Introduction

You've just received your company's auditor's report, and while the financial statements look familiar, the opinion document is filled with technical sections and unfamiliar terminology. Phrases like "SSA 700," "Basis for Opinion," and "true and fair view" appear throughout — but you're unsure which sections matter most.

The real question: does the opinion type you've received signal a problem that could affect your bank credit line, ACRA standing, or investor confidence?

For business owners in Singapore—particularly foreign companies and multinational entities—misreading an auditor's report carries real consequences. A qualified opinion left unaddressed for months can trigger lender restrictions. A disclaimer of opinion may raise governance red flags with regulators. Even the absence of a section like "Material Uncertainty Related to Going Concern" carries meaning.

This guide focuses on the auditor's report itself: its structure under Singapore Standards on Auditing (SSAs), the four opinion types your auditor can issue, and the transparency measures introduced in 2016 that shape every report. Whether you're a director facing your first statutory audit or a CFO managing a modified opinion, knowing how to read this document protects your company's standing with lenders, regulators, and investors.

Key Takeaways

- An auditor's report is a formal, independent opinion on whether financial statements are accurate and comply with Singapore Financial Reporting Standards (SFRS).

- Singapore auditors issue one of four opinion types: unqualified (clean), qualified, adverse, or disclaimer of opinion—each with distinct implications.

- Listed companies now see enhanced reports with Key Audit Matters (KAM) and expanded Going Concern disclosures under SSAs.

- A modified opinion requires prompt action: address root causes with expert guidance before the next audit cycle.

What Is an Auditor's Report in Singapore?

An auditor's report is the formal written communication issued at the conclusion of a statutory audit by a licensed public accountant registered with the Accounting and Corporate Regulatory Authority (ACRA). It is the auditor's primary means of communicating findings to shareholders, investors, lenders, and regulators.

Legal Mandate Under the Companies Act 1967

Under Singapore's Companies Act 1967, most private limited companies must undergo an annual statutory audit and receive an auditor's report. Sections 201 and 207 establish the framework:

- Section 201(8): Financial statements must be "duly audited" before presentation at the AGM, with the auditor's report attached

- Section 207(1)-(2): Auditors must report to members on whether financial statements comply with Accounting Standards and give a "true and fair view," and whether accounting records have been properly kept

- Section 207(7): The auditor's report must be attached to or endorsed on the financial statements

These requirements are governed by Singapore Standards on Auditing (SSAs), issued by the Institute of Singapore Chartered Accountants (ISCA) and approved by ACRA's Public Accountants Oversight Committee.

Audit Exemptions: Who Must File

Not all companies require an auditor's report. Small company exemptions apply to private companies meeting at least two of these criteria for the preceding two consecutive financial years:

- Total annual revenue ≤ S$10 million

- Total assets ≤ S$10 million

- Number of employees ≤ 50

Key exceptions to note:

- Public companies (listed or unlisted) must always be audited

- Companies part of a group must qualify as a "small group" on a consolidated basis

- Shareholders holding ≥5% voting power can require an audit despite exemptions (Section 205B(6))

- Dormant companies (no accounting transactions) are exempt under Section 205B

Report vs. Financial Statements: Key Distinction

The auditor's report — the opinion document — is distinct from the audited financial statements themselves (balance sheet, income statement, cash flow statement, directors' statement).

The report is attached to the audited financial statements filed with ACRA, but it serves a different purpose: providing an independent professional opinion on the reliability and compliance of those statements.

Key Sections of the Auditor's Report Explained

Since new and revised SSAs took effect for periods ending on or after 15 December 2016, auditor reports follow a standardised structure. The most significant change: the Opinion section now appears first, making the auditor's conclusion immediately visible.

Opinion Section

The auditor states whether the financial statements give a "true and fair view" of the company's financial position and performance in accordance with SFRS and the Companies Act. Read this section first — it delivers the overall verdict.

The heading signals the type of opinion issued:

- Opinion — unmodified (clean) report

- Qualified Opinion — material issue, but limited in scope

- Adverse Opinion — statements do not present a true and fair view

- Disclaimer of Opinion — auditor unable to form a conclusion

Basis for Opinion Section

This section describes how the audit was conducted and confirms:

- The auditor followed SSAs

- The auditor is independent and complies with ethical requirements under the ACRA Code of Professional Conduct and Ethics

- The audit evidence obtained is sufficient and appropriate

This section provides assurance that the conclusion was reached through proper professional methodology — not assumption.

Responsibilities of Management and the Auditor

This section clarifies the split of accountability:

Management (directors) is responsible for:

- Preparing accurate financial statements

- Maintaining adequate internal controls

- Assessing the company's ability to continue as a going concern

The auditor's role is to:

- Independently assess whether statements present a true and fair view

- Obtain reasonable assurance (not absolute certainty)

- Identify and assess risks of material misstatement

- Evaluate the appropriateness of accounting policies

Directors cannot delegate responsibility for financial statement accuracy to auditors. The auditor provides independent verification — not preparation.

Other Sections and Disclosures

Additional sections may include:

- Going Concern section: A separate "Material Uncertainty Related to Going Concern" section if significant doubt exists about the company's ability to continue operating (required under SSA 570 Revised)

- Key Audit Matters: For listed entities, a detailed explanation of the areas the auditor judged most significant (required under SSA 701)

- Engagement partner's name: For listed entity audits, providing personal accountability (with a narrow exemption for personal safety risks)

- Other Information: Addressing information in annual reports outside the financial statements (per SSA 720 Revised)

The 4 Types of Audit Opinions in Singapore

An auditor cannot simply "pass" or "fail" a company. Instead, SSA 705 (Revised) establishes four standardised opinion types, each reflecting a different level of concern.

Unqualified (Clean) Opinion

An unqualified opinion means the auditor found the financial statements accurate, complete, and compliant with SFRS — the result every company should be working toward.

What helps achieve a clean opinion:

- Accurate, timely record-keeping throughout the year

- Strong internal controls at the process level

- Proper documentation of significant transactions

- Timely reconciliation of accounts

- Compliance with accounting standards and disclosure requirements

- Cooperation with auditors and timely provision of requested information

A clean opinion tells lenders and investors that your financial reporting is reliable and your governance systems are functioning as they should.

Qualified Opinion

A qualified opinion is issued when the auditor identifies a material misstatement or scope limitation — but one that doesn't undermine the financial statements as a whole.

What "material but not pervasive" means in practice:

- A specific account balance is misstated (e.g., inventory valuation error affecting one product line)

- The misstatement is significant enough to matter to users

- But the rest of the financial statements remain reliable

- Users can still make informed decisions with appropriate caution

The report will include a "Basis for Qualified Opinion" paragraph explaining the specific issue. Start there — it identifies exactly what needs to be corrected before the next audit cycle.

Common causes for qualified opinions:

- Inadequate documentation for certain transactions

- Scope limitations (auditor denied access to specific records)

- Departure from accounting standards on a particular item

- Inability to verify specific balances (e.g., overseas subsidiary accounts)

Adverse Opinion

When issues escalate beyond a qualified opinion, the auditor issues an adverse opinion. This happens when misstatements are both material and pervasive — meaning they fundamentally undermine the financial statements across multiple areas.

What this signals:

- The financial statements cannot be relied upon

- The errors or misstatements affect multiple areas

- Users cannot make informed decisions based on the statements

Real-world implications:

- Lenders may freeze or withdraw credit facilities

- ACRA may initiate enforcement action, requiring restatement and re-audit

- Investors will lose confidence; equity raising becomes difficult

- IRAS may scrutinise tax filings more closely

- Reputational damage with suppliers, customers, and partners

Receiving an adverse opinion requires board-level intervention — restatement, re-audit, and a documented remediation plan are typically the minimum steps expected by regulators.

Disclaimer of Opinion

A disclaimer is issued when the auditor cannot obtain sufficient evidence to form any opinion at all — typically due to scope limitations that make a conclusion impossible.

Common scenarios:

- Management denies access to critical records

- Significant uncertainty about accounting treatments

- Unable to verify existence of material assets

- Incomplete or missing accounting records

Why this is damaging:

- Signals serious governance concerns

- Suggests management may be withholding information

- Raises questions about financial transparency

- Stakeholders cannot rely on the financial statements at all

In practice, stakeholders treat a disclaimer as seriously as an adverse opinion. The inability — or unwillingness — to provide auditors with complete records raises the same fundamental question: can this company's financials be trusted?

Key Audit Matters and Enhanced Disclosures Under SSA 701

Singapore's 2016 auditor reporting reforms reshaped what auditors must disclose — and what stakeholders can expect to learn from an audit report beyond a simple pass/fail opinion.

Key Audit Matters (KAM)

Key Audit Matters are the areas the auditor judged most significant during the audit — issues that required the most attention, carried the highest risk of material misstatement, or involved complex judgments. Disclosure requirements vary by entity type:

- Mandatory for audits of listed entities (shares, stock, or debt listed on SGX)

- Voluntary for private companies, though auditors may include them if beneficial

Typical KAM areas include:

- Revenue recognition (timing, multiple performance obligations)

- Asset valuations (goodwill impairment, property valuations for REITs)

- Business combinations and acquisition accounting

- Complex financial instruments

- Significant estimates (provisions, fair values)

SGX Regulation has emphasised business and real estate valuations as critical KAM areas, particularly for REITs and IPOs. For private companies, KAMs still signal where management should review and strengthen internal controls.

Enhanced Going Concern Disclosures (SSA 570 Revised)

If the auditor concludes that a material uncertainty exists regarding the company's ability to continue as a going concern, a separate section titled "Material Uncertainty Related to Going Concern" must be included.

This section signals that events or conditions cast significant doubt on the entity's ability to keep operating, and that the auditor is drawing explicit attention to the risk. Different stakeholders should read this differently:

- Management: Immediate action required to address liquidity or viability concerns

- Creditors: High risk of default or insolvency

- Investors: Increased risk of investment loss

If going concern disclosures are inadequate, the auditor must issue a qualified or adverse opinion under SSA 705 (Revised).

Independence Statement and Partner Disclosure

Every auditor's report now includes an independence statement confirming compliance with the ACRA Code of Professional Conduct and Ethics. This appears in the Basis for Opinion section and serves a clear purpose: without demonstrated independence, the audit opinion carries no weight for stakeholders.

For listed entity audits, the engagement partner's name must also appear in the report (SSA 700 Revised, Para 46). This ties personal accountability to the professional judgment expressed in the report.

One narrow exemption applies: if disclosure is "reasonably expected to lead to a significant personal security threat," the name may be omitted. This applies only in exceptional circumstances — for example, jurisdictions where auditors face physical harm for reporting fraud.

What a Modified Opinion Means for Your Business—and What to Do Next

A qualified, adverse, or disclaimer opinion signals specific issues that need immediate attention — but how you respond in the weeks that follow determines the real business impact.

Immediate Steps When You Receive a Modified Opinion

1. Understand the Basis paragraph

- Read the "Basis for [Qualified/Adverse/Disclaimer] Opinion" section carefully

- Identify the specific issue: is it a misstatement, a scope limitation, or a disclosure deficiency?

- Determine whether the issue is factual or a difference in judgment

2. Engage your auditor

- Schedule a meeting to clarify the root cause

- Ask: Is this a one-time error or a systemic internal control weakness?

- Request specific remediation recommendations

- Clarify what evidence or process changes would support a clean opinion next cycle

3. Assess the nature of the issue

- One-time error: Isolated transaction or event that can be corrected

- Systemic weakness: Internal control failure requiring process redesign

- Scope limitation: Information gap that can be resolved with better documentation or access

Downstream Consequences to Manage Proactively

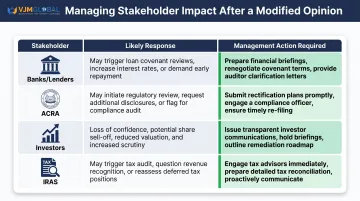

A modified opinion triggers real business consequences that require active management:

| Stakeholder | Likely Response | Management Action Required |

|---|---|---|

| Banks/Lenders | Restrict or withdraw credit facilities; invoke default clauses | Proactive communication; provide remediation plan; negotiate covenant waivers |

| ACRA | Flag company for closer scrutiny; may require restatement and re-audit | Engage compliance experts; prepare detailed response; implement controls |

| Investors | Loss of confidence; reluctance to inject capital | Transparent disclosure; demonstrate corrective action; rebuild trust |

| IRAS | Potential closer review of tax filings and positions | Ensure tax filings are defensible; prepare supporting documentation |

The longer a modified opinion sits unaddressed, the more entrenched stakeholder concerns become — lenders move from monitoring to enforcement, and regulators from inquiry to investigation.

Working with Expert Advisors

Navigating a modified opinion requires specialised expertise. Working with an experienced accounting and audit advisory firm can help you:

- Develop a remediation plan that addresses root causes, not just symptoms

- Strengthen internal controls to close the gaps that triggered the opinion

- Build documentation and processes that hold up under the next audit cycle

- Communicate proactively with ACRA, lenders, and investors before they escalate concerns

- Work toward a clean opinion in the next reporting period with a clear audit trail

For foreign businesses operating in Singapore, the cross-border complexity — reconciling group reporting standards with SFRS requirements, managing ACRA obligations remotely — adds another layer to an already sensitive process. Firms like VJM Global, with 30+ years of experience supporting multinationals across audit readiness and regulatory compliance, bring structured advisory support to help businesses move from a modified opinion back to clean reporting.

Frequently Asked Questions

What are the 4 types of audit reports?

The four opinion types under SSA 705 (Revised) are: unqualified (clean), qualified, adverse, and disclaimer of opinion. An unqualified opinion means financial statements are accurate and compliant; a qualified opinion signals a material but not pervasive issue; an adverse opinion indicates material and pervasive misstatements; and a disclaimer means the auditor could not obtain sufficient evidence to form an opinion.

How to check the financials of a company in Singapore?

A company's audited financial statements can be accessed via ACRA's BizFile+ portal by purchasing a Corporate Compliance and Financial Profile (CCFP) for S$50, which includes up to three years of comparative data and the audit opinion. Listed companies also publish financials through the SGX annual reports portal or directly from the company upon request.

What is included in an auditor's report in Singapore?

Standard sections include: Opinion, Basis for Opinion, auditor's and management responsibilities, and an independence statement. Listed entities also require Key Audit Matters and the engagement partner's name. Additional sections may address going concern uncertainties or other information in the annual report.

What does a qualified audit opinion mean for my company?

A qualified opinion means a material but not pervasive issue was found—such as a specific misstatement or scope limitation. Stakeholders should review the "Basis for Qualified Opinion" paragraph to understand the exact issue, and the company should take corrective action before the next audit cycle to restore a clean opinion.

What are Key Audit Matters (KAM) in an auditor's report?

KAMs are the areas of greatest significance during the audit, as judged by the auditor. They are disclosed in the auditor's report for listed companies under SSA 701, helping investors understand where audit scrutiny was most focused — such as revenue recognition, asset valuations, or other complex accounting estimates requiring significant judgment.

Who can issue an auditor's report in Singapore?

Only public accountants or accounting firms registered with ACRA can issue statutory auditor's reports in Singapore. They must comply with SSAs and the ACRA Code of Professional Conduct and Ethics. Registration and oversight are governed by the Accountants Act and administered by ACRA's Public Accountants Oversight Committee.