Introduction

Imagine receiving your company's first statutory audit report in Singapore. The auditor references "occurrence," "completeness," and "valuation" — terms that mean little without context, yet each one represents a specific claim your management has made about the financial statements. Miss one, and you're looking at a qualified opinion, ACRA scrutiny, or worse.

Those terms are audit assertions — the implicit and explicit representations management makes every time a set of financial statements is prepared. For any Singapore company subject to statutory audit requirements under the Companies Act, understanding how assertions work, and where they fail, is a compliance necessity.

What follows breaks down the assertion framework under SSA 315 (Revised 2021): what each assertion means, the risks attached to it, and how auditors test it in practice.

TL;DR

- Audit assertions are management's implicit claims about the accuracy, completeness, and validity of financial statements — verified independently by auditors during the audit process.

- Under SSA 315 (Revised 2021), assertions are grouped into two categories: transactions/events and account balances, with disclosures embedded in both.

- Each assertion carries distinct misstatement risks — such as overstated revenue (occurrence), understated liabilities (completeness), and inflated assets (valuation).

- Failed assertions can trigger a qualified audit opinion, ACRA regulatory action, or director liability under the Companies Act.

What Are Audit Assertions and Why They Matter in Singapore

When a Singapore company prepares its financial statements, every line item carries embedded representations: that a sale actually happened, that all liabilities are captured, that assets are stated at appropriate values. These representations are audit assertions — and under Singapore's Companies Act, statutory auditors must independently verify them.

Companies that don't qualify for the small company audit exemption under ACRA must appoint auditors and have their statements audited. Exemption requires meeting at least 2 of 3 criteria: annual revenue of S$10 million or less, total assets of S$10 million or less, and 50 or fewer employees — applied over two consecutive financial years. Group companies face additional consolidation criteria.

For companies subject to statutory audit, the governing framework is Singapore Standards on Auditing, published by the Institute of Singapore Chartered Accountants (ISCA). The operative risk-assessment standard is SSA 315 (Revised 2021), effective for periods beginning on or after 15 December 2021 and aligned with ISA 315 (Revised 2019).

Assertions serve three interconnected purposes:

- Guide audit design: Give auditors a structured framework for planning and executing procedures at the assertion level

- Define management's burden: Establish what financial statements must demonstrate to be accurate and compliant under SFRS(I)

- Focus risk assessment: Help both auditors and preparers identify where misstatements are most likely to occur

Those purposes converge at the board level. ACRA's directors' financial reporting guidance is direct: directors must ensure financial statements comply with the Companies Act, meet applicable accounting standards, and give a true and fair view. A failed assertion — say, an unrecognized liability or an overstated asset — isn't just an audit finding. It's a director-level compliance exposure.

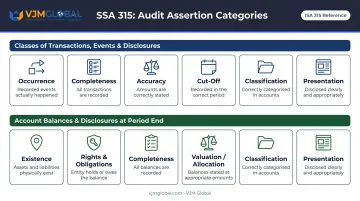

The Two Categories of Audit Assertions Under SSA 315

The current SSA 315 framework uses two groupings — not three. Disclosures are no longer a standalone third category; they're integrated into the assertions for transactions and account balances. Knowing this distinction matters, because older resources still reference a separate presentation and disclosure bucket that the revised standard has absorbed.

| SSA 315 Category | Key Assertions | What It Tests |

|---|---|---|

| Classes of transactions, events, and related disclosures | Occurrence, completeness, accuracy, cut-off, classification, presentation | Whether period activity happened, is complete, is correctly measured, captured in the right period, and properly described |

| Account balances, and related disclosures, at period end | Existence, rights and obligations, completeness, accuracy/valuation/allocation, classification, presentation | Whether year-end balances are real, belong to the entity, are complete, and are stated at appropriate values |

Each category addresses a distinct phase of financial reporting. Here's what auditors focus on within each.

Assertions About Transactions and Events

This category covers everything that moves through the profit and loss account during the year — revenue, purchases, payroll, interest, and other operational entries. The assertions confirm that every recorded transaction is genuine, nothing has been omitted, amounts are correct, timing is right, and items sit in the correct accounts.

Revenue is the highest-sensitivity area. Companies often face pressure to record sales early or inflate volumes, which makes occurrence and cut-off the two assertions auditors prioritize first on any Singapore income statement review.

Key assertions auditors test in this category:

- Occurrence — did the transaction actually take place?

- Completeness — have all transactions been recorded?

- Cut-off — is each entry captured in the correct period?

- Accuracy — are the amounts free from material error?

Assertions About Account Balances

These assertions apply to the balance sheet at year-end. The question shifts from "did this happen?" to "does this exist, and is it measured correctly?" A receivable must represent a real amount owed by a real customer. An asset must be owned or controlled by the entity. Liabilities must capture all genuine obligations, including any structured off-balance sheet.

Valuation is consistently one of the most complex areas to audit. It depends on management estimates, including:

- Depreciation rates and useful life assumptions

- Impairment assessments for goodwill and long-term assets

- Inventory write-downs to net realizable value

- Fair value measurements for financial instruments

Key Types of Audit Assertions Explained

Transaction-Level Assertions

Occurrence: Management claims every recorded transaction actually took place and relates to the entity. Testing it means selecting entries from the ledger and tracing backward to supporting documents — the invoice, the dispatch note, the contract. If no supporting evidence exists, the transaction's occurrence is in doubt. For revenue, this is the primary fraud guard: fictitious sales cannot survive a well-designed occurrence test.

Completeness is the reverse of occurrence — management claims no transactions have been omitted. Testing direction matters: auditors start from source documents (purchase orders, goods received notes, unmatched supplier statements) and trace forward into the ledger. Under-recording purchases can artificially inflate margins, which is why this assertion draws close attention in high-volume procurement environments.

Accuracy and Cut-Off: Accuracy confirms that amounts are mathematically correct and appropriate rates were applied; cut-off confirms transactions fall in the right accounting period. Auditors often test both together around the year-end close. A service delivered in December but invoiced and recognised in January creates a cut-off failure — the revenue belongs in the earlier period under SFRS(I) revenue recognition principles, regardless of when the invoice was raised.

Classification and Presentation — Classification asks whether transactions are in the right account. Misposting a capital expenditure to operating expenses distorts both the P&L and the balance sheet simultaneously. Presentation covers whether disclosures related to transactions are clearly described and disaggregated in the notes consistent with SFRS(I) requirements.

Transaction-level assertions focus on what happened during the period. Account balance and disclosure assertions shift the lens to what the financial statements show at year-end.

Account Balance and Disclosure Assertions

Existence vs. Rights and Obligations: Existence confirms that assets, liabilities, and equity balances recorded at year-end are real. Rights and obligations goes further — it tests whether the company legally owns or controls those assets and is genuinely liable for the obligations recorded.

The distinction matters. A company might hold consignment stock it does not own: that stock passes an existence test but fails rights and obligations. Off-balance-sheet arrangements can pass both tests while still concealing genuine liabilities.

Valuation and Allocation: Management claims all balances are stated at appropriate amounts per SFRS(I). This covers:

- Depreciation methods and useful life estimates

- Impairment testing, including goodwill

- Fair value measurements for financial instruments

- Inventory costing at the lower of cost or net realisable value

ACRA's 2023 Audit Regulatory Report specifically flagged accounting estimates and inventory procedures as inspection themes — reflecting how frequently valuation produces audit findings.

Common Risks When Audit Assertions Fail

An assertion failure is not a technical paperwork issue. Under SSA 320, a misstatement — including an omission — is material if it could reasonably influence economic decisions made by users of the financial statements. In practice, every failed assertion becomes a potential statutory reporting problem.

Occurrence and Existence Failures

When occurrence is not properly verified, fictitious transactions can inflate revenue on the income statement. When existence is inadequately tested, phantom assets can pad the balance sheet. Both create the same downstream problem: financial statements that overstate the company's financial position.

The scale of financial statement fraud globally underlines why this matters. The ACFE's 2024 Report to the Nations, analysing 1,921 occupational fraud cases across 138 countries, found that while financial statement fraud represents only 5% of cases, it is the most costly category by far. For ACRA-regulated companies, confirmed fraud or material overstatement typically triggers a qualified audit opinion and potential regulatory investigation.

Completeness and Valuation Failures

Completeness failures tend to work in the opposite direction, understating rather than overstating. Unrecorded liabilities, omitted expenses, or off-balance-sheet obligations make a company appear more profitable and less leveraged than it actually is. This distorts decisions made by lenders, investors, and tax authorities, including IRAS assessments based on reported income.

Valuation failures are often harder to detect because they involve genuine management judgement rather than deliberate misstatement. Common examples where the valuation assertion breaks down include:

- Goodwill that hasn't been tested for impairment

- Inventory carried above net realisable value

- Receivables without adequate provisioning for expected credit losses

Each of these can materially misrepresent the company's financial position without any single transaction being fraudulent.

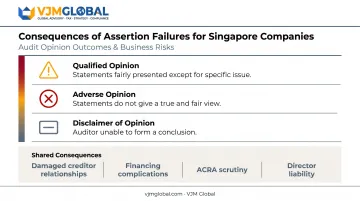

Consequences for Singapore Companies

When assertion-level failures produce a material misstatement, the auditor may issue:

- A qualified opinion — the statements are fairly presented except for the specific issue

- An adverse opinion — the statements do not give a true and fair view

- A disclaimer of opinion: the auditor cannot form a conclusion

Any non-clean opinion carries real consequences: damaged creditor relationships, complications in financing or M&A transactions, potential ACRA scrutiny of both the company and its auditor, and personal exposure for directors under the Companies Act for failing to ensure accurate financial reporting.

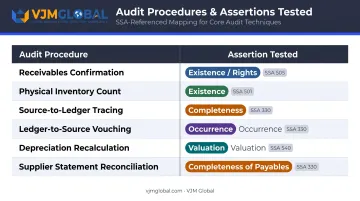

How Auditors Test Assertions in Singapore

SSA 330 defines the two main tracks for testing assertions: tests of controls (evaluating whether internal controls prevent assertion failures) and substantive procedures (directly verifying balances, transactions, and disclosures through tests of detail and analytical procedures).

Common procedures mapped to specific assertions:

| Audit Procedure | Primary Assertion Tested |

|---|---|

| Receivables confirmation (SSA 505) | Existence; rights and obligations |

| Physical inventory count attendance (SSA 501) | Existence and condition |

| Source document to ledger tracing | Completeness |

| Ledger to source document vouching | Occurrence |

| Depreciation recalculation | Valuation and allocation |

| Supplier statement reconciliation | Completeness of payables |

The approach is explicitly risk-based under SSA 315. Auditors assess which assertions carry higher inherent or control risk, then direct testing proportionately. Higher-risk balances — such as revenue occurrence in distribution or inventory valuation in manufacturing — receive more intensive procedures than low-risk, well-controlled items.

Group and Cross-Border Complexity

This risk-proportionality becomes more complex when group structures are involved. For foreign companies operating in Singapore — subsidiaries of US, UK, Australian, or other multinational groups — assertion-level risks are often elevated. Intercompany transactions introduce cut-off and accuracy complexity. Related-party arrangements require specific rights and obligations scrutiny. Group consolidation creates completeness risks if subsidiary reporting is incomplete or delayed.

VJM Global works with international clients navigating cross-border accounting and audit support requirements, including group reporting, internal controls documentation, and pre-audit preparation. For companies managing cross-border obligations across India, Singapore, and other jurisdictions, having advisors with hands-on experience in multi-entity structures reduces the friction around assertion-level preparation.

Frequently Asked Questions

What are the audit assertions in Singapore?

Audit assertions in Singapore are management's implicit or explicit claims about the accuracy, completeness, and validity of financial statements. They are governed by SSA 315 (Revised 2021), published by ISCA, and grouped under two categories: assertions for transactions/events and assertions for account balances, with disclosures embedded in each.

What is the difference between the occurrence and existence assertions?

Occurrence applies to transactions — confirming a recorded transaction actually took place during the period. Existence applies to account balances — confirming that assets, liabilities, and equity recorded at period-end are real. Both guard against overstatement, but occurrence is tested by vouching recorded entries to supporting documents, while existence is tested by physically verifying or confirming balances directly.

Which Singapore standard governs audit assertions?

SSA 315 (Revised 2021) — Identifying and Assessing the Risks of Material Misstatement — governs how auditors identify and test assertions in Singapore. Published by ISCA and effective for periods beginning on or after 15 December 2021, it is closely aligned with ISA 315 (Revised 2019).

How do auditors test the completeness assertion?

To test completeness, auditors start from source documents — such as purchase orders, goods received notes, or payroll records — and trace forward to ledger entries. This direction — source to ledger — distinguishes completeness testing from occurrence testing and ensures no transactions have been omitted.

What risks arise if audit assertions are not properly verified?

Unverified assertions can produce material misstatements — overstated revenue, understated liabilities, or misstated asset values. Consequences include a qualified or adverse audit opinion, ACRA regulatory scrutiny, and potential director liability under Singapore's Companies Act.

Do small companies exempt from statutory audit still need to understand audit assertions?

Companies qualifying for ACRA's small company exemption are not required to undergo statutory audits. However, understanding assertions remains useful for internal financial reporting quality, investor communications, and audit readiness if the company grows past exemption thresholds or pursues voluntary assurance for financing or M&A purposes.