Introduction

Running an Indian subsidiary while reporting to a Singapore parent means navigating two sets of accounting rules simultaneously—and the cash flow statement sits at the intersection of both. Prepared under Ind AS 7 (or AS-3 for non-Ind AS companies), it tracks exactly how cash moves in and out of your Indian entity across three activity categories during a reporting period.

Unlike the income statement, which records revenue and expenses on an accrual basis, the cash flow statement shows actual liquidity. A profitable Indian subsidiary can still face a cash crunch—and this statement is where that reality becomes visible.

This guide is written for Singapore businesses operating a subsidiary, branch office, or joint venture in India. Cross-border operations mean dual compliance obligations: India's Companies Act 2013 and Ind AS on one side, Singapore's FRS 7 on the other.

That dual reporting creates real friction—especially when your Indian entity's April-to-March financial year doesn't match your Singapore parent's reporting calendar, or when intercompany transactions trigger both FEMA and accounting standard implications.

This guide covers what Indian cash flow requirements demand and how the statement is structured. It also addresses where Singapore businesses most often encounter compliance gaps—from working capital adjustments for Indian tax items like TDS and advance tax to currency translation mismatches during group consolidation.

Key Takeaways

- India mandates cash flow statements under Ind AS 7 or AS-3, governed by Schedule III of the Companies Act 2013

- Cash flows split into operating, investing, and financing activities—similar to FRS 7 but with key classification differences

- Most Indian companies use the indirect method; the direct method is permitted but rarely adopted

- Singapore parent companies must translate INR cash flows to SGD for group reporting, managing FX and intercompany flows

- Misclassification or non-compliance triggers audit flags, ROC queries, or statutory filing issues

What Is a Cash Flow Statement Under Indian Accounting Standards?

A cash flow statement is a mandatory financial statement that presents actual inflows and outflows of cash and cash equivalents during a financial year, showing liquidity separately from accrual-based profit. This separation matters: a company can report healthy profits on its income statement while at the same time facing a severe cash shortage. Profit measures economic performance. Cash flow determines whether the business can actually pay its bills.

The governing standards in India are:

- Ind AS 7 (aligned with IFRS IAS 7) applies to companies meeting prescribed thresholds: listed companies, large unlisted companies with net worth exceeding ₹250 crore, or those with specific parent-subsidiary structures

- AS-3 applies to smaller, non-Ind AS companies that fall below these thresholds

Both standards fall under Schedule III of the Companies Act 2013. Any company required to prepare a balance sheet and income statement must also prepare a cash flow statement — unless specifically exempted (covered in the next section).

Unlike the income statement or balance sheet, the cash flow statement is prepared on a cash basis, not accrual. It answers one direct question: where did cash come from, and where did it go?

That simplicity is why auditors, lenders, and regulators in India scrutinize it closely. For Singapore businesses with Indian subsidiaries or joint ventures, it also provides the clearest window into whether the Indian entity is generating — or consuming — real liquidity.

Who Must Prepare a Cash Flow Statement in India—and Why It Matters for Singapore Businesses

Not all Indian companies are required to prepare a cash flow statement. The thresholds that determine who qualifies for an exemption are specific:

Mandatory Preparation:

- All public companies

- All listed companies

- Private companies exceeding ₹10 crore paid-up capital or ₹100 crore turnover

- Companies following Ind AS (prescribed thresholds apply)

- Any company whose financial statements are required to comply with Schedule III, Division II

Exemptions:

- One Person Companies (OPCs)

- Small companies (paid-up capital not exceeding ₹2 crore and turnover not exceeding ₹20 crore, as updated in 2025)

- Dormant companies

Singapore businesses typically enter India via a wholly owned subsidiary (a private limited company) or through a branch office. Liaison offices, which are restricted to non-commercial activities, generally do not prepare standalone cash flow statements.

Branch offices follow specific reporting rules under Section 381 of the Companies Act 2013, requiring the branch to file audited financial statements—including cash flows—with the Registrar of Companies.

Why This Matters Practically

Your Indian subsidiary's cash flow statement feeds directly into your Singapore parent's consolidated financial statements. Errors or misclassifications at the India level affect:

- Group-level financial reporting accuracy

- Auditor sign-offs in Singapore

- Financial credibility with Singapore-based lenders and investors

- MAS-regulated reporting for financial services entities

These reporting risks are compounded by a structural timing issue: India's April-to-March financial year doesn't align with most Singapore companies' December or customized year-ends, requiring pro-rata adjustments or interim cash flow preparation to maintain consolidation accuracy.

Structure and Key Components of an Indian Cash Flow Statement

A compliant Indian cash flow statement follows a standard structure: it starts with the opening cash and cash equivalent balance, presents net cash generated or used across three activity categories, and reconciles to the closing cash and cash equivalent balance—which must match the figure reported in the balance sheet under current assets.

The three sections are:

Operating Activities

Operating activities reflect cash generated or consumed by a company's core revenue-producing operations in India. This includes:

- Cash receipts from customers

- Payments to suppliers and employees

- Rent, utilities, and operating expenses

- Income tax paid

Under the indirect method (the dominant approach in India), this section starts with profit before tax from the income statement, then adjusts for:

- Non-cash items: depreciation, amortisation, provisions, impairment charges

- Non-operating items: interest income, profit or loss on asset disposal

- Changes in working capital: movements in trade receivables, inventory, trade payables, and other current assets/liabilities

The indirect method is preferred because the data is already available from accrual-based accounting records. For Singapore finance teams, this means you can reconcile operating cash flow back to the Indian subsidiary's profit figure—a critical validation step.

Investing Activities

Investing activities capture cash flows from the acquisition or disposal of long-term assets:

- Purchases of property, plant, and equipment

- Investments in securities or subsidiary companies

- Proceeds from asset sales

- Intercompany loans: receipt or disbursement of loans between the Indian entity and the Singapore parent

This section is particularly important for Singapore businesses because FEMA governs cross-border fund flows—and each flow must align with RBI reporting requirements. For example:

- An intercompany loan from the Singapore parent to the Indian subsidiary is an investing inflow for the Indian entity (and must be reported under ECB regulations)

- Repayment of that loan is an investing outflow

Misclassification of these transactions is one of the most common errors VJM Global flags when reviewing Indian entity financials for foreign-parented businesses.

Financing Activities

Financing activities include:

- Borrowings from banks and financial institutions

- Repayment of loans

- Proceeds from share capital issuance (FDI from the Singapore parent)

- Dividend payments to shareholders

Two classification choices require particular attention at the group level:

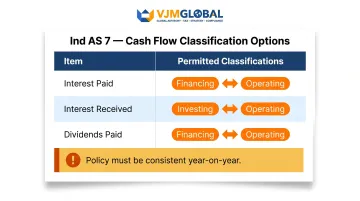

Dividends paid: Under Ind AS 7 (aligned with IAS 7), these can sit under either financing or operating activities—the same flexibility exists under Singapore's FRS 7. The policy must be consistent year-on-year and clearly disclosed to avoid confusion in consolidated reporting.

Interest paid and received: Interest paid can be classified as operating or financing; interest received as operating or investing. Singapore finance teams should confirm which policy the Indian entity has adopted and apply it consistently—inconsistency here distorts trend analysis across the group.

VJM Global prepares Ind AS-compliant cash flow statements for Singapore businesses with Indian subsidiaries, including correct classification of intercompany loans, FDI proceeds, and cross-border interest flows—the transactions most likely to be misreported without specialist oversight.

Preparing a Cash Flow Statement Under Ind AS 7: Direct vs Indirect Method

Ind AS 7 permits two methods for presenting operating cash flows: the direct method and the indirect method.

The Indirect Method

The indirect method begins with profit before tax from the income statement, then adjusts for:

- Non-cash charges: depreciation, amortisation, impairment, provisions

- Non-operating items: interest income credited to profit, profit or loss on asset disposal

- Changes in working capital: movements in receivables, payables, inventory, prepayments

Example calculation:

Profit before tax ₹10,00,000

Add: Depreciation ₹2,00,000

Add: Interest expense ₹1,50,000

Less: Interest income (₹50,000)

Less: Increase in trade receivables (₹3,00,000)

Add: Increase in trade payables ₹2,50,000

Less: Income tax paid (₹1,80,000)

Net cash from operating activities ₹10,70,000

This method is preferred by most Indian companies because the data is already available from accrual accounting records. This makes it easier to audit and verify against the balance sheet.

The Direct Method

The direct method presents gross cash receipts from customers and gross cash payments to suppliers, employees, and the government directly:

Cash received from customers ₹50,00,000

Cash paid to suppliers (₹30,00,000)

Cash paid to employees (₹8,00,000)

Cash paid for operating expenses (₹1,30,000)

Income tax paid (₹1,80,000)

Net cash from operating activities ₹8,90,000

Ind AS 7 encourages the direct method (mirroring IAS 7 preference) because it provides cleaner cash flow visibility. In practice, Indian companies almost universally use the indirect method — tracking gross cash receipts and payments creates a significant additional record-keeping burden.

Singapore businesses whose Indian auditors or board require direct method presentation should plan for this extra record-keeping from the outset.

Critical Alignment Point

Whichever method you choose for operating activities, one rule applies universally: the investing and financing sections are identical under both. The final net change in cash must reconcile to the movement in cash and cash equivalents on the Indian entity's balance sheet. Failure to reconcile is one of the most common audit flags.

AS-3 Treatment for Smaller Entities

Under AS-3 (applicable to smaller, non-Ind AS Indian companies), extraordinary items must be separately disclosed within the cash flow statement. This requirement does not exist under Ind AS 7, which eliminated the extraordinary item concept in line with IFRS. Singapore finance teams reviewing older Indian entities or legacy reporting structures should check which standard applies.

India vs Singapore Cash Flow Reporting: Key Differences Singapore Businesses Must Know

While both India's Ind AS 7 and Singapore's FRS 7 are based on IAS 7, important differences exist:

Scope of Applicability

Singapore (FRS 7): All entities preparing financial statements under SFRS must include a cash flow statement, with limited exceptions for investment funds.

India: Exempts certain small private companies (OPCs, small companies meeting prescribed thresholds). An Indian subsidiary that qualifies for exemption may not be legally required to prepare one—creating a gap in data needed for Singapore group consolidation.

Practical implication: Singapore parent companies should require cash flow statements from Indian entities regardless of local exemption, to ensure complete group reporting.

Financial Year Difference

India: Follows an April-to-March financial year (ending 31 March).

Singapore: Typically follows a January-to-December or customised year-end.

This creates a timing mismatch that typically requires:

- Pro-rata adjustments for overlapping periods

- Standalone interim cash flow preparation

- Careful reconciliation of opening/closing balances

Foreign Currency Translation

The Indian entity's cash flows are denominated in INR. When consolidating into SGD for the Singapore parent's accounts, FRS 21 / Ind AS 21 rules on translating foreign currency cash flows apply:

- Cross-border cash flows — including dividends from the Indian subsidiary to the Singapore parent — must be translated at the exchange rate at the date of the cash flow, not at period-end rates

- Using period-end rates is a common consolidation error that distorts the cash flow statement and creates downstream reconciliation problems

Classification Differences

Under Indian practice:

Ind AS 7 permits flexibility on how certain items are classified — all three of the following have dual-classification options:

- Interest paid: financing or operating

- Interest received: investing or operating

- Dividends paid: financing or operating

Confirm which policy the Indian entity has adopted and apply it consistently year-on-year. Shifts in classification between periods distort group-level trend analysis.

FEMA Compliance Intersection

FEMA compliance intersects with cash flow reporting for Singapore-India cross-border transactions:

- Proceeds from share capital subscribed by the Singapore parent (FDI)

- Loans remitted to the Indian entity (ECB—External Commercial Borrowings)

- Repatriation of dividends or royalties

All these flows carry RBI approval and reporting requirements that must align with how they appear in the Indian entity's cash flow statement. A misclassification — for example, recording an ECB inflow under operating activities instead of financing — can trigger scrutiny during RBI audits and ROC annual filing reviews.

Common Compliance Mistakes Singapore Businesses Make with Indian Cash Flow Statements

Misclassifying Cross-Border Intercompany Transactions

Cross-border intercompany transactions are among the most consistently misclassified items in Indian cash flow statements prepared by Singapore finance teams.

Common mistakes:

- Recording an intercompany loan from the Singapore parent as operating income instead of a financing inflow

- Treating a capital contribution (equity FDI) as revenue rather than a financing inflow

- Failing to tie the cash flow classification to the corresponding FEMA reporting — ECB notification, FC-GPR filing, or FLA return

Correct classification matters on two fronts: Indian statutory compliance and group consolidation accuracy. A misclassified intercompany loan distorts the Indian entity's financing activities and inflates the Singapore parent's consolidated investing cash flows — compounding the error across both sets of books.

The Reconciliation Gap

Many Singapore finance teams rely on the Indian entity's profit figure without verifying that the cash flow statement's closing cash balance ties back to the balance sheet's cash and bank balance.

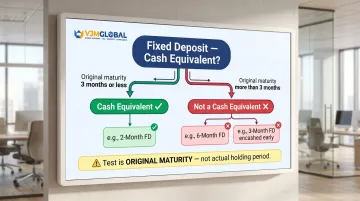

Common cause: Short-term fixed deposits (FDs) may or may not qualify as cash equivalents depending on their maturity.

Ind AS 7 definition: Cash equivalents are short-term, highly liquid investments with original maturity of three months or less from the date of acquisition, subject to insignificant risk of changes in value.

Test to apply:

- FD with 2-month original maturity = cash equivalent

- FD with 6-month original maturity = not a cash equivalent (classified as investment)

- FD placed for 3 months but encashed early = still not a cash equivalent (test is original maturity)

Misapplying this test — particularly for FDs encashed early — is a common reconciliation trap. Singapore finance managers accustomed to simpler cash equivalent rules under FRS 7 often miss the "original maturity" test entirely, leaving unexplained gaps between the cash flow statement and balance sheet.

Working Capital Adjustment Errors

Under the indirect method, changes in receivables, payables, and inventory must reflect movements during the reporting period based on the Indian entity's balance sheet.

Several Indian-specific line items are treated differently from Singapore practice:

- An increase in GST payable is added back to profit — the cash hasn't left the business yet

- Advance tax paid is not a working capital movement; it's classified as income tax paid under operating activities

- A rise in TDS receivable reduces operating cash flow as a working capital adjustment

Applying FRS 7 logic directly to Indian books causes errors here. The most common: treating advance tax as a current asset movement rather than an operating cash outflow. That single misclassification can meaningfully overstate operating cash flow.

Conclusion

A cash flow statement in India is not just a compliance formality—it is a real-time indicator of financial health for any Singapore business operating in India. Getting it right under Ind AS 7 or AS-3 requires understanding both the structural requirements and the classification rules that differ meaningfully from Singapore's FRS 7.

Singapore businesses should not apply Singapore cash flow reporting logic directly to their Indian operations. The differences in financial year conventions, currency translation rules, working capital adjustments, and FEMA-regulated cross-border flows create genuine compliance risk if not managed carefully.

VJM Global works with Singapore businesses on India-specific accounting and financial reporting, including preparation of Ind AS-compliant cash flow statements. Core services include:

- Correct classification of intercompany and cross-border transactions

- Reconciliation of cash and cash equivalents under Ind AS 7

- Accurate consolidation into group accounts for Singapore parent reporting

- FEMA compliance review for regulated capital flows

This covers both local compliance in India and accurate reporting to your Singapore stakeholders.

Frequently Asked Questions

Is a cash flow statement mandatory for all companies registered in India?

No. It is mandatory under the Companies Act 2013 for most companies except certain small private companies (One Person Companies and small companies meeting prescribed thresholds of ₹2 crore paid-up capital and ₹20 crore turnover). All listed and public companies must include it as part of their audited financial statements.

Which accounting standard governs cash flow statements in India?

Ind AS 7 (aligned with IFRS IAS 7) applies to companies meeting prescribed size or listing thresholds; AS-3 applies to non-Ind AS companies. For larger entities, Ind AS 7 has largely replaced AS-3 and removes the extraordinary items disclosure requirement that AS-3 retained.

What is the difference between Ind AS 7 and Singapore's FRS 7?

Both standards are based on IAS 7 and share the same three-section structure. Key differences include application thresholds, financial year convention (April-March in India vs customisable in Singapore), and India-specific regulatory overlays such as FEMA requirements for cross-border cash flows.

Which method—direct or indirect—is most commonly used in India?

The indirect method is dominant in Indian practice because it leverages existing accrual accounting data. While Ind AS 7 (like IAS 7) encourages the direct method for greater transparency, very few Indian companies adopt it due to the additional record-keeping required.

How should Singapore businesses handle foreign currency cash flows from their Indian operations?

INR cash flows must be translated at the exchange rate on the transaction date when consolidating into SGD group accounts under FRS 21/Ind AS 21 — not at period-end rates. FEMA compliance must also be maintained for all cross-border remittances.

Do branch offices and liaison offices of Singapore companies in India need to prepare cash flow statements?

Liaison offices generally do not prepare standalone Indian statutory cash flow statements, given their restriction to non-commercial activities. Branch offices have separate reporting obligations under Section 381 — including audited financials with cash flow components — but the full cash flow statement requirement applies primarily to incorporated subsidiaries and joint ventures.