Introduction

A London-based fintech founder closes her Series A round and sets up her APAC headquarters in Singapore. Within 60 days, she's managing four separate compliance obligations — an ACRA annual return deadline, an IRAS Estimated Chargeable Income (ECI) filing window, mandatory GST registration (projected turnover will exceed S$1 million), and CPF payroll contributions for her first five local hires.

Each obligation runs on a different timeline, governed by a different regulatory body, with different penalties for missing the mark.

That's the reality of Singapore's corporate accounting environment: highly structured, multi-layered, and unforgiving of gaps — but entirely manageable once you understand how the pieces connect.

This guide covers the types of corporate accounting services available in Singapore, the regulatory obligations every company must meet under ACRA, IRAS, and Singapore Financial Reporting Standards (SFRS), and how to decide between in-house and outsourced accounting support. It's written for business owners, finance managers, and foreign companies operating or expanding in Singapore who need to get accounting compliance right from day one.

Key Takeaways

- Singapore corporate accounting requires bookkeeping, financial statements, GST filing, payroll, and audit support — all with strict regulatory deadlines

- Compliance with ACRA, IRAS, and SFRS is mandatory — late filings trigger escalating penalties from S$300 to S$10,000+

- Foreign companies face additional compliance layers, making local accounting expertise essential

- Outsourcing costs S$1,200–S$14,400/year versus S$62,000–S$87,000 for in-house staff

- Select firms with ACRA/IRAS track records, sector expertise, cloud platforms, and full-service packages

What Are Corporate Accounting Services in Singapore?

Corporate accounting services cover the financial management, reporting, and compliance functions required to keep a Singapore-registered company legally operational and financially sound. Unlike personal accounting, these services apply to business entities governed by the Companies Act, the Income Tax Act, and the Goods and Services Tax Act.

Core service categories typically include:

- Bookkeeping and transaction recording

- Financial statement compilation

- Corporate tax filing (ECI and Form C-S/C)

- GST compliance and quarterly filing

- Payroll processing and CPF contributions

- Statutory audits (where applicable)

- Financial advisory and reporting

According to Singapore's Department of Statistics, Singapore had 371,000 enterprises in 2025, of which 369,500 (approximately 99.6%) were SMEs. The same dataset recorded 90,700 foreign enterprises, representing a 3.4% year-on-year increase.

Most of these businesses have no dedicated in-house finance team. That gap drives strong demand for outsourced accounting — especially from foreign-owned subsidiaries that must navigate Singapore's tax and reporting rules while aligning with parent-company requirements abroad.

Understanding who actually needs these services helps clarify the scope:

Who needs these services:

- Local SMEs without dedicated finance teams

- Startups navigating first-year compliance

- Subsidiaries of foreign multinationals

- Holding companies managing cross-border operations

- Any business unfamiliar with Singapore's regulatory environment

Key Corporate Accounting Services Every Singapore Business Needs

Bookkeeping and Financial Recordkeeping

Every Singapore company must maintain accounting records that are audit-ready and ACRA-compliant — and the obligation is backed by law, not just best practice.

Under Section 199 of the Singapore Companies Act, every company must keep proper accounting records that sufficiently explain the transactions and financial position of the company. These records must be retained for a minimum of five years from the end of the financial year.

Proper bookkeeping covers:

- Accounts payable and receivable

- Bank reconciliation

- General ledger maintenance

- Expense tracking and categorization

- Invoice and receipt management

IRAS mirrors this requirement: companies must retain records for at least five years from the relevant Year of Assessment, sufficient to support financial statements that give a true and fair view of the company's affairs.

Directors are personally responsible for meeting these obligations. Non-compliance can trigger penalties under the Companies Act and complicate tax assessments by IRAS.

Financial Statement Preparation and Compilation

Singapore companies are required by the Companies Act to prepare financial statements that comply with Singapore Financial Reporting Standards (SFRS) or SFRS for Small Entities.

Two tiers apply depending on company type and size.

Full SFRS(I) applies to all Singapore-incorporated companies listed on the SGX since 1 January 2018. SFRS(I) is fully converged with IFRS as issued by the International Accounting Standards Board.

SFRS for Small Entities is available to private companies that are not publicly accountable and meet at least two of these three criteria for the previous two consecutive financial years:

- Total annual revenue not exceeding S$10 million

- Total assets not exceeding S$10 million

- Number of employees not exceeding 50

The SFRS for Small Entities features approximately 90% fewer disclosures compared to full SFRS, reducing compliance costs for qualifying companies.

Key financial statements include:

- Income statement (profit and loss)

- Balance sheet (statement of financial position)

- Cash flow statement

- Statement of changes in equity

These documents serve ACRA filing requirements, investor reporting, and bank financing decisions — and they also form the direct input for corporate tax filing obligations.

Corporate Tax Filing and GST Compliance

Singapore's headline corporate income tax rate is a flat 17% of chargeable income. However, generous exemptions reduce the effective rate for SMEs and startups.

Tax exemption schemes (from YA 2020 onwards):

| Scheme | First tier | Second tier | Maximum exemption per YA |

|---|---|---|---|

| Startup Exemption (first 3 YAs) | 75% on first S$100,000 | 50% on next S$100,000 | S$125,000 |

| Partial Tax Exemption (all other companies) | 75% on first S$10,000 | 50% on next S$190,000 | S$102,500 |

Filing deadlines:

- ECI (Estimated Chargeable Income): Within 3 months from end of financial year

- Form C-S / Form C: 30 November each year

Form C-S is available to companies with annual revenue of S$5 million or below. Form C-S (Lite) is available to companies with annual revenue of S$200,000 or below.

GST Compliance:

The current GST rate is 9%. Mandatory GST registration is required when a business's taxable turnover exceeds S$1 million. GST returns and payments are due one month after the end of each accounting period (typically quarterly).

Payroll Processing and CPF Compliance

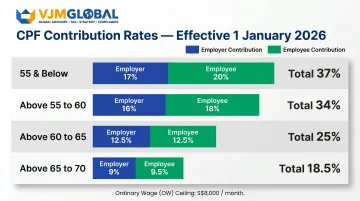

Singapore payroll carries a statutory obligation: employers must contribute to the CPF (Central Provident Fund) for all Singapore citizens and Permanent Residents, with rates tied to the employee's age. From 1 January 2026, the following rates apply for employees earning monthly wages above S$750:

| Employee age (years) | Total rate | Employer share | Employee share |

|---|---|---|---|

| 55 and below | 37% | 17% | 20% |

| Above 55 to 60 | 34% | 16% | 18% |

| Above 60 to 65 | 25% | 12.5% | 12.5% |

| Above 65 to 70 | 18.5% | 9% | 9.5% |

The CPF Ordinary Wage (OW) ceiling increased to S$8,000 per month from 1 January 2026.

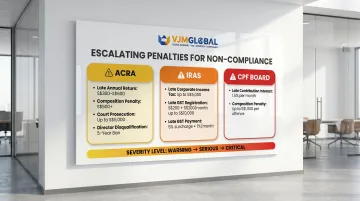

Consequences of late CPF contributions:

The CPF Board charges late payment interest at 1.5% per month, subject to a minimum of S$5, starting from the day after the due date. The CPF Board may also impose a composition amount of up to S$1,000 per offence. Court convictions carry fines between S$1,000 and S$5,000 (first offence) and up to S$10,000 (subsequent offences), with possible imprisonment of 6-12 months.

Singapore's Accounting Regulatory Framework: What Companies Must Know

Singapore's corporate accounting environment rests on three main regulatory pillars: ACRA (Accounting and Corporate Regulatory Authority), IRAS (Inland Revenue Authority of Singapore), and the FRS framework. These interact closely, and non-compliance with any one carries serious consequences.

ACRA Requirements

ACRA oversees companies under the Singapore Companies Act, governing annual return filing, appointment of a company secretary, maintaining a registered office address, and AGM requirements.

Key deadlines:

| Requirement | Deadline (non-listed companies) |

|---|---|

| Annual General Meeting (AGM) | Within 6 months after financial year end |

| Annual Return (AR) filing | Within 7 months after financial year end |

Private companies may skip the AGM if they meet any one of these conditions:

- Send financial statements to all members within 5 months after FYE

- Are dormant with total assets of S$500,000 or less

- Have all members pass a resolution to dispense with the AGM

Small Company Audit Exemption:

A private company qualifies for audit exemption if it meets at least two of the following three criteria for the immediate past two consecutive financial years:

- Total annual revenue of S$10 million or less

- Total assets of S$10 million or less

- 50 or fewer full-time employees

If the company is part of a group, the entire group must also meet these thresholds on a consolidated basis.

Company Secretary:

Every company must appoint a company secretary within six months of incorporation. The position cannot remain vacant for more than six months; failure to comply may result in a fine of up to S$1,000.

IRAS and Tax Compliance

IRAS administers corporate income tax, GST, withholding tax, and stamp duty.

Singapore taxes on a territorial basis — income is taxable if it accrues in or derives from Singapore, or if it is received in Singapore from abroad. Under Section 10(25) of the Income Tax Act 1947, foreign-sourced income is treated as "received" in Singapore when any of the following applies:

- It is remitted to Singapore

- It is used to settle a debt incurred in a Singapore trade

- It is used to purchase movable property brought into Singapore

Withholding Tax:

Withholding tax applies when Singapore-based payers make the following payments to non-resident companies or individuals:

- Royalties and interest

- Technical service fees and management fees

- Rent for movable property

The payer must withhold a percentage and remit it to IRAS by the 15th of the second month after payment. Rates may be reduced under applicable Double Taxation Agreements.

Singapore Financial Reporting Standards (SFRS)

All Singapore-incorporated companies must prepare accounts in compliance with SFRS, which is aligned with International Financial Reporting Standards (IFRS).

Key differences between SFRS(I) and SFRS for Small Entities:

| Feature | Full SFRS(I) | SFRS for Small Entities |

|---|---|---|

| Target users | Listed and large companies | Private small companies |

| IFRS alignment | Fully converged | Based on IFRS for SMEs |

| Goodwill treatment | Annual impairment testing | Amortized over useful life |

| R&D costs | Development costs may be capitalized | Always expensed |

| Borrowing costs | Capitalized for qualifying assets | Always expensed |

| Disclosure volume | Extensive | Minimal |

Companies that qualify as small entities should default to SFRS for Small Entities — the reduced disclosure burden directly lowers audit preparation time and professional fees. Larger or listed companies, and those reporting to international investors, will need to apply the full SFRS(I) framework.

Key Compliance Deadlines and Consequences of Non-Compliance

Annual Compliance Calendar

| Obligation | Deadline | Regulatory body |

|---|---|---|

| ECI filing | 3 months after FYE | IRAS |

| Form C-S / Form C | 30 November each year | IRAS |

| GST return (F5/F8) | 1 month after end of accounting period | IRAS |

| AGM (non-listed private companies) | 6 months after FYE | ACRA |

| Annual return to ACRA | 7 months after FYE | ACRA |

| CPF contributions | Last day of calendar month | CPF Board |

Penalty Framework

| Offence | Penalty |

|---|---|

| Late annual return (up to 3 months) | S$300 lodgement penalty |

| Late annual return (more than 3 months) | S$600 lodgement penalty |

| ACRA composition sum (late AGM or AR) | At least S$500 each |

| Court prosecution (ACRA offences) | Up to S$5,000 per charge |

| Director disqualification | 5-year ban after 3+ filing offences in 5 years |

| Late CIT filing (Form C-S/C) | Up to S$5,000 |

| Late GST filing | S$200 immediate + S$200/month, max S$10,000 |

| Late GST payment | 5% penalty on unpaid tax; additional 1%/month after 60 days (max 12%) |

| Late CPF contribution | 1.5%/month interest (min S$5); composition up to S$1,000/offence |

ACRA Striking Off Process

When ACRA believes a company is no longer in operation, it initiates an ACRA-initiated Striking Off (ASO):

- A Striking Off Notice is sent to the company, directors, secretaries, and shareholders

- A 30-day objection period follows

- If no objection is received, the company name is published in the Gazette with status "Gazetted to be Struck Off"

- After a further 60 days without objection, the company is struck off and ceases to exist

Staying compliant throughout the company's lifecycle is what prevents reaching this point. Foreign company branches and subsidiaries face additional compliance requirements beyond those above, including filing the parent company's audited accounts and maintaining transfer pricing documentation under IRAS guidelines.

In-House vs. Outsourced Accounting for Singapore Companies

The decision between in-house and outsourced accounting comes down to two distinct scenarios. In-house works for large companies with complex, high-volume transactions and dedicated finance teams. Outsourcing suits SMEs, startups, and foreign-owned companies that need expert compliance without the overhead of a full finance department.

Cost Comparison:

| Cost element | Outsourced | In-house (mid-level accountant) |

|---|---|---|

| Monthly base cost | S$100-S$1,200 (by transaction volume) | S$3,500-S$4,500 base salary |

| Annual base cost | S$1,200-S$14,400 | S$42,000-S$54,000 |

| Fully-loaded annual cost (incl. CPF, benefits, overheads) | Same as above | S$62,000-S$87,000 |

Outsourced accounting fees are typically structured by monthly transaction volume:

- S$100-S$300 for fewer than 50 transactions

- S$300-S$400 for 50-100 transactions

- S$400-S$600 for 100-200 transactions

- S$600-S$1,200 for 200-500 transactions

These tiers help set a clear decision threshold. Below S$3 million in annual revenue, outsourcing is almost always more cost-effective. Above S$8 million, transaction complexity and volume typically justify building an in-house team.

Side-by-side comparison:

| Dimension | In-house | Outsourced |

|---|---|---|

| Cost | S$62,000-S$87,000/year | S$1,200-S$14,400/year |

| Expertise | Generalist staff | Specialist firm knowledge |

| Scalability | Fixed headcount | Flexible engagement |

| Technology | In-house tools | Firm-provided cloud platforms (Xero, QuickBooks) |

Specific advantages of outsourcing for foreign companies:

- Immediate access to local regulatory expertise

- Reduced risk of compliance errors during setup phase

- Ability to focus management bandwidth on core business operations

- No need to navigate Singapore employment laws for accounting hires

Data security and confidentiality:

When outsourcing, look for firms with:

- Formal Non-Disclosure Agreements (NDAs)

- ISO 27001 or equivalent data security certifications

- Secure cloud accounting platforms with role-based access controls

- Clear data handling protocols and client data segregation

For foreign companies managing operations across multiple markets, choosing a firm experienced in cross-border accounting — not just local compliance — can significantly reduce the administrative burden of maintaining accurate books in Singapore.

How to Choose the Right Corporate Accounting Firm in Singapore

Choosing the right firm comes down to four practical criteria:

1. Singapore-specific regulatory expertise and ACRA/IRAS track record

Ask for evidence of:

- ACRA Public Accounting Entity (PAE) registration for audit services

- ISCA (Institute of Singapore Chartered Accountants) membership

- Years of experience filing ACRA annual returns and IRAS tax returns

- Track record of zero or minimal late filing penalties for clients

2. Experience with your industry and company type

Different industries face different compliance nuances:

- Tech startups: stock option accounting, R&D tax claims

- Trading companies: transfer pricing, customs duties

- Foreign subsidiaries: withholding tax, parent company reporting

3. Technology stack

Ensure the firm uses:

- Cloud accounting software for real-time reporting (Xero, QuickBooks, Sage)

- IRAS-compliant GST filing systems

- InvoiceNow (Peppol) readiness for e-invoicing mandates

- Secure client portals for document sharing

4. Service breadth

Can the same firm handle:

- Bookkeeping

- Tax filing (ECI, Form C-S/C)

- GST compliance

- Payroll and CPF

- Company secretarial (annual return, AGM)

Bundled service providers reduce coordination overhead and ensure consistency across compliance obligations.

Once you've shortlisted firms against these criteria, a few due diligence steps can confirm the right fit:

- Ask for client references in your industry

- Confirm the firm's Public Accountants or Chartered Accountants credentials

- Review their SLA for turnaround times (especially during filing season)

- Clarify pricing structure upfront (fixed monthly retainer vs. per-service billing) to avoid hidden costs

For international businesses with operations spanning multiple jurisdictions — including companies headquartered in Singapore managing India-side obligations — VJM Global offers outsourced accounting, tax compliance, and CFO support tailored to cross-border complexity. With 30+ years of experience and a 95% client retention rate, their team of 100+ professionals has helped 500+ US, UK, and Australian businesses manage compliance across borders reliably.

Frequently Asked Questions

Is corporate accounting mandatory for all companies in Singapore?

Yes, all Singapore-incorporated companies must maintain proper accounts and file with ACRA and IRAS. However, statutory audit is only mandatory for companies that do not qualify for the small company audit exemption (meeting at least two of three thresholds: S$10M revenue, S$10M assets, 50 employees).

How much do corporate accounting services cost in Singapore?

Costs depend on company size, transaction volume, and service scope. Outsourced monthly accounting typically runs S$100–S$1,200, compared to S$62,000–S$87,000 annually for in-house staff. Compliance add-ons — financial statement compilation (S$500–S$1,500/year) and corporate tax filing (S$300–S$800/year) — are usually priced separately.

What is the difference between bookkeeping and corporate accounting?

Bookkeeping is the transactional recording layer — day-to-day entries of invoices, receipts, payments, and bank reconciliations. Corporate accounting builds on that foundation to cover financial reporting, tax planning, compliance filings, audit preparation, and strategic financial analysis.

Do foreign companies operating in Singapore need local accounting services?

Yes. Any registered entity in Singapore — subsidiary, branch, or representative office — must comply with the Companies Act and IRAS requirements. Local accounting expertise is essential, given that ACRA deadlines, GST rules, and CPF payroll obligations differ significantly from most other jurisdictions.

When must Singapore companies file their financial statements?

Private non-listed companies must hold their AGM within 6 months after financial year-end and file their annual return with ACRA within 7 months after FYE. Companies claiming audit exemption must still prepare compliant financial statements, though they do not need to submit audited accounts. Listed companies face shorter deadlines and additional disclosure requirements.

What accounting software do Singapore companies commonly use?

The most widely used platforms include Xero, QuickBooks Online, ABSS (formerly MYOB), Financio, Zoho Books, and Sage. Xero leads the Singapore SME market thanks to its unlimited-user model, local bank integrations (DBS, OCBC, UOB), and GST compliance features. Most outsourced accounting firms include platform access as part of their service packages.