Introduction

Singapore's small company audit exemption under Section 205C of the Companies Act (Cap. 50) offers qualifying private companies a significant compliance relief: the ability to skip the statutory audit requirement entirely. For eligible companies, this translates to annual savings of approximately S$2,500 to S$5,500 in audit fees, plus considerable management time otherwise spent supporting the audit process.

Foreign investors and SME directors typically face three critical questions: Do we qualify? What does the exemption actually cover? And what obligations remain regardless of exempt status? Getting these wrong can lead to costly retrospective audit appointments or regulatory penalties.

This guide covers the precise eligibility criteria — including the often-overlooked group test that disqualifies many Singapore subsidiaries of multinational companies. It also clarifies what the exemption removes and what it doesn't, and walks through the practical steps directors must take to track their status year by year.

Key Takeaways

- Qualify as "small" by meeting 2 of 3 thresholds for two consecutive years: revenue ≤ S$10M, assets ≤ S$10M, or ≤ 50 employees

- Private companies only — public companies must always be audited

- Groups (including foreign subsidiaries) must separately pass a consolidated "small group" test

- Exemption removes the auditor requirement only — bookkeeping, financial statements, and ACRA/IRAS filings remain mandatory

- Status is self-assessed annually — directors bear full legal responsibility for the correct determination

What Is the Small Company Audit Exemption in Singapore?

The small company audit exemption is a legal provision under Section 205C and the Thirteenth Schedule of Singapore's Companies Act 1967, effective for financial years beginning on or after 1 July 2015. It allows qualifying private companies to forgo appointing an external auditor and obtaining an independent audit report each year. The intent is to reduce compliance costs and administrative burden on small businesses, while preserving accountability through continued financial reporting obligations.

This exemption is distinct from the dormant company exemption under Section 205B, which applies regardless of size but only to companies with no significant accounting transactions. Section 205C applies specifically to active trading companies that stay below defined size thresholds.

Understanding that distinction matters because the eligibility rules differ entirely. The exemption was introduced through the Companies (Amendment) Act 2014, reflecting Singapore's view that mandatory audits impose a disproportionate compliance burden on smaller entities. It replaced the older exempt private company (EPC) regime, broadening eligibility through quantitative size criteria rather than shareholder structure rules.

Who Qualifies: The Two-of-Three Eligibility Test

Core Requirements

To qualify, a company must satisfy two conditions simultaneously:

- Be a private company throughout the entire financial year

- Meet at least 2 of 3 quantitative criteria for each of the two immediately preceding financial years:

- Total revenue ≤ S$10 million

- Total assets ≤ S$10 million

- Employees ≤ 50 at year-end

How Each Criterion Is Measured

Total Revenue: Based on the revenue line in financial statements under Singapore Financial Reporting Standards (SFRS). Key exclusions from the S$10M threshold:

- Other income and gains on disposal

- Finance income appearing below the revenue line

Total Assets: Sum of fixed and current assets at financial year-end per the balance sheet. Note: no deductions for liabilities — this is gross total assets, not net assets.

Employees: Year-end headcount, not a yearly average. ACRA counts full-time employees on the company's payroll. Key points:

- Excludes independent contractors and outsourced staff not directly employed

- Part-time employees on payroll count per head, not as full-time equivalents

Transitional Rule for New Companies

Companies less than two years old may qualify from their first or second financial year if they meet the 2-of-3 criteria for that single year — no two-year history is required when none exists yet.

Practical Lookback Illustration

Example scenario: A company with December year-end is assessing exemption eligibility for FY2026:

- FY2024: Revenue S$9.5M, Assets S$11M, Employees 45 → Passes (2 of 3)

- FY2025: Revenue S$11.5M, Assets S$9M, Employees 48 → Passes (2 of 3)

- FY2026 assessment: Qualifies for exemption because both FY2024 and FY2025 passed the test

Even if FY2026's actual performance exceeds thresholds, the company remains exempt for FY2026 because the test looks backward two years, not at the current year.

Losing and Requalifying

A company loses exemption once it exceeds thresholds for two consecutive years. The loss takes effect from the financial year that follows that second non-compliant year. Requalification requires meeting the criteria for two consecutive years again — which can create a gap of two to three years without exemption if status is lost.

Monitor all three metrics every year. One strong revenue year won't cost you the exemption — but two consecutive years above any two thresholds will.

The Small Group Test for Parent and Subsidiary Companies

The Hidden Disqualifier

Section 205C imposes an additional layer for companies part of a group: a parent company cannot claim audit exemption unless:

(a) It qualifies as a small company individually, AND

(b) The entire group qualifies as a "small group" on a consolidated basis for the two immediately preceding financial years.

This dual requirement catches many Singapore holding companies and subsidiaries of foreign multinationals.

Small Group Thresholds

The group must meet at least 2 of 3 consolidated criteria:

- Consolidated group revenue ≤ S$10 million

- Consolidated group total assets ≤ S$10 million

- Aggregated employees across all group entities ≤ 50

Same 2-of-3 structure, same two-year lookback period. The Thirteenth Schedule (paragraph 7) specifies the consolidation methodology based on applicable Accounting Standards.

Foreign Subsidiaries Are Included

What often catches groups off guard is the scope of consolidation. Foreign subsidiaries must be included in the group test regardless of their location or local reporting standards. A Singapore holding company with operating entities in Vietnam, India, Australia, or the UK must include those entities' revenue, assets, and headcount — even where those foreign companies follow entirely different local audit rules.

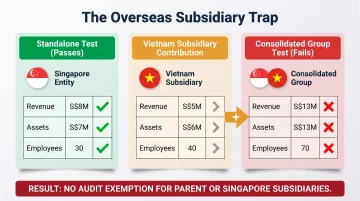

Common Scenario: The Overseas Subsidiary Trap

Example: A Singapore parent company has:

- Singapore entity: Revenue S$8M, Assets S$7M, Employees 30 → Passes standalone test

- Vietnam subsidiary: Revenue S$5M, Assets S$6M, Employees 40

- Consolidated group: Revenue S$13M, Assets S$13M, Employees 70 → Fails group test

Result: Neither the Singapore parent nor its Singapore subsidiaries can claim exemption, despite the Singapore entity easily passing the standalone criteria.

For companies with cross-border structures, getting this assessment right requires accurate consolidated figures across every group entity — not just Singapore. VJM Global works with multinationals on exactly this type of group-level analysis, helping holding companies determine exemption eligibility before filing deadlines create compliance exposure.

How Exemption Status Is Gained, Maintained, and Lost

Gaining Status

Exemption status is self-assessed and applies automatically when criteria are met. No formal application to ACRA is required.

Established companies qualify by meeting the 2-of-3 criteria for two consecutive financial years. Newly incorporated companies can qualify from the first or second financial year if criteria are met for that single year alone.

Directors should document their annual assessment — capturing the three metrics, the calculation methodology, and their conclusion — in case ACRA or shareholders later request evidence of compliance.

Once exemption is established, the focus shifts to keeping it.

Maintaining Status

Once qualified, a company retains small company status in subsequent years unless one of two disqualifying events occurs:

- Ceases to be a private company at any time during the financial year (e.g., conversion to a public company)

- Fails the 2-of-3 quantitative criteria for two consecutive financial years

The two-year buffer protects companies from losing exemption due to a single anomalous year of strong performance or temporary growth. Even so, it's worth tracking thresholds annually — because two quiet breaches can trigger a mandatory audit before most directors notice.

Losing and Requalifying

Disqualification takes effect from the financial year following the second consecutive year of non-compliance.

Example timeline:

- FY2024: Fails criteria (first breach)

- FY2025: Fails criteria (second consecutive breach)

- FY2026: Must appoint auditor and prepare audited statements

- FY2027 onward: Remains non-exempt until requalifies

To requalify, a company must meet the 2-of-3 criteria for two consecutive financial years. Using the example above: failing in FY2024 and FY2025 means passing in both FY2026 and FY2027 before exemption resumes in FY2028.

In practice, losing exemption status creates a gap of two to three financial years with mandatory audits — a significant cost and administrative burden that proactive threshold monitoring can prevent.

What the Audit Exemption Covers — and What It Doesn't

What Is Removed

The audit exemption eliminates:

- The legal obligation to appoint a registered public accountant as auditor

- The requirement to produce an auditor's report under Section 207

- Associated direct audit fees (typically S$2,500 to S$5,500 for SMEs)

- Management time supporting the audit process (documentation requests, inquiries, audit meetings)

What Is NOT Removed

The exemption does not eliminate these obligations:

- Section 199 (Accounting records): Maintain proper records and internal controls for at least five years. Non-compliance carries penalties up to S$10,000 or 12 months imprisonment.

- Section 201 (Financial statements): Directors must prepare SFRS-compliant statements giving a "true and fair view," with a Directors' Statement signed by two directors.

- ACRA filing: Lodge financial statements via BizFile+ as part of the annual return (XBRL format where applicable). Late filing penalties run S$300–S$600 per breach.

- IRAS — ECI filing: Submit Estimated Chargeable Income within three months of financial year-end (exempt only if revenue ≤ S$5M and ECI is nil).

- IRAS — Corporate tax return: File Form C-S, Form C-S Lite, or Form C according to IRAS deadlines.

- Director accountability: Directors remain fully liable under Section 201 to present accurate accounts at the AGM — an auditor's absence does not reduce that responsibility.

Year-round bookkeeping that meets Sections 199 and 201 standards is what keeps the exemption viable. Firms that let records slip risk losing it entirely.

ACRA's Override Power

Section 205D grants ACRA authority to require a company that is otherwise exempt to lodge audited financial statements if:

- There has been a breach of Section 199 or 201, or

- ACRA determines it is in the public interest

In practice, this means qualifying on paper is not enough. Maintaining clean records and compliant financials throughout the year is what keeps the exemption intact.

Common Misconceptions and When to Consider a Voluntary Audit

Common Misconceptions

Misconception 1: Audit exemption means no financial reporting is required

Not quite. Companies must still prepare SFRS-compliant financial statements, maintain accounting records, present accounts at the AGM, and lodge statements with ACRA. Only the auditor's report is eliminated.

Misconception 2: The 2-of-3 test only needs to be met once

False. The criteria must be satisfied for both of the two preceding consecutive financial years, and this assessment must be repeated every year the company wishes to remain exempt.

Misconception 3: Companies with corporate shareholders cannot qualify

This was true under the old rules — but no longer. The small company regime replaced the exempt private company (EPC) framework that restricted shareholder types. Corporate ownership does not disqualify a company from exemption under Section 205C.

When to Consider a Voluntary Audit

Clearing up misconceptions is only half the picture. Even when exemption is available, many companies voluntarily commission an audit for practical business reasons:

- Bank financing: Lenders require audited accounts as a condition of credit facilities to assess creditworthiness and monitor compliance

- Group reporting: Parent companies require subsidiaries to submit audited statements for consolidation, regardless of local exemption rules

- Investor requirements: Private equity, venture capital, and institutional investors mandate audited accounts in shareholder agreements to ensure governance standards

- Grant applications: Many government grant programs require audited financials as part of the application or ongoing compliance process

- M&A preparation: An audit history strengthens due diligence credibility and reduces buyer or investor risk perception when planning an exit or fundraising round

Conclusion

The small company audit exemption is a practical, commercially meaningful concession for eligible Singapore private companies, offering tangible cost savings and reduced administrative burden. Qualifying requires careful annual monitoring — and knowing what the exemption does not cover matters just as much as knowing whether you qualify. Core compliance obligations remain intact, and missing a threshold can trigger retrospective audit appointments with real cost consequences.

Before filing each year, directors should confirm:

- All three quantitative thresholds have been assessed against the correct two-year window

- Group test obligations are reviewed if your company is part of a Singapore-incorporated group

- SFRS-compliant financial statements are prepared and signed off, even without a statutory audit

For directors managing foreign-owned Singapore entities or cross-border group structures, self-assessment errors in this area carry disproportionate compliance risk. VJM Global's advisory team works with multinational companies navigating Singapore and India-linked compliance requirements — including audit exemption reviews, group consolidation analysis, and financial statement preparation — to ensure your annual close is accurate and defensible.

Frequently Asked Questions

Do we need to apply for audit exemption?

No formal application is required. Audit exemption under Section 205C is self-assessed and applies automatically if your company meets the eligibility criteria. Directors should still document their annual assessment to demonstrate compliance if questioned by ACRA or shareholders.

Can a company with corporate shareholders qualify for the small company audit exemption?

Yes, companies with corporate shareholders can qualify. The small company regime replaced the old exempt private company rule that required shareholders to be individuals, so corporate ownership no longer disqualifies a company from exemption.

What happens if our company loses its small company status?

The company must appoint a registered public accountant and prepare audited financial statements starting from the financial year following the second consecutive year of failing the criteria. You must meet the 2-of-3 test for two consecutive years before requalifying.

Does audit exemption apply to the group level, or just the Singapore entity?

For companies that are part of a group (parent or subsidiary), both the individual company AND the consolidated group must pass the qualifying tests. If the group fails the small group criteria, neither the parent nor its Singapore subsidiaries can claim exemption.

Does qualifying for audit exemption mean we no longer need to prepare financial statements?

No. Audit exemption only removes the auditor's report requirement. Companies must still prepare SFRS-compliant financial statements, maintain accounting records under Section 199, present accounts at the AGM, and lodge financial statements with ACRA as part of the annual return.

Are there situations where a company that qualifies for audit exemption should still get audited?

Yes. Companies often choose voluntary audits for compliance or strategic reasons, including:

- Bank loan covenants or investor agreements requiring audited accounts

- Group reporting obligations imposed by a foreign parent

- Government grant applications that mandate audited financials

- Upcoming M&A transactions where audited accounts reduce due diligence risk