Introduction

Singapore businesses investing in Indian companies, establishing subsidiaries, or evaluating joint venture partners face a critical challenge: reading Indian cash flow statements requires familiarity with India-specific accounting standards. Ind AS 7 — India's governing framework for cash flow reporting — introduces structural requirements, terminology, and compliance elements that differ significantly from Singapore's familiar SFRS(I) framework.

Three factors complicate interpretation for Singapore readers:

- India's financial year runs April 1 to March 31 (not calendar year), creating consolidation timing challenges for Singapore parent companies

- India-specific line items — quarterly advance tax payments and GST Input Tax Credit blockages — produce cash outflow patterns that can mislead first-time readers

- Indian group companies must file both standalone and consolidated statements under Section 129(3) of the Companies Act 2013; choosing the wrong version can dramatically misrepresent a subsidiary's true cash position

This guide provides Singapore businesses with a step-by-step process for reading Indian cash flow statements, explains critical differences under Ind AS 7, and identifies the red flags that signal financial distress versus normal operating patterns in the Indian market.

Key Takeaways

- Ind AS 7 governs Indian cash flow statements and applies to listed companies plus unlisted entities with net worth ≥ INR 250 crore

- Three activity sections (Operating, Investing, Financing) use the indirect method almost universally

- Positive operating cash flow signals business health; negative investing cash flow is expected in growing capital-intensive sectors

- Watch for India-specific items: advance tax installments (four per year), GST working capital swings, and related-party disclosures

- Request both standalone and consolidated statements; the subsidiary's standalone version reveals actual cash generation at the entity level

How to Read a Cash Flow Statement in India: A Step-by-Step Approach

Step 1: Identify the Reporting Framework and Period

Confirm the applicable standard. Indian companies apply one of two frameworks:

- Ind AS 7 ("Statement of Cash Flows"): Mandatory for listed companies and unlisted entities with net worth ≥ INR 250 crore, phased in from April 2016 to April 2019

- AS 3 ("Cash Flow Statement"): Still used by smaller private companies below the threshold

Singapore businesses familiar with SFRS(I) 7 will find Ind AS 7 substantially converged with IAS 7, but critical practical differences exist. Ind AS 7 permits both direct and indirect methods, though nearly all Indian companies use the indirect method for operating activities.

Interest paid, interest received, and dividends paid may appear under Operating OR Financing activities depending on the company's accounting policy choice. Verify classification before calculating ratios.

Verify the reporting period. India's statutory financial year runs April 1 to March 31 (Companies Act 2013, Section 2(41)), not calendar year. Singapore parent companies consolidating Indian subsidiaries must address this timing mismatch, typically by requesting interim financials aligned to the Singapore parent's year-end.

Check standalone vs. consolidated. Indian companies with subsidiaries must prepare both versions. The standalone statement shows only the parent entity's cash flows; the consolidated version combines all group entities with intercompany eliminations. For Singapore investors evaluating an Indian subsidiary or acquisition target, the standalone statement reveals the entity's actual cash generation capacity.

Step 2: Start with the Operating Activities Section

The operating section begins with Profit Before Tax (PBT), then adjusts for:

- Non-cash charges: depreciation, amortisation, provisions

- Working capital changes: movements in trade receivables, inventories, trade payables

Watch for two India-specific line items:

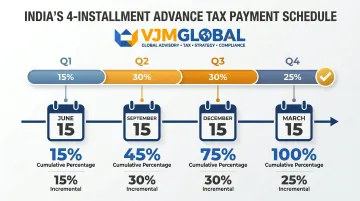

Advance tax paid. Indian corporate tax law (Income Tax Act Section 211) requires four cumulative quarterly installments:

| Due Date | Cumulative % | Incremental Payment |

|---|---|---|

| June 15 | 15% | 15% |

| September 15 | 45% | 30% |

| December 15 | 75% | 30% |

| March 15 | 100% | 25% |

These predictable outflows are heaviest in Q2 and Q3. September and December cash dips are routine tax compliance, not distress signals.

GST-related working capital swings. Blocked Input Tax Credit (ITC) accounts for 21.4% of current assets in Indian manufacturing SMEs and extends the cash conversion cycle by approximately 38 days. Negative or weak operating cash flow in Indian manufacturing may reflect GST administration friction rather than weak demand — examine the notes for blocked ITC amounts.

Step 3: Analyse the Investing and Financing Sections

Once you've assessed operating cash flows, the investing and financing sections reveal how the business allocates and funds that capital.

Investing Activities reveal capital allocation decisions:

- Capital expenditure (CAPEX): Consistently negative in growing Indian companies. India's Gross Fixed Capital Formation reached 29.61% of GDP in 2024. Manufacturing, infrastructure, and energy sectors routinely show negative investing cash flow 2–3x operating cash flow during expansion phases — this is structural, not distress.

- Intercorporate deposits (ICDs): Large outflows to related parties warrant scrutiny. Section 186 of the Companies Act caps ICDs at 60% of paid-up capital plus free reserves and restricts layering beyond two subsidiary tiers. Always cross-reference investing outflows with related-party disclosures — the IL&FS collapse (2018) traced directly to circular ICD lending across 300+ subsidiaries.

Financing Activities show capital structure decisions:

- Equity vs. debt: Track whether inflows come from fresh equity issuance or new borrowings, as this affects leverage and future interest obligations

- Dividend payments: Indian promoter-driven companies typically pay lower dividends than Singapore-listed peers. Sustained financing inflows alongside positive operating cash flow may indicate the parent is not repatriating locally generated cash

- Repatriation flows: Dividends to foreign shareholders appear here (if classified as financing). For Singapore parents, cross-reference against inter-company loan agreements and RBI/FEMA compliance requirements.

Step 4: Reconcile Opening and Closing Cash Balances

Verify that net movement across the three sections equals the change in cash and cash equivalents on the balance sheet. Indian cash equivalents include bank balances plus short-term deposits with original maturities ≤ three months.

If the company holds foreign currency deposits, a minor exchange difference may appear in the reconciliation. This is a legitimate item under Ind AS 7, not an accounting error. Treat any unexplained gap beyond this as a flag for further inquiry.

When Should Singapore Businesses Analyse an Indian Cash Flow Statement?

Cash flow analysis is not an annual compliance exercise—trigger it at specific decision points:

Before FDI into India: Due diligence on an acquisition target or JV partner must include at least three years of cash flow statements to identify cyclical patterns, working capital expansion trends, and hidden debt build-up that single-year snapshots miss.

During ongoing subsidiary monitoring: Quarterly or semi-annual reviews prevent surprises. Singapore parent companies should establish thresholds: if operating cash flow turns negative for two consecutive quarters (excluding seasonal advance tax effects), investigate working capital blockages or revenue recognition issues.

Before extending credit or long-term contracts: Indian companies in sectors with long credit cycles (infrastructure, real estate, textiles) often diverge sharply between accrual profit and actual cash generation. A potential partner's cash flow statement reveals whether reported profits translate to real liquidity.

Seasonal revenue patterns (agriculture, festive-driven consumer goods), extended trade credit terms (90–120 days in B2B sectors), and GST refund delays all widen the gap between P&L profit and operating cash flow. Singapore businesses should benchmark cash conversion cycles against Indian sector norms — infrastructure and textiles, for instance, routinely run debtor days well above what Singapore B2B relationships would signal as a warning.

What Singapore Businesses Need Before Reading Indian Cash Flow Statements

Confirm Familiarity with Ind AS 7 Basics

Unlike Singapore's SFRS(I) 7 (identical to IAS 7 with no modifications), Ind AS 7 mandates the indirect method in practice and requires separate disclosure of interest paid and taxes paid—line items may appear in unfamiliar positions for Singapore readers.

Key comparison:

| Feature | Ind AS 7 (India) | SFRS(I) 7 (Singapore) |

|---|---|---|

| Financial year | April 1 - March 31 (mandatory) | Entity's choice (flexible) |

| Operating method | Indirect (near-universal practice) | Direct or indirect (both permitted) |

| Interest paid | Operating OR Financing (entity's choice) | Operating OR Financing (entity's choice) |

| Tax payments | Operating (unless linked to investing/financing) | Operating (unless linked to investing/financing) |

Where to Source Indian Financial Statements

Always obtain the complete audited annual report — not just the standalone cash flow page. Indian companies file audited financials with:

- MCA21 Portal (Ministry of Corporate Affairs): All companies, including private unlisted entities

- BSE/NSE (stock exchanges): Listed companies

- SEBI: Regulatory filings for listed entities

Always use source documents from these official portals rather than third-party aggregators where data can be restated without notice.

When to Involve a Local Ind AS Expert

Engage a local Indian accounting advisor with Ind AS expertise before making high-stakes decisions based on a first reading. A qualified Ind AS specialist can provide context that the numbers alone won't show, including:

- Distinguishing routine advance tax outflows from genuine liquidity stress

- Flagging non-cash items (like ESOP charges) inflating operating profit adjustments

- Interpreting entity-specific classification choices for interest and dividends

VJM Global's India-based Chartered Accountants work directly with foreign businesses entering India, helping Singapore clients interpret Ind AS-compliant statements with the local regulatory context that a remote reading cannot provide.

Key Sections of an Indian Cash Flow Statement Under Ind AS 7

All three activities are interlinked and must be read together. A company can show strong operating cash flow but face financial stress if its financing section reveals unsustainable debt levels.

Operating Activities

Positive operating cash flow is the clearest indicator of business health — it shows the company generates enough cash from core activities to self-fund operations without relying on borrowings or asset sales.

Conversely, consistently negative operating cash flow in a non-startup Indian company warrants investigation into:

- Working capital mismanagement (rising receivables, inventory build-up)

- Aggressive revenue recognition not backed by cash collection

- GST ITC blockage (check notes to accounts for blocked credit amounts)

Singapore readers should note: Indian indirect-method statements frequently include large add-backs for depreciation (Indian companies sometimes use aggressive depreciation schedules) and provisions. This can inflate operating cash flow relative to what IFRS-familiar readers expect from direct-method presentations. Always calculate the Operating Cash Flow to Net Profit ratio to assess earnings quality.

Investing Activities

For growing Indian companies, negative investing cash flow is expected — and normal. India recorded USD 81.04 billion total FDI in FY 2024-25, with Singapore contributing 30% as the largest source country. Manufacturing FDI grew 18%, driving capital expenditure cycles across the economy.

Typical investing outflows include:

- CAPEX on property, plant, equipment

- Technology and infrastructure investments

- Purchases of financial assets or equity stakes in associates

Red flag: Unexplained large outflows toward "investments in subsidiaries" or "intercorporate deposits" in Indian group structures. The IL&FS case demonstrated how circular lending through 300+ subsidiaries masked true liquidity. Cross-reference with related-party disclosures and verify compliance with Section 186 limits.

Financing Activities

Positive financing cash flow signals capital raising — either equity or debt. For Singapore businesses monitoring an Indian subsidiary, sustained financing inflows despite positive operating cash flow may indicate:

- The parent is not fully utilising locally generated cash

- The Indian entity is being over-leveraged to fund group needs

- Cash is trapped due to regulatory restrictions or tax inefficiency

Dividend repatriation: Dividends to foreign shareholders appear here (if classified as financing). Under the India-Singapore DTAA Article 10, withholding tax is capped at 10% for ≥25% equity holding, or 15% otherwise.

Singapore parent companies should verify that dividend outflows reconcile with planned repatriation and comply with RBI's FEMA requirements. Current account transactions require no prior approval, but documentation via Forms 15CA/15CB is mandatory.

Key Metrics to Extract from an Indian Cash Flow Statement

Raw figures are less useful than derived ratios. Calculate at least three core metrics:

Operating Cash Flow to Net Profit Ratio

Formula: Operating Cash Flow ÷ Net Profit After Tax

Benchmark: A ratio consistently ≥1.0 indicates high earnings quality (cash-backed profits). Ratios well below 1.0 in non-growth-phase companies suggest:

- Aggressive revenue recognition

- Poor cash collection (rising receivables)

- Working capital tied up in inventory or blocked GST credits

CRISIL Ratings uses Net Cash Accrual to Total Debt (NCATD) as the primary cash adequacy measure but explicitly states it "does not adopt an arithmetic approach"—industry context matters more than fixed thresholds.

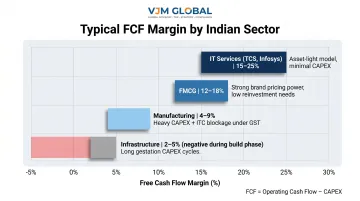

Free Cash Flow (FCF)

Formula: Operating Cash Flow − Capital Expenditure

FCF is the most direct measure of financial flexibility for an Indian operating company — and the figure Singapore investors should anchor on when valuing a potential acquisition.

| Sector | Typical FCF Margin (% of Revenue) |

|---|---|

| IT Services (TCS, Infosys) | 15–25% (asset-light model) |

| FMCG | 12–18% |

| Manufacturing | 4–9% (heavy CAPEX, ITC blockage) |

| Infrastructure | 2–5% (negative during build phase) |

The IT services gap stands out: companies like TCS and Infosys convert roughly 80–100% of net income to free cash, reflecting asset-light operations with minimal CAPEX. Capital-intensive sectors compress FCF from two directions simultaneously — heavy capital expenditure requirements and GST working capital blockage that can tie up cash for months.

Cash Conversion Cycle Implications

Changes in working capital line items (trade receivables, inventories, trade payables) reveal how efficiently an Indian company converts sales to cash.

One pattern worth flagging: Indian B2B markets already operate on credit terms of 90–120 days — well above the 30–60 day norms Singapore businesses typically see. If receivables grow faster than revenue for two consecutive periods, that gap is widening, not normalizing. Dig into customer creditworthiness and collection processes before drawing conclusions about profitability.

Common Mistakes Singapore Businesses Make When Reading Indian Cash Flow Statements

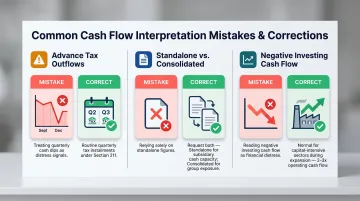

Treating Advance Tax Outflows as a Red Flag

Singapore businesses unfamiliar with India's advance tax system often misread September and December cash outflows as distress signals. These are routine, non-discretionary quarterly payments mandated by Section 211 of the Income Tax Act, 1961. They appear in every Indian company's operating section regardless of financial health.

Ignoring the Standalone vs. Consolidated Distinction

Indian holding companies must file both standalone and consolidated statements (Companies Act Section 129(3)). Singapore investors evaluating an Indian group sometimes rely on standalone figures, which exclude subsidiary performance. This omission can distort total cash generation figures and hide group-level debt exposure.

To avoid this:

- Request the consolidated statement for group-level cash assessment

- Request the standalone statement when evaluating a specific subsidiary's cash position

Misinterpreting Negative Investing Cash Flow as Distress

Indian manufacturing, infrastructure, and energy businesses are capital-intensive in ways that don't map to Singapore's asset-light or trading models. Negative investing cash flow of 2–3x operating cash flow is normal during expansion phases. Evaluate it alongside:

- Management CAPEX guidance and sector benchmarks

- Gross Fixed Capital Formation trends (India's GFCF grew 7.1% in FY 2024-25)

- Industry-specific investment cycles

Frequently Asked Questions

How do I read a statement of cash flow?

Start with the Operating Activities section to assess core business cash generation. Verify that operating cash flow is positive and supported by the P&L. Then review Investing Activities for capital allocation decisions and Financing Activities for debt/equity structure. Finally, reconcile the net movement to the balance sheet cash position to confirm accuracy.

Is a higher or lower cash flow better?

Higher operating cash flow is generally better as it indicates strong cash generation from core business. However, negative investing cash flow can be positive if driven by productive CAPEX in a growth phase. Negative operating cash flow is a concern for established (non-startup) companies and signals working capital or collection issues.

What is cash flow analysis as per IND AS 7?

Ind AS 7 is India's cash flow standard, aligned with IAS 7 under IFRS, requiring companies to classify cash flows into Operating, Investing, and Financing activities. The indirect method — starting with Profit Before Tax and adjusting for non-cash items and working capital changes — is used almost universally for the operating section.

How does India's Ind AS 7 differ from Singapore's SFRS(I) 7 for cash flow reporting?

Both standards converge with IFRS, but India's mandatory April–March financial year, near-universal use of the indirect method, and India-specific line items (advance tax installments, GST working capital adjustments) differ from Singapore practice. These variations affect how Singapore businesses interpret timing and cash flow classification.

What are red flags in an Indian company's cash flow statement?

Key warning signs include: consistently negative operating cash flow, large unexplained "intercorporate deposit" outflows in the investing section, a persistent gap between reported net profit and operating cash flow (OCF/NP ratio <0.7 for two+ periods), and rapid growth in trade receivables without corresponding cash collection. Cross-reference with related-party disclosures.

Can Singapore businesses repatriate profits from India and where does this appear in the cash flow statement?

Dividend repatriation appears under Financing Activities and is freely permitted under FEMA. Withholding tax under the India-Singapore DTAA is 10% (for ≥25% equity) or 15% otherwise. Loan repayments show in Financing Activities; royalty payments fall under Operating Activities — both subject to RBI and FEMA compliance.

VJM Global's India-based Chartered Accountants work directly with Singapore businesses interpreting Ind AS-compliant financials. Services include:

- Due diligence and financial statement review

- Subsidiary monitoring and management reporting

- FEMA compliance and repatriation advisory

Contact us at info@vjmglobal.com to discuss your India investment or partnership.