Introduction

If your business leases office space, equipment, or vehicles in Singapore, your balance sheet looks different than it did before 2019—and that has real consequences for loan covenants, investor reporting, and tax timing.

Singapore's lease accounting landscape shifted on 1 January 2019, when SFRS(I) 16 and FRS 116 replaced the outdated FRS 17 standard. For foreign companies expanding into Singapore or operating branches there, lease commitments can no longer stay off-balance sheet. What was once a simple operating lease expense now appears as a Right-of-Use (ROU) asset and a corresponding lease liability, directly impacting financial ratios and investor perception.

Multinational businesses face a dual challenge: complying with Singapore's Financial Reporting Standards while reconciling differences between accounting treatment and tax deductions. The Inland Revenue Authority of Singapore (IRAS) continues to allow cash-basis lease payment deductions, creating timing differences that must be tracked as deferred tax assets or liabilities.

For cross-border operators managing entities across the UK, USA, Australia, and Singapore, these rules are not theoretical—they affect annual ACRA filings, group consolidations, and intercompany reporting. VJM Global helps foreign businesses navigate exactly this kind of multi-jurisdiction compliance complexity.

Key Takeaways

- Singapore adopted SFRS(I) 16 and FRS 116 (both equivalent to IFRS 16) effective 1 January 2019, replacing FRS 17

- Lessees must now recognise almost all leases on the balance sheet as ROU assets and lease liabilities

- The new standards eliminate "off-balance sheet" operating lease treatment, making all financial obligations visible on the balance sheet

- Short-term leases (12 months or less) and low-value asset leases (approximately USD 5,000 at inception) remain exempt

- IRAS permits cash-basis tax deductions, while accounting standards require depreciation and interest expense — creating deferred tax differences

- Foreign companies operating in Singapore must track and disclose these timing differences in their financial statements

Singapore's Lease Accounting Standards: SFRS(I) 16 and FRS 116

Singapore operates two parallel but substantively identical lease accounting frameworks. SFRS(I) 16 applies to Singapore-incorporated companies listed on SGX or those voluntarily adopting IFRS-aligned standards. FRS 116 applies to all other Singapore entities following the domestic Financial Reporting Standards framework. Both became effective for annual periods beginning on or after 1 January 2019, following the Accounting Standards Council's issuance of FRS 116 on 30 June 2016.

Who Uses Which Standard?

- SGX-listed companies: Apply SFRS(I) 16 (mandatory from 1 January 2018 onward)

- Non-listed Singapore companies: Apply FRS 116

- Practical difference: None for lessees—both standards mirror IFRS 16's recognition and measurement requirements

Core Objective

Both standards ensure that significant lease commitments appear on the balance sheet, giving stakeholders—investors, creditors, regulators, and banks—a complete view of a company's financial obligations. Before 2019, operating lease commitments lived only in footnotes, understating true leverage and debt levels.

Global Context and Consolidation Benefits

Singapore's adoption aligns the country with more than 140 jurisdictions that apply IFRS 16. For multinationals managing entities across Asia-Pacific, Europe, and North America, this alignment directly reduces consolidation complexity.

Key practical benefits for cross-border groups include:

- Consistent lessee recognition across IFRS 16, SFRS(I) 16, and FRS 116 jurisdictions

- Easier reconciliation between US GAAP ASC 842 and Singapore standards — both eliminated the operating vs. finance lease distinction for lessees

- Improved comparability of financial statements across group entities

Early Regulatory Warnings

In December 2016, SGX issued an advisory urging listed issuers to review loan covenants and communicate expected FRS 116 impacts to creditors early. The regulator warned that capitalising previously off-balance sheet leases could trigger covenant breaches or technical defaults if not proactively addressed.

The Accounting Standards Council reinforced this message with a formal reminder to directors and CFOs on 28 December 2016.

Key Changes from FRS 17 to FRS 116

The Problem with FRS 17

Under the old standard, operating leases were treated as executory contracts: companies simply expensed lease payments on the income statement without recording any asset or liability. This "off-balance sheet" treatment meant significant obligations — office leases spanning 5-10 years, equipment leases, vehicle fleets — never appeared on the balance sheet.

Only finance leases were recognised as assets and liabilities, leaving readers with an incomplete picture of a company's true financial commitments.

Fundamental Change: One Model for Lessees

FRS 116 eliminates the lessee-side distinction between operating and finance leases. With limited exemptions, all leases must now be capitalised on the balance sheet. The distinction still exists for lessors, but lessees apply a single recognition model.

Statement-by-Statement Impact

Balance Sheet:

- New ROU assets (representing the lessee's right to use the leased asset)

- New lease liabilities (the present value of future lease payments)

- Increased total assets and total liabilities

Income Statement:

- Operating lease expenses (previously straight-line) are replaced by:

- Depreciation expense on the ROU asset

- Interest expense on the lease liability

- Creates a front-loaded expense profile: higher combined charges in early years, declining over time

- EBITDA typically improves because lease payments are no longer operating expenses—depreciation and interest sit below the EBITDA line

Cash Flow Statement:

- Principal portion of lease payments: classified as financing activities

- Interest portion: classified as operating or financing activities depending on the entity's accounting policy

- Short-term and low-value lease payments: remain in operating activities

- Variable lease payments (not included in lease liability): remain in operating activities

Financial Covenant and Ratio Implications

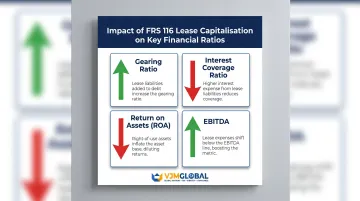

These cash flow reclassifications are significant — but the balance sheet changes carry even broader consequences for companies with existing loan covenants. Bringing leases onto the balance sheet increases reported debt, which directly affects:

- Gearing ratio (debt-to-equity): rises as lease liabilities are added to total debt

- Interest coverage ratio: may decline as interest expense on lease liabilities increases total finance costs

- Return on assets: typically declines as ROU assets inflate the asset base

- EBITDA: improves mechanically (not operationally) because operating lease expenses become depreciation and interest

Foreign companies should:

- Review existing loan agreements for covenant triggers

- Renegotiate or obtain waivers before FRS 116 adoption triggers technical defaults

- Communicate the accounting-driven (not operational) nature of these changes to lenders, investors, and board members

A mid-2016 study by ISCA and Nanyang Business School found that 72% of surveyed companies were aware of FRS 116, yet 53% had not yet started preparing for implementation.

Recognising and Measuring Leases: ROU Assets and Lease Liabilities

Initial Recognition Trigger

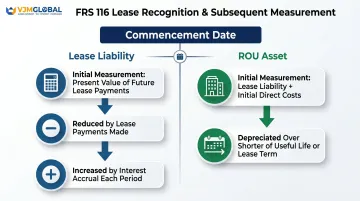

At the lease commencement date—the date when the lessor makes the underlying asset available for use—the lessee records:

- A Right-of-Use (ROU) asset

- A corresponding lease liability

The commencement date is not necessarily the contract signing date; it's when the lessee can physically begin using the leased asset.

Measuring the Lease Liability

The lease liability equals the present value of future lease payments unpaid at commencement. The discount rate is:

- The interest rate implicit in the lease, if readily determinable, or

- The lessee's incremental borrowing rate (IBR) if the implicit rate is unavailable

IBR defined: The rate a lessee would pay to borrow funds, over a similar term and with similar security, to obtain an asset of comparable value in the relevant economic environment. Foreign companies typically reference home-country borrowing costs, adjusted for currency and local Singapore market conditions.

Lease payments included in the liability:

- Fixed lease payments (less any lease incentives receivable)

- Variable lease payments linked to an index or rate (e.g., CPI, market rental rates)

- Amounts expected to be payable under residual value guarantees

- Exercise price of purchase options (if reasonably certain to exercise)

- Termination penalties (if lease term reflects expected termination)

Measuring the ROU Asset

The ROU asset at commencement includes:

- Initial lease liability amount

- Lease payments made on or before commencement (net of incentives received)

- Initial direct costs incurred by the lessee

- Estimated dismantling, removal, or restoration costs

Subsequent Measurement

Lease Liability evolves as follows:

- Reduced as lease payments are made

- Increased by interest accrual each period (interest expense = lease liability × discount rate)

ROU Asset is measured as:

- Depreciated over the shorter of the asset's useful life or the lease term

- Depreciation expense = ROU asset value ÷ lease term (or useful life if shorter)

This structure front-loads expenses. Early in the lease, the liability balance is high — so interest expense is high. Combined with straight-line depreciation, total annual cost (depreciation + interest) exceeds what FRS 17 would have shown. As the liability decreases over time, interest expense falls, and total expense drops below the old straight-line amount.

Lease Modifications and Reassessments

When lease terms change—scope adjustments, payment revisions, exercise of options, or changes in variable payments linked to an index—the lessee must:

- Remeasure the lease liability using the original (unchanged) discount rate

- Adjust the ROU asset correspondingly

- Revise depreciation expense for the remaining term based on the new ROU asset value

This ongoing reassessment adds compliance overhead. Foreign companies operating in Singapore — particularly those managing multi-site office or retail leases — should maintain a centralised lease register that logs modification dates, revised payment schedules, and option exercise deadlines. Auditors in Singapore routinely test whether remeasurement was triggered and correctly applied, making documentation the first line of defence.

Exemptions Under Singapore's Lease Accounting Standards

Short-Term Lease Exemption

Leases with a term of 12 months or less (at commencement date, including reasonably certain renewal options) may be excluded from balance sheet recognition. Instead, lease payments are expensed on a straight-line or other systematic basis.

Application Rule: The exemption must be applied by class of underlying asset, not lease-by-lease. A "class" is a grouping of assets with similar nature and use (for example, all office equipment, all vehicles, all IT hardware). The lessee cannot selectively apply the exemption to individual leases within a class.

Low-Value Asset Exemption

Leases of individual assets valued at approximately USD 5,000 or less when new can be excluded from balance sheet recognition, regardless of the lessee's size or circumstances. Examples include laptops, tablets, small office equipment, and personal computers.

Critical Rule: This exemption is assessed lease-by-lease, giving lessees more flexibility than the short-term exemption. The threshold comes from paragraph BC100 of IFRS 16's Basis for Conclusions, not the standard text itself.

| Exemption Feature | Short-Term Lease | Low-Value Asset |

|---|---|---|

| Threshold | 12 months or less at commencement | Approximately USD 5,000 when new |

| Application basis | By class of underlying asset | Lease-by-lease |

| Affected by lessee size | No | No |

| Expense treatment | Straight-line or systematic | Straight-line or systematic |

Practical Relevance for Foreign Investors

These exemptions reduce compliance complexity for companies leasing primarily short-duration or low-value items, which is typical for tech startups, branch offices, and companies with mobile workforces. Whether an exemption applies depends on the nature of your lease portfolio:

- Likely exempt: Short laptop or tablet leases under 12 months, small IT hardware, minor office equipment under USD 5,000

- Must capitalise: Office premises, warehouses, manufacturing equipment, or any lease exceeding 12 months

- Mixed portfolios: Each asset class must be evaluated separately — exemptions cannot be applied selectively across classes

Foreign investors establishing Singapore operations should map their lease portfolio early to determine which obligations require balance sheet recognition from day one.

Tax and Compliance Implications for Foreign Companies in Singapore

Accounting-Tax Disconnect

While FRS 116 requires lessees to record depreciation and interest in the profit and loss account, IRAS continues to allow tax deductions on a cash basis as contractual lease payments are incurred. This creates timing differences between accounting profit and taxable profit.

Lessee Tax Treatment (Operating Leases for Tax Purposes):

- Deduct the full contractual lease payment under Section 14(1) of the Income Tax Act

- Add back accounting depreciation of ROU asset (not deductible)

- Add back accounting interest on lease liability (not deductible)

- Exchange gains/losses from revaluation of lease liability are disregarded for tax purposes; only realised exchange differences on actual payments are taxable/deductible

Deferred Tax Tracking: Foreign companies must track these timing differences as deferred tax assets or liabilities, disclosed in the financial statements filed with ACRA. The Fourth Edition of IRAS's e-Tax Guide (published 30 January 2026) provides authoritative guidance.

Singapore's Tax Environment

Despite compliance complexity, Singapore remains attractive for foreign investment:

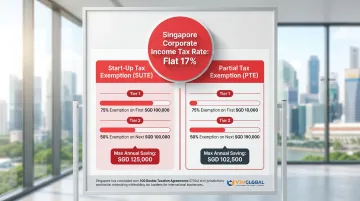

- Corporate Income Tax Rate: Flat 17% of chargeable income, applying to both local and foreign companies

- Start-Up Tax Exemption (SUTE): Available for the first three consecutive Years of Assessment for qualifying companies

- 75% exemption on first SGD 100,000 of chargeable income

- 50% exemption on next SGD 100,000

- Maximum exemption: SGD 125,000 per year

- Partial Tax Exemption (PTE): Available to all other companies

- 75% exemption on first SGD 10,000

- 50% exemption on next SGD 190,000

- Maximum exemption: SGD 102,500 per year

- Double Taxation Avoidance Agreements: Singapore has signed DTAs, limited DTAs, and Exchange of Information Arrangements with around 100 jurisdictions

ACRA Compliance Obligations for Foreign Companies

Foreign companies operating in Singapore must file annual financial statements with ACRA (Accounting and Corporate Regulatory Authority) covering:

- Listed companies follow applicable listing rules; unlisted companies follow standards-based requirements for head office statements

- Branch statements must cover the profit and loss account, assets used in Singapore, and liabilities arising from Singapore operations

- Active branches require audited financial statements; dormant branches may file unaudited statements

- Statements not in English must be filed with a certified English translation

Lease Accounting Disclosures: Financial statements must comply with applicable Accounting Standards (FRS or SFRS(I)), which include FRS 116 disclosure requirements:

- Information on ROU assets by class

- Maturity analysis of lease liabilities

- Total cash outflows for leases

- Additions, depreciation, and carrying amounts of ROU assets

- Interest expense on lease liabilities

- Significant leasing arrangements and restrictions

For foreign companies managing both Singapore and home-country reporting, VJM Global supports foreign entities with ACRA filing, deferred tax reconciliation, and FRS 116 disclosure across multiple jurisdictions — drawing on 30+ years of cross-border accounting experience.

Impact on Financial Ratios and Stakeholder Communication

The increase in reported assets and liabilities from lease capitalisation affects:

- EBITDA: Improves because operating lease expenses are replaced by depreciation (below EBITDA) and interest (below EBITDA or EBIT)

- Return on assets: Typically declines as ROU assets inflate the denominator

- Gearing and debt-to-equity ratios: Increase as lease liabilities are added to total debt

These are accounting presentation changes, not operational improvements. Foreign companies should proactively communicate with lenders, investors, and board members about the nature of these shifts — cash flows and underlying business performance remain unchanged.

Frequently Asked Questions

How do you account for a lease in accounting?

At the lease commencement date, the lessee records a Right-of-Use asset and a corresponding lease liability measured at the present value of future lease payments. The liability is reduced as payments are made and interest is accrued, while the ROU asset is depreciated over the lease term.

How does a 99-year lease work in Singapore?

Under FRS 116, long-term leases such as HDB flats and government land leases are recognised on the balance sheet as ROU assets and lease liabilities. The full 99-year lease term determines both the depreciation schedule for the ROU asset and the interest calculations on the lease liability.

What is the difference between SFRS(I) 16 and FRS 116 in Singapore?

Both standards have identical accounting requirements for lessees and are Singapore's equivalent of IFRS 16. The difference is that SFRS(I) 16 applies to companies following the IFRS-aligned Singapore Financial Reporting Standards (typically SGX-listed companies), while FRS 116 applies to companies following the domestic FRS framework.

Are short-term leases exempt from Singapore's FRS 116 requirements?

Yes. Leases with a term of 12 months or less (without a purchase option) can be elected out of balance sheet recognition and expensed on a straight-line basis instead. The same exemption applies to leases of low-value assets (approximately USD 5,000 or less when new).

How does lease capitalisation under FRS 116 affect a company's financial ratios?

Bringing leases onto the balance sheet increases both total assets and total liabilities, raising gearing and debt-to-equity ratios. EBITDA typically improves because lease payments shift from operating expenses to depreciation and interest charges below the EBITDA line. This reflects an accounting presentation change, not an operational one.

What are the ACRA filing requirements related to lease accounting for foreign companies in Singapore?

Foreign companies must include lease accounting disclosures (ROU assets, lease liabilities, maturity profiles, and key leasing arrangements) in audited financial statements filed annually with ACRA. Branches must also file accounts for both the Singapore branch and the overseas head office.