Introduction

From 6 April 2024, HMRC made cash basis the default accounting method for sole traders and partnerships — meaning businesses must now actively elect accruals (traditional) accounting if they want to use it. For many business owners, this regulatory reversal has brought the differences between the two methods into sharp focus.

Understanding which method applies to you is not just a bookkeeping decision. Your choice affects tax compliance, financial reporting accuracy, access to finance, and your ability to scale. The wrong choice can trigger unexpected tax bills, undermine credibility with lenders, or breach Companies Act 2006 requirements.

This article explains what the accruals basis is, how it compares to cash basis, who must use it under UK rules, and the practical implications of switching between methods.

TLDR:

- Accruals basis records income when earned and expenses when incurred — not when cash changes hands

- From 6 April 2024, cash basis became the default for sole traders; accruals basis now requires active election

- All UK limited companies must use accruals basis under Companies Act 2006, UK GAAP, or IFRS

- Businesses with inventory must use accruals basis; it is also standard for securing finance and long-term planning

- Switching methods triggers HMRC transitional adjustments to prevent double-counting

What is the Accruals Basis of Accounting in the UK?

The accruals basis (also called traditional accounting) records income when it is earned and expenses when they are incurred—regardless of when cash actually changes hands. HMRC Helpsheet HS222 states: "traditional accounting (accruals basis) - you record income when you invoice your customers and expenses when you receive a bill."

HMRC and UK accounting standards all recognise accruals as the required basis for statutory accounts. This includes:

- UK GAAP — the domestic framework for most limited companies

- FRS 102 — the standard for small and medium-sized entities

- IFRS — applied by listed and larger UK companies

Why "Traditional Accounting"?

Historically, accruals basis was the default method for all UK businesses before cash basis was introduced as a simpler option for smaller traders. The two terms—accruals basis and traditional accounting—are used interchangeably in HMRC guidance and UK law.

Practical Example

A sole trader invoices a customer on 31 March 2026. Under accruals basis, that invoice counts as sales income for that accounting year—even if the customer hasn't paid yet.

The same logic applies to expenses. Insurance paid in October covering the following six months should only be partially included as an expense in the current year—specifically the portion running from October through year-end.

This has a direct impact on your balance sheet: under accruals, outstanding debtors and unpaid creditors both appear as line items. Under cash basis, neither does—only actual cash movements are recorded. The difference affects both tax liability timing and the accuracy of your financial picture.

Cash Basis vs. Accruals Basis: Key Differences Explained

From 6 April 2024, cash basis became the default method for sole traders and partnerships (without corporate partners) filing Self Assessment returns. Businesses must now actively elect to use traditional accounting if they prefer it.

Here's how the two methods compare:

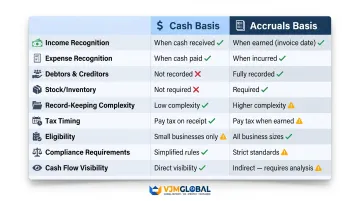

| Factor | Cash Basis | Accruals Basis |

|---|---|---|

| Income recognition | Only when cash received | When invoice raised/earned |

| Expense recognition | Only when cash paid | When bill received/incurred |

| Debtors & creditors | Not recorded | Appear on balance sheet |

| Stock/inventory | Expensed when purchased | Only cost of goods sold expensed; unsold stock is an asset |

| Record-keeping complexity | Simpler, fewer adjustments | More complex: requires tracking prepayments, accruals, debtors, creditors |

| Tax timing | Tax on income received in year | Tax on income earned in year, regardless of payment |

| Who can use it | Sole traders and partnerships (individuals only) | All businesses; mandatory for limited companies |

| Compliance requirements | Cannot meet FRS 102/105 or IFRS | Required for Companies Act 2006 statutory accounts |

| Cash flow visibility | High—shows actual cash position | Lower—can show profit while cash is tight |

The table captures the mechanics — but three differences tend to drive most business decisions: tax timing, stock treatment, and eligibility. Here's what each means in practice.

Tax Timing Implications

Under cash basis, a business that invoices a client in March but receives payment in June only pays tax on that income in the following tax year. Under accruals basis, the income is taxed in the year the invoice was raised, regardless of when payment arrives.

Stock Treatment

Under cash basis, goods purchased for resale are treated as an expense when paid for. Under accruals basis, only the cost of goods actually sold counts as an expense — unsold stock sits on the balance sheet as an asset.

For businesses carrying significant stock, this distinction affects both reported profit and tax liability. Accruals basis gives a more accurate picture of what's actually been consumed versus what remains.

Which Method Suits Which Business?

Cash basis suits:

- Simple, cash-transaction-based sole traders

- Small partnerships with minimal credit sales

- Businesses with low or no stock

Accruals basis is appropriate (or mandatory) for:

- All UK limited companies

- Businesses seeking bank finance or investment

- Businesses with stock or long-term contracts

- Businesses planning to scale

- Statutory accounts under UK GAAP (FRS 102/FRS 105) or IFRS

Core Principles of Accruals Accounting

Two fundamental principles underpin the accruals basis: revenue recognition and matching.

The Revenue Recognition Principle

Revenue is recorded in the accounting period in which it is earned—when the business has fulfilled its obligation to the customer—not when cash is received.

Example: A consultancy completes a project in March, invoices the client in March, and records revenue in March—even if payment arrives in May.

The Matching Principle

Expenses are recognised in the same period as the revenue they help generate. If a business buys materials in September to fulfil a contract completed in September, those costs are recorded in September—even if the supplier's invoice isn't paid until October.

This ensures each period's profit figure reflects what was actually earned and spent—not just what moved through the bank account.

Why These Principles Matter

Both principles work together to produce financial statements that reflect economic reality rather than cash flow. They underpin UK GAAP (FRS 102 and FRS 105) and IFRS, which is why accruals accounting is mandated for statutory reporting by limited companies and larger businesses in the UK.

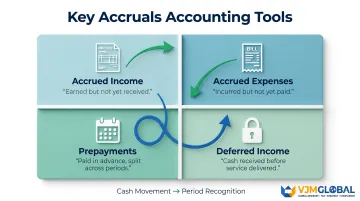

Four Practical Tools in Accruals Accounting

Accruals accounting uses four key adjustments to match income and expenses to the correct period:

- Accrued income: Revenue earned but not yet invoiced or received—recorded as a debtor. An invoice raised in March for completed work, with payment due in April, is recognised in March.

- Accrued expenses: Costs incurred but not yet paid—recorded as a creditor. A supplier bill arriving in March but settled in April still hits March's accounts.

- Prepayments: Advance payments for future periods, split across the periods they cover. Annual insurance paid in October is expensed proportionally—only the share falling within the current financial year counts now.

- Deferred income: Cash received before the service is delivered, held as a liability until earned. A six-month retainer paid upfront in February is recognised gradually as each month's work is completed.

HMRC guidance BIM70065 confirms these adjustments are required when switching between accounting methods.

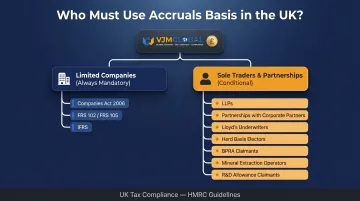

Who Must Use the Accruals Basis in the UK?

The accruals basis is mandatory for some businesses and optional — but often advisable — for others. Here's how the rules break down.

Limited Companies (Mandatory)

All UK limited companies must prepare statutory accounts using the accruals basis under the Companies Act 2006, UK GAAP (FRS 102 or FRS 105 for micro-entities), or IFRS (for listed companies).

Cash basis is not an option for limited companies under any circumstances.

Sole Traders and Partnerships (Conditional)

HMRC guidance BIM72010 lists categories that cannot use cash basis and must use accruals:

- Limited liability partnerships (LLPs)

- Partnerships with one or more corporate partners

- Lloyd's underwriters

- Those with a current herd basis election

- Those that claimed business premises renovation allowance within the previous seven years

- Mineral extraction trade operators

- R&D allowance claimants

Voluntary Election to Use Accruals Basis

Even when cash basis is permitted, accruals is often the stronger choice. Businesses typically elect it when:

- Seeking bank finance (lenders often require accruals-based accounts to assess creditworthiness)

- Planning to scale or attract investment

- Holding significant stock or inventory

- Preparing for Making Tax Digital for Income Tax (MTD ITSA) from 2026/27 onwards

If you're unsure which basis applies to your business — or preparing for MTD ITSA — VJM Global's UK accounting outsourcing team can review your position and handle the transition to accruals-based records.

Pros and Cons of the Accruals Basis

Pros and Cons of the Accruals Basis

Advantages

- Matches income to the period earned, giving a true picture of profitability — critical for assessing performance over time

- Required under UK GAAP (FRS 102/FRS 105), IFRS, and Companies Act 2006; non-compliance risks rejected accounts and legal penalties

- Preferred by banks and investors: GOV.UK notes that lenders often ask for accruals accounts "to see what you owe and are due before agreeing a loan"

- Necessary for businesses with inventory, long-term contracts, or deferred revenue — cash basis simply cannot capture these accurately

Disadvantages

That said, accruals basis comes with real trade-offs — especially for smaller businesses managing accounts without dedicated staff.

- Requires separate tracking of debtors, creditors, prepayments, accruals, and stock, demanding more sophisticated systems

- Can show a profitable business on paper while cash reserves run low — separate cash flow monitoring is essential

- Higher administrative cost: ACCA guidance notes the burden is not significantly lighter under cash basis for most businesses

Switching Between Accounting Methods in the UK

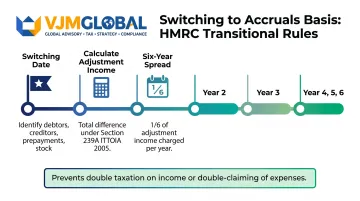

Switching from cash basis to accruals basis (or vice versa) triggers HMRC transitional rules designed to prevent income from being taxed twice or expenses being double-claimed.

Adjustments are made in the first year of the new method to account for any debtors, creditors, prepayments, or stock at the point of switching. When moving from cash basis to accruals, Section 239A of ITTOIA 2005 spreads any adjustment income across six tax years — one-sixth charged per year — preventing a large one-time tax hit.

Practical Steps Required

Once you understand the transitional adjustments, the next question is how to formalise the switch. From 2024/25 onwards, sole traders using the accruals basis must actively elect traditional accounting on their Self Assessment return (or MTD software), since cash basis is now the default.

Process checklist:

- Review your election status each year

- Calculate transitional adjustments for debtors, creditors, prepayments, and stock at the switching date

- Ensure the election is recorded on your Self Assessment return

- Seek professional advice before switching if the change affects loan covenants, investor reporting, or ongoing HMRC compliance

LITRG guidance covers the transitional rules for both directions of switch.

Frequently Asked Questions

What is the accrual basis of accounting in the UK?

The accruals basis (also called traditional accounting) records income when earned and expenses when incurred, regardless of cash movement. It's required for UK limited companies under the Companies Act 2006 and UK GAAP (FRS 102/FRS 105) or IFRS.

Is the UK using IFRS or GAAP?

The UK uses both. Listed companies on UK public markets use UK-adopted IFRS, while most private companies and SMEs use UK GAAP—primarily FRS 102 or FRS 105 for micro-entities. Both require the accruals basis of accounting.

Is it better to do cash basis or accrual basis?

It depends on your business type and size. Cash basis suits simple sole traders and small partnerships for its simplicity and tax deferral benefits. Accruals basis is more accurate, required for limited companies, and better suited to businesses with credit transactions, inventory, or growth plans.

Do limited companies have to use the accruals basis in the UK?

Yes. All UK limited companies must use the accruals basis to prepare statutory accounts under the Companies Act 2006. Cash basis is not an option for limited companies regardless of size.

What changed with cash basis accounting in the UK in 2024?

From 6 April 2024 (the 2024/25 tax year), HMRC made cash basis the default method for sole traders and partnerships filing Self Assessment returns. To continue using the accruals basis, businesses must now actively elect to do so on their Self Assessment return.

Can a sole trader switch from cash basis to accruals basis in the UK?

Yes, sole traders can switch, but HMRC transitional rules apply to prevent double-counting of income or expenses. Sole traders elect the switch on their Self Assessment return, and a spreading adjustment applies over up to six years.