Introduction

Singapore businesses expanding to Dubai face a regulatory environment fundamentally different from what they're accustomed to. ACRA, IRAS, and SFRS give way to the Federal Tax Authority (FTA), EmaraTax portal, and IFRS-based reporting. The stakes for getting it wrong are high: late VAT registration alone carries a penalty of AED 10,000, and late payment of tax incurs a 14% annual interest rate.

Those penalties stem from two major reforms that reshaped Dubai's compliance landscape: VAT introduction in January 2018 and Corporate Tax implementation in June 2023. For foreign companies, professional accounting support is now a practical requirement for staying compliant.

This guide covers UAE compliance requirements, the accounting services most relevant to Singapore businesses, key regulatory differences, and how to choose the right accounting partner in Dubai.

Key Takeaways

- Singapore businesses in Dubai face UAE VAT (5%), Corporate Tax (9% above AED 375,000), and IFRS reporting — all distinct from Singapore's GST and SFRS rules

- FTA non-compliance carries real costs: AED 10,000 for late registration, 14% annual interest on overdue tax, and AED 20,000 for record-keeping failures

- Core services needed: IFRS-compliant bookkeeping, VAT registration and filing via EmaraTax, corporate tax compliance, WPS payroll, and audit preparation

- Your accounting partner should hold FTA registration, carry international experience, and offer cross-border advisory

- Free zone vs. mainland structure directly affects accounting obligations, audit requirements, and tax treatment

Why Singapore Businesses Need Specialized Accounting Support in Dubai

Singapore and Dubai are both business-friendly jurisdictions, but their regulatory infrastructures are distinct. A Singapore business cannot simply apply its home-country accounting processes to Dubai operations without risking non-compliance. Structural choices made at setup — and compliance gaps discovered later — carry real financial consequences.

The choice of business structure—mainland LLC versus free zone company—creates different accounting, audit, and tax obligations that aren't immediately obvious to new entrants. Free zones have specific reporting requirements tied to zone authorities (such as JAFZA or DMCC), while mainland companies face mandatory statutory audits under UAE Commercial Companies Law regardless of revenue size.

Recent Regulatory Changes Create Compliance Complexity

UAE's VAT and Corporate Tax regimes are relatively recent (2018 and 2023 respectively) and expand regularly as the FTA issues updated circulars and decisions. Businesses without dedicated local accounting support risk missing regulatory updates that trigger penalties. For example:

VAT penalties under Cabinet Decision No. 40 of 2017 include:

- AED 10,000 for late tax registration

- AED 1,000 for late filing (first offence), AED 2,000 for repeat offences within 24 months

- 14% per annum on late payment of tax

- AED 10,000 for failure to keep records (AED 20,000 for repetition)

- AED 20,000 for obstructing a tax auditor

Corporate tax registration deadlines are staggered based on license issuance date under FTA Decision No. 3 of 2024, and missing your deadline incurs a flat AED 10,000 penalty.

Beyond avoiding penalties, Singapore businesses have a structural tax advantage worth actively managing.

The Singapore-UAE Tax Treaty Advantage

A Double Taxation Avoidance Agreement (DTAA) exists between Singapore and the UAE, effective since 1996 and updated with Multilateral Instrument (MLI) modifications in 2019. Key provisions include:

- 0% withholding tax on dividends and interest

- 5% withholding tax on royalties

- Credit method for elimination of double taxation

- Principal Purpose Test (PPT) introduced via MLI to prevent treaty abuse

Applying this treaty correctly requires careful coordination across both jurisdictions. Without it, inter-company transactions, royalty arrangements, and dividend flows can fall foul of the PPT — stripping treaty benefits precisely when they matter most.

VJM Global's membership in EAI International provides access to a network of independent accounting and tax professionals across multiple jurisdictions, supporting the cross-border coordination that Singapore businesses need to manage Dubai and home-country positions together.

UAE Compliance Framework: What Singapore Businesses Must Know

VAT Requirements

The UAE introduced a 5% VAT on 1 January 2018. Registration, filing, and payment are all managed through EmaraTax, the FTA's official digital portal.

Registration thresholds:

- Mandatory: AED 375,000 in taxable supplies and imports over the previous 12 months, or expected within the next 30 days

- Voluntary: AED 187,500 in taxable supplies/imports or taxable expenses

Filing frequency:

- Quarterly: Businesses with annual turnover below AED 150 million

- Monthly: Businesses with annual turnover of AED 150 million or more

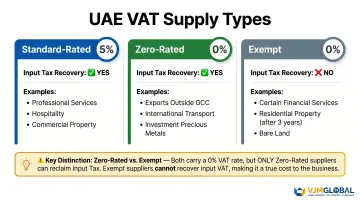

Supply classifications:

| Classification | Rate | Input Tax Recovery | Examples |

|---|---|---|---|

| Standard-rated | 5% | Yes | Most goods and services, commercial property, professional services, hospitality |

| Zero-rated | 0% | Yes | Exports outside GCC, international transport, investment precious metals (99%+ purity), first supply of new residential buildings (within 3 years), crude oil and natural gas |

| Exempt | 0% | No | Certain financial services (life insurance, loan interest, securities), residential property (after 3 years), bare land |

Singapore businesses in trading, services, or e-commerce must correctly categorize sales to avoid miscalculation and FTA penalties. The difference between zero-rated and exempt supplies is critical: zero-rated allows input tax credit recovery, while exempt does not.

Corporate Tax Requirements

The UAE introduced Corporate Tax via Federal Decree-Law No. 47 of 2022, effective for financial years starting on or after 1 June 2023.

Rate structure:

- 0% on taxable income up to AED 375,000

- 9% on taxable income exceeding AED 375,000

Small Business Relief: Available for entities with revenue of AED 3,000,000 or less (both current and all previous tax periods), treating them as having no taxable income. Available until 31 December 2026. Not available to Qualifying Free Zone Persons or members of MNE groups with consolidated revenues exceeding AED 3.15 billion.

Transfer pricing implications: The UAE follows OECD Transfer Pricing Guidelines. Intra-group transactions between a Singapore parent and its Dubai entity must be priced at arm's length and formally documented. This includes maintaining a transfer pricing policy, conducting benchmarking studies, and aligning with BEPS Action Plans — requirements Singapore businesses often underestimate when first entering the UAE.

IFRS and Audit Obligations

IFRS is mandatory: Article 27(2) of Federal Decree-Law No. 32 of 2021 requires UAE companies to prepare financial statements under International Financial Reporting Standards. While Singapore's SFRS(I) is largely converged with IFRS, businesses cannot simply re-submit Singapore-prepared accounts without UAE-specific review.

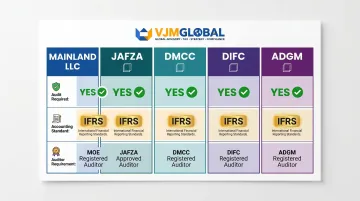

Audit requirements vary by structure:

| Entity Type | Audit Required? | Standard | Auditor Requirement |

|---|---|---|---|

| Mainland LLC | Yes, no threshold | IFRS | Ministry-approved auditor |

| JAFZA | Yes, all entities | IFRS | JAFZA-approved auditor |

| DMCC | Yes, including dormant | IFRS | DMCC-approved auditor |

| DIFC | Yes, all entities | Full IFRS only | DFSA-recognized auditor |

| ADGM | Yes, most entities | IFRS | ADGM-approved auditor |

Mainland companies must prepare annual financial statements (balance sheet, P&L, annual report) within 4 months of financial year-end, per Article 101 of the Companies Law.

Core Corporate Accounting Services Singapore Companies Need in Dubai

Bookkeeping and IFRS-Compliant Financial Reporting

Accurate, IFRS-compliant bookkeeping is the foundation of every compliance obligation in Dubai. Core components include:

- General ledger maintenance

- Bank reconciliations

- Accounts payable and receivable management

- Preparation of financial statements (P&L, balance sheet, cash flow)

Record retention: Article 26(2) of Federal Decree-Law No. 32 of 2021 requires companies to keep accounting books and records at the head office for at least 5 years from the end of the financial year. FTA VAT legislation aligns with this requirement, while corporate tax records require retention for up to 7 years.

VJM Global's ACCA-qualified, CA (ICAI), and CPA-credentialed professionals deliver IFRS-compliant financial reporting via cloud platforms like QuickBooks Online — giving Singapore-based management teams real-time visibility without being in the room.

VAT Registration, Return Filing, and FTA Advisory

End-to-end VAT compliance management includes:

- Initial FTA registration

- Monthly or quarterly return preparation based on turnover

- Submission via EmaraTax portal

- Input tax credit management for businesses with mixed supplies

- Handling VAT refunds and FTA queries

Corporate Tax Registration, Filing, and Strategic Advisory

Corporate tax services extend beyond simple filing:

- Tax impact assessments

- Structuring advice to optimize tax position (such as free zone qualifying income)

- Preparation of corporate tax returns within FTA deadlines

- Advisory considering both UAE and Singapore tax positions simultaneously

Qualifying Free Zone Person (QFZP) status allows 0% tax on qualifying income. Maintaining that status requires meeting all of the following conditions:

- Adequate substance in a Free Zone

- Deriving qualifying income only

- Compliance with arm's length principle

- Maintaining transfer pricing documentation

- Maintaining audited financial statements regardless of revenue

- Non-qualifying revenue not exceeding AED 5 million or 5% of total revenue

Failure to meet QFZP requirements results in loss of status for that period plus the subsequent 4 periods — 5 years in total.

Payroll Management and WPS Compliance

The UAE's Wage Protection System (WPS) is a mandatory electronic salary payment system monitored by the Ministry of Human Resources. Key requirements:

- All private sector employers registered with MOHRE must comply

- Salaries considered delayed if not paid within 15 days of due date

- Must pay at least 90% of workforce through WPS monthly

- Must pay at least 80% of total salary value through WPS

Penalties for non-compliance:

- Work permit block

- AED 1,000 per employee for non-WPS payment

- AED 5,000 per employee (up to AED 50,000) for incorrect WPS data

- Escalation for delays beyond 30-60 days includes public announcement and judicial referral

End-of-service gratuity differs from Singapore's CPF system. UAE gratuity is a lump-sum terminal payment calculated at the end of employment:

- Minimum service: 1 year continuous employment

- 21 days of basic wage per year for the first 5 years

- 30 days of basic wage per year for each year thereafter

- Capped at 2 years' total remuneration

No contributions accrue during employment — the full amount is calculated and paid out only when the employee exits.

Singapore vs. UAE Accounting: Key Differences at a Glance

Accounting Standards: SFRS vs. IFRS

Singapore adopted SFRS(I)—Singapore Financial Reporting Standards (International)—with full IFRS convergence effective 1 January 2018. SFRS(I) are essentially identical to IFRS, but Singapore businesses maintaining dual reporting must prepare:

- Singapore-consolidated accounts under SFRS(I)

- Dubai entity accounts under full IFRS

The standards are substantively converged — but UAE-specific filing timelines, audit obligations, and FTA registration requirements add a distinct compliance layer that Singapore finance teams need to map out before going live.

Tax System Comparison

| Element | Singapore | UAE |

|---|---|---|

| Consumption Tax | GST 9% (effective 1 Jan 2024) | VAT 5% (effective 1 Jan 2018) |

| Corporate Tax | Flat 17% on chargeable income | 0% up to AED 375,000; 9% above |

| Tax Authority | IRAS | FTA |

| Filing Portal | myTax Portal | EmaraTax |

| Transfer Pricing | OECD-aligned | OECD-aligned |

The UAE's lower corporate tax rate can meaningfully reduce the overall tax burden for Singapore-headquartered groups — provided intercompany pricing is documented to OECD standards on both sides of the structure.

Regulatory Bodies and Filing Infrastructure

Each UAE authority has a Singapore counterpart. Knowing the parallel structure helps Singapore CFOs assign responsibility quickly when setting up reporting lines for a Dubai entity:

| Singapore | UAE Equivalent | Function |

|---|---|---|

| ACRA | Ministry of Economy | Company registration and governance |

| IRAS | FTA | Tax administration |

| SGX | Free zone authorities (JAFZA, DMCC, DIFC) | Listing and reporting requirements |

How to Choose the Right Corporate Accounting Partner in Dubai

Key Criteria to Evaluate

A suitable accounting partner for a Singapore business should demonstrate:

FTA registration as a tax agent: Only FTA-registered agents can formally represent businesses before the FTA. Registration requirements include:

- Bachelor's or Master's in Tax, Accounting, or Law from a recognized institution

- Minimum 3 years recent professional experience in tax, accounting, or law

- Proficiency in Arabic and English

- Passing the FTA Tax Agent Examination

- Professional Indemnity Insurance

IFRS expertise and cross-border experience: Prioritize firms that have served APAC or Singapore clients. Verify team qualifications — Chartered Accountants (CA/ICAI), ACCA-certified professionals, or CPAs with UAE practice experience carry the most weight here.

Coordination with Singapore stakeholders: Investors, banks, and Singapore parent-company auditors often require Dubai financials to meet internationally accepted standards. Firms with global network affiliation are better positioned to deliver this without back-and-forth delays.

Global Network Affiliation and International Expertise

Firms with membership in internationally recognized accounting networks bring global standards to local practice. VJM Global, as a member of EAI International with 30+ years of experience serving foreign businesses across multiple continents, brings the cross-border perspective Singapore companies need when setting up in Dubai.

EAI International is an association of independent accounting, audit, tax, and advisory firms founded in 1986, with reach across 40+ countries. Members are rigorously selected, locally regulated, and globally connected—offering Singapore businesses access to standardized service quality across jurisdictions.

VJM Global has maintained a 95% client retention rate while serving businesses across 15+ industries globally — including American, UK, and Australian companies navigating multi-layered compliance in unfamiliar markets. That experience translates directly to Singapore businesses facing the same challenge in Dubai.

Technology, Communication, and Transparency

Modern Dubai accounting practice is digital-first. Beyond credentials, how a firm communicates and structures its engagement matters — especially when your management team is based in Singapore.

Cloud accounting platforms: UAE-compatible options include Zoho Books (with direct EmaraTax integration), QuickBooks, Xero, Tally, and Sage. VJM Global uses QuickBooks Online with multi-factor authentication, role-based access controls, and real-time reporting dashboards — so Singapore-based teams can monitor Dubai financials without waiting on email updates.

Engagement structure clarity: Before signing, confirm:

- Who prepares the accounts and who files VAT and corporate tax

- What is explicitly included in the service agreement

- How often the firm communicates with Singapore stakeholders — and through which channels

A well-defined engagement letter with fixed fees or clear billing thresholds removes ambiguity and protects both sides as the relationship scales.

Frequently Asked Questions

Is a CPA valid in Dubai?

Yes, the CPA (Certified Public Accountant) qualification is recognized in Dubai and commonly held by finance professionals working there. However, it is not mandated by UAE law for providing accounting services. UAE firms typically employ CAs (Chartered Accountants), ACCAs, and CPAs. Clients should focus on the firm's FTA registration and professional credentials rather than a single qualification type.

Is CPA worth it in Dubai?

The CPA qualification carries strong credibility in Dubai, particularly in multinational companies or US-headquartered businesses. For UAE-specific compliance work, however, ACCA and CA qualifications are more directly aligned with local regulatory frameworks — making the choice dependent on the professional's target client base.

Which is better, CA or ACCA in Dubai?

Both CA (Chartered Accountant) and ACCA are well-respected in Dubai. CA (particularly ICAI) is common among South Asian professionals and carries strong recognition across UAE firms, while ACCA is favored by international and Big Four-affiliated firms — and may feel more familiar to Singapore businesses given ACCA's strong local presence there.

Do Singapore businesses need to register for VAT in Dubai?

Yes, VAT registration in Dubai is mandatory once a business's taxable turnover meets or exceeds AED 375,000 over 12 months or is expected within the next 30 days. Singapore businesses operating in Dubai through a UAE entity—regardless of where the parent is headquartered—must comply with UAE VAT obligations if they meet the threshold.

What is the corporate tax rate in Dubai for foreign companies?

The UAE Corporate Tax rate is 9% on taxable income exceeding AED 375,000 per year, with 0% on income up to that threshold. Foreign companies with a UAE presence—including Singapore businesses operating through a Dubai subsidiary or branch—are subject to this rate on UAE-sourced income, with specific provisions applicable to qualifying free zone entities.

What accounting standards do businesses use in Dubai?

Businesses in Dubai are required to prepare financial statements under IFRS (International Financial Reporting Standards). Singapore businesses familiar with SFRS(I) will find the frameworks broadly similar, though differences in areas like revenue recognition and lease accounting require careful attention. An IFRS-experienced accounting partner in Dubai ensures compliant reporting across both frameworks.