Introduction

The US has over 11,000 state and local tax jurisdictions—each setting its own rates, rules, and exemptions. Unlike most countries that use a single national tax system, the United States has no federal sales tax. Foreign companies and e-commerce sellers entering the US market routinely underestimate this complexity.

This fragmentation creates real compliance risk. Businesses that fail to collect and remit sales tax correctly face back taxes, penalties, and interest charges — sometimes across multiple states simultaneously. This guide breaks down how US sales tax works, what triggers a collection obligation, and how to stay compliant.

TLDR

- The US has no federal sales tax; 45 states plus D.C. levy their own state-level taxes

- Five states have no statewide sales tax: Alaska, Delaware, Montana, New Hampshire, and Oregon

- Combined state and local rates can exceed 10% — Louisiana averages 10.11%

- Businesses must collect sales tax wherever they have "nexus," triggered by physical presence or $100,000+ in annual sales

- Sales tax differs fundamentally from VAT systems used in the UK, EU, and Australia

What Is Sales Tax in the USA and How Does It Work?

US sales tax is a consumption tax levied at the point of retail sale on tangible personal property and certain services. Unlike a Value Added Tax (VAT), which applies at multiple stages of production, sales tax is collected once—by the seller from the buyer at checkout—and then remitted to state or local governments.

Sales tax generated $468.1 billion in state government collections in 2024, making it a critical revenue source that states protect aggressively. This revenue dependence explains why states enforce compliance strictly and penalize failures to collect or remit tax.

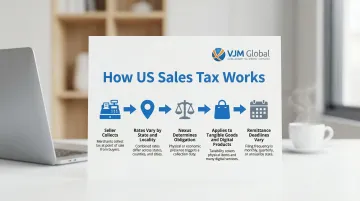

At its most basic, the mechanics follow a consistent pattern across all 45 states that impose it:

- Seller collects tax from the buyer at the point of sale

- Rates vary by state and locality — ranging from 0% (Oregon, Montana) to over 10% in some combined state/local jurisdictions

- Nexus determines obligation — a business must have sufficient connection to a state before it's required to collect

- Applies to tangible goods and, increasingly, select digital products and services

- Remittance deadlines vary by state, ranging from monthly to annually depending on sales volume

Understanding Use Tax

Use tax is the counterpart to sales tax — and it's one most buyers overlook. When you purchase taxable goods from an out-of-state seller who doesn't collect sales tax, you're typically required to self-assess and remit use tax directly to your home state.

According to the California Department of Tax and Fee Administration, use tax applies to "the use, storage, or consumption of personal property" purchased without sales tax paid. For businesses making regular out-of-state purchases, this creates a real compliance obligation — not just a technicality.

Sales Tax Rates Across US States: From Zero to Highest

State-level sales tax rates vary dramatically, and local additions create even wider differences. Here's what businesses need to know:

States With No Sales Tax

Five states impose no statewide sales tax:

- Alaska

- Delaware

- Montana

- New Hampshire

- Oregon

Alaska is a special case—while it has no state tax, local jurisdictions can impose their own taxes, meaning buyers in some Alaskan municipalities still pay sales tax.

Highest State-Level Rates

California leads at 7.25%, followed by four states tied at 7.0%:

- Indiana

- Mississippi

- Rhode Island

- Tennessee

Colorado has the lowest non-zero rate at 2.9%, with Alabama, Georgia, Hawaii, New York, and Wyoming all at 4.0%.

Combined State and Local Rates Tell a Different Story

When local taxes stack on top of state rates, the picture changes dramatically:

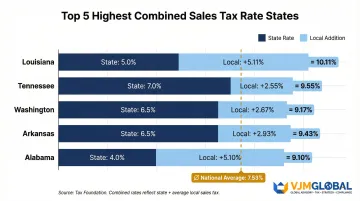

Top 5 Combined Rates (2026):

- Louisiana – 10.11%

- Tennessee – 9.61%

- Washington – 9.51%

- Arkansas – 9.46%

- Alabama – 9.46%

The nationwide average combined rate is 7.53%.

State Rates Can Understate Your Actual Tax Burden

A state's base rate can understate your real exposure. New York's 4% state rate looks modest, but an average local rate of 4.54% pushes the combined average to 8.54%. Colorado's 2.9% climbs to nearly 8% once local taxes apply. Always model both layers before making location or pricing decisions.

Recent Rate Changes

Louisiana increased its state rate from 4.45% to 5.0% effective January 1, 2025 — the most recent statewide rate increase. South Dakota cut its rate from 4.5% to 4.2% in 2023, though this reduction is set to sunset in 2027. Rate cuts at the sales tax level remain uncommon — most states have focused legislative energy on income tax relief instead, leaving sales tax burdens largely stable or rising.

How Local Sales Taxes Stack on Top of State Rates

Thirty-eight states allow local governments—cities, counties, and special districts—to impose additional sales taxes on top of state rates. This means the effective rate depends on the buyer's precise location, not just the state, and tax boundaries don't follow ZIP codes. Businesses need address-level accuracy to get the rate right.

Local Taxes Can Exceed State Taxes

In some states, average local rates exceed state rates:

- Colorado: 2.9% state rate + 4.99% average local = 7.89% combined

- Louisiana: 5.0% state rate + 5.11% average local = 10.11% combined

- New York: 4.0% state rate + 4.54% average local = 8.54% combined

Chicago's combined rate reaches 10.25%, consisting of:

- 6.25% Illinois state tax

- 1.75% Cook County tax

- 1.25% Chicago city tax

- 1.0% Regional Transportation Authority tax

These rate differences drive consumer behavior. Per capita sales in border counties of sales-tax-free New Hampshire have tripled since the late 1950s, while sales in neighboring Vermont border counties stagnated. Consumers cross state lines specifically to avoid higher tax burdens.

Home-Rule Administration Adds Complexity

In Colorado, municipalities that have enacted a "home-rule" charter can administer their own local sales taxes independently of the state. These "self-collected" jurisdictions require businesses to register and file separately at both state and local levels.

For multi-location retailers and e-commerce sellers, this creates a layered compliance workload:

- Register separately with each self-collected jurisdiction

- File local returns on the jurisdiction's own schedule

- Track rate changes independently from state-level updates

- Maintain separate records for state vs. local tax collected

What Is Taxable—and What Is Exempt—Under US Sales Tax?

Tangible personal property is generally taxable, but exemptions vary widely by state. The categories below cover the most common exemptions—and a few areas where businesses frequently get it wrong.

Common Exemption Categories

Groceries/Unprepared Food:

- Most states exempt groceries

- Mississippi taxes groceries at 5% (reduced from 7% effective July 1, 2025)

- Tennessee taxes food at a reduced 4% state rate

Prescription Drugs:

- Exempt in 44 of the 45 states with sales tax

- Illinois is the sole exception, taxing prescriptions at 1%

Clothing:

- New York exempts clothing and footwear under $110 per item

- Pennsylvania generally exempts clothing but taxes formal apparel, fur, and sporting goods

Physical goods follow relatively predictable exemption rules. Digital goods and services are a different story—and the source of most modern compliance surprises.

Digital Goods and Services: The Compliance Challenge

Historically, most states didn't tax services. That's changing. States are increasingly taxing digital products, software, streaming services, and specific enumerated services.

SaaS (Software as a Service):

- Taxable in approximately 24 states, including New York, Texas, and Washington

- Non-taxable in others, including California and Florida

- Taxability varies state by state—always verify before assuming taxability

Resale Exemption and Exemption Certificates

Businesses buying goods for resale can skip sales tax at purchase by providing the seller a valid exemption certificate. Sellers must retain these certificates for audit purposes. Misuse of exemption certificates carries penalties for both buyers and sellers. Keeping accurate records of every certificate collected is one of the simplest ways to protect your business in a sales tax audit.

Sales Tax Compliance for Businesses: Nexus, Registration, and Filing

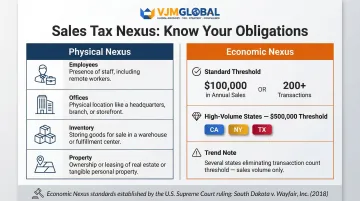

The June 21, 2018 Supreme Court decision in South Dakota v. Wayfair, Inc. reshaped US sales tax law: the Court ruled that states can mandate tax collection from businesses without physical presence in the state. This created "economic nexus" and transformed compliance requirements for e-commerce sellers and foreign companies.

Understanding Nexus

Nexus is the legal connection between a business and a state that creates a sales tax collection obligation. Two types exist:

Physical Nexus:

- Having employees, offices, inventory, or property in a state

- Traditional basis for tax collection obligations

Economic Nexus:

- Exceeding a state's sales or transaction threshold

- All 45 sales-tax states have enacted economic nexus laws post-Wayfair

- Most common threshold: $100,000 in annual sales or 200 transactions into the state

- Higher thresholds: California, New York, and Texas require $500,000 in sales

- Transaction count elimination: States including Illinois, South Dakota, and Wisconsin have eliminated the 200-transaction threshold, relying solely on revenue

Registration and Collection Requirements

Once nexus is established, businesses must:

- Register with the state's tax authority before collecting sales tax—there's no federal registration; each state requires separate registration

- Collect the correct combined rate (state + local) on all taxable transactions shipped or delivered to customers in that state

- Maintain accurate records of all transactions and exemption certificates

Filing and Remittance Obligations

States assign filing frequencies based on sales volume:

- Monthly (high-volume sellers)

- Quarterly (mid-volume sellers)

- Annually (low-volume sellers)

Critical rules:

- File returns and remit collected tax on schedule even if no taxable sales occurred

- Collected sales tax is held in trust for the state

- Failure to remit on time triggers penalties and interest that the business bears

Penalties vary significantly by state. Here's how two major states handle late filings:

California penalties:

- 10% penalty for late filing plus 10% penalty for late payment

- Interest calculated monthly based on IRS rate plus 3%

Texas penalties:

- $50 late filing penalty

- 5% penalty if paid 1-30 days late

- 10% penalty if paid over 30 days late

Origin-Based vs. Destination-Based Sourcing

For intrastate sales, states use either:

Destination-Based (Majority):

- Sales tax based on buyer's location

- Most states use this method

Origin-Based (11 States):

- Sales tax based on seller's location

- Arizona, Illinois, Mississippi, Missouri, New Mexico, Ohio, Pennsylvania, Tennessee, Texas, Utah, Virginia

Important: Remote sellers (out-of-state) almost always use destination-based sourcing, regardless of the state's intrastate rules.

VJM Global's US Tax Compliance Advisory

For multinational companies and foreign businesses with US operations, cross-border tax obligations add another layer of complexity on top of multi-state compliance. VJM Global's international taxation and advisory team has worked with 500+ American business owners and clients across the UK, Australia, and Europe, helping them navigate regulatory requirements on both sides of the border.

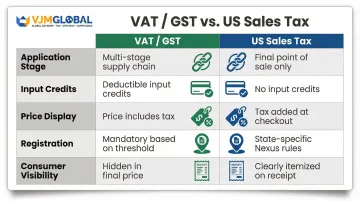

US Sales Tax vs. VAT: Key Differences for International Businesses

The US has no Value Added Tax (VAT) at any level of government—unlike the UK (20% standard VAT), EU member states, and Australia (10% GST). Currently, 176 countries have implemented a VAT or GST system. That makes the US an outlier — and understanding how its system works is essential for any foreign business selling here.

Core Structural Differences

| Feature | VAT/GST | US Sales Tax | |---------|---------|--------------|\n| Application | Multi-stage—applied at every step of the supply chain | Single-stage—applied only at final retail sale | | Input Credits | Businesses claim input tax credits for VAT paid on purchases | No input credits—businesses pay sales tax on their own purchases unless buying for resale | | Price Display | Tax-inclusive pricing (embedded in listed price) | Tax-exclusive pricing (added at checkout as separate line item) | | Registration | Single national registration per country | Separate registration required in each of 45+ states | | Visibility | Hidden from consumer at checkout | Visible as separate line item on receipt |

Practical Implications for Foreign Businesses

Three operational differences tend to catch international businesses off guard:

- Pricing displays exclude tax. Prices are listed without sales tax, which is added as a separate line item at checkout — the opposite of VAT-inclusive pricing common in the UK, EU, and Australia. Invoicing and accounting systems need to reflect this.

- Registration is state-by-state. VAT typically requires one national registration per country. In the US, businesses must register and file separately across 45+ states, making compliance considerably harder to manage for foreign entrants.

- No input tax credits exist. Under VAT, businesses recover tax paid on inputs. US businesses cannot claim credits for sales tax paid on their own purchases — the only exception is inventory bought for resale using a valid exemption certificate.

Frequently Asked Questions

Which US states have no sales tax?

Five states have no statewide sales tax: Alaska, Delaware, Montana, New Hampshire, and Oregon. However, Alaska allows local jurisdictions to levy their own taxes, so some Alaskan municipalities do impose sales taxes.

Which US state has the highest sales tax?

California has the highest state-level rate at 7.25%. Louisiana has the highest combined state and local average rate at 10.11%. Which state "wins" depends on whether you're measuring base rates or combined averages.

What are the 10 states with the highest sales tax?

Based on population-weighted combined state and local rates, the top 10 are:

- Louisiana — 10.11%

- Tennessee — 9.61%

- Washington — 9.51%

- Arkansas — 9.46%

- Alabama — 9.46%

- Oklahoma — 9.06%

- California — 8.99%

- Illinois — 8.96%

- Kansas — 8.69%

- New York — 8.54%

What city in the USA has the highest sales tax?

Seattle, Washington has the highest combined rate among major cities at 10.35%, followed by Chicago, Illinois and Long Beach, California at 10.25%. Some smaller jurisdictions in Louisiana and Alabama push even higher, with certain local rates exceeding 12%.

Which US states have a 7% sales tax?

Indiana, Mississippi, Rhode Island, and Tennessee all have a 7% state-level sales tax rate, making them tied for the second-highest state rate after California.

Does the United States have a VAT, and how does it differ from sales tax?

The US has no VAT at any level of government. VAT is collected at every stage of the supply chain, with businesses receiving input tax credits along the way. US sales tax, by contrast, is charged only once at the final retail sale and appears as a separate line item at checkout.