This guide will walk you through what cash basis accounting is, how it differs from traditional (accruals) accounting, who can and cannot use it, the major rule changes from the 2024/25 tax year, and the key pros and cons — so you can confidently choose the best accounting method for your Self Assessment return.

Key Takeaways

- Cash basis records income when you receive payment and expenses when you pay them — not when invoices are raised or received

- It became the default method for UK sole traders and partnerships from 6 April 2024

- Limited companies, LLPs, and partnerships with corporate partners cannot use cash basis

- April 2024 also removed turnover thresholds, lifted the £500 interest deduction cap, and scrapped loss relief restrictions

- Choosing between cash basis and traditional accounting can shift when your tax bill falls due — worth reviewing before your next Self Assessment

What is Cash Basis Accounting in the UK?

Cash basis accounting is a simplified method of recording business income and expenses. Under this method, income is recognised only when payment is physically received, and expenses are recorded only when they are actually paid — not when the invoice was issued or received.

This approach is used by sole traders and partnerships to calculate taxable profits for Self Assessment tax returns. Crucially, it means you pay no Income Tax on money you haven't yet received.

HMRC introduced cash basis accounting in April 2013 as an optional simplified method. From the 2024/25 tax year onwards, it became the default method — meaning businesses no longer need to opt in. If you prefer traditional accounting, you now need to actively opt out on your Self Assessment return.

Practical Example: Cash Basis in Action

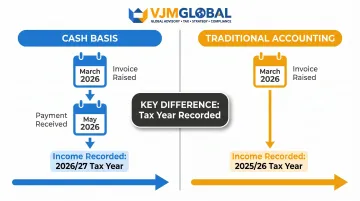

Let's say you're a freelance graphic designer. You invoice a client £1,500 in March 2026 (which falls in the 2025/26 tax year), but the client pays you in May 2026 (which falls in the 2026/27 tax year).

Under cash basis:

- The £1,500 income is recorded in the 2026/27 tax year (when you actually receive payment)

- You won't pay tax on this income until your 2026/27 Self Assessment return

Under traditional accounting:

- The £1,500 would be recorded in the 2025/26 tax year (when you raised the invoice)

- You'd pay tax on it a year earlier — even though you hadn't received the money yet

The timing difference extends to expenses too. Under cash basis, most capital equipment purchases — except land, buildings, and cars — can be treated as a direct expense in the year you pay for them. This removes the need to calculate capital allowances. Cars are the exception: they still require capital allowances to be claimed separately.

Cash Basis vs. Traditional (Accruals) Accounting in the UK

Traditional accounting — also known as accruals basis — records income and expenses at the point an invoice is raised or received, regardless of when cash changes hands. This is the alternative method businesses can elect to use by opting out of cash basis on their Self Assessment return.

The Core Difference

The core difference comes down to timing:

- Accruals accounting matches income and costs to the period they are "earned" or "incurred"

- Cash basis ties everything to actual cash movement

Under accruals, businesses must account for:

- Debtors (money owed to you)

- Creditors (money you owe)

- Prepayments (advance payments)

- Accruals (expenses incurred but not yet paid)

- Closing stock at year-end

As outlined in HMRC's MTD guidance, none of these adjustments are required under cash basis — making record-keeping significantly simpler.

Key Differences at a Glance

| Feature | Cash Basis | Traditional (Accruals) |

|---|---|---|

| Income recorded | When payment received | When invoice raised |

| Expenses recorded | When payment made | When invoice received |

| Year-end adjustments | None required | Debtors, creditors, prepayments, accruals, stock |

| Capital equipment | Direct expense (except cars, land, buildings) | Capital allowances |

| Loss relief | Full flexibility (from 2024/25) | Full flexibility |

| Best suited for | Service businesses, simple cash flows | Stock-heavy businesses, complex credit terms |

When Traditional Accounting May Be Better

Traditional accounting may be the better choice if you:

- Hold significant stock levels (retailers, manufacturers)

- Operate complex credit arrangements

- Seek finance (banks often prefer accruals-based accounts showing debtors and creditors)

- Deal in securities or claim mineral royalties

- Need to track business performance more precisely when there are timing gaps between invoicing and payment

That said, uptake of cash basis was historically low. Before 6 April 2024, only around 1.2 million of 4.2 million eligible businesses used it — roughly 29%. Most stuck with traditional accounting due to interest deduction limits and loss relief restrictions, both of which have since been removed.

Important: If you choose traditional accounting, you must declare this on your Self Assessment return.

Who Can and Cannot Use Cash Basis Accounting in the UK?

Who Is Eligible

You can use cash basis if you are:

- A sole trader

- A partnership where all partners are individuals

From 2024/25, there are no turnover thresholds — any unincorporated business, regardless of size, can use cash basis as the default.

Businesses with multiple trades can now choose cash basis independently for each trade. Previously, if you had more than one business, you had to apply the same method across all of them.

Hard Exclusions (Entity Types)

You cannot use cash basis if your business is a:

- Limited company

- Limited liability partnership (LLP)

- Partnership with one or more corporate partners

There are no exceptions for these structures.

Specific Business Types Excluded

You also cannot use cash basis if you are:

- A Lloyd's underwriter

- A farming business with a current herd basis election

- A farming or creative business with a fluctuating profit averaging claim

- A business that has claimed Business Premises Renovation Allowance within the previous 7 years

- A business carrying on a mineral extraction trade

- A business that has ever claimed Research and Development Allowance

Businesses Where Cash Basis Is Not Suitable

Some businesses can technically opt in, but doing so would disqualify them from tax reliefs specific to their trade, including:

- Dealers in securities

- Mineral royalty relief claimants

- Lease premium businesses

- Ministers of religion

- Pool betting duty payers

- Managed service companies

- Intermediaries treated as making employment payments

- Waste disposal businesses

- Cemeteries or crematoria

If You Cannot Use Cash Basis

If excluded, you must use traditional accounting. That means:

- Declaring traditional accounting on your Self Assessment

- Maintaining stock valuations and accruals records

- Tracking debtors and creditors separately

Key Cash Basis Accounting Changes from the 2024/25 Tax Year

The 2024/25 tax year brought three major changes to cash basis accounting, making it more flexible and accessible for a wider range of businesses.

Default Method Shift

Before 6 April 2024: Traditional accounting was the default. Businesses had to elect to use cash basis.

From 6 April 2024: Cash basis is the default. Businesses must actively elect to use traditional accounting instead.

Turnover thresholds removed entirely:

- Previous entry threshold: £150,000 (£300,000 for Universal Credit claimants)

- Previous exit threshold: £300,000

- Current thresholds: None

Any eligible business, regardless of size, can now use cash basis.

The default shift alone expanded access considerably. But two further restrictions — on interest deductions and loss relief — were also removed at the same time.

Removal of the £500 Interest Deduction Cap

Previously, cash basis users could only deduct up to £500 per year in interest and financing costs. This restriction dated back to 2013 and made cash basis unviable for businesses with significant borrowing. An estimated 98,000 taxpayers avoided cash basis specifically because of this cap.

From 6 April 2024: This cap is removed. Businesses can now deduct all interest and financing costs that are wholly and exclusively for business purposes.

Practical example:

| Before 6 April 2024 | From 6 April 2024 | |

|---|---|---|

| Annual interest (£20k loan @ 6%) | £1,200 | £1,200 |

| Deductible amount | £500 | £1,200 |

| Non-deductible (added to taxable profit) | £700 | £0 |

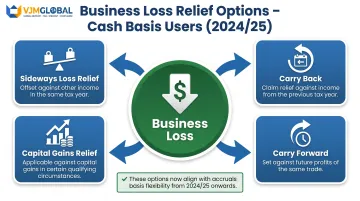

Removal of Loss Relief Restrictions

Previously, cash basis users could only carry losses forward against future profits of the same trade. Approximately 94,000 taxpayers chose accruals specifically to access sideways loss relief.

From 2024/25: Cash basis losses can now be relieved in the same ways as accruals basis losses, including:

- Sideways loss relief — offset against other income in the same tax year

- Carry back — relief against the previous tax year

- Relief against capital gains — in certain circumstances

- Carry forward — against future profits of the same trade

For start-ups and businesses with uneven income, this removes one of the main reasons to choose accruals over cash basis.

Estimated impact: These changes are expected to benefit 250,000 businesses that move into using cash basis as a result.

Pros and Cons of Cash Basis Accounting for UK Businesses

Advantages

Cash basis accounting offers several practical benefits, particularly for smaller sole traders and freelancers:

- Simpler record-keeping — no need to track debtors, creditors, prepayments, or accruals at year-end; your records align directly with your bank statements

- No Income Tax on unpaid invoices — tax liability only arises when you actually receive payment, which improves cash flow

- Capital equipment as a direct expense — most equipment (excluding cars, land, and buildings) can be deducted in the year paid, removing the need to calculate capital allowances

- Flexible loss relief — from 2024/25, you can offset losses sideways, carry them back, or carry them forward, matching the flexibility of traditional accounting

Best suited for:

- Freelancers and consultants

- Tradespeople (plumbers, electricians, builders)

- Service-based sole traders

- Businesses with straightforward, predictable cash flows

That said, cash basis isn't the right fit for every business. Here are the key limitations to weigh up:

Disadvantages and Limitations

- Not available to all business types — limited companies, LLPs, and partnerships with corporate partners are excluded, as are certain specialist businesses

- May not reflect true financial performance — large volumes of outstanding debtors or creditors can distort reported profits, since timing gaps between invoicing and payment aren't captured

- Less useful for raising finance — banks and lenders typically prefer accruals-based accounts; cash basis accounts don't show debtors as assets

- Problematic for stock-heavy businesses — retailers, wholesalers, and manufacturers may find cash basis misrepresents profitability, as closing stock isn't tracked as an asset

- VAT accounting is separate — cash basis for Income Tax is distinct from VAT accounting; if you're VAT-registered and considering the VAT Cash Accounting Scheme (£1.35 million turnover threshold), the two schemes operate independently

If you're unsure which method suits your business, VJM Global works with 250+ UK businesses on accounting compliance and can help you choose the right approach for your circumstances.

Frequently Asked Questions

Who can use cash basis accounting in the UK?

Sole traders and partnerships (without corporate partners) can use cash basis as the default from 2024/25, regardless of turnover. Limited companies, LLPs, Lloyd's underwriters, mineral extraction trades, and businesses with certain allowance claims cannot use it.

How does cash basis accounting differ from accrual (traditional) accounting in the UK?

Cash basis records income and expenses when cash is received or paid, while traditional (accruals) accounting records them when the invoice is issued or received. This means under accruals, you may pay tax on income not yet received and cannot deduct expenses not yet paid.

What types of accounting methods are used in the UK?

The two main methods for unincorporated businesses are cash basis accounting (default from 2024/25) and traditional accounting (accruals basis). Limited companies are required to use accruals-based accounting under UK GAAP or FRS standards.

What changed about cash basis accounting in the 2024/25 tax year?

Four significant changes took effect from 2024/25:

- Cash basis became the default (opt-out rather than opt-in)

- All turnover thresholds were removed

- The £500 interest deduction cap was lifted

- Loss relief rules were aligned with accruals basis, allowing sideways relief, carry back, and relief against capital gains

Can I switch from cash basis to traditional accounting?

Yes, you can switch by making an election on your Self Assessment return. However, transitional adjustment rules apply to ensure income and expenses are only taxed or relieved once. Any additional income arising from the switch is spread over six years for tax purposes.

Is cash basis accounting suitable for VAT-registered businesses?

Yes, VAT-registered businesses can use cash basis for Income Tax purposes. However, how income is recorded may affect Making Tax Digital for Income Tax obligations. The VAT Cash Accounting Scheme (with its own £1.35 million turnover threshold) is a separate scheme from income tax cash basis.