This guide compares five of the leading UK business bank accounts — Starling, Monzo, Tide, Revolut, and Barclays — across fees, FSCS protection, accounting integrations, and suitability by business type. Whether you're a freelancer opening your first account or an SME reassessing your current banking setup, this comparison gives you a clear, side-by-side picture.

Key Takeaways

- Limited companies must legally separate business finances; sole traders aren't required to, but it's strongly advisable

- Digital providers (Starling, Monzo, Tide, Revolut) offer lower fees and faster onboarding

- Traditional banks (Barclays) provide lending, overdrafts, and in-branch support

- FSCS protection, accounting integrations, FX support, and true running costs matter more than the headline monthly fee

- Most digital providers open accounts the same day; traditional banks may take longer

- The right account depends on how your business operates, not just which plan costs least

What Is a Business Bank Account in the UK?

A business bank account is a dedicated account for managing business income and expenditure, kept separate from personal finances. It's available to sole traders, limited companies, LLPs, partnerships, and charities.

The legal position varies by business structure:

- Limited companies are legally separate entities registered at Companies House — they must maintain a separate business bank account

- Sole traders and ordinary partnerships are not legally required to open a business account, according to Business.gov.uk

Do I Need a Business Bank Account?

You definitely need one if you're running a limited company. For sole traders, it's technically optional — but most personal bank terms restrict commercial use, and separating finances makes HMRC Self Assessment significantly easier to manage.

HMRC's Making Tax Digital (MTD) for Income Tax Self Assessment adds further pressure. The rollout targets sole traders and landlords by income threshold:

- From April 2026: qualifying income over £50,000

- From April 2027: qualifying income over £30,000

- From April 2028: qualifying income over £20,000

A business account with direct accounting software integration removes most of the manual MTD compliance burden.

Best Business Bank Accounts in the UK Compared

The five accounts below represent the leading options across digital and traditional banking, selected on fees, FSCS protection, accounting integrations, and fit for different business types. Always verify current fees and features directly with each provider before applying.

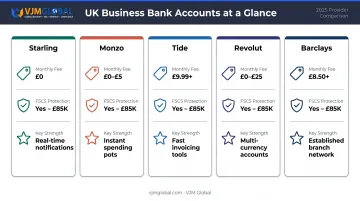

Starling Bank — Best for Fee-Free Everyday Banking

Starling is a UK-licensed bank with no monthly fee on its standard Business Current Account. Over 500,000 UK businesses have joined, and it's consistently rated highly for its mobile app experience.

Strengths:

- No monthly fee and no minimum balance requirement

- Full FSCS protection — eligible deposits covered up to £85,000 per eligible person

- Direct integrations with Xero, QuickBooks, and FreeAgent

- In-app cheque imaging and in-app invoicing

Limitations:

- No physical branches

- Currency conversion fees apply on international transfers

- Fewer lending products than traditional banks

| Detail | Info |

|---|---|

| Monthly Fee | £0 (standard Business Current Account; paid add-ons available) |

| FSCS Protection | Yes — up to £85,000 per eligible person |

| Best For | Startups, sole traders, and SMEs wanting fee-free banking with strong accounting integrations |

Monzo Business — Best for Mobile Banking Experience

Monzo offers a tiered account structure: Lite at £0/month, Pro at £9/month, and Team from £25/month. Its app is one of the most recognised in UK personal banking, and the business product delivers the same polished interface.

Strengths:

- Full FSCS protection up to £85,000 on eligible deposits

- Tax Pot feature on paid plans — automatically ring-fences a percentage of income for VAT or tax

- Integrations with Xero, FreeAgent, Sage, and QuickBooks

- Instant spending notifications

Limitations:

- Tax Pot and advanced integrations locked behind paid tiers

- The free Lite plan has limited functionality

| Detail | Info |

|---|---|

| Monthly Fee | £0 (Lite); paid tiers available |

| FSCS Protection | Yes — up to £85,000 per eligible person |

| Best For | Business owners who want a polished mobile experience and built-in tax management tools |

Tide — Best for Accounting Software Integration

Tide is an FCA-authorised electronic money institution designed specifically for small businesses, sole traders, and freelancers. Its free plan has no monthly fee, with paid tiers offering expanded features.

A note on FSCS: Tide's current accounts are powered by ClearBank, meaning eligible funds are FSCS-protected up to £85,000 per eligible person. Older Tide e-money accounts use safeguarding under FCA e-money regulations rather than FSCS — so confirm which account type you're opening if FSCS coverage is a priority.

Strengths:

- Integrations with Xero, QuickBooks, Sage, FreeAgent, and KashFlow

- Purpose-built for businesses that want tight bank-to-bookkeeping synchronisation

- Fast online account opening

Limitations:

- Transaction fees apply on the free plan

- FSCS protection depends on account type (ClearBank-powered vs. older e-money accounts)

| Detail | Info |

|---|---|

| Monthly Fee | £0 (Free plan); paid tiers available |

| FSCS Protection | Yes on ClearBank-powered accounts (up to £85,000); older e-money accounts use safeguarding only |

| Best For | Sole traders and small businesses with heavy accounting software use wanting seamless reconciliation |

Revolut Business — Best for Multi-Currency and International Payments

Revolut received its full UK banking licence in March 2026, bringing it under full PRA/FCA regulation. It supports 25+ currencies, making it a practical choice for businesses paying overseas suppliers or invoicing international clients.

Strengths:

- Multi-currency accounts covering 25+ currencies

- Real-time spending notifications and built-in expense management

- FSCS protection on eligible deposits following full UK banking licence

- Competitive FX rates within plan allowances

Limitations:

- FX fees apply once free monthly allowances are exceeded (varies by plan)

- Advanced features locked behind higher-tier paid plans

- Pricing and specific allowances should be confirmed on Revolut's current pricing page before applying

| Detail | Info |

|---|---|

| Monthly Fee | From £0 (Basic plan); higher tiers available |

| FSCS Protection | Yes — eligible deposits protected following full UK banking licence |

| Best For | SMEs and startups with international suppliers or clients needing multi-currency support in one platform |

Barclays Business — Best for Traditional Full-Service Banking

Barclays is one of the UK's oldest and largest banks, offering a Business Current Account with 12 months of free banking for new businesses, then £8.50/month thereafter (per the current published tariff — verify the latest figure directly with Barclays before applying).

Strengths:

- Extensive UK branch and ATM network, including cash deposit access

- Full FSCS protection up to £85,000 per eligible person

- Access to business loans, overdrafts, and merchant services

- Dedicated relationship manager for eligible accounts

Limitations:

- Lags behind digital providers on app experience and multi-currency tools

- Transaction, cash deposit, and non-sterling fees apply — check the current Barclays business tariff for the full breakdown

| Detail | Info |

|---|---|

| Monthly Fee | £0 for first 12 months; £8.50/month thereafter (verify current rate with Barclays) |

| FSCS Protection | Yes — up to £85,000 per eligible person |

| Best For | New businesses wanting a full-service traditional bank with branch access, lending options, and a free startup period |

How to Choose the Right Business Bank Account

Most business owners focus on the monthly fee and ignore the total cost of ownership. That's a mistake. A £0/month account with per-transaction charges, cash deposit fees, and FX markups can cost more than a £10/month account with included allowances.

Work through these five decision factors:

- Business structure — Limited companies need a business account by law. Sole traders benefit practically but choose based on volume and complexity

- Transaction type — High cash turnover favours banks with branch access (like Barclays); predominantly digital payments favour fintechs

- FSCS protection — Businesses holding larger balances should prioritise fully licensed banks with confirmed FSCS coverage

- International payments — Multi-currency support and competitive FX rates become critical for businesses paying overseas suppliers or receiving foreign income

- Accounting integration — Xero reports that UK users save 5.5 hours a week using bank feeds and automated transaction matching, which directly supports MTD compliance

Scalability Matters

The account you open today should grow with your business. Look for tiered plans, multi-user access, and features like corporate cards or spend management tools — rather than switching providers every 12 months as your needs evolve.

For UK businesses with cross-border operations, the account choice quickly connects to wider questions — which entity structure minimises tax exposure, how payroll is handled across jurisdictions, and what compliance obligations apply under HMRC and overseas regulators. These aren't banking questions, but the wrong account makes answering them harder.

VJM Global works with UK businesses managing India-linked operations, international payroll, and multi-entity accounting structures — helping align banking decisions with the tax and regulatory setup before the first transaction clears.

How to Open a Business Bank Account in the UK

What You'll Need

For sole traders:

- Valid photo ID (passport or driving licence)

- Proof of UK residential address

For limited companies:

- The above, plus your Companies House registration number and Certificate of Incorporation

Requirements vary by provider, so check directly with your chosen bank before applying.

Onboarding Timelines

Once your documents are in order, how long you wait depends heavily on which provider you choose. Digital providers like Starling and Tide advertise account opening in minutes once documents are submitted. Traditional banks typically involve manual review processes that take longer — factor this in if you need an account quickly.

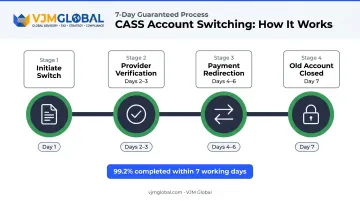

Switching Your Account

Most UK business current accounts are covered by the Current Account Switch Service (CASS). CASS transfers incoming and outgoing payments to your new account and closes the old one within seven working days. CASS Q4 2025 data shows 99.2% of switches completed within seven working days with a 93% customer satisfaction rate — so the process is reliable if you decide to move.

Conclusion

There's no single best business bank account for every UK business. The right fit depends on how you operate:

- Starling — best for fee-conscious startups and sole traders

- Monzo — suits mobile-first users who want built-in tax management

- Tide — strong bookkeeping integrations for admin-heavy businesses

- Revolut — the natural choice for international-heavy operations

- Barclays — go-to for branch access, lending, or overdraft facilities

Look past the monthly fee alone. Assess the full cost against operational value: accounting integrations, cash handling charges, and room to scale as your business grows.

Choosing the right banking setup is one piece of running a financially sound UK business. VJM Global has supported 250+ UK businesses with compliance, accounting outsourcing, and financial advisory services.

If you want to understand how your banking setup fits into your broader compliance and tax position, their team of accounting professionals can help you get the foundations right from day one.

Frequently Asked Questions

Which bank is best for business accounts in the UK?

There's no single answer. Starling is strong for fee-free everyday banking; Revolut suits businesses with international payment needs; Monzo is best for mobile-first users. Traditional banks like Barclays are better suited to businesses needing branch access, overdrafts, or lending products.

Do I need a business bank account as a sole trader in the UK?

Sole traders aren't legally required to hold a separate business account. That said, most personal bank terms restrict commercial use, and keeping finances separate makes HMRC Self Assessment and Making Tax Digital compliance easier to manage.

What documents do I need to open a business bank account in the UK?

You'll typically need valid photo ID and proof of UK address. Limited companies also need a Companies House registration number and Certificate of Incorporation. Exact requirements vary by provider, so check before applying.

How long does it take to open a business bank account in the UK?

Digital-first providers like Starling and Tide can open accounts in minutes once documents are verified. Traditional high-street banks involve more manual review and typically take one to four weeks, so plan ahead if you need an account quickly.

Is my business bank account protected by the FSCS?

FSCS covers eligible deposits up to £120,000 (the standard limit since 1 December 2025) at fully licensed UK banks including Starling, Monzo, Barclays, and Revolut. Tide's ClearBank-powered accounts are also FSCS-protected, though older Tide e-money accounts use FCA safeguarding instead — always confirm your account type before depositing large balances.

Can I switch my business bank account in the UK?

Yes. Most UK business current accounts participate in the Current Account Switch Service (CASS), which completes the switch — including redirecting payments and closing the old account — within seven working days, with a 99.2% completion rate based on Q4 2025 data.