Introduction

Singapore's corporate income tax system is one of the most straightforward in Asia — and one of the most advantageous. A flat 17% rate, territorial taxation, and generous exemption schemes have made the city-state a preferred base for foreign companies across industries.

Whether you're a startup founder or the CFO of a multinational, understanding how Singapore taxes corporate income is essential to structuring your operations correctly. This guide covers what you need to know: how the 17% rate applies, what qualifies as chargeable income, which exemption schemes are available, and your filing obligations.

For companies from the USA, UK, and Australia operating across Singapore, India, and broader Asia-Pacific markets, Singapore's tax rules don't exist in isolation. The interaction with other jurisdictions adds complexity — and that's where cross-border tax guidance becomes critical. VJM Global works with foreign businesses navigating exactly these situations, from initial structuring through ongoing compliance.

TLDR: Key Facts About Singapore Corporate Income Tax

- Singapore charges a flat **17% corporate income tax** on chargeable income for both resident and non-resident companies

- Tax follows a preceding-year basis and territorial system—only Singapore-sourced or qualifying remitted foreign income is taxed

- Startup Tax Exemption offers up to SGD 125,000 tax-free annually for the first three years of incorporation

- All other companies qualify for the Partial Tax Exemption on chargeable income

- Two mandatory filings: Estimated Chargeable Income (ECI) within 3 months of year-end, and Form C-S/C by 30 November annually

- Singapore operates a one-tier tax system—corporate dividends are tax-exempt for shareholders

Singapore Corporate Tax Rate and Basis of Taxation

The Flat 17% Rate

Singapore applies a flat corporate income tax (CIT) rate of 17% on chargeable income (taxable profits after deductions) for all companies, whether resident or non-resident. This contrasts with individual income tax, which uses progressive rates up to 24%. For businesses, this flat structure provides predictability and often makes corporate structures more tax-efficient than sole proprietorships.

Preceding-Year Assessment System

Singapore taxes companies on a preceding-year basis. Income earned during your financial year 2024 is assessed in Year of Assessment (YA) 2025. Your "basis period" is the 12-month financial year preceding the YA. For example:

- Financial year ending 31 December 2024

- Taxed in YA 2025

- Returns filed by 30 November 2025

This system gives businesses time to finalize accounts before filing tax returns.

Territorial Basis of Taxation

Singapore follows a territorial tax system: you're taxed on income that:

- Arises in Singapore (Singapore-sourced income from trade, business, or services performed in Singapore)

- Is received in Singapore from foreign sources (under specific conditions)

Foreign income becomes taxable when remitted to Singapore. Remittance covers income transmitted into the country, used to settle Singapore trade debts, or used to purchase movable property brought into Singapore.

The Foreign-Sourced Income Exemption (FSIE) regime can exempt qualifying foreign income from this rule, provided specific conditions are met.

One-Tier Corporate Tax System

Once a Singapore-resident company pays corporate tax, dividends distributed to shareholders are entirely tax-exempt, regardless of whether shareholders are individuals or corporations, resident or non-resident. This "one-tier" system eliminates double taxation of corporate profits and makes Singapore an attractive location for holding company structures.

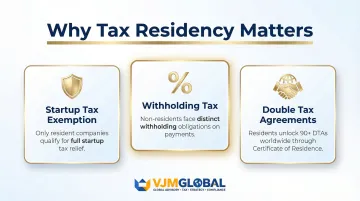

Tax residency ties directly to these advantages — and the rules may surprise you.

Determining Tax Residency in Singapore

Tax residency is not determined by where you incorporate. Instead, it depends on where "control and management" of the business is exercised — typically where the board of directors meets and makes strategic decisions.

How control and management is assessed:

- A company incorporated in Singapore but controlled from abroad may be non-resident

- A company incorporated abroad but controlled from Singapore may be resident

- For virtual board meetings, at least 50% of authorized directors must be physically in Singapore, or the Chairman must be present

- Singapore branches of foreign companies are generally treated as non-resident (controlled by their foreign parent)

Getting residency right has direct tax consequences:

- Only resident companies qualify for the Startup Tax Exemption

- Non-residents face different withholding tax obligations

- Residents can obtain a Certificate of Residence (COR) to access Singapore's 90+ Double Tax Agreements (DTAs)

Tax Exemption Schemes and CIT Rebates

Singapore's tax exemption framework is structured in two tiers — one for qualifying new companies, one for everyone else — plus annual rebates that IRAS applies automatically.

Startup Tax Exemption Scheme (SUTE)

Qualifying newly incorporated companies enjoy enhanced exemptions for their first three consecutive Years of Assessment:

Exemption structure (YA 2020 onwards):

- 75% exemption on the first SGD 100,000 of normal chargeable income

- 50% exemption on the next SGD 100,000

- Maximum exemption: SGD 125,000 per year

Qualifying conditions:

- Incorporated in Singapore

- Tax resident in Singapore

- No more than 20 shareholders

- At least one individual shareholder holding ≥10% shares

- Excludes: Investment holding companies and property development companies

Partial Tax Exemption Scheme (PTE)

All companies that don't qualify for SUTE (including from their fourth YA onwards, branches, and investment holding companies) can claim PTE:

Exemption structure (YA 2020 onwards):

- 75% exemption on the first SGD 10,000 of normal chargeable income

- 50% exemption on the next SGD 190,000

- Maximum exemption: SGD 102,500 per year

YA 2026 CIT Rebate and Cash Grant

For YA 2026, the government has announced:

- 50% CIT Rebate on tax payable, capped at SGD 40,000

- SGD 2,000 non-taxable CIT Rebate Cash Grant for active companies with local employees (those making CPF contributions in 2025)

Important: IRAS applies these rebates automatically. Do not adjust your ECI or Form C filings to account for the rebate.

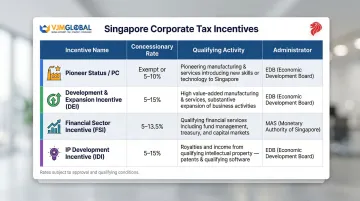

Major Tax Incentives Beyond Exemptions

Beyond the SUTE and PTE tiers, Singapore grants concessionary (reduced) tax rates to companies in specific industries or activities. Each incentive is awarded for a fixed period and requires substantive economic activity in Singapore to qualify.

| Incentive | Rate | Qualifying Activity | Administrator |

|---|---|---|---|

| Pioneer Status / Pioneer Services (PC) | Exempt or 5%–10% | Pioneering manufacturing or services activities | EDB |

| Development and Expansion Incentive (DEI) | 5%, 10%, or 15% | High value-added manufacturing or services | EDB |

| Financial Sector Incentive (FSI) | 5%–13.5% | Qualifying financial services income | MAS |

| IP Development Incentive (IDI) | 5%, 10%, or 15% | Royalties from qualifying patents and software copyrights (modified nexus approach) | EDB |

To apply for any of these incentives, companies submit applications to the relevant agency — EDB for most industrial incentives, MAS for financial sector incentives — typically before commencing the qualifying activity.

Foreign-Sourced Income Exemption (FSIE)

Foreign dividends, branch profits, and service income received in Singapore by tax residents are exempt if:

- Subject to tax in the source country

- Source country's headline tax rate ≥15%

- Exemption is beneficial to the company

Alternative: Companies can elect for Foreign Tax Credit (FTC) pooling, which allows aggregating foreign taxes paid across jurisdictions to offset Singapore tax on pooled foreign income.

How Chargeable Income Is Computed

Chargeable income is not simply your accounting profit. Four adjustments reduce gross profit to taxable income: deductible expenses, capital allowances, approved donations, and available exemptions. Getting each one right determines your actual tax bill.

Definition of Chargeable Income

Chargeable income = Profits from trade, business, or vocation – deductible expenses – capital allowances – approved donations

No Capital Gains Tax (With One Exception)

Singapore generally does not impose capital gains tax on gains from selling property, shares, or financial instruments—unless the gains are considered revenue (trading) income under the "badges of trade" test.

New rule from 1 January 2024: Under Section 10L, foreign-sourced disposal gains received in Singapore by covered entities of an MNE group may be taxable if the entity lacks adequate economic substance in Singapore. Gains from disposing of foreign Intellectual Property Rights (IPRs) are strictly taxable regardless of substance.

Deductibility of Business Expenses

Under Section 14(1) of the Income Tax Act, expenses are deductible only if "wholly and exclusively" incurred in producing income.

Commonly deductible:

- Staff salaries and CPF contributions

- Office rent and utilities

- Professional fees (accounting, legal, consulting)

- Marketing and advertising costs

- Business travel expenses

Not deductible:

- Capital expenditure (use capital allowances instead)

- Private or domestic expenses

- Fines and penalties

- Expenses not related to income production

Capital Allowances

Capital expenditure on qualifying assets (plant, machinery, equipment, certain IP rights) is deducted through capital allowances (Singapore's equivalent of tax depreciation).

Standard rates:

- Plant and machinery: 3-year write-off (33.3% annually)

Accelerated options:

- 1-year write-off (100%): Computers, prescribed automation equipment, low-value assets (≤SGD 5,000 each, capped at SGD 30,000 per YA)

- Section 19B: Writing-down allowances for acquiring qualifying IPRs

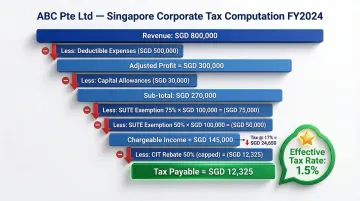

The worked example below pulls all four adjustments together to show how a startup's headline profit of SGD 300,000 translates to an effective tax rate well below 17%.

Simplified Tax Computation Example

ABC Pte Ltd - First Year of Operation (YA 2025)

| Item | Amount (SGD) |

|---|---|

| Revenue | 800,000 |

| Less: Deductible expenses | (500,000) |

| Adjusted profit | 300,000 |

| Less: Capital allowances | (30,000) |

| Profit before exemptions | 270,000 |

| Less: Startup Tax Exemption – 75% × first SGD 100,000 | (75,000) |

| Less: Startup Tax Exemption – 50% × next SGD 100,000 | (50,000) |

| Chargeable income | 145,000 |

| Tax at 17% | 24,650 |

| Less: YA 2026 CIT Rebate (50%, max SGD 40,000) | (12,325) |

| Tax payable | 12,325 |

Effective tax rate: 1.5% (versus headline 17%)

Corporate Tax Filing Requirements and Deadlines

Every Singapore-incorporated company must submit two annual tax filings to IRAS — miss either deadline and you're looking at estimated assessments, composition penalties, or court summons. Here's what each filing requires and when it's due.

Two Required Filings

1. Estimated Chargeable Income (ECI)

- Deadline: Within 3 months from financial year-end

- Purpose: Provisional income estimate for the year

- Waiver: Available if annual revenue ≤ SGD 5 million AND ECI is nil

2. Form C-S / C-S (Lite) / Form C

- Deadline: 30 November each year (e-filing)

- Which form:

- Form C-S: Revenue ≤ SGD 5 million, no complex claims (group relief, foreign tax credit)

- Form C-S (Lite): Revenue ≤ SGD 200,000

- Form C: All other companies

Record-Keeping Obligations

Companies must maintain source documents, accounting records, and supporting schedules for at least 5 years from the relevant YA. Non-compliance risks disallowed expenses and fines up to SGD 5,000.

Additional requirement: Companies with gross revenue exceeding SGD 10 million must maintain contemporaneous transfer pricing documentation and submit it within 30 days upon IRAS request.

Penalties for Late or Non-Filing

Getting either filing wrong — or missing it entirely — triggers a tiered penalty structure:

- IRAS may issue an estimated Notice of Assessment (NOA), which must be paid within one month even if you object

- Composition amount of up to SGD 5,000 per offence may be offered

- Continued non-compliance can lead to court summons, resulting in penalties of twice the tax assessed plus additional fines

- Transfer pricing non-compliance attracts a 5% surcharge on the adjustment amount, regardless of whether additional tax is payable

What Foreign Companies and MNEs Need to Know

Foreign businesses face additional considerations when operating in Singapore, particularly regarding residency, withholding tax, and new global minimum tax obligations.

Foreign Branch Taxation

A Singapore branch of a foreign company is taxed as a non-resident:

- Pays 17% CIT on Singapore-sourced income

- Eligible for Partial Tax Exemption

- Not eligible for Startup Tax Exemption

- Generally cannot obtain a Certificate of Residence for DTA benefits

Withholding Tax on Payments to Non-Residents

Certain payments to non-residents are subject to withholding tax:

| Payment Type | Standard Rate |

|---|---|

| Interest | 15% |

| Royalties | 10% |

| Rent on movable property | 15% |

| Management / technical service fees | 17% (if services performed in Singapore) |

These rates can be reduced under Singapore's network of over 90 Double Tax Agreements (DTAs).

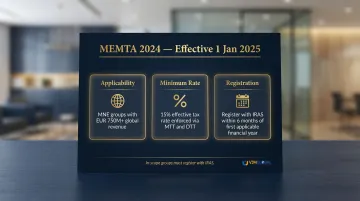

Singapore's BEPS 2.0 / Global Minimum Tax

Singapore enacted the Multinational Enterprise (Minimum Tax) Act 2024 (MEMTA), effective for financial years starting on or after 1 January 2025.

Key points:

- Applies to MNE groups with annual global revenues of EUR 750 million or more

- Imposes a 15% minimum effective tax rate via:

- Multinational Enterprise Top-up Tax (MTT) – equivalent to Income Inclusion Rule

- Domestic Top-up Tax (DTT) – domestic minimum tax

- In-scope groups must register with IRAS within 6 months of their first applicable financial year

Transfer Pricing Rules

Related-party transactions must be conducted on arm's-length terms. Non-compliance attracts a 5% surcharge on transfer pricing adjustments, even if no additional tax is due.

Companies with gross revenue exceeding SGD 10 million must prepare transfer pricing documentation contemporaneously.

Navigating Complexity Across Jurisdictions

For companies with operations in both Singapore and India, tax exposure spans multiple frameworks — Singapore CIT, Indian income tax, FEMA compliance, and applicable DTA provisions all intersect.

VJM Global works with foreign companies to map these obligations clearly — from transfer pricing documentation and treaty benefit claims to FEMA filings for India-side operations. With 30+ years of experience in cross-border tax and advisory, the firm has helped hundreds of American, UK, and Australian businesses structure their Asia-Pacific operations compliantly.

Frequently Asked Questions

How much is corporate tax in Singapore?

Singapore levies a flat 17% corporate income tax rate on chargeable income for all companies. However, effective tax rates are typically much lower due to exemption schemes—qualifying startups can achieve effective rates below 5% in their first three years.

Is Singapore corporate tax on profit or revenue?

Corporate income tax is assessed on chargeable income (profits), not gross revenue. Revenue itself is not taxed—only your net taxable profits after allowable deductions, capital allowances, and exemptions are subject to the 17% rate.

What is the corporate tax filing deadline in Singapore?

Two deadlines apply: ECI must be filed within 3 months of your financial year-end, and Form C-S/C-S (Lite)/Form C must be filed by 30 November each year. Both are mandatory unless specific waivers apply — for example, the ECI waiver for companies with revenue ≤ SGD 5 million and nil ECI.

Do foreign companies pay corporate tax in Singapore?

Yes, foreign companies operating through Singapore branches are taxed at 17% on Singapore-sourced income. They qualify for Partial Tax Exemption but not the Startup Tax Exemption. Non-residents may also face withholding tax on certain Singapore-sourced payments, with relief available under applicable tax treaties.

What is the startup tax exemption in Singapore?

Qualifying newly incorporated Singapore-resident companies receive 75% exemption on the first SGD 100,000 and 50% exemption on the next SGD 100,000 of normal chargeable income for their first three consecutive Years of Assessment. The maximum exemption is SGD 125,000 per year (from YA 2020 onwards).

Does Singapore have a capital gains tax?

Singapore does not impose capital gains tax. However, gains treated as trading income under the "badges of trade" are taxable. From 1 January 2024, certain foreign asset disposal gains received in Singapore by entities without adequate economic substance may be subject to income tax under Section 10L.