Introduction

If you've searched for "VAT in Singapore" and found conflicting information, here's the clarification: Singapore doesn't use the term VAT. Instead, the country applies GST (Goods and Services Tax) — which works exactly like the VAT systems used across Europe and Australia. The name differs, but the mechanism is the same: a consumption tax added at each stage of the supply chain, with the end consumer bearing the full cost.

For foreign businesses entering Singapore or selling to Singapore customers, understanding GST obligations is a compliance requirement you can't afford to overlook. Singapore is a major hub for cross-border commerce, attracting businesses from the US, UK, Australia, and beyond. Whether you're establishing a local entity, selling digital services, or shipping low-value goods to Singapore consumers, you may face GST registration and filing obligations, even without a physical presence.

This guide covers Singapore's GST system from a foreign business perspective: current rates, registration thresholds, the Overseas Vendor Registration (OVR) regime, how to charge and claim GST, filing requirements, and penalties for non-compliance. If the OVR regime applies to you — and for many foreign digital and e-commerce sellers it does — the obligations start earlier than most businesses expect.

Key Takeaways

- Singapore uses GST (not VAT) — currently set at 9% for most goods and services since January 2024

- Mandatory registration threshold: SGD 1 million taxable turnover; foreign digital sellers face a lower SGD 100,000 threshold for B2C supplies under OVR

- Zero-rated exports (0%) allow full input tax recovery; exempt supplies like financial services and residential property do not

- File quarterly via myTax Portal: GST returns (Form F5) are due within one month of each accounting period — late filing triggers automatic penalties

- OVR regime applies to cross-border sellers: foreign businesses selling digital services or low-value goods to Singapore consumers must register, charge 9% GST, and file returns

GST Rates in Singapore: What You'll Pay

Singapore's standard GST rate is 9%, effective 1 January 2024. This followed two recent increases: from 7% to 8% in January 2023, then to the current 9% rate. If you're setting up systems or updating pricing, ensure you apply the correct 9% rate — not outdated figures from prior years.

This 9% rate applies to most supplies of goods and services made within Singapore. However, not all transactions are taxed at this rate. Singapore's GST system divides supplies into four categories:

Standard-rated (9%): Most local sales fall here — retail goods, professional services, restaurant meals, software subscriptions sold to Singapore customers, and imported low-value goods delivered to consumers.

Zero-rated (0%): Zero-rated supplies are still taxable supplies under GST law, but charged at 0%. The key benefit: businesses making zero-rated supplies can claim back input tax on their costs. Zero-rated supplies primarily include:

- Exports of goods (shipped out of Singapore)

- International services such as cross-border transport and services directly connected to goods or land outside Singapore

Zero-rating keeps Singapore's exports competitive by removing GST from the final price.

Quick Comparison:

| Supply Type | GST Rate | Common Examples | Input Tax Claimable? |

|---|---|---|---|

| Standard-rated | 9% | Local retail, professional services, imported low-value B2C goods | ✅ Yes |

| Zero-rated | 0% | Exported goods, international transport, international services | ✅ Yes |

| Exempt | N/A | Financial services, residential property sale/lease, digital payment tokens | ❌ No |

| Out-of-scope | N/A | Private transactions, third-country sales, sales within Free Trade Zones | N/A |

Exempt Supplies

Exempt supplies fall outside GST entirely — no GST is charged, and businesses making only exempt supplies cannot register for GST or claim input tax on their costs. Key exempt categories include:

- Bank accounts, currency exchange, loans, and insurance (financial services)

- Sale and lease of unfurnished residential homes and apartments

- Gold, silver, and platinum meeting specific purity standards (investment precious metals/IPM)

- Cryptocurrency and similar digital assets (digital payment tokens)

Unlike zero-rated supplies — where input tax recovery remains fully available — making exempt supplies means GST on your costs is a permanent expense, not a recoverable one.

Out-of-scope supplies sit entirely outside Singapore's GST system: goods delivered overseas to overseas (third-country sales), goods sold within Free Trade Zones, and private non-business transactions. No GST treatment applies.

Who Needs to Register for GST in Singapore?

GST registration becomes mandatory when your taxable turnover exceeds SGD 1 million in a 12-month period. Singapore applies two tests:

Retrospective test: Did your taxable turnover exceed SGD 1 million in the last calendar year (1 January to 31 December)?

Prospective test: Do you reasonably expect your taxable turnover to exceed SGD 1 million in the next 12 months?

If either test is met, you must register. From 1 July 2025, businesses registering under the prospective test receive a 2-month grace period before they must start charging GST.

This threshold applies to both local and foreign businesses making taxable supplies in Singapore. "Taxable turnover" includes all standard-rated and zero-rated supplies — but excludes exempt supplies.

Voluntary registration:

Businesses below the SGD 1 million threshold can register voluntarily. Benefits include claiming input tax on purchases, which can improve cash flow if you incur significant GST on expenses. However, voluntary registration comes with obligations:

- Must remain registered for at least 2 years

- Required to set up a GIRO account for GST payments

- Must make taxable supplies within 2 years of registration

- Must charge GST to all customers and file quarterly returns

Overseas Vendor Registration (OVR) Regime

The rules shift for foreign businesses once you move beyond local registration. The OVR regime — introduced in January 2020 for digital services and expanded in January 2023 to cover low-value goods and non-digital remote services — sets out a separate framework for overseas vendors selling to Singapore consumers.

OVR registration is required if:

- Your global annual turnover exceeds SGD 1 million, AND

- Your B2C supplies to Singapore customers exceed SGD 100,000 annually

This lower SGD 100,000 threshold applies specifically to business-to-consumer (B2C) sales. If you're a SaaS company, digital product seller, e-commerce platform, or online service provider serving Singapore consumers, you likely fall under OVR.

What qualifies as "low-value goods" (LVG)?

Goods located outside Singapore at the time of sale, delivered by air or post, not subject to import duties (or duties waived), and valued at SGD 400 or less.

How OVR differs from standard registration:

The OVR regime is a simplified pay-only system. You charge and remit GST but cannot claim input tax on your costs. Beyond that, you don't need to appoint a local agent or provide a security deposit. That's a meaningful difference from standard non-resident registration, which requires appointing a Section 33(1) fiscal representative who becomes jointly liable for your GST obligations.

B2B vs B2C treatment under OVR:

By default, OVR treats all sales as B2C (you charge GST). However, if your customer provides a valid Singapore GST registration number at checkout, the transaction becomes B2B — you don't charge GST, and the Singapore-registered customer accounts for GST under reverse charge instead.

For foreign businesses, OVR registration, fiscal representative requirements, and ongoing filing obligations can add up quickly. Working with cross-border tax advisors who understand Singapore's compliance framework helps ensure you register correctly, apply the right treatment to each transaction, and stay current as the rules evolve.

How GST Works: Charging, Claiming, and Input Tax Credits

Singapore's GST operates as a value-added tax system where businesses collect GST from customers and reclaim GST paid to suppliers, remitting only the net difference to IRAS (Inland Revenue Authority of Singapore).

Output Tax vs. Input Tax

Output tax is the GST you charge customers when selling goods or services — typically at 9%. You collect it on IRAS's behalf and remit it with your GST return. Only GST-registered businesses are legally permitted to charge GST.

Input tax is the GST you pay to suppliers when purchasing goods or services for your business. Registered businesses can claim this back from IRAS, subject to three conditions:

- Purchase must be for business purposes

- Must hold a valid tax invoice showing the supplier's GST registration number

- Expense must relate to taxable supplies (standard-rated or zero-rated)

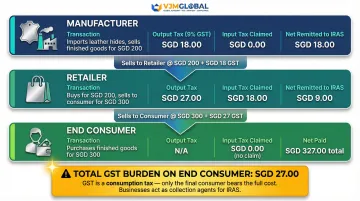

How the Input/Output Mechanism Works

The net effect: each business in the supply chain pays GST only on its own value-add. The end consumer bears the full tax burden.

| Party | Transaction | Output Tax | Input Tax Claimed | Net Remitted to IRAS |

|---|---|---|---|---|

| Manufacturer | Imports leather; sells bag to retailer for SGD 200 | SGD 18 | SGD 9 (import GST) | SGD 9 |

| Retailer | Buys bag for SGD 200; sells to consumer for SGD 300 | SGD 27 | SGD 18 (paid to manufacturer) | SGD 9 |

| End Consumer | Buys bag for SGD 300 | — | — | SGD 27 (full burden) |

Reverse Charge Mechanism

The standard input/output mechanism covers domestic transactions. For cross-border purchases, Singapore applies a different rule: reverse charge.

Under reverse charge, the Singapore buyer — not the overseas seller — accounts for GST on imported services and low-value goods purchased from overseas suppliers.

When it applies: When a GST-registered Singapore business procures services from an overseas vendor — such as cloud software, consulting, or marketing services — the local business must self-account for GST "as if they were the supplier." This catches businesses using international SaaS tools, engaging foreign consultants, or purchasing digital services from non-OVR registered vendors.

Reverse charge also applies to partially exempt businesses importing low-value goods for business use.

How it works: You report the GST due as output tax on your GST return, then immediately claim it back as input tax — provided your business makes only taxable supplies. Partially exempt businesses may not recover the full amount, making the net cost a real expense rather than a pass-through.