Introduction

UK businesses face their most significant financial reporting shake-up in over a decade. The Financial Reporting Council issued wide-ranging amendments to FRS 102 in March 2024, affecting an estimated 3.4 million businesses that report under UK GAAP. These changes become mandatory for accounting periods beginning on or after 1 January 2026.

The stakes are high. Revenue recognition now follows a five-step control-based model. Operating leases move onto the balance sheet. These aren't just accounting technicalities—they'll reshape reported profits, affect loan covenants, alter tax timing, and potentially restrict dividend capacity.

This guide breaks down what's changing, who's affected, and what finance teams must act on now—before the deadline creates real compliance pressure.

Key Takeaways

- FRS 102 overhaul takes effect 1 January 2026 for most UK entities not using full IFRS

- Revenue recognition shifts to five-step model; lease accounting goes on-balance-sheet

- Changes affect tax timing and EBITDA calculations

- Debt ratios and dividend capacity may also shift under the new rules

- Businesses must assess contract portfolios and lease agreements now—not in December 2025

- Transition relief available but requires early planning and stakeholder communication

What Is FRS 102 and Why Is It Changing in 2026?

The Standard and Its Scope

FRS 102 is the primary UK GAAP standard for entities that don't apply full IFRS, FRS 101 (reduced disclosure framework), or FRS 105 (micro-entities). Most medium and larger UK companies and groups use it, making it the backbone of UK financial reporting.

To keep the standard current, the FRC reviews FRS 102 every five years. This second periodic review targets closer alignment with two major international standards:

- IFRS 15 — revenue recognition

- IFRS 16 — lease accounting

According to PwC's technical analysis, the amendments are "broadly aligned to the principles of IFRS 15 and IFRS 16" but include practical relief for smaller preparers.

Timeline and Adoption Rules

Effective date: Accounting periods beginning on or after 1 January 2026. For calendar year-end companies, this means 2026 financial statements (filed in 2027) will be the first under the new rules.

Early adoption: Permitted, but only if all amendments are applied simultaneously—you can't cherry-pick the bits you like.

Micro-entity carve-out: FRS 105 micro-entities adopt the new revenue model but are exempt from on-balance-sheet lease accounting. For micro-entities, this keeps compliance costs lower and balance sheets simpler.

The New Revenue Recognition Rules: The 5-Step Model Explained

The revised Section 23 replaces the old risks-and-rewards approach with a control-based model. Revenue is now recognised when (or as) control of goods or services transfers to the customer, not when risks and rewards pass.

The Five Steps

Every revenue contract must be analysed through this framework:

- Identify the contract(s) with a customer – Determine which agreements create enforceable rights and obligations

- Identify distinct performance obligations – Break bundled contracts into separate deliverables

- Determine the transaction price – Calculate total consideration, including variable amounts

- Allocate the price to each obligation – Split revenue across multiple deliverables based on stand-alone selling prices

- Recognise revenue as each obligation is fulfilled – Record revenue when control transfers, either at a point in time or over time

Practical Implications

Two contract types will feel the most immediate impact:

- Bundled deals (products + services): Revenue must be split across each element using standalone values — for many businesses, this accelerates or delays recognition compared to the old rules.

- Long-term service agreements: SaaS providers, consultancies, and construction firms with milestone billing may need to defer revenue if control hasn't yet transferred at the billing date.

Example: A construction firm contracts to build a warehouse for £500,000, with payments at 25%, 50%, 75%, and completion. Under old FRS 102, the firm might recognise revenue when each payment milestone was reached. Under the new model, if the client controls the work-in-progress — the building sits on their land and they can't redirect it — revenue must be recognised over time as construction progresses. This can create a mismatch between cash received and profit recognised.

Variable Consideration: The "Highly Probable" Threshold

Variable revenue — bonuses, rebates, discounts, performance payments — can only be recognised if it's "highly probable" the amount won't reverse. According to PwC's technical analysis, this is a "higher threshold" than the previous "probable and capable of being measured reliably" test. In practice, this means more conservative revenue estimates upfront.

Transition Options for Revenue

Entities have two choices:

| Method | How It Works | Comparatives |

|---|---|---|

| Cumulative catch-up | Apply the new policy from 1 January 2026; record cumulative adjustment to opening retained earnings | Not restated |

| Full retrospective | Restate prior-year comparatives as if the new model always applied | Restated |

Practical expedients available:

- Skip restatement of contracts that began and ended in the same period

- Use actual transaction price (with hindsight) for variable consideration on completed contracts

- Reflect aggregate effect of all contract modifications before transition date

Most entities will opt for cumulative catch-up, avoiding the significant effort of restating multiple prior reporting periods.

The New Lease Accounting Requirements: Going On-Balance Sheet

This is the change that will hit balance sheets hardest. The old operating lease/finance lease distinction disappears for lessees.

The Fundamental Shift

Lessees must now recognise:

- A right-of-use (ROU) asset representing the right to use the leased asset

- A corresponding lease liability representing the obligation to make lease payments

This applies to virtually all leases—property, vehicles, equipment. ACCA explains the change eliminates off-balance-sheet operating leases, bringing UK GAAP in line with IFRS 16.

Exemptions

Two narrow carve-outs exist:

- Short-term leases: 12 months or less at commencement (no purchase option)

- Low-value assets: Laptops, tablets, small office furniture, mobile phones

Land, buildings, cars, vans, trucks, and production equipment don't qualify as low-value. If you lease premises or vehicles, they're going on the balance sheet.

Measurement at Inception

Lease liability: Present value of future lease payments, discounted using one of three permitted rates:

| Rate | Description | When to Use |

|---|---|---|

| Rate implicit in lease | Lessor's rate built into the lease | If readily determinable (rare) |

| Incremental borrowing rate (IBR) | Rate you'd pay to borrow for similar asset over similar term | IFRS 16 equivalent |

| Obtainable borrowing rate (OBR) | Rate you'd pay to borrow an amount similar to total undiscounted lease payments | New FRS 102 simplification |

The OBR is unique to FRS 102 and designed for smaller entities without dedicated treasury teams.

ROU asset: Equals lease liability plus any prepaid rent, initial direct costs, or restoration obligations, minus lease incentives received.

P&L Impact

The P&L treatment changes significantly under the new model:

- Old model: Single operating lease expense (rent), spread evenly over the lease term

- New model: Depreciation of ROU asset (straight-line) plus a finance charge on the lease liability (effective interest method)

This front-loads costs — early lease years carry higher total expense than under the old model. BKL notes that EBITDA will mechanically increase, because rent (an operating cost) becomes depreciation and interest — both sitting below the EBITDA line.

Critical point: EBITDA rises without any change in underlying cash flows. Boards and lenders need to understand this is presentational, not operational improvement.

Transition Options for Leases

Unlike revenue, FRS 102 does not permit comparative restatement for leases. The cumulative effect hits opening retained earnings at 1 January 2026. Two practical options ease the transition:

- Standalone entities: Calculate ROU assets and lease liabilities from scratch using the permitted discount rates

- Group subsidiaries: If your parent already applies IFRS 16, you can elect to use the parent's IFRS 16 carrying amounts as opening balances — no recalculation required

Other Notable Changes in the 2026 FRS 102 Amendments

Beyond revenue and leases, the 2026 amendments include several targeted updates across specific accounting areas:

Supplier finance arrangements (Section 7): New disclosures required for reverse factoring and similar arrangements—terms, carrying amounts, payment date ranges. This took effect 1 January 2025, one year ahead of the main package. If you haven't reviewed this yet, check compliance immediately.

Fair value measurement (Section 2A): Aligned with IFRS 13, updating definitions of markets, treatment of transaction costs, and valuation techniques.

Business combinations (Section 19): New guidance on identifying the accounting acquirer when a "Newco" is formed, and distinguishing contingent consideration (part of purchase price) from remuneration (employee cost).

Software capitalisation (Section 18): Clarifies when software integral to hardware (such as building management systems) must be treated as tangible PPE rather than an intangible asset.

Section 1A small entities: Material (not "significant") accounting policies must be disclosed. New disclosure requirements for going concern uncertainties, provisions, share-based payments, deferred tax, and dividends. These changes affect annual accounts disclosures directly, so treat them with the same rigour as the main package.

FRS 105 revenue carve-out: Micro-entities adopt the five-step revenue model but keep old lease accounting. Confirm your entity classification before scoping transition work.

The FRC published updated factsheets in November 2024 covering each of these changes in detail — essential reading for preparers.

How These Changes Could Impact Your Business Beyond Accounting

Tax Timing Effects

Changes in when revenue is recognised or how lease costs are presented can shift taxable profit between periods. While total tax paid may not fundamentally change over the life of a contract or lease, timing matters.

If transition creates a debit to retained earnings (revenue previously recognised now deferred), that's potentially a tax deduction in 2026. If it creates a credit (revenue accelerated), that's taxable income.

KPMG notes that Finance Act 2019 spreading rules are expected to apply to lease transitional adjustments, spreading them over the weighted average remaining lease term rather than hitting year one in full.

Corporate Interest Restriction (CIR): If your group's net tax interest expense exceeds £2 million annually, new lease finance charges will affect tax-EBITDA and interest restriction calculations, potentially creating deferred tax assets.

HMRC guidance: At time of writing, HMRC had not published a specific Revenue & Customs Brief on FRS 102 2026 transitions. The expectation is that existing IFRS 16 treatment (Business Leasing Manual BLM 51000) will extend to FRS 102 lessees. Consult a tax adviser before filing.

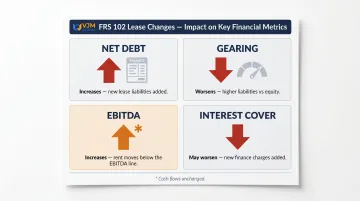

Financial Ratios and Loan Covenants

Bringing operating leases onto the balance sheet mechanically increases reported debt. For businesses with significant property or fleet leases, this can be material.

Metrics affected:

- Net debt: Increases (new lease liabilities added)

- Gearing: Worsens (higher liabilities vs equity)

- EBITDA: Increases (rent moves below the line)

- Interest cover: May worsen (new finance charges in denominator)

Covenant risk: If loan agreements calculate leverage as Net Debt/EBITDA or require gearing below a threshold, the FRS 102 changes could trigger technical breaches—even though underlying cash flows haven't changed.

Action required: Review loan documentation now. Engage lenders proactively to agree whether covenants will be calculated on frozen GAAP (old basis) or new GAAP (adjusted basis). ICAEW warns that entities should "seek waivers or revisions before the first reporting date."

Distributable Reserves and Dividend Capacity

Distributable reserves are calculated using "realised profits" under the Companies Act 2006. Transition adjustments to retained earnings could affect dividend capacity.

If the new revenue model defers previously recognised revenue, opening retained earnings fall on 1 January 2026. For businesses where reserves are already tight, this could restrict or eliminate dividend headroom.

ICAEW TECH 02/10 provides authoritative guidance on realised profits, but no specific supplement for FRS 102 2026 has been published yet. Seek professional advice before declaring dividends in 2026.

Stakeholder and Commercial Implications

The knock-on effects extend into commercial agreements and stakeholder relationships:

- Management bonuses: If tied to EBITDA or revenue targets, FRS 102 changes could artificially inflate or deflate payouts — review and restate targets where needed.

- Business valuations: EBITDA multiples will shift as a direct result of the new standard; buyers and investors need a clear explanation of the new basis.

- Investor communications: Disclose that EBITDA increases are presentational, not operational, to avoid misleading stakeholders.

What UK Businesses Should Do Now to Prepare

Step 1: Conduct a Thorough Impact Assessment

Don't wait until Q4 2025. Start now.

Revenue contracts: Identify all multi-year, milestone-based, or bundled contracts. Ask:

- Does the contract contain multiple performance obligations?

- Is any consideration variable (bonuses, rebates, penalties)?

- When does control transfer—at a point in time or over time?

Lease agreements: Build a complete lease inventory—property, vehicles, equipment. Capture:

- Lease term and remaining payments

- Discount rate to use (implicit, IBR, or OBR)

- Whether short-term or low-value exemptions apply

Quantify the financial impact before transition. Model opening balance sheet adjustments, P&L changes, and ratio effects.

Step 2: Update Systems and Processes

The new standards demand more granular data.

Contract tracking: You'll need to track performance obligations separately, allocate transaction prices, and monitor satisfaction over time. Spreadsheets may not scale.

Lease schedules: Calculate and track ROU assets and lease liabilities, including depreciation and finance charges. Many mid-market accounting systems lack dedicated lease modules—add-on tools or manual schedules may be required.

Software updates: Check whether your accounting software has been updated for FRS 102 2026. If not, contact your vendor or consider alternatives.

Step 3: Communicate Early with Stakeholders

Once your systems are in order, turn to the people who rely on your numbers. Each stakeholder group has different concerns—address them before accounts are filed.

Lenders: Discuss covenant treatment early. Agree frozen-GAAP or new-GAAP calculations and seek waivers or amendments if necessary.

Auditors: Engage early. Complex judgements around discount rates, performance obligations, and transition elections require audit review.

Investors and boards: Prepare briefing materials explaining the changes, particularly the mechanical EBITDA increase and balance sheet expansion.

Tax advisers: Model corporation tax cash flow impacts, particularly for transitional adjustments and quarterly instalment payments.

If internal resource constraints make any of these steps difficult, outside support is worth considering early. VJM Global has worked with 250+ UK businesses on financial reporting and compliance, and can help assess transition impacts, prepare stakeholder briefings, and keep filings on schedule.

Frequently Asked Questions

Is FRS 102 changing?

Yes. The FRC published amendments in March 2024 following its second periodic review. Changes are mandatory for accounting periods beginning on or after 1 January 2026, covering revenue recognition, lease accounting, and several other areas.

Does FRS 102 apply to small companies?

Yes — small companies can use Section 1A of FRS 102, which allows simplified disclosures. FRS 102 applies broadly to UK entities not using full IFRS, FRS 101, or FRS 105; micro-entities fall under FRS 105 instead.

What is the effective date for the 2026 FRS 102 amendments?

Accounting periods beginning on or after 1 January 2026, with early adoption permitted provided all amendments are applied simultaneously. One exception: supplier finance disclosures carried an earlier effective date of 1 January 2025.

How does the new lease accounting change affect a company's balance sheet?

Most leases previously classified as operating leases must now be recognised on the balance sheet. This means recording a right-of-use asset and a corresponding lease liability, increasing both total assets and total liabilities reported.

Will the FRS 102 changes affect my corporation tax liability?

Your overall corporation tax liability is unlikely to change significantly, but the timing of when tax falls due may shift as revenue recognition and lease cost profiles change. Businesses should consult a tax adviser about transitional adjustments.

Does the new on-balance-sheet lease model apply to micro-entities under FRS 105?

No. The lease accounting change does not apply to FRS 105 micro-entity reporters—their lease treatment remains unchanged. However, FRS 105 does adopt the new five-step revenue recognition model.