's Companies Act. A small company must meet at least two of three criteria for two consecutive years: revenue ≤ SGD 10 million, total assets ≤ SGD 10 million, or ≤ 50 employees. Groups must satisfy these thresholds on a consolidated basis.

Can a Singapore company choose its own financial year-end?

Yes, Singapore companies can choose any financial year-end date and are not required to follow the calendar year. However, they must file their ECI within three months from that year-end and annual returns within the prescribed timelines (5 months for listed companies, 7 months for non-listed companies).