Introduction

For Singapore businesses, Dubai offers a compelling expansion case: zero corporate tax on most income, free zone incentives, and direct access to Gulf and African markets. The UAE pulled in $45.6 billion in FDI inflows during 2024, ranking 10th globally — and Singapore operators are among those moving in. But entering a new jurisdiction means taking on compliance obligations that many overseas operators underestimate.

External audits are often treated as a compliance checkbox — a cost to absorb before the license renewal date. For Singapore businesses operating in Dubai, the real value runs deeper than that. Audited financial statements affect your ability to open corporate bank accounts, maintain free zone licenses, and attract investors.

They also protect operations from internal control failures that become harder to detect when you're managing an entity from across a border.

This guide breaks down the specific, measurable benefits of external audits in Dubai from a Singapore business perspective. You'll learn what the process requires, what risks it protects against, and how to use it to support growth.

Key Takeaways

- External audits in Dubai are legally mandatory for free zone companies and mainland LLCs under UAE law

- Compliance covers UAE Federal Tax Authority requirements, IFRS reporting standards, and free zone-specific regulations

- Audited statements are critical for corporate banking, investor confidence, and license renewal

- Non-compliance triggers fines up to AED 100,000, license suspension, and reputational damage

- Singapore businesses face dual-jurisdiction complexity — UAE audit rules differ significantly from Singapore's ACRA framework, making local UAE expertise essential

What Is External Audit in Dubai?

An external audit is an independent, third-party examination of your company's financial statements. The auditor verifies accuracy, completeness, and compliance with accounting standards in force — in Dubai's case, International Financial Reporting Standards (IFRS) as mandated by Federal Law No. 2 of 2015, Article 27(3).

External audits in Dubai must be performed by licensed audit firms registered with the relevant UAE authority. This means:

- Mainland companies require auditors licensed by the Ministry of Economy and registered with the emirate's Department of Economic Development

- Free zone entities must use auditors approved by their specific free zone authority (DMCC, JAFZA, DAFZA, etc.)

- DIFC operates its own Registrar of Auditors under a common law framework

For Singapore businesses, knowing which licensing regime applies to your Dubai entity is the first step. Beyond that, external auditing is the mechanism through which your foreign-owned entity demonstrates financial legitimacy to regulators, banks, and commercial counterparties — giving it real operational weight in the market.

Key Advantages of External Audit for Singapore Businesses in Dubai

The advantages below address specific challenges Singapore businesses face when managing UAE entities remotely: regulatory unfamiliarity, cross-border oversight gaps, and the need to build credibility in a new market. Each benefit ties to measurable business outcomes.

Regulatory Compliance and Penalty Avoidance

Dubai and the broader UAE have significantly tightened compliance requirements since introducing UAE Corporate Tax (effective June 2023) and ongoing VAT obligations monitored by the Federal Tax Authority (FTA).

External auditors systematically review financial records against UAE-specific requirements:

- VAT return accuracy and reconciliation

- Transfer pricing documentation

- IFRS-compliant financial statement preparation

- Corporate Tax return supporting documentation

Discrepancies get flagged before they become regulatory violations.

Non-compliance in Dubai carries direct financial penalties. According to Cabinet Decision No. 75 of 2023:

- AED 10,000 penalty for late Corporate Tax registration

- AED 500/month for late tax returns (first 12 months), escalating to AED 1,000/month thereafter

- AED 10,000 to AED 100,000 for failing to maintain proper accounting records

- AED 50,000 to AED 500,000 for false financial reporting, with potential imprisonment

Free zone authorities have reinforced mandatory audit requirements for license renewal. JAFZA imposes an AED 5,000 fine for non-submission of audited statements. DMCC blocks license renewal entirely until compliant statements are submitted.

For Singapore businesses operating remotely, limited day-to-day oversight compounds these risks. A single regulatory penalty or license suspension often costs far more than the annual audit fee — typically AED 5,000 to AED 12,000 for SMEs.

KPIs impacted:

- Compliance penalty rate (target: zero)

- On-time license renewal rate

- FTA audit readiness score

- VAT return accuracy rate

When this advantage matters most: During your first 1-2 years of Dubai operations, when teams are still learning UAE-specific obligations, and during Corporate Tax return filing periods.

Investor Credibility and Banking Access

One of the most practical barriers Singapore businesses face in Dubai is opening a UAE corporate bank account and attracting regional investors.

UAE banks require audited financial statements as part of due diligence. The UAE Central Bank's regulations mandate customer verification under Decree Federal Law No. 20 of 2018 (AML/CFT), and banks commonly request audited financials for account opening, credit facilities, and ongoing banking relationships.

Local family offices, regional VCs, and global partners all treat audit reports as baseline evidence of financial integrity. No audit means no seat at the table.

Singapore businesses enter the UAE with no established reputation or credit history. An audited financial statement from a UAE-recognized audit firm substitutes for that track record — you're evaluated on the quality of your financials, not your name recognition.

The numbers back this up. The UAE recorded $45.6 billion in FDI inflows in 2024 and attracts 37% of all MENA investment capital — a market where financial transparency directly determines who gets access to deals. Businesses with audited accounts are better positioned to secure UAE banking, qualify for contract tenders, and close joint ventures with regional partners.

KPIs impacted:

- Bank account opening success rate

- Investor due diligence pass rate

- Contract tender qualification rate

- Time-to-operational readiness

When this advantage matters most: For Singapore businesses in capital-intensive sectors (real estate, trading, construction, fintech) and any entity seeking financing or joint ventures with UAE-based partners.

Cross-Border Financial Visibility and Fraud Prevention

When Singapore headquarters manages a Dubai entity remotely, the head office often has limited real-time visibility into what's happening on the ground — leaving the door open to internal control failures, unauthorised transactions, or undetected accounting errors.

An external auditor, as an independent party, examines financial transactions, reconciles accounts, and tests internal controls. This gives the Singapore parent company an objective view of whether the Dubai entity's financial reporting reflects actual business activity.

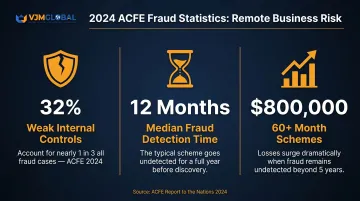

According to the ACFE 2024 Report to the Nations, organisations with external audits experienced approximately 51% lower median fraud losses. The global median occupational fraud case caused $145,000 in losses, with small businesses (fewer than 100 employees) suffering median losses of $150,000 — higher than the global average.

Key findings relevant to remote operations:

- Lack of internal controls drives 32% of all fraud cases

- Median detection time is 12 months

- Frauds lasting 60+ months result in median losses of $800,000

For Singapore companies subject to ACRA reporting requirements, accurate financial data from Dubai operations is necessary for group-level compliance — making Dubai external audits directly relevant to Singapore obligations.

KPIs impacted:

- Internal control deficiency rate

- Intercompany reconciliation accuracy

- Fraud incident rate

- Group financial reporting accuracy

When this advantage matters most: For Singapore businesses that have hired local UAE staff or third-party managers to run day-to-day Dubai operations, and for businesses in their early operational phase before robust internal processes are established.

What Happens When External Audit Is Skipped or Delayed

The benefits of audit compliance become clearest when you see what happens without it. For Singapore businesses unaware of UAE audit obligations — or those deferring audits to cut short-term costs — the consequences compound fast.

Most common outcomes:

DMCC, JAFZA, and DAFZA require audited financial statements for license renewal. JAFZA mandates submission within 90 days of financial year-end, with an AED 5,000 fine for non-submission. IFZA's Administrative Resolution No. 001/2025 (effective 30 September 2025) extends this to entities with AED 3 million+ turnover or 10+ employees.

Unaudited VAT and Corporate Tax filings trigger penalties under Cabinet Decision No. 75 of 2023. Late registration alone costs AED 10,000; failure to maintain records adds AED 10,000 for a first offence and AED 20,000 for repeat violations.

Banks require current audited statements for account maintenance and financing decisions. Without them, passing due diligence — even for existing relationships — becomes a real obstacle.

Local commercial partners and investors treat audit compliance as a baseline in Dubai. An unaudited entity raises immediate red flags in deal and partnership contexts.

Delayed audits create backlogs that cost more to fix the longer they're left. Multi-year reconstruction means rebuilding records from bank statements, invoices, and contracts. This is a pattern seen repeatedly among foreign SMEs that underestimated UAE compliance requirements on entry.

How Singapore Businesses Can Get the Most Value from External Audits in Dubai

External audits deliver the most business value — not just compliance value — when treated as an annual financial health review, not a last-minute obligation.

Three practices make a measurable difference:

- Maintain IFRS-compliant records year-round. Singapore businesses accustomed to SFRS face minimal transition friction given the convergence with IFRS — but consistency throughout the year matters more than a last-minute records scramble before the audit.

- Act on audit findings, not just the final report. A quality external audit surfaces inefficiencies and highlights where internal controls can be tightened. The management letter is where the operational roadmap lives — read it.

- Bring in cross-border advisors early. Professionals familiar with both Singapore business contexts and UAE regulatory requirements reduce the errors that delay or complicate the audit process.

VJM Global's team brings 30+ years of cross-border accounting and advisory experience, helping international businesses build compliant financial systems before their first audit cycle — not after. That foundation reduces audit preparation time in subsequent years and keeps your Dubai entity ready for banking access and ongoing license compliance.

Conclusion

External audits in Dubai are not a bureaucratic formality for Singapore businesses — they are the operational foundation that makes banking access, investor trust, license renewal, and regulatory standing possible in a market that demands financial transparency.

The value of external auditing builds over time. Businesses that establish clean, audited financial records from their first year in Dubai accumulate a track record that unlocks financing, partnerships, and market expansion — advantages that gaps in audit history will consistently block.

Schedule your external audit proactively and build it into your annual operational calendar. The businesses that treat auditing as routine — not reactive — are the ones positioned to move quickly when opportunities arise.

Frequently Asked Questions

Is audit mandatory in Dubai?

Audit requirements depend on business structure and jurisdiction. Free zone companies (DMCC, JAFZA, IFZA) must submit audited financial statements for license renewal, while mainland LLCs must comply under Federal Law No. 2 of 2015. UAE Corporate Tax and VAT regulations create effective audit obligations for most entities regardless of structure.

What are the audit requirements for free zone companies in Dubai?

Most major Dubai free zones — including DMCC, JAFZA, DAFZA, and IFZA — require companies to submit audited financial statements prepared under IFRS by an approved, licensed audit firm as part of their annual license renewal process. Deadlines are typically 90 days from financial year-end.

How is an external audit in Dubai different from Singapore's audit requirements under ACRA?

Both frameworks require independent audits and IFRS-based reporting, but Dubai audits must be conducted by UAE-licensed firms approved by the relevant free zone or mainland authority. Singapore offers audit exemptions for small companies meeting specific criteria — no equivalent exemption exists in Dubai free zones or for mainland LLCs.

How often should a Singapore business in Dubai conduct an external audit?

External audits in Dubai should be conducted annually, aligned with your company's financial year-end, to meet free zone renewal deadlines and Corporate Tax filing obligations. Proactive scheduling well before renewal dates avoids backlogs and penalties.

What happens if a company in Dubai fails to comply with audit requirements?

Consequences include free zone license renewal rejection, FTA financial penalties (AED 10,000 to AED 100,000), inability to open or maintain UAE corporate bank accounts, and reputational damage with local business partners.

Can a Singapore-based accounting firm conduct the external audit for a Dubai company?

No — the audit must be performed by a firm licensed and approved by the relevant UAE authority (free zone or mainland). Singapore businesses need to engage a UAE-registered audit firm, though they may work alongside their Singapore accountants for group reporting coordination.