Outsourced accounting in Singapore resolves this by placing locally qualified professionals in charge of all Singapore-side compliance. Your UK finance team stays focused on HMRC obligations and group reporting — without needing to develop Singapore-specific expertise from scratch.

This guide covers what Singapore outsourced accounting includes, what it costs, the compliance deadlines that matter, and how to choose a provider equipped for cross-border UK-Singapore work.

Key Takeaways

- Outsourced Singapore accounting covers bookkeeping, GST returns, ECI and Form C-S/C tax filing, XBRL financial statements, and CPF payroll

- UK businesses carry dual compliance obligations — a Singapore provider handles local filings while your UK team handles HMRC

- Outsourcing costs S$1,080–S$4,800/year for routine SME compliance, compared to S$95,940–S$112,320/year for a full-time in-house hire including employer CPF

- Singapore compliance deadlines run independently of HMRC and Companies House — late filing attracts fixed monetary penalties

- Prioritise providers with Singapore-qualified staff, cross-border UK experience, and fixed-fee transparent pricing

Why UK Businesses Use Outsourced Accounting for Their Singapore Entity

The Cost Numbers Make the Case

A full-time accountant in Singapore costs between S$82,000 and S$96,000 per year in base salary, according to Robert Walters' 2026 Singapore salary guide. Add employer CPF contributions at 17% for employees aged 55 and below, and the total employment cost rises to S$95,940–S$112,320 per year — roughly £55,700–£65,300 at current exchange rates.

Outsourced accounting packages for Singapore SMEs run closer to S$1,080–S$4,800 per year for routine bookkeeping and compliance. Even with payroll, GST, and XBRL added, the gap remains significant — particularly for UK businesses managing a satellite entity that doesn't yet justify a Singapore headcount.

UK Finance Teams Face a Steep Learning Curve

UK finance teams are not equipped to file Singapore returns without substantial upskilling. The differences aren't minor:

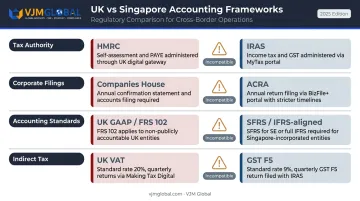

- Tax authority: IRAS operates entirely separately from HMRC, with its own filing formats and assessment processes

- Corporate filings: ACRA requires XBRL-format financial statements — a technical format UK accountants rarely work with

- Accounting standards: Singapore companies use Singapore Financial Reporting Standards (SFRS), which aligns closely with IFRS but differs from UK GAAP

- GST mechanics: Singapore GST operates differently from UK VAT in registration triggers, rates, and quarterly F5 filing procedures

Without local expertise, these differences translate directly into missed deadlines, incorrectly filed returns, and ACRA or IRAS queries that require expensive remediation.

Time Zone and Scalability

Singapore runs at GMT+8, meaning a UK team working GMT or BST has no real-time oversight of Singapore filing windows. A local provider monitors deadlines and submits on schedule regardless of UK office hours.

That operational coverage also scales naturally. As the Singapore entity grows — more transactions, GST registration, local hires — the outsourced provider absorbs that added complexity without triggering recruitment cycles or additional employment costs on the Singapore side.

Penalties Fall on the Entity Regardless of Where the Owner Sits

IRAS prosecuted over 4,700 companies for late or non-filing of corporate income tax returns in 2023 alone. For UK parent companies, those penalties don't just create a local headache — they affect group audit sign-off and group reputation. A Singapore-based provider with direct IRAS access handles deadline tracking, correspondence, and submissions — so penalties don't reach the group P&L in the first place.

What Outsourced Accounting Services in Singapore Include

Bookkeeping and Bank Reconciliation

Day-to-day income and expense recording in SGD, Singapore bank account reconciliation, and monthly or quarterly management accounts. For UK parent companies, this data typically feeds into group consolidation reporting — so format and timing matter as much as accuracy.

GST Returns

GST registration becomes compulsory once taxable turnover exceeds S$1 million under IRAS retrospective or prospective tests. The current GST rate is 9% (effective 1 January 2024). Once registered, companies file a quarterly F5 return — due one month after the end of each accounting period. A January–March period, for example, is due by 30 April.

UK businesses sometimes trigger this threshold earlier than expected, particularly when Singapore-based revenue grows faster than anticipated. Outsourced providers flag the threshold proactively rather than waiting for an IRAS notice.

Corporate Tax Filing

Two separate IRAS obligations apply:

- Estimated Chargeable Income (ECI) — must be filed within three months of the financial year end

- Annual corporate tax return (Form C-S, Form C-S Lite, or Form C) — due 30 November each year

Form C-S applies to Singapore-incorporated companies with annual revenue of S$5 million or below. Form C-S Lite is available for companies with revenue of S$200,000 or below. Companies outside these thresholds file Form C.

These deadlines run on fixed calendar dates — unlike HMRC's self-assessment cycle, which is tied to the individual entity's accounting period and can vary.

Financial Statements and XBRL

Singapore companies must prepare year-end financial statements under SFRS. Most companies are also required to file these with ACRA in XBRL format, a structured digital format ACRA uses for regulatory data extraction.

The simplified XBRL filing option applies to smaller non-publicly accountable companies with revenue and total assets each not exceeding S$500,000. Companies above that threshold file full XBRL.

UK parent companies also need these financial statements compatible with group consolidation — either IFRS or UK GAAP. That typically means the outsourced provider prepares a single set of accounts structured to satisfy both ACRA filing requirements and the parent's consolidation package.

Payroll Processing

Singapore payroll involves statutory complexity that UK businesses routinely underestimate when their entity hires its first local staff member:

- CPF contributions: Employer rate is 17% for employees aged 55 and below; rates step down for older age bands

- IR8A reporting: Employers submit annual income statements to IRAS by 1 March each year

- MOM compliance: Itemised payslips must be issued within three working days of salary payment; salary must be paid within seven days of the salary period end

UK-Specific Considerations When Outsourcing Singapore Accounting

UK-Singapore Double Taxation Agreement

The UK-Singapore DTA is in force, updated by a second protocol that entered into force on 27 December 2012. Under current treaty provisions:

- Dividends: Generally 0% withholding tax for qualifying ordinary dividends; up to 15% for REIT distributions

- Interest: Maximum 5% withholding tax

- Royalties: Maximum 8% withholding tax

These rates apply subject to beneficial ownership conditions and treaty eligibility. The outsourced provider needs to reflect correct DTA treatment in both the Singapore entity accounts and any consolidated group reporting — getting this wrong creates double taxation that requires unwinding later.

Financial Year End Alignment

Singapore allows flexible financial year end selection. The UK's standard April–March year doesn't have a Singapore equivalent, and misaligned year ends complicate group consolidation — you end up with different reporting periods requiring bridging calculations.

UK businesses setting up a Singapore entity should discuss year end selection with their provider before incorporation, not after. Aligning the Singapore FYE as closely as possible to the UK parent's year end simplifies group reporting considerably.

Transfer Pricing Documentation

Beyond year end alignment, intercompany transactions between a UK parent and Singapore subsidiary require careful handling. Arrangements such as management fees, intercompany loans, and royalties must all be priced at arm's length and properly documented. Both HMRC and IRAS have authority to challenge underdocumented intercompany pricing. Confirm that your provider has experience preparing or reviewing transfer pricing documentation — not just recording the transactions.

Consolidation-Ready Reporting

UK group accounts prepared under IFRS or UK GAAP need Singapore entity financials in a compatible format and currency. A provider that delivers accounts requiring extensive rework by your UK finance team adds cost and friction that undercuts the whole point of outsourcing. Ask specifically how they format the Singapore entity accounts for group consolidation.

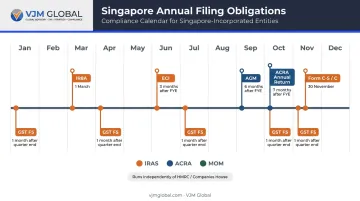

Singapore Compliance Deadlines UK Businesses Must Know

Singapore's compliance calendar operates independently of HMRC and Companies House — missing these dates triggers its own penalty regime.

| Obligation | Deadline |

|---|---|

| ECI filing | Within 3 months of financial year end |

| Annual corporate tax return (Form C-S/C) | 30 November each year |

| Annual General Meeting (AGM) | Within 6 months of financial year end |

| ACRA Annual Return | Within 7 months of financial year end |

| IR8A payroll reporting | 1 March each year |

| GST F5 return | 1 month after each quarterly period end |

Late filing penalties include:

- ACRA annual return: S$300 if up to three months late; S$600 if more than three months late

- Late tax payment: 5% penalty from the first day overdue; an additional 1% per month after 60 days, capped at 12%

- Non-filing of Form C-S/C: composition amounts up to S$5,000 per offence

Record Retention

Singapore's Companies Act requires accounting records to be kept for at least five years after the end of the financial year when the transactions were completed. This is one year shorter than the UK's six-year standard for limited companies — relevant if your UK team manages combined record-keeping.

Track the GST registration threshold throughout the year, not just at year end. Once taxable turnover exceeds S$1 million, GST registration becomes compulsory. UK businesses that catch the breach only at year end are often already liable for back-registration.

How to Choose the Right Outsourced Accounting Provider in Singapore

What to Look For

- Holds CA Singapore credentials or equivalent, with direct IRAS and ACRA filing experience

- Has documented experience with UK parent structures and UK group reporting — not just a generic "international clients" claim

- Uses cloud-based software (Xero, QuickBooks Online, or equivalent) so the UK parent has real-time visibility without being on the ground

- Offers transparent fixed-fee pricing with core services clearly separated from add-ons such as XBRL, payroll, GST registration, and transfer pricing documentation

- Assigns a dedicated named contact who knows your entity, not a rotating helpdesk

One factor that often gets overlooked: the UK-Singapore time gap. A provider that only responds during Singapore business hours leaves UK-based owners unable to review and approve filings within their working day — worth confirming before you sign any engagement letter.

Red Flags to Avoid

- No documented experience with UK-Singapore cross-border compliance or group consolidation

- Scope definitions that are vague enough to generate hidden charges as filings become more complex

- No clarity on how DTA treatment is handled or how consolidation packs are formatted

- Slow response times that prevent UK-based owners from meeting IRAS and ACRA submission windows

What Good Looks Like

VJM Global — with 250+ UK businesses served and 30+ years of cross-border accounting experience — offers a useful reference point for what to look for. Its membership of EAI International, a global network of independent accounting and tax firms, enables coordinated compliance support across jurisdictions, which matters when UK-Singapore structures involve multiple reporting lines.

A 95% client retention rate signals that service quality holds up as businesses grow and compliance requirements get more complex. When evaluating any provider for this role, start by confirming their specific Singapore credentials and verifiable IRAS/ACRA filing experience.

Common Misconceptions UK Businesses Have About Singapore Accounting

"My UK accountant can manage Singapore compliance."

UK accountants are not authorised to file on behalf of a Singapore-registered entity unless they hold Singapore-specific credentials and regulatory knowledge. IRAS and ACRA are entirely separate bodies from HMRC and Companies House. Filing formats (XBRL, ECI), accounting standards (SFRS), and penalty regimes have no direct UK equivalents. The barrier is jurisdictional qualification, not effort or expertise.

"Singapore is straightforward, so the compliance burden is minimal."

Singapore ranked first in the 2026 IMD World Competitiveness Ranking, and that reputation for business efficiency is well-earned. Business-friendly, however, does not mean lenient.

For UK businesses, the compliance picture includes:

- A strict Singapore filing calendar with real financial penalties for missed deadlines

- Foreign-owned entities held to the same standards as local companies

- Dual compliance obligations across both Singapore and UK frameworks

That combined burden makes local professional support more important for UK businesses, not less.

Frequently Asked Questions

How much does it cost to outsource accounting for a Singapore entity?

Indicative packages for Singapore SMEs range from approximately S$1,080 to S$4,800 per year for routine bookkeeping and compliance. Fees increase with transaction volume, GST registration, payroll, XBRL preparation, and tax advisory. This compares to S$95,940–S$112,320 per year for a full-time in-house hire including employer CPF contributions.

Do UK businesses need a separate accountant for their Singapore entity?

Yes. A Singapore entity has its own IRAS and ACRA obligations that require locally qualified professionals. UK-based accountants cannot file on behalf of a Singapore company without the relevant Singapore credentials — this is a regulatory requirement, not just a best practice recommendation.

What are the key Singapore compliance deadlines UK businesses should know?

Key deadlines to track:

- ECI: within three months of financial year end

- Form C-S/C (corporate tax return): due 30 November

- AGM: within six months of year end

- ACRA annual return: within seven months of year end

These deadlines run independently of HMRC and Companies House.

Can a UK company manage its Singapore accounting without a local team?

Yes: outsourced accounting providers handle all local IRAS and ACRA compliance on the company's behalf. Cloud-based accounting tools give the UK parent real-time access to management accounts, tax filings, and reconciliations without needing on-the-ground staff in Singapore.

How does the UK-Singapore double taxation agreement affect accounting?

The UK-Singapore DTA can reduce or eliminate withholding taxes on dividends (generally 0%), interest (maximum 5%), and royalties (maximum 8%) flowing between entities. The accounting provider needs to apply correct DTA treatment in the Singapore entity accounts and ensure this flows correctly into group consolidated reporting.

What is the difference between UK and Singapore accounting standards?

Singapore uses SFRS, which aligns closely with IFRS but differs from UK GAAP (FRS 102). UK businesses should confirm their Singapore provider can produce financials compatible with their group reporting framework (IFRS-aligned or with GAAP bridging) to avoid rework by the UK finance team.