Introduction

Choosing between cash and accrual accounting affects far more than day-to-day bookkeeping: it shapes tax obligations, financial reporting accuracy, and access to funding. For UK business owners, the wrong choice can obscure true profitability and complicate growth planning.

From the 2024/25 tax year, HMRC made cash basis the default method for calculating trading profits for all eligible sole traders and partnerships. This regulatory shift, enacted through Finance Act 2024, affects approximately 3.57 million unincorporated businesses across the UK — so understanding which method suits your business has never mattered more.

Key Takeaways

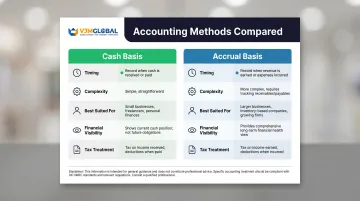

- Cash basis records income when payment is received and expenses when bills are paid; accrual records them when earned or incurred, regardless of payment timing

- Sole traders and small partnerships can use cash basis; limited companies must use accrual under UK GAAP or FRS 102

- From 6 April 2024, cash basis became the default for eligible sole traders and partnerships—businesses must actively opt out via Self Assessment to use accrual accounting

- Banks and investors favour accrual-based accounts when evaluating loan or investment applications

- If you're planning to scale, raise finance, or take on investors, accrual accounting gives you a stronger foundation from the start

Cash vs Accrual Accounting: Quick Comparison

| Aspect | Cash Basis | Accrual Basis |

|---|---|---|

| Timing of recording | When money changes hands | When earned or incurred (invoice issued/bill received) |

| Complexity | Simpler — no tracking of receivables or payables | More complex — requires tracking all outstanding amounts |

| Best suited for | Sole traders, freelancers, small partnerships | Limited companies, inventory businesses, those seeking finance |

| Financial visibility | Bank account view (actual cash position) | Economic reality (earnings and obligations) |

| Tax treatment | Tax due only on received income | Tax due on invoiced income, even if unpaid |

| UK regulatory compliance | Default for sole traders/partnerships from 2024/25 | Required for limited companies under Companies Act 2006 |

The key distinction is timing: cash basis records when money moves, while accrual records when it's earned or owed — regardless of when payment arrives.

One important caveat: a hybrid approach (cash basis for some transactions, accrual for others) is not recognised for UK tax purposes and must be managed carefully if used in practice.

What is Cash Basis Accounting?

Cash basis accounting records income when payment is received and expenses when bills are paid. Transactions are only logged when cash actually changes hands—no accounts receivable or payable are tracked until payment occurs. GOV.UK defines it simply: "you only record income or expenses when you receive money or pay a bill."

For small UK businesses, the operational benefits are tangible:

- Simpler bookkeeping with fewer records to maintain

- Lower administrative overhead

- Real-time view of available funds

This makes cash basis particularly useful for businesses with irregular income or tight cash flow, where knowing exactly what's in the bank drives day-to-day decisions.

The 2024/25 HMRC Change

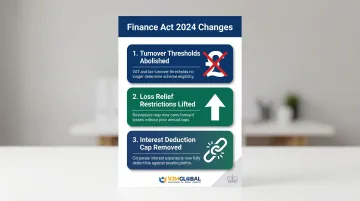

From 6 April 2024, cash basis became the default accounting method for eligible sole traders and partnerships. Under Finance Act 2024, Section 16 and Schedule 10 — which amended the Income Tax (Trading and Other Income) Act 2005 — three major changes took effect:

Turnover thresholds abolished — The previous entry threshold of £150,000 and exit threshold of £300,000 were removed entirely. Any sole trader or qualifying partnership can now use cash basis regardless of turnover.

Loss relief restrictions lifted — Cash basis losses can now be offset sideways against other income or carried back under early-years relief, aligning fully with accruals basis (sideways relief under s64 ITA 2007; early-years relief under s72 ITA 2007).

Interest deduction cap removed — The previous £500 annual cap on interest deductions was eliminated, benefiting businesses with significant borrowing costs.

Businesses must now opt out when filing Self Assessment if they prefer traditional accounting—the election under s25C ITTOIA 2005 remains in effect until revoked.

Practical example: A UK freelance graphic designer invoices a client £2,000 in March 2025 and receives payment in May 2025. Under cash basis, that £2,000 is recorded as May income (falling in the 2025/26 tax year), not March. The tax obligation follows the cash receipt, not the invoice date.

Use Cases of Cash Basis Accounting

Cash basis works best for:

- Sole traders and freelancers with straightforward transactions and minimal credit arrangements

- Service-based businesses without significant stock or inventory to track

- Seasonal businesses where aligning tax payments to actual cash receipts eases pressure during slow periods

- Businesses with irregular income that benefit from simplified month-to-month bookkeeping

Cash basis is not suitable when:

- The business holds large inventory (stock adjustments aren't captured)

- Seeking bank financing—lenders typically want accrual-based statements showing full assets and liabilities

- Dealing with significant debtors or creditors that distort the cash position

- Required to follow UK GAAP, FRS 102, or FRS 105

What is Accrual Accounting?

Accrual accounting records income when it is earned (when an invoice is issued) and expenses when they are incurred (when a bill is received)—regardless of when cash actually moves. It captures financial commitments at any given time, including amounts owed by customers (accounts receivable) and amounts owed to suppliers (accounts payable).

For UK businesses, this method enables accurate profit and loss reporting by period, supports reliable cash flow forecasting, and provides the detailed financial statements that investors, lenders, and auditors require.

UK Compliance Context

Limited companies are required by law to use accrual accounting. Section 393 of the Companies Act 2006 requires directors to prepare accounts giving a "true and fair view" of assets, liabilities, financial position, and profit or loss—which inherently requires accrual-based accounting. Limited companies and LLPs cannot use cash basis; they must prepare accounts under UK GAAP (FRS 102 or FRS 105) or UK-adopted IFRS for publicly listed companies.

Accounting framework by company size (from 6 April 2025):

- Micro-entities: Turnover up to £1 million, balance sheet up to £500,000—can apply FRS 105

- Small companies: Turnover up to £15 million, balance sheet up to £7.5 million—typically apply FRS 102

- Medium companies: Turnover up to £54 million, balance sheet up to £27 million—apply FRS 102

- Listed companies: Must use UK-adopted IFRS for consolidated accounts

Practical example: The same freelance designer invoicing £2,000 in March 2025 would record that income in March under accrual accounting, even if payment arrives in May. This results in a different profit figure for March versus cash basis and creates a potential tax obligation on income not yet received in cash.

Use Cases of Accrual Accounting

Accrual accounting is essential for:

- Limited companies and LLPs (legally required under Companies Act 2006)

- Businesses with inventory that need to track stock value and cost of goods sold

- Firms seeking loans or investment—banks and investors assess true revenue and outstanding obligations from accrual-based statements

- Businesses with long-term contracts, retainer arrangements, or subscription models

- Companies planning for acquisition, expansion, or raising capital

Cash vs Accrual Accounting: Which is Right for Your UK Business?

Key Decision Factors

Evaluate these dimensions:

- Legal structure: Sole trader or partnership vs limited company

- Business complexity: Simple transactions vs complex contracts or inventory

- Credit transactions: Volume of invoicing and payment delays

- External financing needs: Seeking loans, investment, or remaining self-funded

- Growth trajectory: Staying small vs planning expansion or acquisition

Situational Guidance

Choose cash basis if you:

- Are a sole trader or small partnership with simple transactions

- Have no significant stock or inventory

- Want straightforward Self Assessment filing with minimal administrative burden

- Operate on a cash-in, cash-out model with minimal credit arrangements

Choose accrual if you:

- Operate as a limited company (legally required)

- Hold inventory that fluctuates in value

- Seek bank loans or investment (lenders require accrual-based statements)

- Need period-accurate financial reporting for management decisions

- Plan for growth, acquisition, or exit

Tax Timing Differences

Under cash basis, tax is only due on received income. If you invoice £5,000 in December 2024 but receive payment in January 2025, that income falls in the 2025/26 tax year. Under accrual, December income is taxable in the 2024/25 tax year regardless of when payment arrives. For businesses with slow-paying clients, this timing gap can create real cash flow strain.

Switching Considerations

Switching between methods requires transitional adjustments. HMRC guidance (BIM70065) specifies three adjustment categories:

- Debtors: Deduct amounts already taxed under accruals but received as cash in the first cash basis year, to avoid double taxation

- Creditors: Deduct amounts already relieved under accruals but paid in the first cash basis year

- Trading stock: Add closing stock value from the final accruals year to cash basis purchases so the cost is fully relieved

Inform HMRC by declaring your chosen method on your Self Assessment return. It stays in effect until you actively elect to switch back.

Transitioning between methods incorrectly can trigger HMRC compliance issues. VJM Global has worked with 250+ UK businesses on accounting outsourcing and compliance, including method switches and Self Assessment filings.

Conclusion

Cash basis suits simplicity-first businesses: sole traders, freelancers, and small partnerships without complex credit arrangements benefit from reduced admin burden and tax aligned to actual receipts. Accrual accounting is the standard for businesses with regulatory obligations or growth ambitions. It provides the complete financial picture that lenders, investors, and strategic planning require.

Your choice of method affects more than recordkeeping. It determines how you report tax, attract funding, and manage cash flow as your business evolves. Consider which factors apply to your situation:

- Turnover and HMRC eligibility — cash basis is only available below the £150,000 threshold

- Credit terms — businesses with significant receivables or payables need accrual's accuracy

- Growth plans — lenders and investors expect accrual-based accounts

- Complexity — VAT-registered businesses and limited companies are generally required to use accrual

If you need guidance on selecting or transitioning between methods, VJM Global's team of Chartered Accountants and CPAs supports UK businesses with outsourced accounting and bookkeeping services, helping you maintain accurate records and stay compliant as your business grows.

Frequently Asked Questions

Is it better to use cash or accrual accounting?

Neither is universally better—cash basis offers simplicity and is the default for UK sole traders from 2024/25, while accrual provides more accurate financial insight and is required for limited companies. The best choice depends on your business structure, complexity, and growth plans.

What accounting method does the UK use?

The UK uses both. Cash basis is the default for eligible sole traders and partnerships from 2024/25, while limited companies and businesses following UK GAAP (FRS 102/FRS 105) must use accrual accounting. Publicly listed companies follow UK-adopted IFRS.

Can you change from cash accounting to accrual in the UK?

Yes, businesses can switch methods, but must account for transitional adjustments (recognising outstanding receivables and payables at the transition point) and reflect the change in their Self Assessment or statutory accounts. An accountant can help ensure a clean, compliant transition.

Does the UK use GAAP or IFRS?

UK-incorporated companies typically follow UK GAAP (primarily FRS 102), while publicly listed companies on UK stock exchanges are required to use UK-adopted IFRS for consolidated accounts. Both frameworks require accrual accounting.

Who can use cash basis accounting in the UK?

From 6 April 2024, cash basis is the default for sole traders and partnerships (without corporate partners) filing Self Assessment. Limited companies, LLPs, and businesses with more complex structures are ineligible and must use accrual accounting.

What are the main disadvantages of cash basis accounting for UK businesses?

Cash basis doesn't capture accounts receivable or payable, which can misrepresent profitability in a given period. It's also not compliant with UK GAAP, and lenders typically prefer accrual-based statements showing full assets and liabilities — which can limit access to bank financing.