Introduction

Singapore's GST shares a name with India's tax, but little else. Where India runs a dual-GST system with five rate slabs (0%, 5%, 12%, 18%, 28%), monthly filings, and separate CGST/SGST authorities, Singapore operates under a single authority — the Inland Revenue Authority of Singapore (IRAS) — with one standard rate of 9% and quarterly filing cycles.

That structural gap is where most Indian businesses run into compliance trouble.

For Indian IT firms, SaaS providers, e-commerce platforms, and professional service businesses entering Singapore, the differences run deeper than the rate:

- Registration thresholds differ substantially (SGD 1 million vs. INR 20–40 lakh)

- The Overseas Vendor Registration (OVR) regime adds B2C obligations that catch many foreign vendors off guard

- The input tax credit mechanism works differently from India's ITC rules

This guide walks through Singapore GST rates, registration triggers, how the input/output tax mechanism works, and what Indian businesses specifically need to know to stay compliant.

Key Takeaways

- Singapore's GST rate is 9% as of January 2024, administered by IRAS under a single-rate, single-authority system

- Mandatory registration applies once taxable turnover exceeds SGD 1 million; Indian digital service providers selling into Singapore may separately trigger Overseas Vendor Registration (OVR) obligations at SGD 100,000

- GST-registered businesses charge output tax on sales, claim input tax on purchases, and remit the difference quarterly

- Singapore and India's GST differ fundamentally in rate structure, filing frequency, and exemption categories

- Input tax on motor cars, medical benefits, and family benefits cannot be claimed — a common compliance pitfall for Indian businesses new to Singapore

What Is Singapore GST? A Primer for Indian Businesses

Legal Basis and Core Definition

Singapore's Goods and Services Tax (GST) is a broad-based consumption tax levied on nearly all goods and services supplied locally and imported into Singapore. Functionally equivalent to VAT in most countries, it is governed by the Goods and Services Tax Act (Cap. 117A) and administered by the Inland Revenue Authority of Singapore (IRAS).

Historical Rate Trajectory

Singapore introduced GST at 3% in April 1994, with progressive increases driven by healthcare spending, rising elderly care costs, and infrastructure investment needs:

| Effective Date | GST Rate |

|---|---|

| 1 April 1994 | 3% |

| 1 January 2003 | 4% |

| 1 January 2004 | 5% |

| 1 July 2007 | 7% |

| 1 January 2023 | 8% |

| 1 January 2024 | 9% |

As of April 2026, Singapore's Ministry of Finance has not announced further rate increases.

Structural Comparison: India GST vs. Singapore GST

For Indian businesses accustomed to a multi-slab, dual-authority system, Singapore's structure is notably simpler — but the differences run deeper than just the rate.

| Feature | India GST | Singapore GST |

|---|---|---|

| Tax Authority | Dual structure (CGST/SGST/IGST) | Single national authority (IRAS) |

| Rate Structure | Multi-slab: 0%, 5%, 12%, 18%, 28% | Single standard rate: 9% |

| Registration Threshold (Goods) | INR 40 lakh (Normal); INR 20 lakh (Special category) | SGD 1 million |

| Registration Threshold (Services) | INR 20 lakh (Normal); INR 10 lakh (Special category) | SGD 1 million |

| Filing Cycle | Monthly (GSTR-1, GSTR-3B); quarterly for QRMP | Quarterly (GST F5) |

| HSN/SAC Codes | Mandatory for classification | Not required |

Four Conditions for GST Applicability

A transaction is subject to Singapore GST only when all four conditions are met:

- Made in Singapore — the supply occurs within Singapore's jurisdiction

- Taxable supply — the supply is standard-rated or zero-rated (not exempt)

- Made by a taxable person — the supplier is GST-registered or liable to register

- In the course of business — the supply occurs as part of business operations, not private activities

Out-of-Scope Supplies

Transactions falling outside Singapore's GST Act include:

- Goods delivered overseas — goods shipped from one overseas location to another without entering Singapore

- Private transactions — non-business activities performed without payment or commercial expectation

- Supplies by non-registered businesses — entities below the registration threshold making taxable supplies

Knowing which transactions fall out of scope directly affects how Indian businesses structure their Singapore operations — and whether GST registration is triggered from day one.

Current GST Rates, Exemptions, and Zero-Rated Supplies

Three Supply Categories

| Category | Rate | Input Tax Recovery | Examples |

|---|---|---|---|

| Standard-Rated | 9% | Fully claimable | Most local sales of goods and services |

| Zero-Rated | 0% | Fully claimable | Exports of goods; international services (cross-border freight, air/sea transport) |

| Exempt | No GST | Not claimable | Residential property sale/lease; most financial services; investment precious metals; digital payment tokens |

Practical Implications for Indian Businesses

The distinction between exempt and zero-rated supplies has a direct impact on cash flow and pricing:

- Zero-rated businesses (e.g., exporters, international freight providers) can claim input tax in full, so GST costs don't accumulate on purchases

- Exempt businesses (e.g., financial services firms, residential property companies) cannot claim input tax, meaning GST on purchases becomes a direct business cost

Indian financial services or real estate-adjacent companies entering Singapore must factor this into their cost structure and pricing strategy.

Recent GST Regime Expansion (January 2023)

Beyond the standard supply categories, Singapore's 2023 reforms expanded GST coverage in ways that directly affect Indian businesses operating digitally or cross-border:

- Imported low-value goods (LVG) — goods under SGD 400 delivered via air or post now attract GST at the point of import, affecting Indian e-commerce businesses selling physical products to Singapore consumers

- Remote/non-digital services — B2C services supplied and received remotely (telemedicine, online counselling, consulting) now fall under OVR obligations

Who Needs to Register for GST in Singapore?

Mandatory Registration Thresholds

Businesses must register for GST if taxable turnover (standard-rated plus zero-rated supplies) exceeds SGD 1 million under either:

- Retrospective basis: taxable turnover for the calendar year (1 Jan to 31 Dec) exceeded SGD 1 million

- Prospective basis: reasonable expectation that taxable turnover will exceed SGD 1 million in the next 12 months

Submit applications via IRAS's myTax Portal. IRAS processes 60% of applications within 10 working days, with the remainder completed within 30 days. Voluntary registrants receive approval within 2 weeks from the approval letter date.

Voluntary GST Registration

Indian businesses below the SGD 1 million threshold may register voluntarily to claim input tax on Singapore business expenses. This makes financial sense for:

- Startups making significant capital investments in equipment or infrastructure

- B2B service providers with substantial local operating costs

- Businesses in early growth phases expecting to cross the threshold soon

Voluntary registration comes with three conditions:

- Must remain registered for at least 2 years

- Must use GIRO for payments and refunds

- Must complete an IRAS e-Learning course

Overseas Vendor Registration (OVR) Regime

For Indian companies selling directly to Singapore consumers — rather than through a local entity — a separate regime applies. Businesses providing digital services (software, SaaS, apps, online content) or remote services (online consulting, telemedicine) must register under OVR if:

- Global revenue exceeds SGD 1 million, AND

- Key characteristics of the OVR regime:

- Applies to B2C transactions only — B2B transactions are handled via Reverse Charge

- Digital services have been covered since 1 January 2020

- Non-digital remote services were added from 1 January 2023

- Simplified "pay-only" structure: overseas vendors charge and remit GST but cannot claim input tax

Reverse Charge Mechanism for B2B Imported Services

Where the Singapore buyer is a GST-registered business making both taxable and exempt supplies (partially exempt), the obligation shifts. That business must self-account for GST on services imported from Indian suppliers. This means:

- The Indian supplier does not register for Singapore GST

- The Singapore client self-accounts for GST on the invoice

- Singapore clients will often request specific invoicing documentation from Indian IT firms and consultants

In practice, Indian service providers don't register or charge Singapore GST on B2B services. However, clients may ask you to confirm the service is subject to reverse charge and to provide invoices explicitly showing that no GST has been charged.

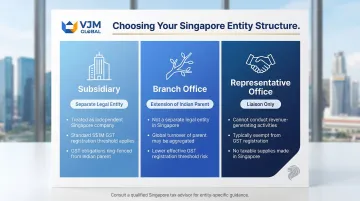

Entity Structure Considerations

A "taxable person" under Singapore's GST Act includes individuals, companies, partnerships, and non-profit organisations. Indian businesses with a Singapore subsidiary, branch, or representative office each face distinct registration obligations:

- Subsidiary: treated as a separate legal entity; subject to standard registration thresholds

- Branch office: extension of the Indian parent; turnover aggregated globally for threshold purposes

- Representative office: typically limited to liaison activities; usually not subject to GST registration

Choosing the right entity structure shapes your GST obligations from day one — a decision worth mapping carefully before Singapore market entry.

How Singapore GST Works: Charging, Claiming, and the Input Tax Credit Mechanism

Output Tax: Charging and Invoicing

Once registered, GST-registered businesses must:

- Charge 9% GST on all standard-rated taxable supplies

- Issue a valid tax invoice to GST-registered customers within 30 days of the time of supply

- Collect this output tax and account for it to IRAS

Input Tax: Claiming and Conditions

Businesses can claim back GST paid on business purchases and imports (input tax), subject to strict conditions:

- Claimant is GST-registered

- Goods/services are supplied to or imported by the claimant

- Supported by a valid tax invoice or import permit

- Used for making taxable supplies (not exempt supplies)

- Claimed within 5 years from the end of the relevant accounting period

Blocked Input Tax (Key Restrictions for Indian Businesses)

Certain expenses are blocked from input tax claims under Singapore law, which differs from India's GST framework:

- Motor car costs — purchase, lease, running expenses, and maintenance (unless specifically excluded from the 'motor car' definition)

- Medical expenses — staff healthcare costs (unless mandatory under Work Injury Compensation Act or specific health risk advisories)

- Family benefits — benefits provided to family members or relatives of staff

- Club subscriptions — membership fees for recreational or social clubs

In India, many of these expenses qualify for input tax credit — Singapore's rules are stricter, and misapplying Indian assumptions here is a common compliance error.

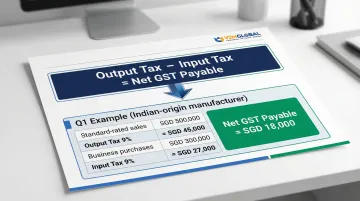

Net GST Payment Mechanism

Calculation: Net GST payable = Output Tax collected - Input Tax claimed

Two scenarios follow from this formula:

If output tax > input tax: Pay the difference to IRAS within one month of the accounting period end (or 15 days later if using GIRO).

If input tax > output tax: IRAS refunds the difference within a period matching your accounting cycle — for example, within 3 months for quarterly filers. The refund is processed from the date IRAS receives your return, provided no outstanding returns or audits are pending.

Example (Indian-origin manufacturer in Singapore):

- Standard-rated sales for Q1: SGD 500,000

- Output tax charged (9%): SGD 45,000

- Business purchases: SGD 300,000

- Input tax paid (9%): SGD 27,000

- Net GST payable: SGD 45,000 - SGD 27,000 = SGD 18,000

GST vs. Withholding Tax: Two Separate Obligations

Indian businesses often confuse GST with withholding tax. The two operate independently and carry different compliance requirements:

| GST | Withholding Tax | |

|---|---|---|

| What it covers | Consumption tax on supplies | Payments to non-residents (royalties, interest, service fees) |

| Rate | 9% on standard-rated supplies | Varies by payment type and tax treaty |

| How it's settled | Paid/claimed through quarterly returns | Deducted at source by the Singapore payer |

India-Singapore DTAA: The Double Taxation Avoidance Agreement between India and Singapore provides treaty relief on withholding tax rates. Headline rates for non-residents include:

- Interest, loan fees: 15%

- Royalties: 10%

- Technical assistance/service fees: Prevailing corporate tax rate or 24% for individuals

Important: If an imported service attracts withholding tax, the GST Reverse Charge value is the full consideration paid, without deducting the withholding tax amount.

GST Filing and Compliance Requirements

Standard Filing Cycle and Deadlines

Quarterly filing (GST F5):

- Returns and payments due one month after the accounting period ends

- GIRO extension: Businesses using GIRO receive an additional 15 days; deductions occur on the 15th day of the month following the filing due date

- All filing is electronic via IRAS's myTax Portal

Monthly filing option:

- Businesses regularly receiving GST refunds can apply to IRAS for monthly accounting periods

- Subject to IRAS approval

- Faster refund turnaround (within 1 month instead of 3 months)

Record-Keeping Requirements

GST-registered businesses must retain all business and accounting records for at least 5 years, including:

- Tax invoices (issued and received)

- Import permits

- Credit notes and debit notes

- Sales and purchase records

- Bank statements and payment documentation

Digital record-keeping:

- Fully accepted and encouraged by IRAS

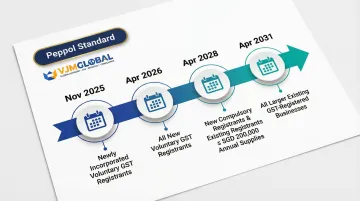

- InvoiceNow e-invoicing initiative based on Peppol standard

- Mandatory transmission of invoice data to IRAS being phased in from November 2025 through April 2031

InvoiceNow phased implementation timeline:

| Effective Date | Businesses Covered |

|---|---|

| 1 Nov 2025 | Newly incorporated companies registering voluntarily |

| 1 Apr 2026 | All new voluntary registrants |

| 1 Apr 2028 | New compulsory registrants + existing registrants with annual supplies ≤ SGD 200,000 |

| Phased to 1 Apr 2031 | All larger existing businesses |

Penalties and Voluntary Disclosure

Late filing penalties:

- SGD 200 imposed immediately

- Additional SGD 200 for every completed month outstanding

- Maximum SGD 10,000 per return

Late payment penalties:

- 5% penalty on unpaid tax

- Additional 2% per month if unpaid after 60 days

- Capped at 50% of outstanding tax

Wrongful collection:

- Charging GST without being registered is an offence under Section 64A

- Penalty: 3 times the amount collected + fine up to SGD 10,000

Voluntary Disclosure Programme (VDP):

- IRAS offers reduced penalties for businesses that voluntarily disclose past errors or omissions

- Applies to incorrect GST returns, under-declared output tax, or over-claimed input tax

- Disclosure should be made proactively before IRAS audit or investigation

For Indian businesses, building compliance processes from day one — rather than retrofitting them later — is the smarter move. IRAS conducts periodic GST audits, and proactive disclosure through the VDP can meaningfully reduce penalties when errors surface.

Frequently Asked Questions

What is the Goods and Services Tax (GST) in Singapore?

Singapore GST is a broad-based 9% consumption tax levied on goods and services supplied locally and imported into Singapore. Administered by IRAS and comparable to VAT in other countries, it operates under a single-rate, single-authority system distinct from India's dual-GST framework.

What is the current GST rate in Singapore and are further increases planned?

The current rate is 9% as of 1 January 2024, following a two-step increase from 7% (2022) to 8% (2023) to 9% (2024). As of the latest official communications (including Budget 2026), no further rate increases have been announced by the Ministry of Finance or IRAS.

Who needs to register for or pay GST in Singapore?

Businesses with taxable turnover exceeding SGD 1 million must register (retrospectively or prospectively), while voluntary registration is available below this threshold. Indian companies supplying digital or remote services to Singapore consumers must also register under the OVR regime if global turnover exceeds SGD 1 million and Singapore B2C sales exceed SGD 100,000.

Do tourists or foreigners have to pay GST in Singapore?

Yes, foreigners and tourists pay 9% GST on purchases from GST-registered businesses. Tourists can claim refunds through the Tourist Refund Scheme (TRS) on eligible purchases of at least SGD 100 when departing within 2 months, though work pass and long-term pass holders are excluded from TRS and GST import relief.

What is the difference between GST and service charge in Singapore?

GST (9%) is a government tax remitted to IRAS, while service charge (typically 10%) is a fee collected and retained by the business (e.g., hotels, restaurants) as staff compensation. The two are separate and often appear together as "++" pricing. GST is calculated on the total price including service charge (e.g., Price × 1.10 × 1.09).

Is there withholding tax on services in Singapore?

Yes, Singapore imposes withholding tax on certain payments to non-residents, including royalties, technical service fees, and interest — with rates varying by payment type and applicable tax treaty. Indian businesses receiving payments from Singapore clients should verify their obligations under the India-Singapore Double Taxation Avoidance Agreement.